Where we are

2024 has been a significant year for momentum in Indigenous economic reconciliation. The mainstreaming of Indigenous equity ownership in major projects has been a long-sought goal. Significant strides include:

The final investment decision on the first Indigenous-owned LNG facility, Cedar LNG in B.C.

The sale and purchase agreement completed by the Nisga’a Nation on Ksi Lisims LNG in B.C.

The continued expansion of the largest Indigenous-led energy project in Ontario, Wataynikaneyap Power.

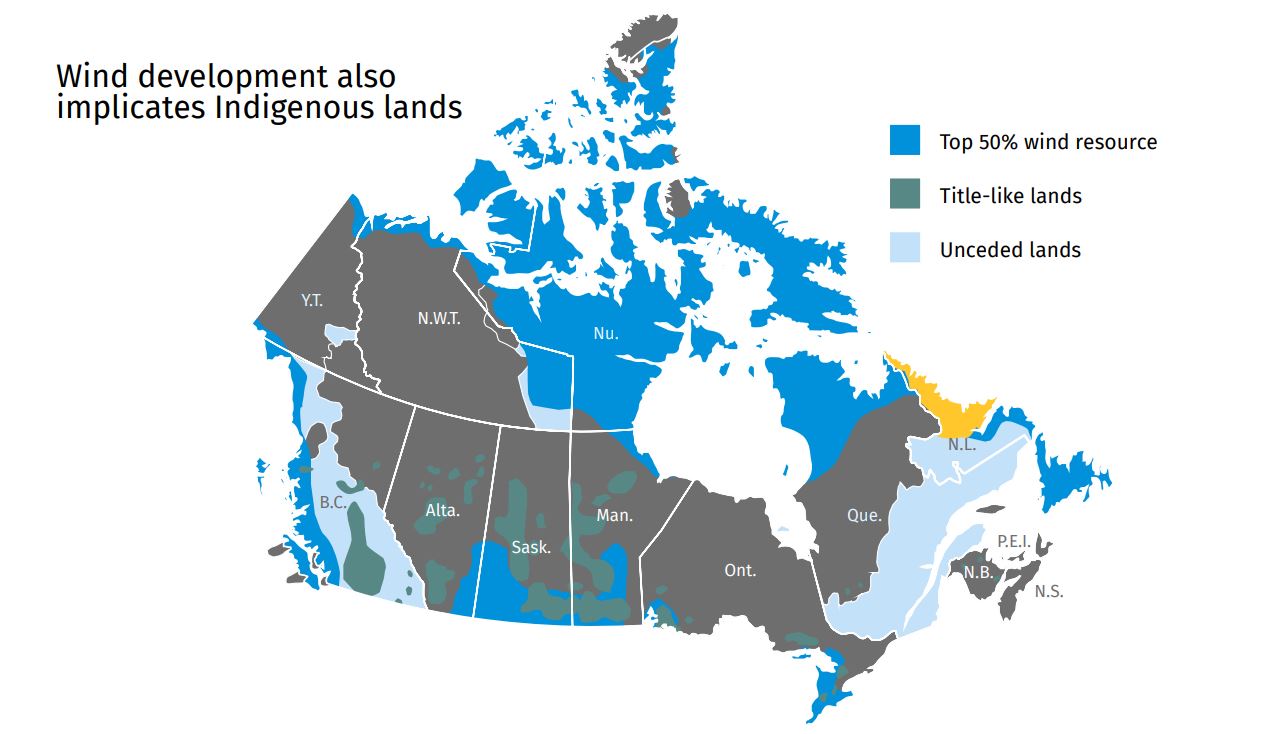

The announcement of a new, Indigenous-owned wind energy project—Seven Stars Energy—which is expected to be the largest in Saskatchewan.

Enabling meaningful Indigenous economic participation is now the status quo, and it’s incumbent on both governments and the private sector to advance proactive Indigenous participation. It is important to get this right for Canada—to grow the Indigenous economy, enable free, prior and informed consent for project development, and provide investor certainty.

Both provincial and federal governments are starting to catch up. BC Hydro announced the first competitive power bid in 15 years that mandated a minimum 25% Indigenous equity ownership requirement. Ontario recently announced its largest competitive energy procurement with the scoring expected to continue incentivizing (but not mandating) Indigenous participation1. All SaskPower renewable projects require a minimum of 10% Indigenous ownership.

And, after years of advocacy from both outside and within governments, three Indigenous loan guarantee programs were announced this year – one federal, and one in B.C. and Manitoba. These programs, if effectively implemented, will provide access to capital for Indigenous Nations seeking equity partnerships in major projects. Direct equity participation can enable greater economic self-determination by going beyond the traditional structures of impact-benefit agreements and employment, procurement, and contracting covenants. In some cases, it gives governance rights on projects that directly impact Nations. With existing access to capital support through provincial loan guarantee programs and federal Crown corporations, the next few years present a significant opportunity to advance meaningful progress on Indigenous economic reconciliation and equity ownership across the country.

Canada is amid an energy transition—which is both a climate and economic imperative. The road to Net Zero goes through Indigenous territory as our previous report 92 to Zero underscored. Indigenous ownership, participation and partnerships are now table stakes when advancing important resource and energy projects. Through financial and non-financial partnerships, early and deep Indigenous involvement in major project development can be a made-in-Canada model for inclusive economic growth as proactive relationship building is prioritized between Indigenous Nations, governments, and the private sector.

