Even as the world reels from tariffs, there’s a new levy lurking on international borders: a carbon duty on imports.

The EU rolled out its Carbon Border Adjustment Mechanism (CBAM) in 2023; Mark Carney’s government is considering a Border Carbon Adjustments (BCA) to level the playing field for domestic energy and heavy industry against foreign competitors; and a handful of bills in the U.S. at the federal and state level are proposing fees on imports with weaker climate compliance.

The idea of a border carbon fee is simple: ensure that manufacturers from, say, Montreal or Berlin, that spend money and effort to adhere to their domestic robust carbon policies are not disadvantaged against competitors that benefit from weak climate policies in their jurisdictions. Combined, a domestic carbon policy and a border carbon fee is a one-two punch that forces foreign competitors to raise their environmental standards, and ensures domestic industries are not unduly penalized for pursuing decarbonization strategies. Think of Ottawa taxing coal-powered Chinese steel to ensure its not unfairly advantaged against Canadian steel that’s forged by low-carbon but highly capital-intensive electric furnaces.

While a border carbon fee would be a natural extension to Canada’s industrial carbon policy, its implementation is tricky. For starters, it could further inflame Ottawa’s already tense relationship with the Trump administration, which has cracked down on climate policies.

Canada’s carbon policy is in a state of flux, too. Earlier this year, the federal government scrapped a fuel charge—widely known as a carbon tax, followed soon after by British Columbia that had one of the longest and most stable emissions pricing systems globally. The past year has seen Canadian policymakers wobble on industrial carbon pricing: commitment to carbon pricing in Quebec and British Columbia all the while Alberta froze its carbon price at $95/tCO2e earlier in the year, and Saskatchewan cancelled its industrial carbon pricing system.

Canada’s industrial carbon policy has had mixed success to date—it has helped fund renewable energy projects, but with limited direct impact on emissions reduction to date. As the federal government and some provincial jurisdictions look to adjust their industrial carbon pricing strategy, they will also need to factor in shifting trading patterns, changing global economic priorities and the competitiveness of Canada’s industries.

Carbon pricing crosses the border

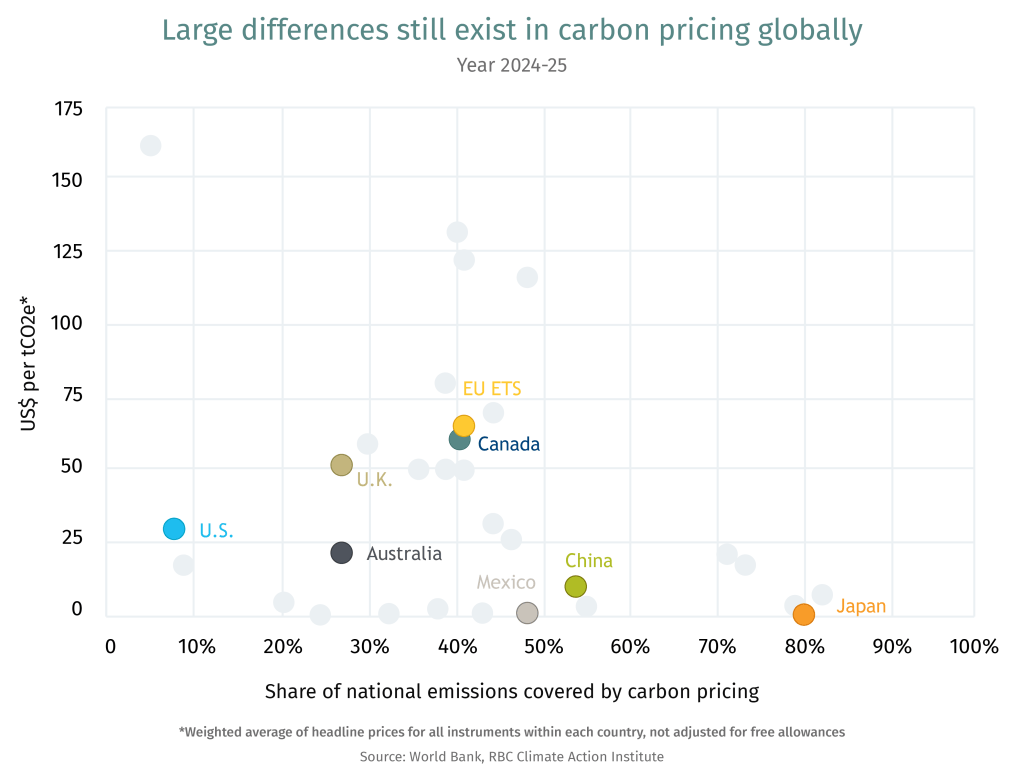

Canada is one of 40-plus countries that have deployed a version of carbon pricing, covering 28% of global emissions.1 Several are now also exploring or advancing domestic carbon pricing systems in response to the European Union’s CBAM:

Emerging markets such as India, Türkiye and Brazil are pursuing domestic carbon pricing mechanisms to ensure their exports comply with EU rules.

The U.K. is in the process of linking its carbon market to the EU to streamline its climate policy with the economic bloc.

China recently expanded its carbon pricing coverage to include cement, steel and aluminum sector emissions.

Japan is consolidating its carbon pricing regimes into a single market as part of its Green Transformation (GX) plan, starting early 2026.

Still, pricing of carbon remains varied. Emissions trading schemes (ETS)—the most common carbon pricing system—rely on market signals to determine the pathway for emissions reduction. As the chart below shows, different jurisdictions assess their sectoral emission profiles, emission reduction potential and costs, that has led to significant differences in how they price carbon.

The U.S.’s Border Carbon Policy Proposals

The Foreign Pollution Fee Act (of 2025) is making its way through the U.S. Senate. It’s a policy designed to impose hefty levies on carbon-intensive imports from primarily China and Russia. But Canada could also get caught in the crossfire, and potentially face carbon tariffs ranging between 17%-33% on its industrial exports to the U.S.2

American policymakers have also been looking to shield domestic industries through a slew of other carbon policy proposals. These include:

The FAIR Transition and Competition Act aimed at ensuring American businesses are not undercut by unregulated importers by imposing a border carbon adjustment on carbon-intensive imports.

A U.S. Clean Competition Act would establish US$55 per tonne carbon tax on domestic producers and protect them from imports through border adjustments.

PROVE IT Act, if enacted, will facilitate the collection of emissions intensity data for energy intensive industries across major trading partners to ensure global transparency on carbon emissions. It was considered a precursor to the Foreign Pollution Fee Act.

The Foreign Pollution Fee Act, reintroduced on April 8, 2025, by Republican Senators Bill Cassidy and Lindsey Graham, seems most advanced. The structure avoids domestic carbon tax, and creates a linear relationship between the levy on importers and their emissions intensity gap. While the bill is unlikely to proceed, it’s seen as another form of protectionism under the guise of climate change policies.

Canada’s carbon pricing patchwork

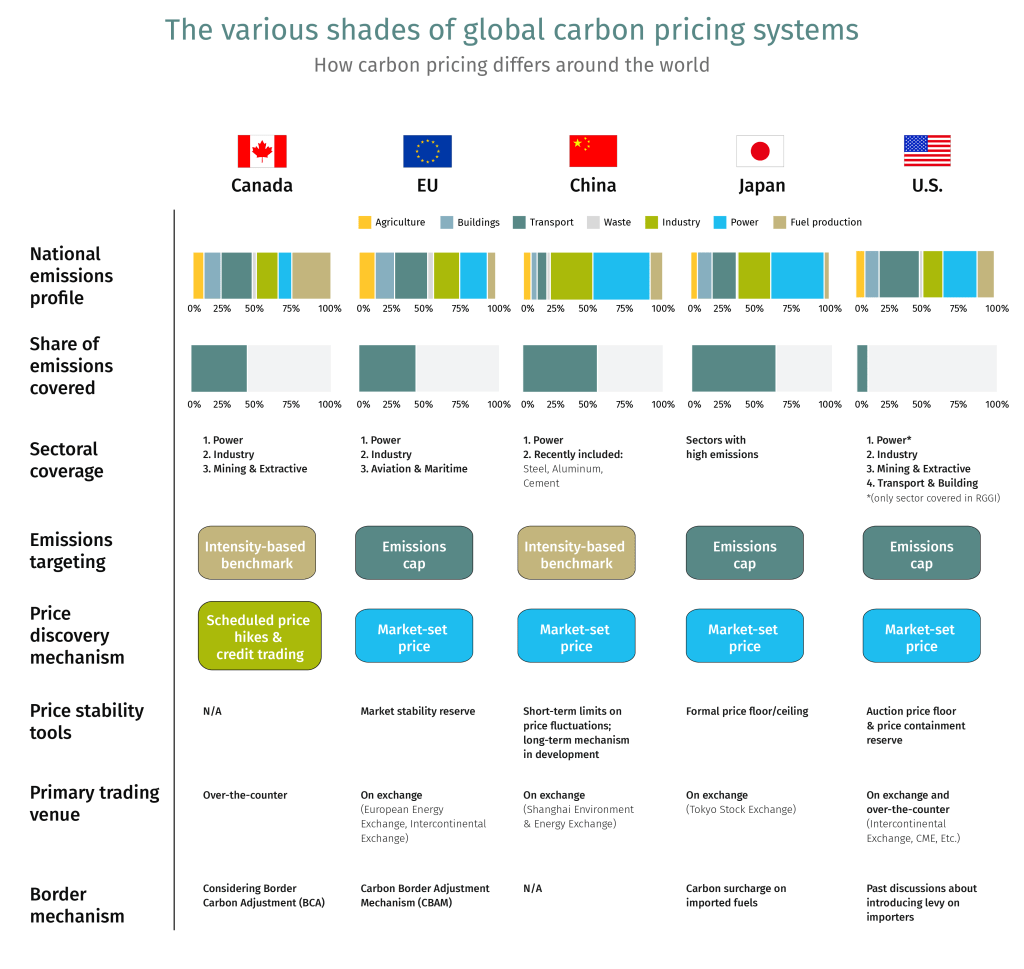

Alberta and Quebec kicked off Canda’s carbon pricing journey in 2007, pursuing two different ways to apply carbon levies on their large industrial emitters. Now, a patchwork of federal and provincial carbon pricing regimes in Canada apply to a range of sectors including power, industry, mining and extraction, and covering nearly half of the country’s total emissions.

With some exceptions, the emissions trading system is Canada’s preferred carbon pricing mechanism. This is how it works: a greenhouse gas emissions performance benchmark places allowance limits on a company’s emissions. Companies emitting beyond those benchmarks buy permits from other companies with emissions that are under the prescribed level. The policy is designed to incentivize investments in low-carbon technologies that would help sharpen Canada’s competitive edge.

The system has encouraged capital to flow to sustainable projects: More than $80 billion worth of projects in carbon capture, utilization and storage (CCUS), wind, solar and bioenergy were either shovel-ready or under consideration and poised to benefit from carbon credit revenues, according to the Major Projects Inventory in 2024.3 Similarly, Emissions Reduction Alberta, funded through the province’s industrial carbon pricing, has facilitated over 300 clean technology projects, valued at more than $10 billion.4

Setting performance benchmarks means not all emissions are subject to carbon pricing, only those beyond the allowance limit—by design. Average cost in Canada, when adjusted for free pollution allowances, stood at $10 per tonnes of carbon dioxide equivalent (tCO2e) in 2024, a fraction of the $80 headline carbon price, according to latest estimate by the Canadian Climate Institute.5 This helps limit carbon leakage (i.e., manufacturers moving to jurisdictions with lower compliance).

Impact on emissions reduction

Carbon pricing reduces emissions with limited or no impact on the economy, according to several studies. But the scale of emissions reduction remains relatively small, with up to 2% annual GHG reduction on average across a range of countries with carbon pricing, including Canada.6 Emissions will need to climb down 6% annually for Canada to reach its climate goals by 2030, as set out in its Nationally Determined Contribution (NDC) commitment to the United Nations.

But there’s a reason the impact on emissions has been muted over the past two decades: Carbon prices were kept low as most clean technologies were nascent with high costs and in early-adoption stage. That’s slowly changing, with solar and wind becoming competitive with fossil fuels, and electric vehicles poised for price parity with conventionally-powered cars; in places like China, EVs are cheaper than gas-powered vehicles. Meanwhile, carbon-capture capacity has doubled globally over the past 10 years.

What’s at stake?

Major discrepancies in carbon pricing with its trading partners can impact Canada’s competitiveness at a time of a structural global upheaval.

Overall, about a fifth of Canada’s imports and exports are from jurisdictions that don’t price carbon. In the U.S.—where policy vary by state—the average carbon price is only US$6 per tonne when adjusted for Canada-U.S. trade flows at the state level.

Here’s what Canada should watch for as its looks to maintain its global competitiveness amid fragmented trade and climate policies:

Diversify trade partners: This won’t be an easy task with 75% of goods destined for the U.S. But nearly a third of Canadian export categories are more diversified; even oil and gas exports are finding new customers in Asia since the expansion of the TMX pipeline and the start of LNG Canada. Beyond the U.S., the global rise of climate-compliant products could give Canada an edge. For instance, Japan’s evolving carbon pricing policy favours cleaner fuel sources.

Foster predictable policy: Access to capital was the top challenge businesses faced in their emissions reduction goals, as noted in our Climate Action Report 2025. Large-scale investments to advance low-carbon technologies require strong and stable price signals to lower risk and allow capital to flow. Policy certainty could help pave the way for capital to be directed towards Canada.

Streamline provincial systems: Reducing barriers and inefficiencies could help de-risk the investment environment. Businesses operating in multiple jurisdictions face different rules, varying price levels and limited or no ability to transfer credits between their facilities. We have previously emphasized that harmonizing fragmented markets could offer considerable economic upside. Removing interprovincial trade barriers could offer greater market access and liquidity.

Beware the wrath of the U.S.: Reconciling carbon policy differences with the U.S.— where less than a tenth of total emissions are priced and at a much lower rate—is eventually required. With 80% of Canada’s oil production, 90% of aluminum, about half of steel and a third of cement shipped to the U.S., Ottawa needs to be mindful of how the U.S. reacts to changes to our policies. For some industries like the oilsands, compliance with emissions obligations costs about $1 per barrel, and less than 50 cents when using carbon offsets. This limits the competitiveness concerns. However, other industries already under tariff pressure and commanding much lower profit margins might require more support.

U.S. trade irritants cut both ways: Extending carbon pricing to imports through BCA is effectively a tariff. With Canada already at odds with its biggest trading partner, any attempt to level the playing field with American companies might be viewed as a trade escalation.

Resolve administrative complexity: From reporting to verifying, BCA is a daunting administrative task. Especially with varying provincial prices, coverage and benchmarks. It’s another reason to pursue harmonization as we wrote previously. The EU excluded SMEs and individual importers from CBAM to avoid regulatory complexity and reduce their costs. Canada should also strive for simplicity of rules.