How we got here

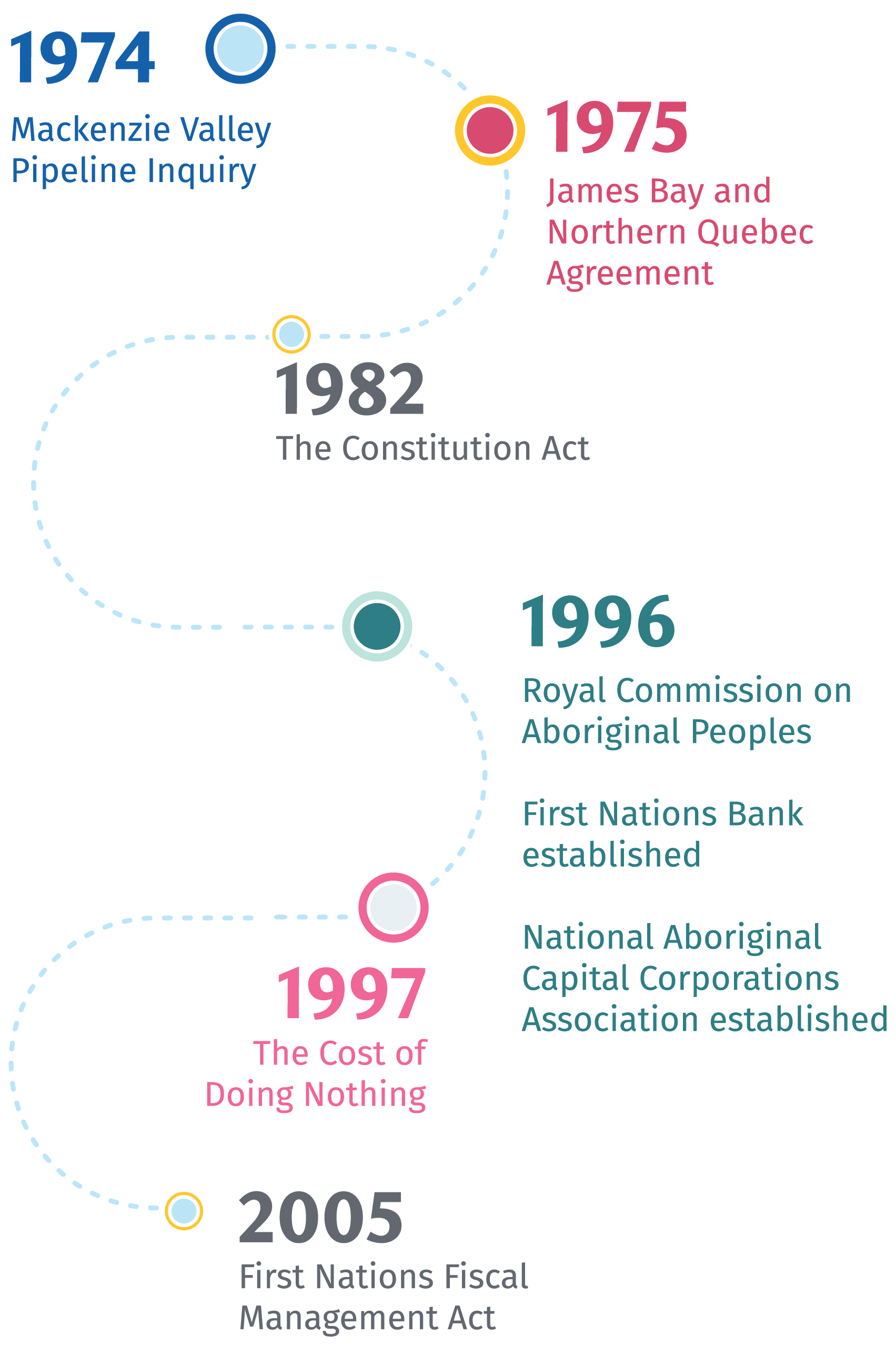

The story of Canada is one of the Indigenous Nations that have occupied these lands and waters before all settlers. The Canadian government (personified through the Crown) recognized their independence, autonomy, and nationhood through treaties and agreements including the Tawagonshi Treaty (Two Row Wampum Treaty) of 1613, the Hudson’s Bay Charter of 1670, and the Royal Proclamation of 1763. Canada as a country and a concept has been and continues to be shaped by its relationship with its First Peoples. These agreements and documents recognize Indigenous rights and titles, but the Supreme Court of Canada has also recognized that they only express and affirm what already exists—that Indigenous Nations have stewarded Canada since time immemorial2.

The Canadian government pursued colonization through a range of administrative, legal and other means (including, but not exclusively, through violence). Following the conclusion of the process of Confederation in 1867, the Canadian government consolidated various pieces of legislation relating to Indigenous peoples in the form of the first Indian Act (1876), marking the shift in federal policy from mutuality to assimilation. Post-Confederation historic treaties signed with First Nations were sometimes done so under duress, or were implemented in a manner that breached the terms and spirit of the treaty relationship.

Following the Red River Resistance, the Canadian government often removed members of the Métis Nation from the lands they had been living on to give it to settlers and in some instances, offered scrip—titles to land that were either untenable for agriculture and hunting or bought out by unscrupulous speculators at a significant discount. The Inuit faced similar dispossession with resource extinguishment due to the whaling industry and forced relocation to the High Arctic. These are only some examples of the direct and indirect impacts of colonialism that First Nations, Inuit and Metis Nations have faced over history.

Indigenous Nations have found themselves increasingly dislocated from their legal orders, governance and economic systems through a process of dispossession of their lands, waters and resources.3 Despite this marginalization, Indigenous Nations have advocated for, and advanced legal, political and governance rights, including having Aboriginal rights and titles entrenched in the Constitution. Being able to participate fully in the mainstream Canadian economy while maintaining sui generis rights continues to be an important priority for Indigenous peoples and is an important aspect of the pathway toward economic self-determination and true reconciliation.

Indigenous Nations continue to face significant institutional and legal barriers to raising affordable capital to enable entrepreneurship and participation. This includes the inability to collateralize reserve land due to Section 89 of the Indian Act for First Nations, the inability to access federal funding programs for the Métis Nation, and the difficulty of securing project funding in remote, rural areas for the Inuit.

Major strides have already been made, including the passage of the First Nations Fiscal Management Act, the creation and devolution of powers to territorial governments and the creation of Indigenous-led financial institutions. Further strides must be made to unlock Indigenous economic potential and create the pathway for true economic reconciliation.

Timeline of key events

The story today

When Indigenous Nations consider major project participation, they often face a combination of institutional, legal and economic barriers that have led to many (but not all) Indigenous Nations to build a balance sheet, deal history, or internal capacity. Access to affordable capital that enables Nations that reduce the cost of capital and safeguard Indigenous assets remains a challenge. This is because of a combination of legal and institutional barriers outlined above, as well as network effects and a lack of awareness on the part of the private sector on the benefits of proactive Indigenous participation.

This gap is particularly evident in opportunities where Indigenous Nations may wish to have an ownership stake in energy and natural resource projects on their territories. Indigenous ownership is now a leading model to align interests and advance project development in a timely way by prioritizing Indigenous-corporate relationships, incorporating Indigenous values and priorities, and potentially streamlining regulatory processes4.