Beware of unintended consequences: Emissions-intensive trade-exposed (EITE) sectors account for only 5% of Canadian GDP. However, those materials feed into an array of downstream industries. In effect, BCA could cascade through the supply chains. Raising costs for imported steel, for example, while protecting domestic manufacturing may raise costs for automakers, and construction companies, among others, as estimated by the Bank of Canada.7

Canada’s $30-billion supply management system has underpinned national food sovereignty and security for more than 50 years. Covering dairy, chicken, turkey and eggs, the system has ensured price and supply stability for food staples.

The system recognizes that producing food is costly. The arrangement fosters supply-chain stability, however, it could lead to higher consumer prices, especially amid rising input costs.

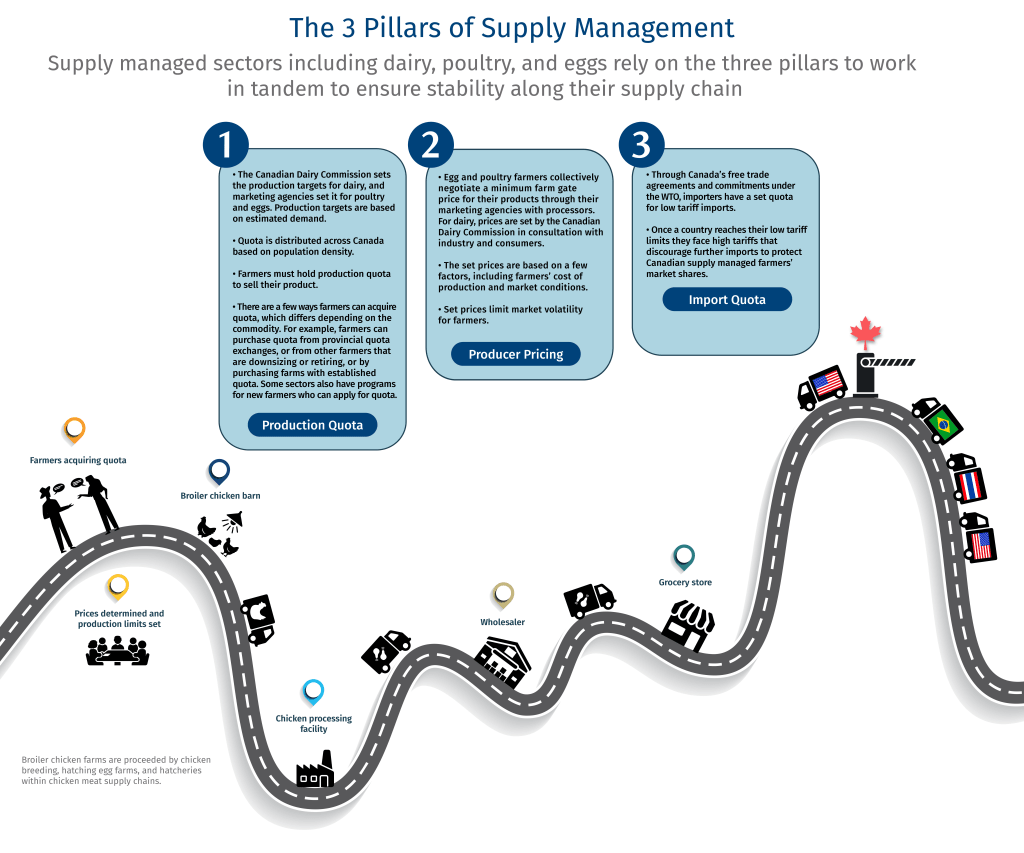

Supply management’s three foundational pillars are under attack—again. Production quotas, set pricing, and import quotas ensure the system’s integrity. But all three are facing calls for reform within Canada and from its biggest trading partners, including the United States (U.S.).

A new law limits Ottawa’s ability to open up the sector. The system’s advocates say Bill C-202 prioritizes national food security and restricts the Foreign Affairs Minister from making new concessions in any trade deal. Other experts say it could hurt Canada’s position in trade negotiations, including the impending Canada-U.S.-Mexico Agreement (CUSMA) review next year.

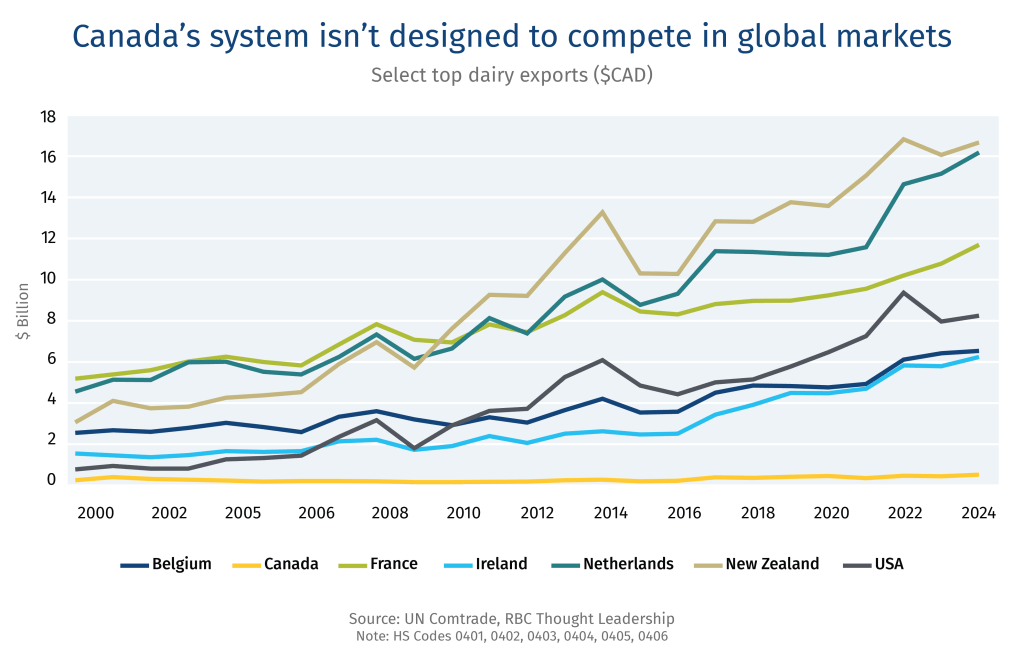

Trade deals are chipping away at Canadian producers’ dominance. Yet, expanded global market access for Canadian supply managed farmers may run counter to the system’s design. A small production base tailored to domestic consumption makes them ill-equipped to compete as exporters in global markets, where high volume and competitive pricing are crucial.

Canada is not alone in facing tough policy choices on agriculture. New Zealand agriculture is grappling with its outsized greenhouse gas footprint, while the United Kingdom is finding its feet post-Brexit. Brazil, second only to the U.S. in total agri-food export value, is eyeing greater global market share. Canada could draw some lessons from these international shifts as it evolves its domestic food sector.

Shifting trade policy landscape for supply managed industries

Canada’s supply management has caught the eye of the Trump administration, again, which has identified it as a major irritant as the two countries renegotiate their trade deal.

That has led to a new debate about Canada’s supply managed food industries, including dairy, chicken, turkey and eggs, that has been a staple of Canadian policy since the 1970s.

At its core, the system provides a stable price that fairly compensates farmers for producing high-quality food. The system’s advocates say it boosts food security, supports domestic producers, and ensures consistency of quality and supply for consumers, while critics say it stifles innovation, inflates prices and limits competition.

The system has come under scrutiny in nearly every trade negotiation and economic downturn, and will likely be a discussion item at the impending Canada-U.S.-Mexico-Agreement (CUSMA) review next year. It’s also being debated amid a domestic push to develop a unified market for goods and services. The conversations are evolving from polarizing calls between dismantling the system and business-as-usual, to a wider spectrum of ideas on reforming the system that’s been around for more than half a century.

Those looking to preserve the system are on the move. In June, Bill C-202 received Royal Assent with strong support from Canada’s supply-managed farmer associations. The Act instructs the foreign affairs minister to stop opening more dairy, poultry or egg quota to trading partners through international trade agreements. Still, the debate continues as stakeholders carve out specific areas for discussion, from the regional milk pooling systems to debating which part of the supply chain should get access to the foreign quota allotment.

The debate is not just bouncing off agriculture’s silo walls. It impacts many aspects of the Canadian economy, including food prices, choices, supply-chain jobs, and Canada’s trade diversification and growth prospects.

What’s at stake?

Supply management in numbers:

1%. The managed sectors’ contribution to Canada’s GDP, amounting to more than $30-billion. The entire agriculture and agri-food sector accounts for more than 7% of Canada’s GDP.12

339,000. The number of full-time jobs in supply managed industries, from farm to processor to distribution.3

14,699. The number of supply managed farms in Canada, or 8% of nearly 190,000 farms across the country.4

9,430. The number of dairy farms, primarily in Quebec and Ontario. Dairy farm numbers across Canada are down by more than 50% since the early 2000s, due to market consolidation.5

7%. The growth in the number of poultry and egg farms over the past two decades. They are largely concentrated in Ontario, British Columbia, and Quebec, with Prairie provinces also seeing an uptick.6

The 3S of supply management

The Canadian system is designed to uphold food sovereignty, stability and standards, which helps the industry prosper, but also presents challenges in a changing global food market.

Sovereignty

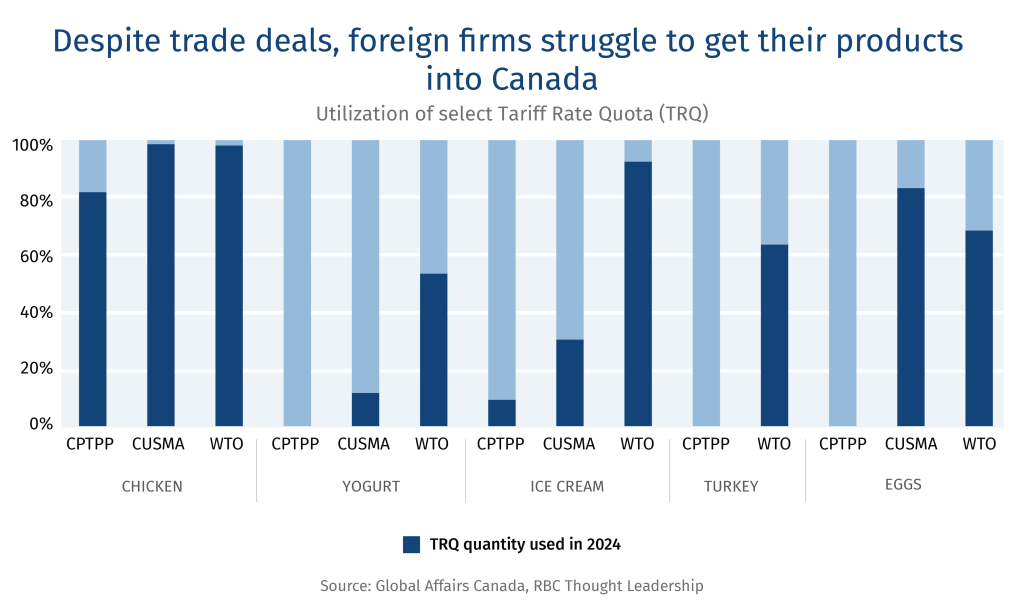

Supply management ensures stable prices and a robust domestic supply chain to meet demand. But as Canadian processors hold the majority of the tariff rate quota (TRQ), which is a set amount of low tariff imports, foreign importers have argued that they have limited access to Canada’s markets to fulfill their non-tariffed trade volumes negotiated in the agreement.

Supply management has emerged as a point of friction with Canada’s largest trading partners, especially the U.S., the European Union (E.U.), and, more recently, New Zealand. A key sticking point: Canada’s restrictions on import quotas.

The quotas are intended to limit imports within Canada’s supply management industries. In recent trade negotiations, however, Canada has made greater concessions, for example, in the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) negotiations Canada agreed to provide participating countries, with an estimated 3.25% of Canada’s domestic dairy market.7 But as Canadian processors hold the majority of tariff import quotas, foreign importers have argued that they have limited access to Canada’s markets to fulfill their non-tariffed trade volumes negotiated in the agreement.

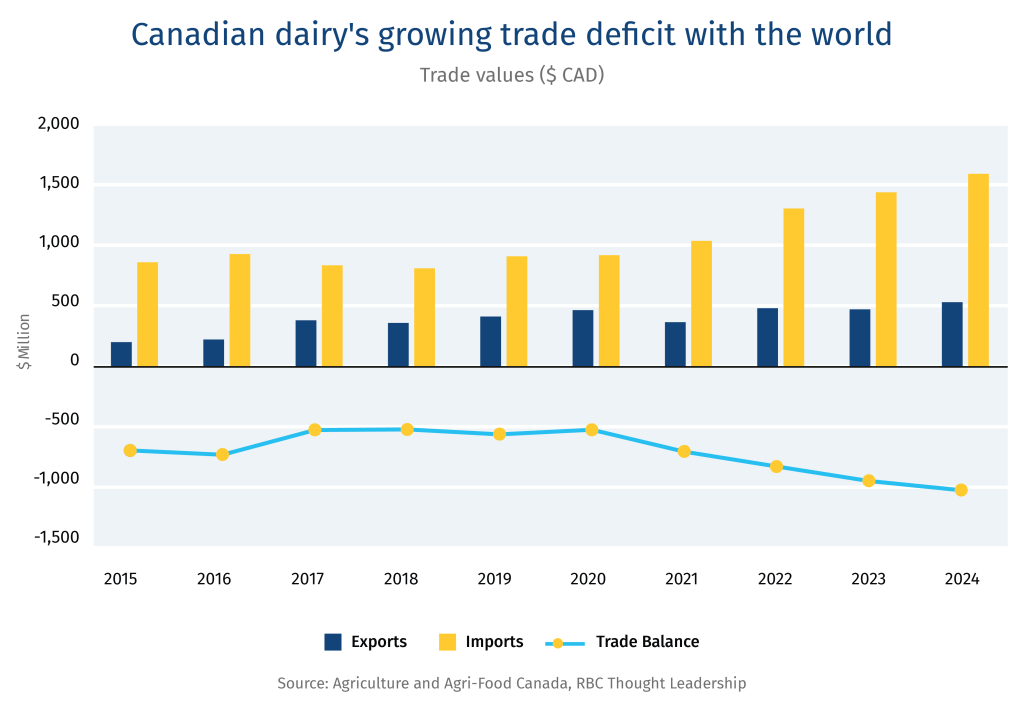

Trade deals are chipping away at domestic producers’ dominance: Trade concessions have resulted in Canada running a small trade deficit on all supply managed products, except chicken meat. For example, imports now represent roughly 4% of Canada’s dairy market.8 This has led to government payouts to dairy, poultry, and egg farmers and processors of $4.8 billion to compensate the industry’s forgone profits from foreign competition.9 Such payouts means Canadians are paying for their supply managed food at the cash register—and additionally through taxes.