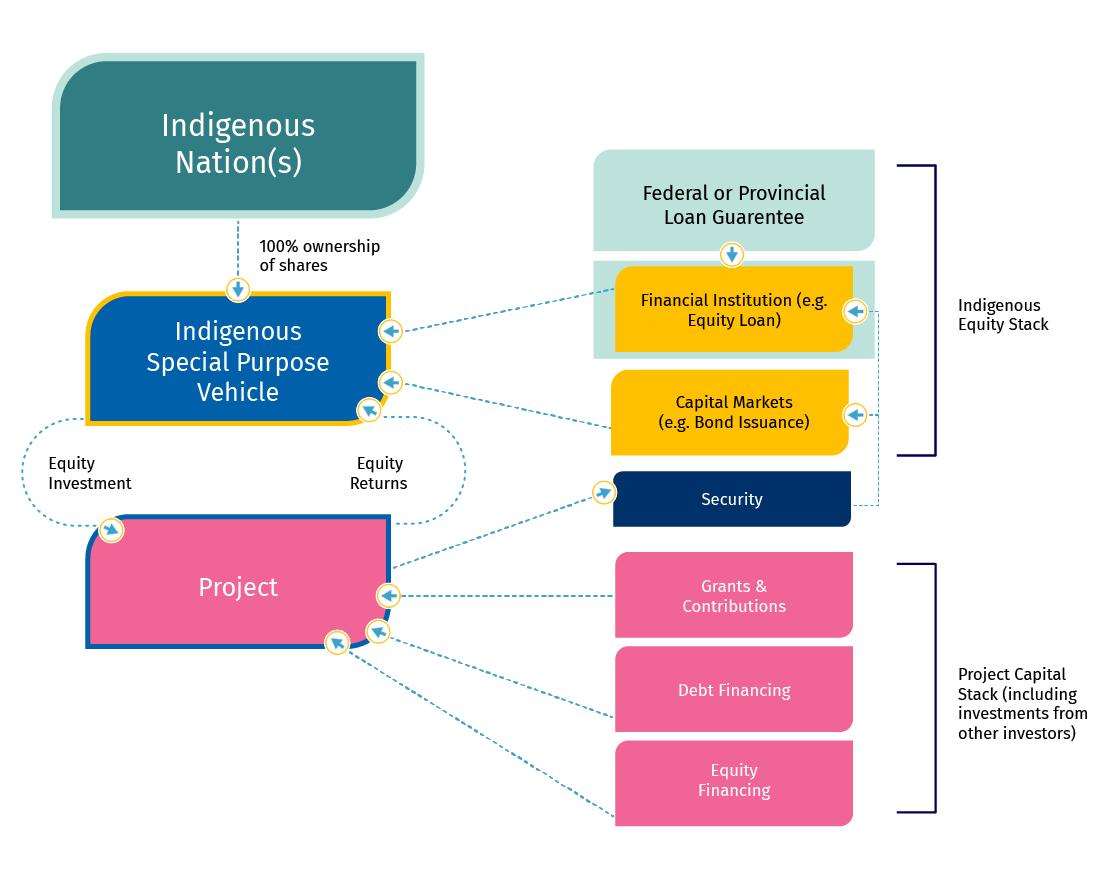

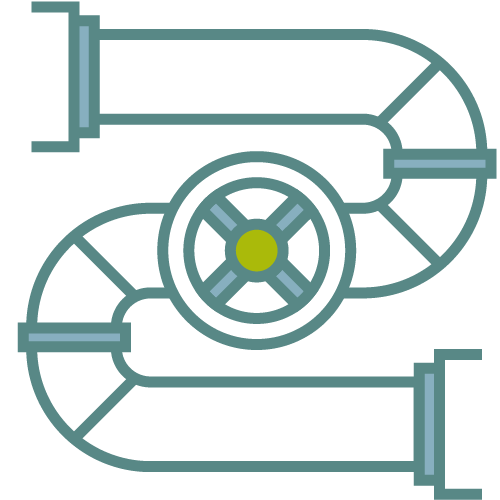

What is a loan guarantee and how are they structured?

A loan guarantee is a contractual agreement to repay a debt provided by a third-party lender such as a bank, when the borrower can no longer pay (i.e., “backstopping a loan”). For the lender, this can virtually eliminate the risk of economic loss. For Indigenous investors, equity loans without guarantees can be prohibitively expensive (i.e., the cost of the loan, if granted at all, is less than the cost of financing without a guarantee). Without guarantees, Indigenous investors are often faced with the scenario of an uneconomic cost of capital, accepting a much smaller equity position—or none at all—which are sub-optimal outcomes.

A loan guarantee facilitates the lending environment to fund the equity portion of a transaction, providing credit enhancement and liquidity support for Indigenous borrowers. Importantly, the use of limited partnerships and special purpose vehicles do not put Indigenous community assets at risk, as the project debt raised is non-recourse/limited recourse to equity partners. Use of a special purpose vehicle owned by Indigenous Nations, and generating distributions back to the community limit exposure of liabilities to the value of the initial equity investment made by a Nation.

Loan guarantee programs have emerged as a “brick in the wall”—a part of the solution to address the access to capital gap among other complementary tools. The figure below outlines an example of the ownership structure and the relationship between an Indigenous Nation and equity ownership in a project, in particular, where a loan guarantee may play a role.

The federal government along with the B.C. and Manitoba governments announced loan guarantee programs in 2024 on the heels of advocacy by Indigenous Nations and the private sector amid growing maturity in the public policy development process. These programs, if effectively deployed, could help close the gap in the substantial demand for Indigenous equity participation, estimated by the First Nations Major Projects Coalition to be approximately $45 billion over the next 10 years. Both the development and deployment of newly announced loan guarantee programs will benefit from existing models in Ontario, Alberta and Saskatchewan.

Project finance tools for advancing Indigenous ownership in major projects

These announcements are an important contribution to the set of tools available for Indigenous Nations to economically participate in resource and energy projects. As these programs are implemented, important considerations will include the risk mandate of a loan guarantee program, adequate capacity support to enable partnerships, robust governance to ensure decision-making and issuance of guarantees are undertaken commercially, and stacking with other guarantee programs and support. Priorities to pay attention to as these programs are being implemented will include:

Indigenous people must be supported to make free, prior and informed decisions on project participation. Partnerships across all Indigenous Nations—First Nations, Inuit and Métis—must be supported. Indigenous perspectives, leadership and talent recruitment, development and retention should also be prioritized when implementing loan guarantee programs.

Programs should support the widest scope of projects to maximize Indigenous economic opportunity as a first-order priority in addition to wider productivity gains to Canada.

Government financial support should be backed by a robust due diligence process. A path toward market sustainability is necessary, so Indigenous Nations can access capital on an equal footing with other market participants over the long term.

Time is of the essence. Individual project negotiations must move at the speed of trust, but the bureaucratic functions of the loan guarantee programs must move at the speed of business. This priority will have to be balanced with the need to have a robust due diligence process.

Existing loan guarantee programs continue to learn and develop new approaches to better enable Indigenous ownership and participation. For instance, how best to support Indigenous ownership in greenfield or pre-construction projects. New loan guarantee programs need to retain flexibility in the structuring and deployment of guarantees to develop and adopt best practices across both public and private sectors.

Risk mandate and project application

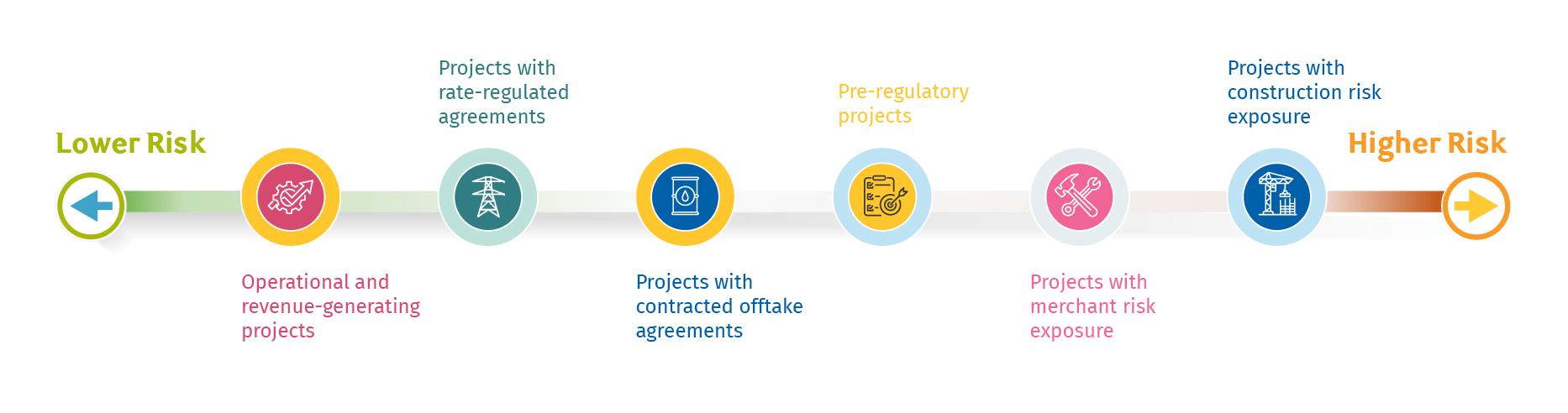

Projects that provincial and federal governments select to guarantee will depend largely on the risk mandate of the loan guarantee program. Generally, loan guarantee programs mandated to be low or zero-risk will primarily provide support for relatively low-risk sectors (such as rate-regulated or operational projects). A loan guarantee program with a more accommodative risk mandate could take

on earlier-stage projects in riskier sectors (such as those with more merchant risk exposure) and larger/smaller ticket sizes—facilitating the completion of net-new projects that would not have occurred without Indigenous economic participation. Figure 2 presents the notional risk across a range of possible sectors and project stages, ranging from low to high risk.

It is likely that loan guarantee programs, similar to many government funding programs, will start out relatively risk-averse. However, given the ability of governments (particularly the federal government) to absorb more risk, these programs should adopt an evolving, dynamic risk mandate as they gain expertise through “learning by doing.” For instance, annual risk mandate reviews can incorporate the inputs of Indigenous clients and private sector participants in guarantee programs to re-evaluate whether new, innovative approaches and sectors can be covered. The risk would entail multiple dimensions, including:

Although partial loan guarantees that do not cover the entire Indigenous equity loan may be preferred initially, guaranteeing up to 100% of the equity loan can enable a greater degree of Indigenous economic participation and returns on projects where previously infeasible.

A sector-agnostic approach is important, enabling Indigenous Nations to retain full say and determination on the types of projects that happen on their territory and broadening the positive impacts of Indigenous participation. The loan guarantee program should prioritize a mix of projects across a range of sectors and geographies

Loan guarantee programs will seek to minimize undue risk and a call on guarantees due to both fiscal and reputational risk. Over time, as loan guarantee programs demonstrate success, a wider range of considerations can include guaranteeing projects with a smaller ticket size and greenfield or pre-regulatory projects versus brownfield projects, have a range of risk exposure. Ensuring this mix will capitalize on the program opportunity to maximize Indigenous opportunity and enable investment into net-new projects that contribute to energy and economic goals.

A larger number of Nations in a deal may add complexity, and dilute returns and the equity stake for individual Nations, but it can provide positive multiplier effects. Nations with a greater degree of capacity can support Nations that are developing and building their own internal capacity. Facilitating relationship building across Nations, and with the private sector will be an important impact measure for loan guarantee programs.

A loan guarantee does not create a cash profile on a government’s public accounts, but a loan loss provision can set aside part of the cash requirement for a call on a guarantee. However, when a guarantee is issued, part of this provision would be “locked in” until the loan is repaid. Accounting for a diversity of loan durations (e.g. a mix of five, 10 and 15-year terms) can enable the program to recycle capital and issue new guarantees that would unlock a greater value of equity partnerships.

Additional structuring protections governments may consider to mitigate risk would include:

Indigenous Nations that can invest their own capital can create an equity buffer, which can mitigate risk and further reduce the cost of equity capital.

Loan guarantee programs must lower the barrier to entry, including onerous fees, but these fees can also be tailored to the specific risk profile of the guarantee.

These are standard contractual terms that can stipulate timely repayment of debt by directing cash flows toward debt repayment before distributions, and create a buffer to ensure that future issues can be cured through funds capitalized upfront and over time.

Often used in minority ownership positions, share buyback provisions obligate the majority partner (and often the operator) to re-acquire the Indigenous equity shares in the case of full default.

A standard aspect of commercial debt monitoring, post close due diligence can help address potential issues proactively and enable a government, proponents or financiers to step in prior to an issue being raised. Both commercial monitoring and relationship management with individual Indigenous Nations will be important.

The federal minister of finance has indicated that the government would look forward to seeing the program oversubscribed and a request to increase the funding beyond $5 billion. Indeed, one major project can take over the entire loan guarantee envelope. A larger guarantee envelop is a positive signal of the government’s commitment to enable greater Indigenous partnerships and meet the $45 billion potential.

Capacity

A combination of institutional factors and network effects may mean Indigenous Nations have varying degrees of relationships, know-how and deal history to build the commercial capacity to assess and negotiate deals. The degree of capacity may be variable based on the Indigenous Nation and the nature of the deal. Capacity support can be crucial to the success of access to capital tool that enables Nations to access appropriate commercial, legal and financial expertise to make the right decisions.

As a comparator that highlights the importance of capacity amongst other factors, the U.S. Tribal Energy Loan Guarantee Program created in 2005 issued its first loan guarantee in March 2024. The program’s slow progress may be attributable to multiple factors, but an important omission appears to be that it did not fund for capacity for Native American tribes to make informed decisions on the commercial and technical aspects of a deal.

The federal government has provided $3.5 million over two years to support capacity funding under the program. This is a start, but capacity funding must be more highly prioritized to ensure Indigenous Nations have the appropriate commercial, technical and legal expertise to make project participation decisions. Capacity is often further enabled through the fees charged on loan guarantees, which can be recycled into a capacity fund, alongside support by project proponents. The B.C. loan guarantee program has indicated that it will capitalize a capacity fund with $10 million. The Manitoba loan guarantee program has not indicated whether it will fund capacity.

Organizations such as the First Nations Major Projects Coalition have played an important role in supporting Nations build and consolidate internal commercial, technical and environmental capacity. Continued support of existing and new organizations will be a crucial success factor over the long run.

A positive trend that is Indigenous Nations is growing the number of Nations supporting each other in building capacity. Anecdotally, in deals with multiple Indigenous Nations involved, Nations with more experience and a greater degree of internal commercial or technical expertise often allocate their internal or external resources or contribute their relationships or past experience to support those Nations that are building this capacity.

Governance

Independent, arms-length administration has been a priority with existing programs, including in Ontario (managed through a Crown agency) and Alberta and Saskatchewan (managed through an arms-length corp.). Independence and autonomy enable decision-making to happen with minimal political interference, and generally, have enhanced credibility. Indigenous perspectives and inclusion must be a critical component in all governance structures. Key priorities in developing a transparent, inclusive and nimble governance model will include:

Indigenous leadership and representation across governance and decision-making bodies must be a priority and imperative, given the focus of these programs on Indigenous economic reconciliation and inclusion.

The focus should remain on assessing guarantees on apolitical criteria, including ensuring commercial viability and inclusivity, limiting the scope for political interference in the issuance of individual guarantees.

A corollary for loan guarantee programs to remain apolitical is ensuring the approval and decision-making processes prioritize speed. Approvals by an independent, arms-length board with representation across Indigenous leaders, government officials, and the private sector can expedite implementation and communications.

-

Part of deploying at speed is enabling, particularly at the federal level, a “single window” approach or coordinating efforts across federal and provincial loan guarantee programs to ensure appropriate service delivery to Nations.

Robust, commercially comparable due diligence criteria and evaluation processes must be developed to ensure loan guarantee decisions are made on the commercial and economic merits of the underlying project and loan guarantee.

Buy-in and transparency go hand in hand to bulwark the credibility and reputation of loan guarantee programs. Both a clear governance process and robust monitoring and reporting requirements will be required for Indigenous Nations and the private sector to understand how and why guarantee decisions are made.

Stacking

There are a range of organizations that provide financial support for Indigenous major project participation, notably provincial loan guarantee programs. Considerations that would enable better stacking with the aim of maximizing the economic opportunity of Indigenous ownership using the full weight of government resources include:

Offering a “single window” for Nations considering both provincial and federal guarantees.

-

This includes coordination and communication between officials, which is especially important in complex projects that require support across multiple organizations. The federal loan guarantee program has an opportunity to show leadership in this regard.

Aligned financing and contractual terms including fees, guarantee structure and flexibility in rules that enable Nations to tap into multiple financing “pots.”

For capacity grants—not restricting the number of sources Nations can access.

Organizations that provide both financing and capacity support include the provincial guarantee programs, the First Nations Finance Authority, the Canada Infrastructure Bank, Export Development Canada, Business Development Bank of Canada, Farm Credit Canada, and multiple provincial agencies that provide support towards Indigenous economic opportunity.