Between 1995 and 2017 foreign access to Canada’s dairy TRQ was limited to commitments under the World Trade Organization (WTO). As CUSMA, the Canada-European Union Comprehensive Economic and Trade Agreement (CETA) and CPTPP are phased in over the next ten years, Canadian foreign market access is expected to climb to roughly 10% of Canada’s dairy production.10 In return, Canada has expanded market access for dairy, poultry and eggs in these markets. Canada has a small production base with supply-chain logistics and relationships designed for domestic markets, which makes Canadian supply managed industries ill-equipped to be leaders in global markets where high volumes at competitive prices are critical for success.

Domestic supply chains are helping shield Canadians from trade wars: In times of global disruption, the domestic food supply chain has served Canadians well. Take the made-in-Canada movement that was kickstarted by U.S. President Donald Trump’s trade war. It drove down sales of American brands, with Canadians swapping them with domestic products, wherever possible. For dairy, poultry, and eggs, Canadians can remain especially confident they have immediate access to Canada-based supply chains.

Eliminating loopholes

Processed products such as prepared meals can blur the lines of which food products are traded under which HS code, which categorize the trade of goods and services.

These blurred lines have allowed importers to move products into Canada tariff-free, taking advantage of loopholes that sidestep Canada’s TRQ system, which sets the volume allotted to importers under free trade agreements, including CUSMA, CETA and CPTPP.

Some of these loopholes have been closed, such as cheese being imported tariff-free when it was classified as part of a prepared meal like pizza-making kits for restaurants, which fell outside of TRQ allotments. Other loopholes have yet to be closed such as spent fowl (i.e., old laying hens) which can be used as a category to trade misrepresented broiler chicken raised for meat consumption, to avoid paying Canadian duties.

While importers have TRQ allotments for dairy, egg and poultry products, this low-tariff pathway to Canada is often underutilized as Canadian processors control the majority of TRQs as well as earmarked space in grocery store shelves.

This underutilization of TRQs has been a mounting irritant between Canada and its trading partners, most notably by the Americans who say Canada has not “respected the spirit” of CUSMA, and made it challenging for their producers to access Canada’s market.

Stability

Supply management is synonymous with stability. But, at what cost and for whom? With global market disruptions on the rise, it’s critical to determine a pathway that benefits both Canadian farmers and consumers.

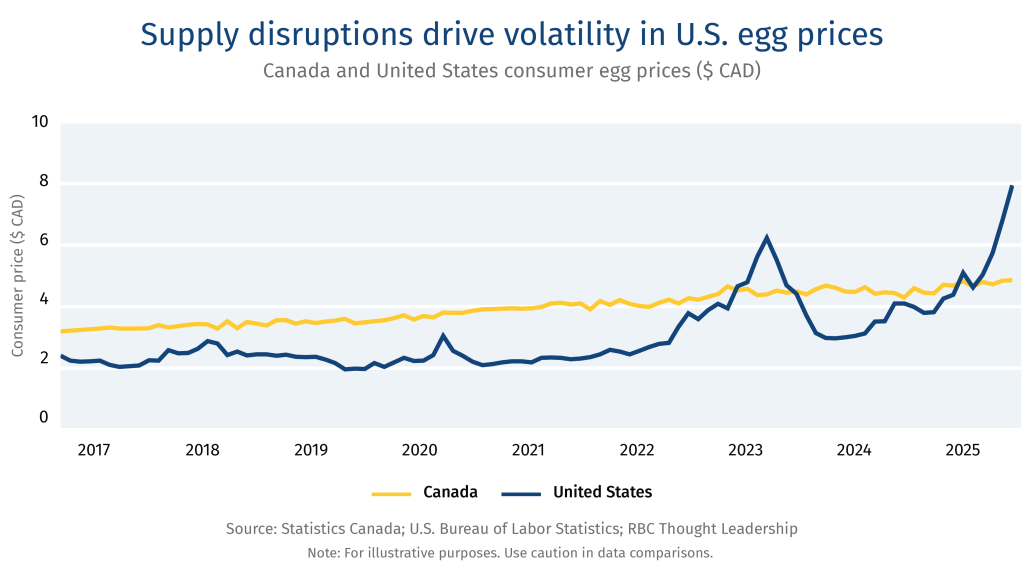

Canada-based food supply chains have distinguished themselves during the pandemic and other crises, such as the recent avian influenza outbreak that’s ravaged the U.S. industry.

Indeed, egg prices in the U.S. have skyrocketed over the past year as the flu takes its toll on animal production, with 174 million confirmed poultry cases, and more than 1,074 dairy cow herds impacted in the U.S. by July 2025.11

The impact has been far less severe in Canada, with roughly 14 million birds infected and no reported cases among dairy herds.12 Canada’s poultry, egg and dairy farms have also been more resilient because of the industry’s standards in biosecurity and animal welfare. Smaller scale production that’s more dispersed compared to U.S. farms (aside from production-dense areas such as the Fraser Valley in British Columbia) has also helped. These on-farm factors have knock-on effects for stability in consumer pricing and product availability. On average, between 2017 and 2025, a dozen eggs sold in Canada was $1 more than in the U.S. However, that had flipped by February 2025 when a dozen eggs in the U.S. cost $3.52 dollars more than in Canada.1314

Supply chain and market disruptions are anticipated to intensify from several issues, including a global movement away from rules-based trade and climate change triggering extreme weather events and spreading disease and pest outbreaks. It’s an important consideration for policymakers as frequent volatility impacts commodity market prices.

Producing food is a costly affair. Fixed quota and price in supply managed sectors generate certainty for farmers, which fosters stability in the supply chain. However, this stability comes with its own cost as it inherently leads to more expensive products as the cost of inputs rise in Canada. Worsening affordability disproportionally impacts food insecurity in low-income families; however significant price volatility is disruptive to average household spending, too.1516

In contrast, non-supply managed farmers growing wheat and raising beef cattle, for example, are exposed to commodity markets, resulting in farmers’ profit margins and consumer prices fluctuating as markets shift. Non-supply managed farmers are often price receivers and cannot pass rising costs onto consumers.