Future tools

Loan guarantees can be an effective tool—but are only a brick in the wall and not a silver bullet. Crowding in private investment and creating a path to market sustainability will be important.

Future considerations for governments as they consider expanding the toolkit may include:

Indigenous economic interests intersect with almost every sector in the economy including fisheries, agriculture, telecommunications, infrastructure, manufacturing, tourism, and others. Federal and provincial loan guarantee programs can start expanding support across multiple sectors, particularly beyond the energy and natural resources sectors where most of the focus has remained.

Guaranteeing project debt, albeit riskier, may be the next stage after a critical mass of support and private capital is available to guarantee equity. This would functionally on-lend the federal government’s credit rating to Indigenous borrowers, and provide a greater range of flexibility for banks to lend toward.

Providing 100%-plus guarantees can support Indigenous participation for projects in the pre-construction, pre-revenue generation phase. Similar to guaranteeing debt, this may be riskier, but if strategically employed in otherwise commercially viable projects, it can unlock meaningful, early Indigenous participation in projects, particularly in strategic sectors such as critical minerals.

In higher-risk sectors such as mining, particularly in some frontier critical minerals projects, Indigenous Nations may prefer to participate through a royalty or income stream. By creating an institutional structure to transfer part of the royalty revenue to Indigenous Nations, governments can incentivize participation in sectors such as mining or forestry (where the royalty is referred to as stumpage fees). Federal government action is called for here. Provincial governments in B.C. and Alberta amongst others already have resource-revenue sharing agreements.

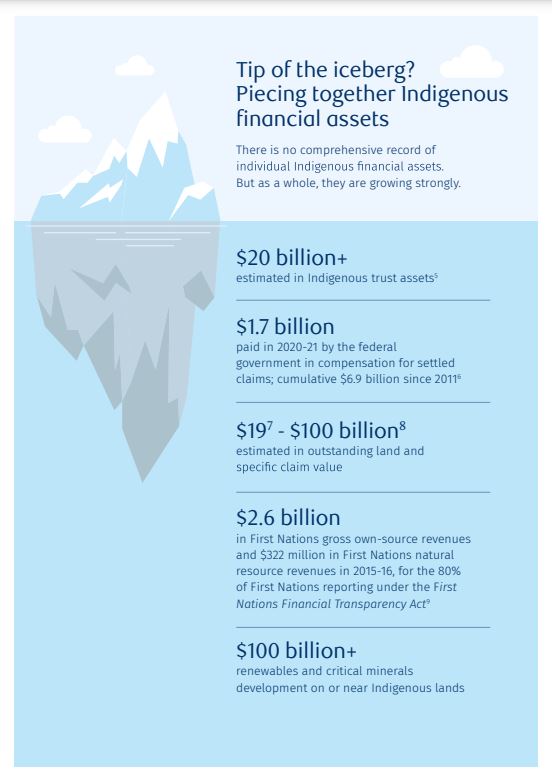

The growing wealth of Indigenous Nations includes an estimated $20 billion in trust assets and up to $100 billion in outstanding land and other claims. Pooling trust and investment assets through optional Indigenous-led institutions can help generate significant investment income as well as a vehicle to further advance participation and ownership.

An Indigenous Development Bond, akin to development bonds issued by emerging economies and multilateral institutions, can support financing of Indigenous-led projects. This would build on the existing success of the First Nations Finance Authority’s pooled lending and bond issuance program. This instrument would require consensus on bond issuance standards.

Building on the work of the Canadian Sustainability Standards Board and the federal sustainable investment guidelines, integrating Indigenous perspectives and considerations to investment standards can be an additional tool to drive investment to Indigenous-led projects and organizations.

An Indigenous-led development finance institution that consolidates debt, equity and grant instruments could offer a comprehensive set of tools to durably finance projects and businesses. The model for such an institution would be akin to community development banks, capitalized by both public and private sectors, rather than multilateral development banks with votes allocated by share capital.

The private sector is developing innovative structures to crowd in Indigenous participation and inclusion in major projects, including:

-

Breaking out lower-risk, revenue-generating elements of a larger project and facilitating Indigenous ownership—often elements that outlive the life of a single project (e.g. transmission lines or toll roads).

-

Post-construction options for Indigenous ownership, wherein the option can be exercised by Indigenous Nations to purchase an equity stake upon project completion.

-

Minimum annual payments to mitigate the potential downside and protect Nations from undue risk when a project goes through periods of no revenue.

-

Share buybacks upon project failure to commit to a set price to repurchase equity stakes by the project proponent if the project fails to be completed.

-

Negotiating Indigenous governance rights even in cases of minority equity positions through a separate share-class structure to recognize Indigenous owners sit in a unique position apart from other commercial participants.

-

Co-investing with institutional investors, particularly, with co-investors that can deploy large sums of capital over long durations, both in individual major projects and by bundling smaller opportunities through joint ventures.

-

Proponent guarantees or contractual supports: Proponents may seek to provide their loan guarantees or other forms of contractual support to enable Indigenous participation, particularly in riskier projects. This may be balanced by a higher equity sale price.

A proactive, relationship-focused and trust-based approach for Indigenous partnerships is now necessary in both public and private sectors. Advancing economic reconciliation through meaningful partnerships is both a moral and economic imperative – presenting an opportunity to grow out collective prosperity as a country.

For more, go to rbc.com/en/thought-leadership/

Download the Report

Contributors:

Varun Srivatsan, Director, Policy and Strategic Engagement

Rajeshni Naidu-Ghelani, Managing Editor, Economics & Thought Leadership

Caprice Biasoni, Graphic Design Specialist

Finance

Finance Electricity Infastructure

Electricity Infastructure  Labour force

Labour force Supply Chains

Supply Chains

Asia, on the other hand, will have a harder time turning away from natural gas. As one of the world’s biggest LNG importers, Japan is alarmed by its dependence on Russian and Middle Eastern countries as well as new export limits proposed by major LNG supplier Australia. It’s encouraging the development of nuclear energy, hydrogen and natural gas as part of this year’s G7 agenda.

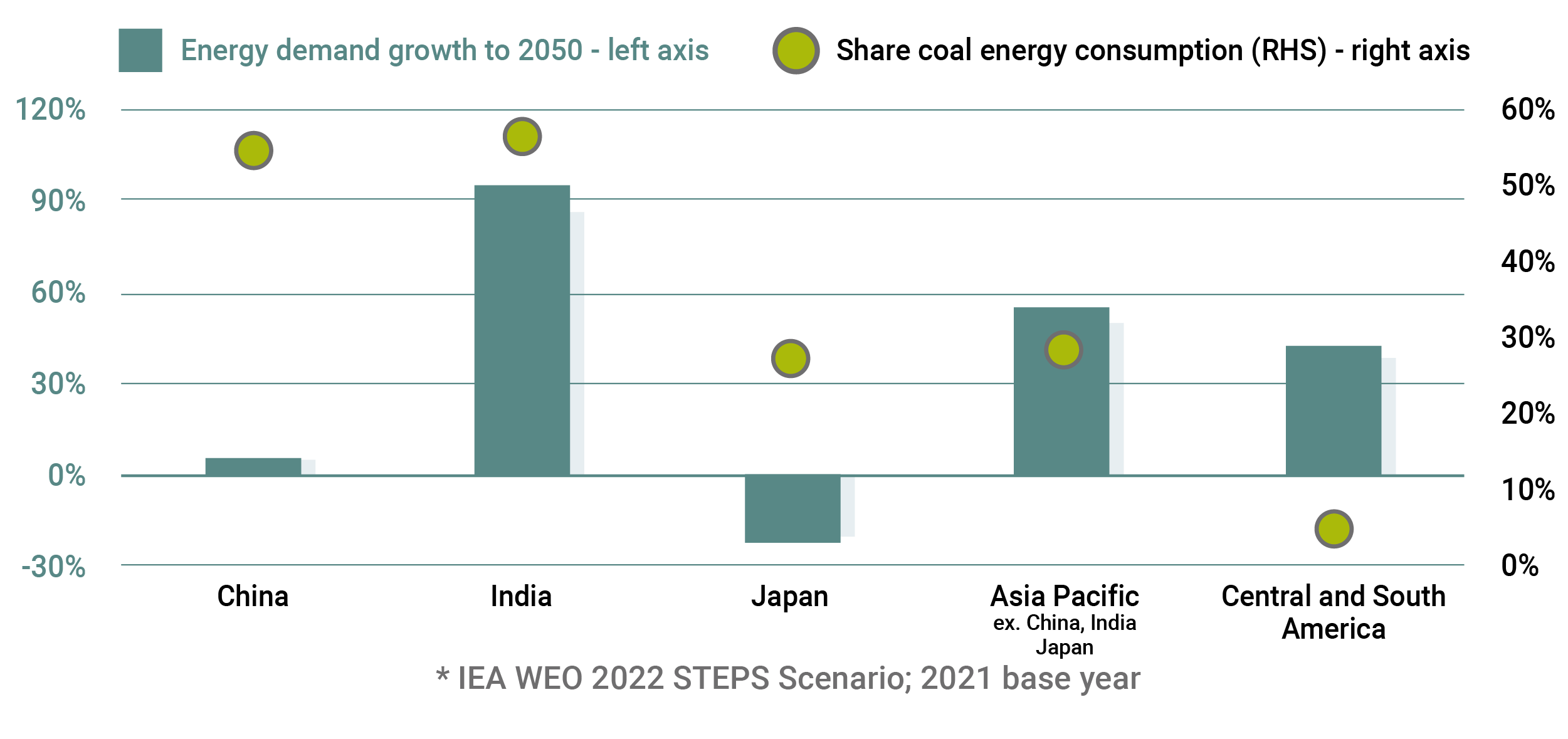

LNG will also remain an essential fuel in China, India and other populous countries of South Asia and Southeast Asia as these countries seek to meet growing energy demand while reducing a strong reliance on coal to meet climate commitments. China, India and Southeast Asia will see gas demand grow by around 44% by 2050 in the International Energy Agency’s base case scenario. LNG would take the bulk of the growth with declining local pipeline-based production.

But it’s hardly a full-blown bull case for gas. Stunned by last year’s five-fold jump in LNG prices, many Asian countries raised their coal consumption, while others pivoted to renewables, especially as the economics of switching directly from coal to clean energy in Asia improved dramatically. Non-emitting energy rollout may take a while to gain traction in Asia, but it’s still a cloud hanging over the long-term gas outlook.

Asia, on the other hand, will have a harder time turning away from natural gas. As one of the world’s biggest LNG importers, Japan is alarmed by its dependence on Russian and Middle Eastern countries as well as new export limits proposed by major LNG supplier Australia. It’s encouraging the development of nuclear energy, hydrogen and natural gas as part of this year’s G7 agenda.

LNG will also remain an essential fuel in China, India and other populous countries of South Asia and Southeast Asia as these countries seek to meet growing energy demand while reducing a strong reliance on coal to meet climate commitments. China, India and Southeast Asia will see gas demand grow by around 44% by 2050 in the International Energy Agency’s base case scenario. LNG would take the bulk of the growth with declining local pipeline-based production.

But it’s hardly a full-blown bull case for gas. Stunned by last year’s five-fold jump in LNG prices, many Asian countries raised their coal consumption, while others pivoted to renewables, especially as the economics of switching directly from coal to clean energy in Asia improved dramatically. Non-emitting energy rollout may take a while to gain traction in Asia, but it’s still a cloud hanging over the long-term gas outlook.