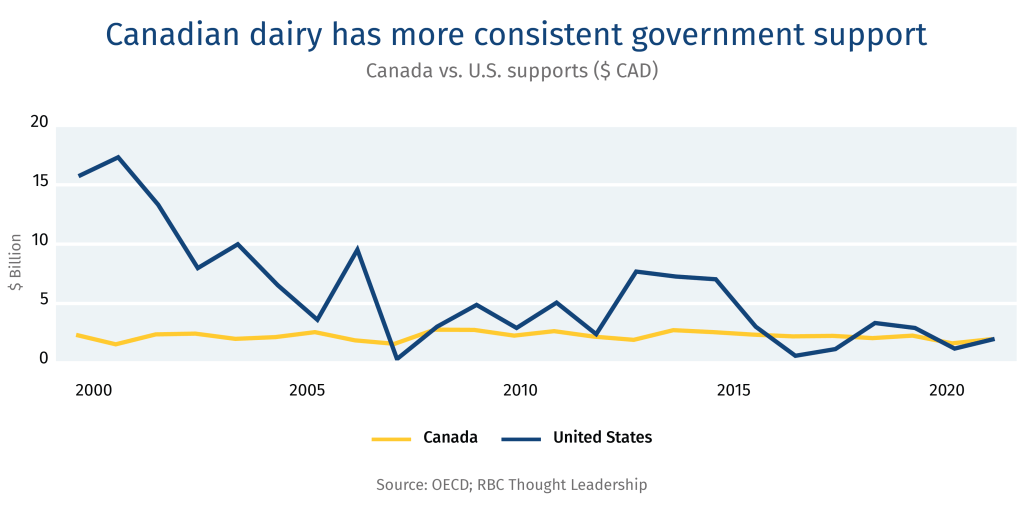

Canada’s support for farms is contentious—but comparable to the U.S. When comparing total direct producer supports, U.S. contributions are 6.5 times larger than Canada’s. Yet, the countries are roughly at par when estimating direct producer supports as a portion of value produced at the farmgate–around 7%.17 However, this support is not evenly distributed across all commodities. Specific to supply managed products, producer supports are clearly aligned with the respective countries’ approach. Canada’s contribution has been consistent with the price producers receive based on supply management, while U.S. farmer supports fluctuate in line with market volatility.

Supply managed farms contribute to Canada’s rural economy prosperity. Stability also plays a broader role in Canada’s rural economy. The most recent agriculture census data, shows the number of Canadian dairy farms fell 11% while herd size rose 13% over a five-year period (2016–2021).18 In the U.S., the number of dairy farms decreased by 34% and herd size increased by 48% over the same period.19 Consolidation enables larger dairy farms in the U.S. to achieve economies of scale. Yet, this recent rapid trend of fewer, bigger farms in the U.S. reduces the diversity of farm sizes, concentrates herd locations, making them more susceptible to disease and pest outbreaks, and can hollow out demand for supporting businesses and rural communities.

Standards

Canada’s supply management allows for a system that adheres to high standards, leading to greater efficiency and sustainability outcomes. However, the system is not designed to maximize production.

Canadian farmers are increasingly ramping up their capabilities to measure, report and verify their progress in adopting best management practices, especially those related to environmental sustainability and animal welfare. The strong governance and market control of supply management allows for widespread and consistent adoption of practices and standards at the farm and along the supply chain. To participate in the regulated market, supply managed farms adhere to an industry code of practice and regulated standards, which has raised Canada’s standards for animal welfare and health and food quality. Non-supply managed production systems in Canada such as beef also have quality assurance programs that ensure high standards on farms such as the Ontario Corn Fed Beef Quality Assurance Program. Yet, the governance system of supply management enables widespread and consistent adoption of practices—an ambition that’s challenging to achieve when there is less regulation and market control.

More stringent standards than the U.S. Nonetheless, on both sides of the border, milk is safe and produced to a high standard. ProAction is the Dairy Farmers of Canada’s framework for best management practices and standards across six themes: milk quality, food safety, traceability, biosecurity, animal care and the environment—with 99.7% of Canadian dairy farmers registered.20 Similarly, the U.S. has the National Dairy Farmers Assuring Responsible Management (FARM), which covers 99% of the U.S. milk supply.21 However, standards within these two programs and the complementary regulations differ, which can impact animal health and milk quality. The U.S. also allows for a higher Somatic Cell Count (SCC), which counts white blood cells in cows. Similar to humans, high white blood cells mean the body is fighting an illness or inflammation, which could negatively impact milk quality. Somatic Cell Count in the U.S. is 750,000 individual cells (IC) per millilitre (mL), while in Canada stands at 400,000 IC per mL.2223

Industry is focused on efficiency and sustainability. The governance frameworks of supply management also provide a platform to scale farmer engagement in industry-wide initiatives on issues such as efficiency, innovation and sustainability. For example, egg farmers across Canada are measuring and reporting their progress on sustainability through the National Environmental Sustainability and Technology Tool (NESTT) platform. This unified approach sidesteps the increasingly fragmented landscape of sustainability and regenerative agriculture projects that many farmers are navigating for market access or to develop new revenue streams through mechanisms such as carbon credits and green premiums.

Global dairy lessons: How other markets are navigating transition and disruption

Food security and sovereignty are featuring high on government agendas globally as extreme weather interrupts food production and trade barriers disrupt trade flows.

Dairy, a nutrient and culturally significant staple in many diets around the world—from French cheese to lassi in India—, has high demand but also high volatility in international markets, resulting in the industry attracting elevated attention in policy, trade, and farmer support.

Here’s how other countries are managing their dairy sector during times of transition and disruption.

New Zealand: An international leader with a rising GHG footprint

New Zealand removed its production quota in the 1980s due to a budget crisis, transforming the country into the world’s largest dairy exporter. In 2001, the government launched Fonterra, a farmers’ co-op, which sets prices and is now the largest purchaser of domestic milk. Its price calculation is based on revenue from milk sales minus operating and overhead costs and capital recovery. New Zealand has more than doubled its national herd since the early 1980s, and individual herd sizes increased three-fold. Consolidation meant the number of herds fell from 15,753 in 1985 to 10,485 in 2024.24 Market liberalization has transformed the New Zealand dairy supply chain, especially powder milk production, which has grown 237% in volume since 2000, driven by free trade agreements with large importers such as China and targeted foreign and domestic investment in building capacity and automating manufacturing processes.25

The dairy sector has become highly efficient and competitive, as demonstrated by its herd consolidation, but the growth in the number of cows has raised the sector’s environmental impacts, such as greenhouse gas emissions (GHG). Led by dairy, agriculture now accounts for over 50% of New Zealand’s GHG emissions.26 Recent national GHG targets have created uncertainty in the sector, resulting in a review of national targets and agriculture’s role in meeting them. AgriZero, a public-private partnership, is focused on matching funds and accelerating climate action in agriculture. It’s seen as a unique model to stack funds at a time when attention on climate mitigation has slowed down.

Lesson for Canada: A first of its kind, AgriZero serves as an example for Canada to explore as pools of climate funds shrink and the need for coordinated, scaled action in agriculture grows.

United Kingdom: Transitioning away from the EU model

The U.K. is transitioning its policy approach to area-based subsides under the Environmental Land Management Schemes (ELMS) post-Brexit that’s underpinned by sustainable agriculture such as marginal land rehabilitation. Dairy producers in the U.K. received direct payments under the EU’s Common Agriculture Policy (CAP), but these types of payments are being phased out until 2028, as part of the U.K. departure from the economic bloc. This transition in farmer support imposes both financial and administrative burdens on the sector as farmers navigate change, amid rising costs of domestic production and competition from importers.

To enable greater agri-food trade among E.U. countries and the U.K., the two have agreed to move forward with establishing a common Sanitary and Phytosanitary area (i.e., shared standards on food safety and quality) that aims to ease the movement of agriculture and food products across the U.K. and EU. However, some say that the move could impact the U.K.’s ability to form trade agreements with countries outside of the E.U. and maintains the U.K.’s ties to the economic region.

Lesson for Canada: As Canada embarks on a mission to strengthen and diverse its international trade, it might avoid going from an over-reliance on the U.S. to over-indexing to another region or country via overly restrictive standard alignment of agri-food products for trade.

Brazil: The struggle to break into the global market despite high ambition

Brazil has transformed its agriculture sector and is now a leader in global agri-food exports—the second largest in the world, after the U.S. Yet, less than 1% of Brazil’s dairy production is exported.27 Domestic demand, market infrastructure that’s not export-oriented, and a highly competitive international market has impeded Brazil’s global push.