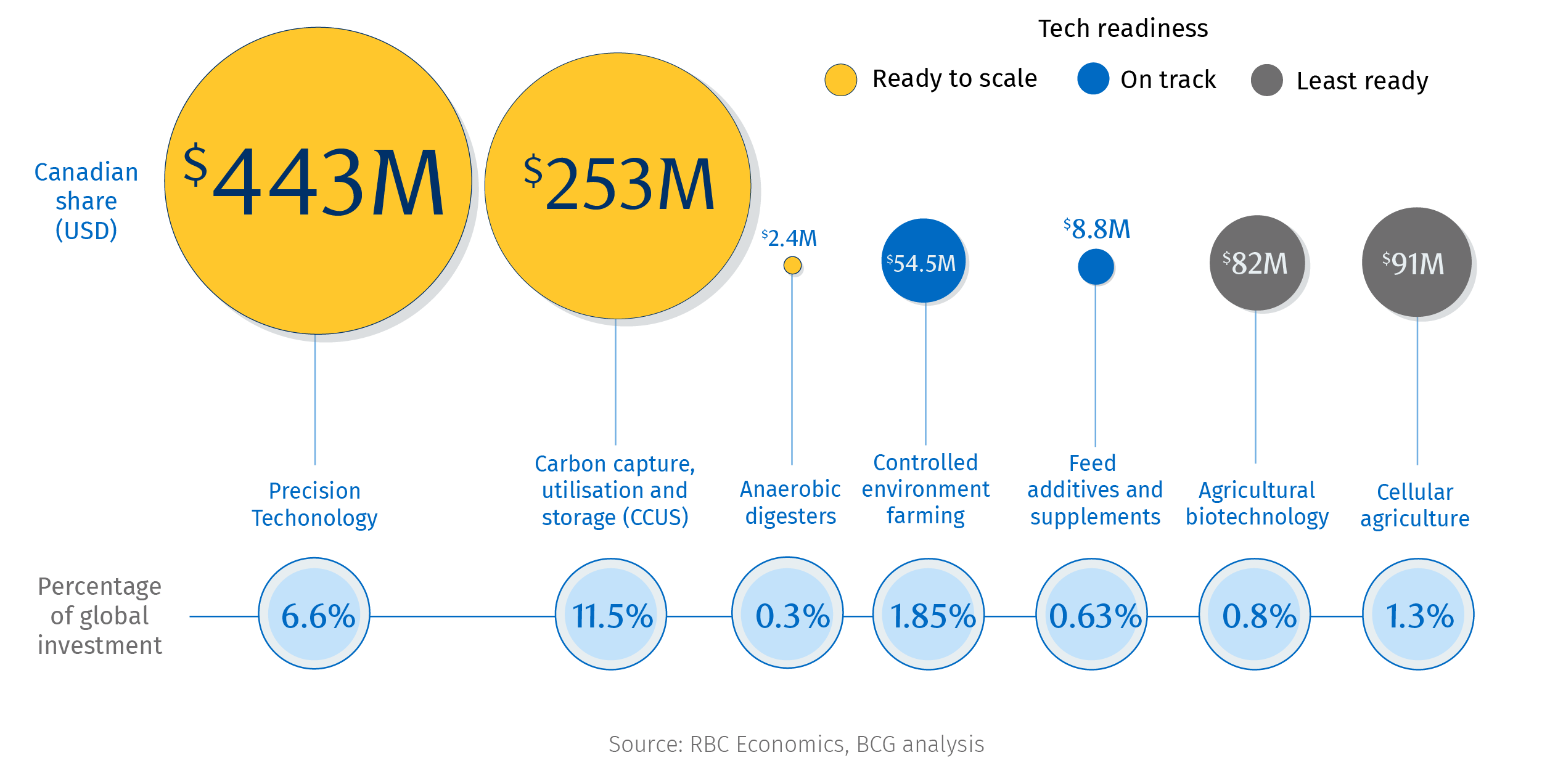

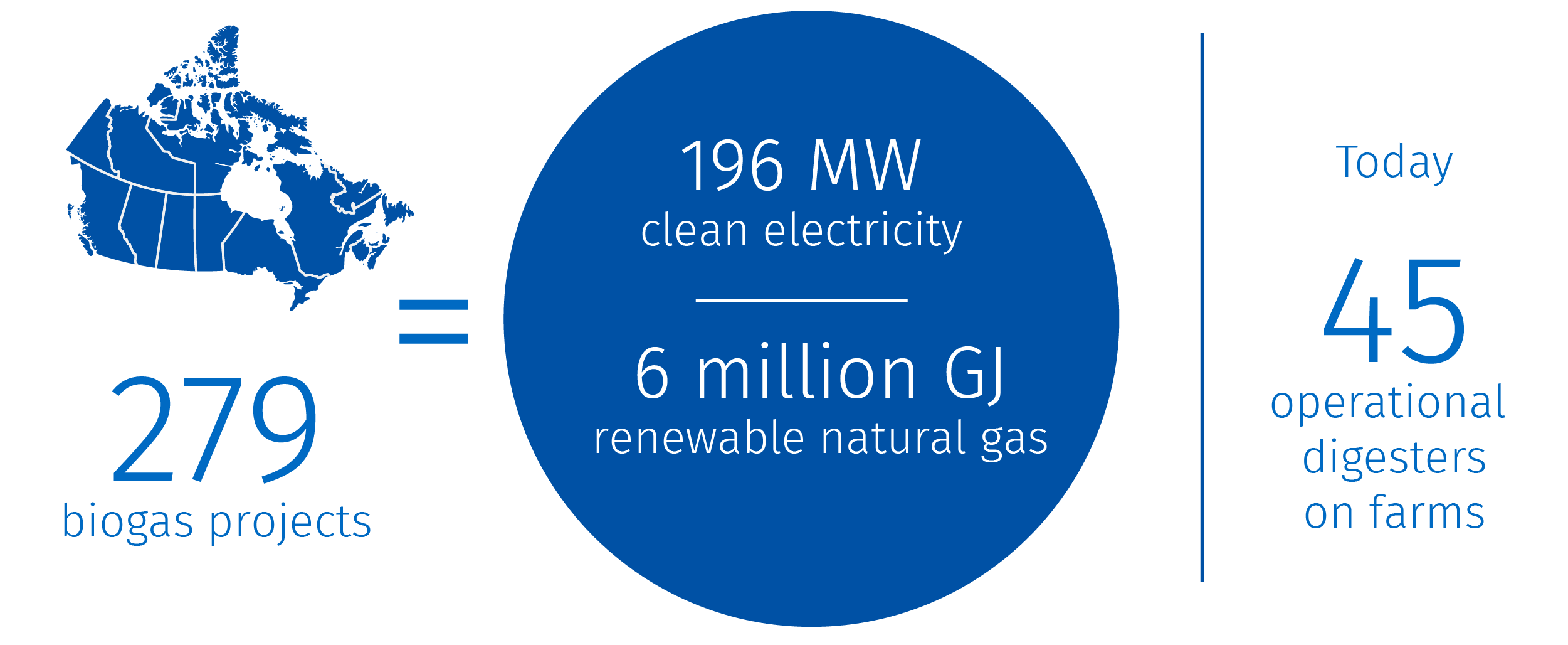

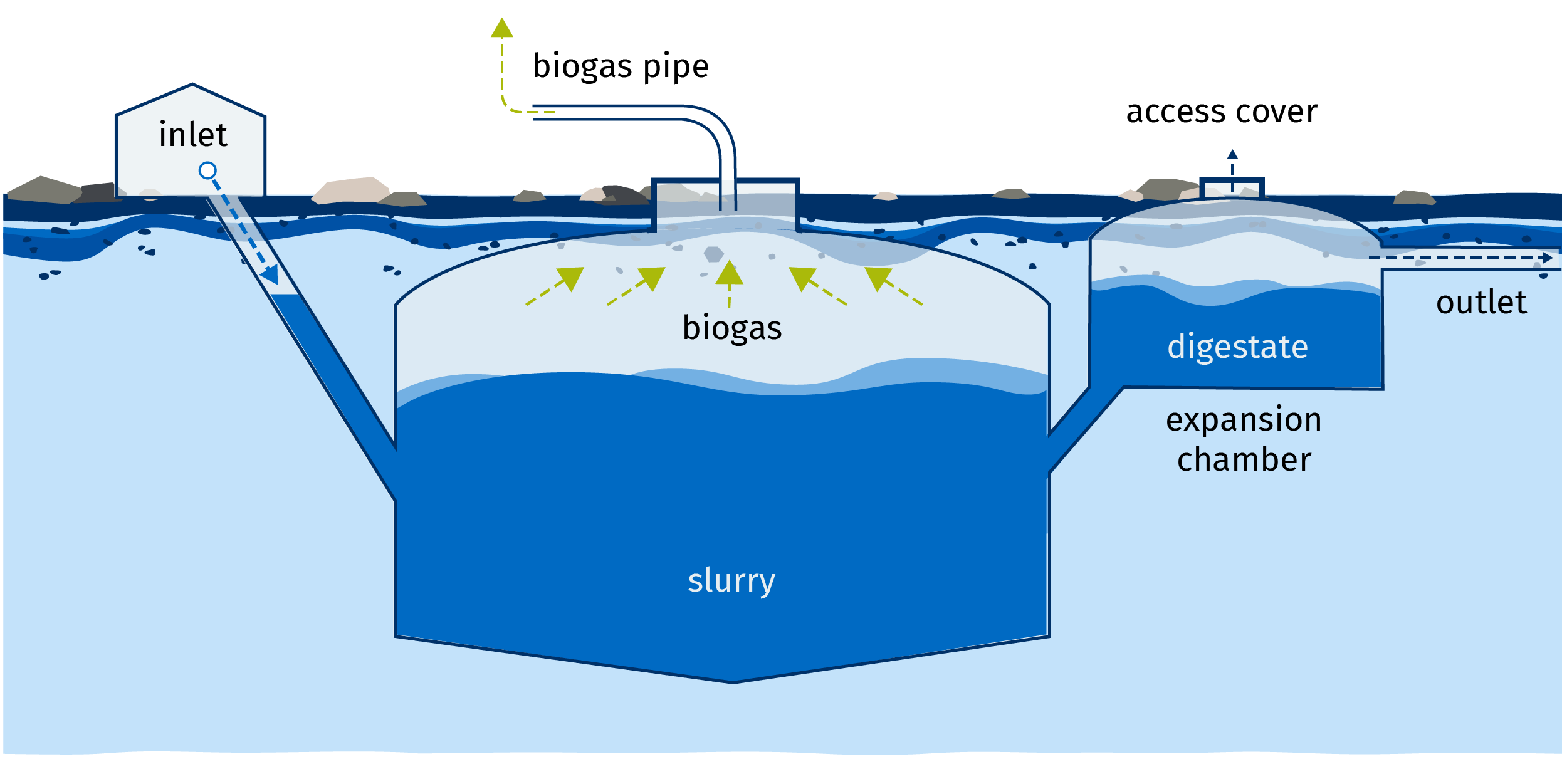

In Canada, biogas development (including anaerobic digesters) has been driven by provincial energy and waste management policies. There is huge opportunity for growth, especially in agriculture, where crop residues and animal manure make up two-thirds of Canada’s easily available biogas resources. In addition to on-farm plants, community digesters have been touted as a pathway to growth, where their use and costs can be split among multiple farms and potentially even local municipalities.

The Challenges

But investment and development thus far is anemic, with just 29 projects underway. (Data on investments in anaerobic digester development is also quite sparse). The high costs for building these facilities (in the tens of millions per facility, depending on the size) are a barrier. While there are significant tailwinds for the industry, including from government policies like the clean fuel regulations and offset markets, greater demand for biofuels and derisking structures like power purchase agreements will also need to be developed.

In Canada, biogas development (including anaerobic digesters) has been driven by provincial energy and waste management policies. There is huge opportunity for growth, especially in agriculture, where crop residues and animal manure make up two-thirds of Canada’s easily available biogas resources. In addition to on-farm plants, community digesters have been touted as a pathway to growth, where their use and costs can be split among multiple farms and potentially even local municipalities.

The Challenges

But investment and development thus far is anemic, with just 29 projects underway. (Data on investments in anaerobic digester development is also quite sparse). The high costs for building these facilities (in the tens of millions per facility, depending on the size) are a barrier. While there are significant tailwinds for the industry, including from government policies like the clean fuel regulations and offset markets, greater demand for biofuels and derisking structures like power purchase agreements will also need to be developed.

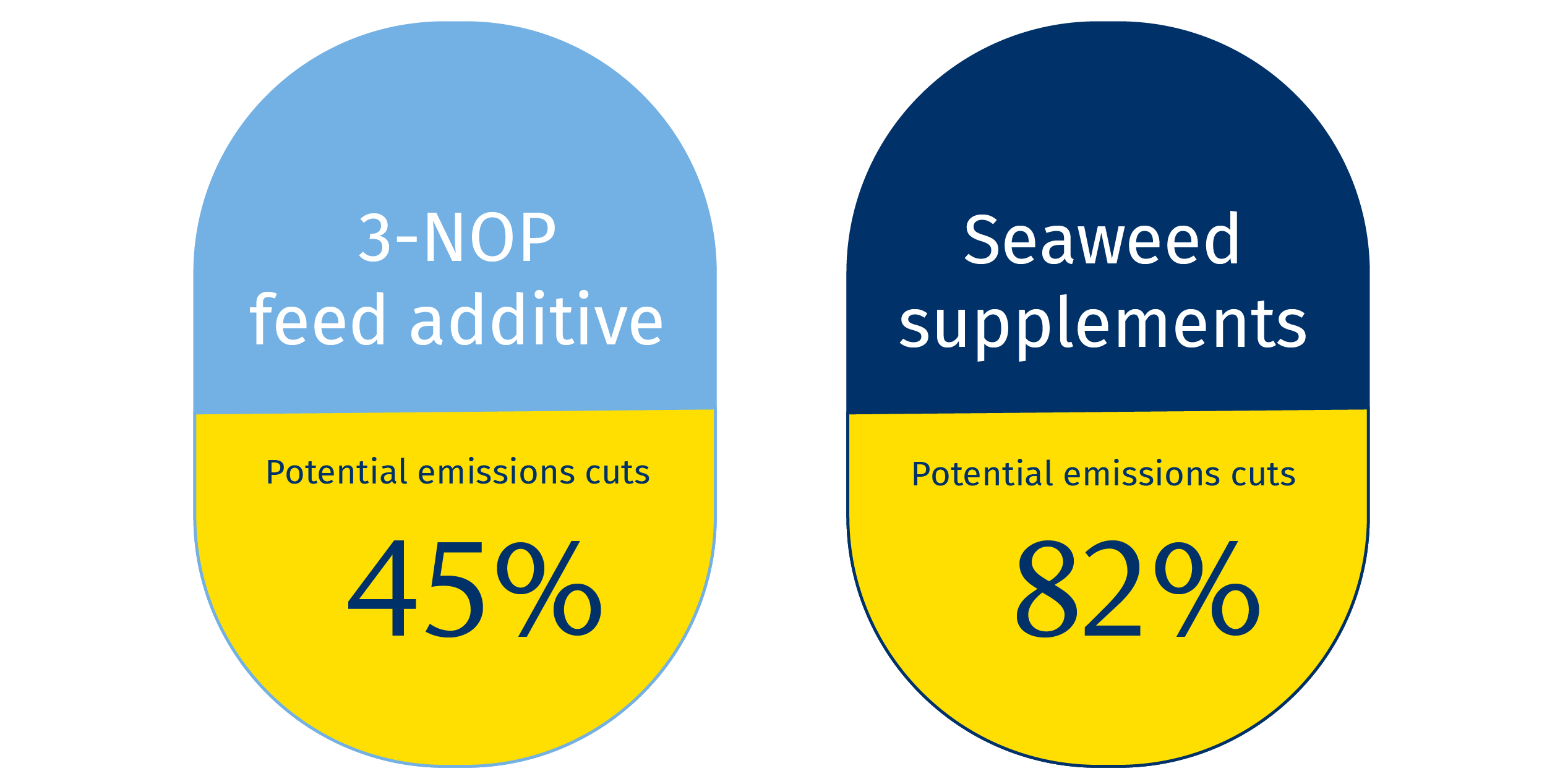

3-NOP has been shown to cut emissions by as much as 45% while adding seaweed to the diet of dairy cows could cut emissions by as much as 82%. Scientists are also working to ensure that this can be done without yield losses—potentially even improving the efficiency of cattle (that is, helping them grow more using less feed). 12

The Challenges

The biggest challenge to scaling feed additives is regulatory approval. 3-NOP has been approved in Brazil and in the European Union, where it was categorized under feed additives that offer an environmental benefit (streamlining the path to commercialization). But in Canada, where it’s classified as a veterinary drug, it’s unlikely to be approved for several years.

Cost is also a key barrier. Without a price on greenhouse gases (such as a carbon tax), farmers lack the incentive to adopt methane-reducing additives because there is not yet a clear economic benefit—only an environmental one. While a carbon credit scheme could help, there is still a heavy burden placed on the farmer to gather data to gain the credit.

3-NOP has been shown to cut emissions by as much as 45% while adding seaweed to the diet of dairy cows could cut emissions by as much as 82%. Scientists are also working to ensure that this can be done without yield losses—potentially even improving the efficiency of cattle (that is, helping them grow more using less feed). 12

The Challenges

The biggest challenge to scaling feed additives is regulatory approval. 3-NOP has been approved in Brazil and in the European Union, where it was categorized under feed additives that offer an environmental benefit (streamlining the path to commercialization). But in Canada, where it’s classified as a veterinary drug, it’s unlikely to be approved for several years.

Cost is also a key barrier. Without a price on greenhouse gases (such as a carbon tax), farmers lack the incentive to adopt methane-reducing additives because there is not yet a clear economic benefit—only an environmental one. While a carbon credit scheme could help, there is still a heavy burden placed on the farmer to gather data to gain the credit.