The country’s dairy production and processing infrastructure greatly varies from smallholder, subsistence farms to modern, large-scale farm businesses. The former is supported through subsidies for asset investments such as cooling tanks, pasture, and milking infrastructure. Farmer prices are mostly market-driven, but the government may intervene via CONAB (National Supply Company) to buy excess milk or offer storage subsidies.

With ambitions to break into the global market in a big way, Brazil is up against tough competition, notably from New Zealand, as it eyes the Middle East, Latin American and Asian markets. To grow globally, Brazil must also address its weaker standard and regulatory approach to land use, GHG emissions, traceability and cold-chain logistics.

Lesson for Canada: While Brazil and Canada have had different agri-food development trajectories to date, they are increasingly competing for the same piece of the global agri-food export pie. Brazil’s approach to enabling diverse scales of production, targeted at both domestic and export growth, should prompt Canada to investigate its own production, which continues to consolidate and faces rising foreign competition.

Market Outlook

Canada’s supply management systems is designed to protect the country from changes in international markets. Yet, policymakers still need to be alert to structural shifts and macro trends in the global industry.

Dairy

Real global dairy prices for farmers are projected to trend downward within this decade. But, relative to input costs, prices are expected to rise, especially as milk produced per animal grows.28 U.S. farmers could see an average annual drop of 8% year-over-year in real price, signalling lower returns for dairy farms in commodity markets that do not innovate and grow.29

Global dairy consumption is expected to modestly increase 1% per year, while production is projected to grow at 1.6% per year to 1,085 million tonnes, driven by production in India, Pakistan and Sub-Saharan Africa, primarily for their domestic consumption.30

Fresh dairy consumption in North America and Europe are stable or declining as consumers move away from full-fat milk and cream, and plant-based alternatives such as oat milk mature as an established replacement. Processed dairy consumption, including butter and powder milks are on the rise driven by their use in food manufacturing, including infant formula and baked goods. Finally, cheese consumption, which is closely connected to household income has been on the rise in growing international markets such as Mexico, the U.S., Brazil and Saudia Arabia.31

Only 7% of global milk production is traded internationally due to its perishability and as market infrastructure in many countries is primarily designed for domestic or regional distribution with few exceptions, such as New Zealand and Ireland. However, over 50% of milk powder, including whole and skim products, are traded.32

World dairy trade is expected to grow by more than 12% over the next eight years. Skim milk powder from the U.S. and cheese from the E.U., two of the largest dairy export segments, are poised for the highest growth.33

Poultry and eggs

Global prices for poultry and eggs are projected to decline as inflation and input costs fall. For example, U.S. farm prices per dozen of eggs are projected to decline by US$0.90 over the next decade, with an average year-over-year decline of 4%.34 However, U.S. production is expected to rise 12% by 2033, from a 2022 baseline.

Poultry production is expected to increase with growing demand, and account for nearly half of all meat produced. Global poultry consumption is expected to grow 16% over the next decade—the most among animal proteins. Poultry is projected to account for 43% of animal protein consumed by 2034, with notable growth in Brazil, Europe, and the U.S.35

China’s self-sustaining food policy and recent rebound from African swine fever and avian influenza outbreaks has resulted in a decline in global meat trade from its height in 2021, when China accounted for roughly a quarter of global meat imports.

Population and GDP growth in Africa and Asia are expected to rebound meat exports within the next decade, driven by poultry which is expected to account for over 40% of total meat imports.36

Statistics Canada. GDP at basic price, by industry, province and territory, 2025.

Legal Disclaimer2

Agriculture and Agri-Food Canada (AAFC). Overview of Canada’s agriculture and agri-food sector, 2025.

Legal Disclaimer3

Dairy Farmers of Canada. What Supply Management Means for Canadians, 2024.

Legal Disclaimer4

Statistics Canada. Farms classified by farm type, Census of Agriculture historical data, 2022.

Legal Disclaimer5

Statistics Canada.

Legal Disclaimer6

Statistics Canada.

Legal Disclaimer7

Dairy Processors Association of Canada. Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP).

Legal Disclaimer8

Statistics Canda. Dairy statistics and market information, 2025.

Legal Disclaimer9

Agriculture and Agri-Food Canada (AAFC). Supporting Canada’s supply-managed sectors, 2023.

Legal Disclaimer10

Dairy Processors Association of Canada. Canada-United States-Mexico Agreement (CUSMA).

Legal Disclaimer11

U.S. Centers for Disease Control and Prevention. Avian Influenza (Bird Flu), 2025.

Legal Disclaimer12

Canadian Food Inspection Agency (CFIA). Status of ongoing avian influenza response by province, 2025.

Legal Disclaimer13

Statistics Canada. Monthly average retail prices for selected products, 2025.

Legal Disclaimer14

U.S. Bureau of Labor Statistics. Consumer Price Index – Average price data, 2025.

Legal Disclaimer15

Statistics Canada. Household spending by household income quintile, Canada, regions and provinces, 2025.

Legal Disclaimer16

Statistics Canada. Food insecurity by economic family type, 2025.

Legal Disclaimer17

Organisation for Economic Co-operation and Development (OECD). Agricultural policy monitoring, 2024.

Legal Disclaimer18

Statistics Canada. Number of cattle, by class and farm type (x 1,000), 2025.

Legal Disclaimer19

United States Department of Agriculture, National Statistic Services (USDA NASS) 2022 Census of Agriculture, 2024.

Legal Disclaimer20

Dairy Farmers of Canada (DFC). ProAction, 2025.

Legal Disclaimer21

Farmers Assuring Responsible Management (FARM).Animal Care, 2025.

Legal Disclaimer22

DFC. ProAction – Milk Quality, 2021.

Legal Disclaimer23

USDA. Determining U.S. Milk Quality Using Bulk-Tank Somatic Cell Counts, 2018.

Legal Disclaimer24

DairyNZ and LIC. New Zealand Dairy Statistics 2023-24, 2024.

Legal Disclaimer25

USDA Foreign Agricultural Service. New Zealand: Dairy and Products Annual, 2025.

Legal Disclaimer26

Ministry of the Environment, New Zealand. New Zealand’s Greenhouse Gas Inventory, 2025.

Legal Disclaimer27

Food and Agriculture Organization, United Nations (FAO). Dairy Market Review: Overview of global market developments in 2024, 2025.

Legal Disclaimer28

OECD and FAO. OECD-FAO Agricultural Outlook 2024-2033, 2024.

Legal Disclaimer29

USDA Economic Research Service. USDA Agricultural Projections to 2034, 2025.

Legal Disclaimer30

OECD-FAO.

Legal Disclaimer31

FAO.

Legal Disclaimer32

OECD-FAO.

Legal Disclaimer33

OECD-FAO.

Legal Disclaimer34

USDA.

Legal Disclaimer35

OECD-FAO.

Legal Disclaimer36

OECD-FAO.

As artificial intelligence comes of age, Canada finds itself at a crossroads. While we possess world-class research and a robust talent pool, the country is falling behind as global competitors race ahead in AI adoption. The core challenge is not a lack of technology or talent, but a pervasive “imagination gap”—a widespread inability among Canadian businesses, especially small and medium-sized enterprises (SMEs), to see AI as relevant or beneficial to their operations. Only 12% of Canadian firms have integrated AI into their production or services, placing Canada among the lowest in AI adoption in the OECD. Data from the OECD also shows that Canadian firms tend to explore a more limited set of use cases for AI than other nations.

And yet, the upside is clear. A recent Business Development Bank of Canada survey revealed that 97% of AI-adopting SMEs reported ‘tangible’ benefits. And Statistics Canada data showed that AI’s impact on task reduction is particularly pronounced in companies with fewer than 100 employees—underscoring significant potential for SMEs. The issue was also high on the agenda at the G7 in Kananaskis, Alberta, where leaders committed to “double down” on AI adoption efforts to improve prosperity.

To better understand why Canadian businesses have been so slow to adopt AI, RBC Thought Leadership partnered with the University of Toronto’s Munk School of Global Affairs & Public Policy and conducted more than two dozen in-depth interviews with senior business, public service and technology leaders in Canada. Here’s what we learned about the barriers that companies, both big and small, are facing. And some lessons from organizations that have taken the challenge of AI adoption head-on.

1. First-Mover Dilemma: Certain Costs, Uncertain Benefits

Some companies that have been slow to adopt AI are locked in inertia. The costs associated with AI adoption are immediate and tangible, while the benefits seem distant and notional. For chief technology officers, AI initiatives carry fixed, up-front financial costs, as well as reputational costs if the project fails. But, as some of the leaders we spoke with recognized, late adoption carries the risk of lagging behind quick-moving competitors. It’s a double‑edged sword: move early and risk losing scarce capital and personnel resources; move late and risk competitive disadvantage.

Several technology leaders noted that these uncertainties frequently stall approvals by six to 12 months. Adding to that, they expressed frustration that Canadian industry leaders often failed to clearly perceive the benefits competitors were already achieving through AI. Technology developers even cited achieving greater success pitching their AI solutions to U.S. based divisions of Canadian companies than their domestic counterparts.

To navigate these obstacles successful AI transformation leaders recommended clearly quantifying AI investments by contrasting the costs of immediate action versus the cost of inaction. Tools such as ‘cost of delay’ dashboards help clarify the opportunity costs of not acting sooner.

Bell Canada: Overcoming Inertia Bias

When GPT‑4 burst onto the scene in early 2023, Bell’s directors wanted to know immediately what waiting to implement might cost them. Within weeks, the AI Group President convened two board‑level tutorials and unveiled ‘cost‑of‑delay’ analysis that contrasted lost productivity with the modest price of pilot projects. The numbers were decisive: capital to fund AI applications was released the same quarter. Real‑time speech analytics now mine 100% of the firm’s 50,000 daily customer calls, surfacing friction points that were previously buried in anecdotal samples. This has enabled AI voice and chat agents to handle inquiries with greater accuracy.

Cultivating a ‘culture of entrepreneurship and experimentation’ has also allowed Bell to grow innovative AI use cases from the bottom up, developing novel AI applications that vastly improve communication processes, workflows and customer satisfaction.

2. AI Literacy: Moving from Apprehension to Opportunity

Whether it’s a fear that AI is coming to take their jobs or just a lack of understanding of its benefits, Canadians are skeptical of AI. One recent KPMG study found that 79% of Canadians are concerned about negative AI outcomes. And it’s estimated that less than one-in-four Canadian employees have received AI training. Simply put, most Canadians haven’t engaged sufficiently with AI to demystify it.

While having an AI champion in the corner office or a single business unit dedicated to experimentation and implementation helps, if AI expertise remains confined to a narrow ‘priesthood,’ widespread adoption stalls. Our research indicates that companies that invest in AI literacy for their staff see faster scale-up of AI projects, stronger employee engagement, and growing organizational confidence. Knowledge is a powerful catalyst for continuous innovation and competitive differentiation.

Hopper: Workforce Reskilling for Enhanced Efficiency

Rather than using AI to displace its customer support staff, Hopper, a Montreal-based travel platform, trained employees to take on roles focused on AI content, training, and testing. Up-skilling its staff to embed AI into its customer support function not only addressed employee hesitation, it allowed Hopper to handle customer inquiries 75% faster—reducing average resolution time from 15–20 minutes to 3–5 minutes. It did this without compromising customer satisfaction and led to cost savings of ~90% compared to human-driven interactions.

Canada’s most successful adopters match grassroots experimentation (“super‑agency” employees who already prompt, patch and prototype with GenAI) with an executive‑mandated transformation agenda. When only the bottom layer is active, shadow‑IT proliferates and pilots stall for lack of budget or risk authority. When only the top pushes, initiatives feel imposed, and staff revert to old workflows.

Lumberhub: Bottom‑Up “Super‑Agency” in Traditional Industry

When a chronic pricing lag between sawmills and home‑builders kept eating into margins, George McKeown, a PhD chemist turned lumber trader, asked a simple question: Why do we accept this inefficiency?

Lacking a deep coding background, he turned to GenAI pair‑programmers to develop over 40k lines of code and in less than three months built a conventional react/typescript web app running on Amazon Web Services that ingest real‑time futures data, spits out dynamic quotes for every stock keeping unit (SKU), and auto‑generates purchase orders for suppliers.

AI as an enabler, not the end‑product: The final platform runs on conventional SQL + Python; the code itself was written multiple times faster thanks to Copilot‑style tools.

Immediate pay‑off: The quote‑to‑order cycle time dropped from days to minutes, metigating inefficient and volatile price swings.

Leadership unlock: Once the CEO saw a live demo, the lumber mill fenced budget to refine the prototype and plugged it into the ERP stack inside.

3. Paralysis of Plenty: Too Many Use‑Cases

AI has opened the floodgates. To a technologist’s eye, every process, product, and customer touch‑point looks like it can be automated. But abundance can lead to inaction—‘choice paralysis.’ The bottleneck is often choosing the first use case. To accelerate the decision process, some firms tapped the expertise of their staff, including hosting a ‘use‑case tournament’ to evaluate options.

But even if a pilot program is selected and initiated, mid-size Canadian firms frequently encounter significant barriers to scaling projects. Our interviews highlighted three primary factors impeding AI initiatives:

Budget cliff: Public incentives frequently support only initial pilot phases, covering equipment or personnel but rarely address subsequent integration, training, and retrofitting costs. Many initiatives stall after pilot phases because ongoing costs typically fall into operating budgets instead of capital expenditure.

Champion churn: Key sponsors, such as plant managers or IT leads, often rotate or are promoted after pilots begin, leaving successors to inherit risks without corresponding enthusiasm or clarity around the initiative’s original vision.

ROI lost in translation: Tangible benefits essential for scaling rarely make it into capital allocation discussions. Technical improvements proposed by engineers must translate into clear cash-flow projections. Consequently, potential operational expenditures must be explicitly justified by cash-flow benefits rather than abstract metrics like ‘defects-per-million.

4. Data: Fragmented and Low-Quality

Many of the leaders interviewed cited the enormous lengths they had to go through to get to a place where AI usage was even possible, underscoring how foundational data architecture is to successful AI adoption. Some leaders flagged the shortage of high-quality, production-level data in manufacturing. That, in combination with the difficulties around unifying diverse datasets, creates a data integration burden that ends up thwarting or delaying AI implementation. Significant upfront investments are often required to improve data quality, reliability, and governance before AI can even be contemplated, which acts as a deterrent to adoption.

Strengthening Canada’s data foundations by building robust, AI-ready data ecosystems is essential. Many SMEs, nearly half of which are more than 20 years old, face significant hurdles adapting legacy systems and fragmented datasets. Legacy management information systems capture data in incompatible formats, riddled with gaps and duplicative records. The time spent cleaning and stitching these sources drains enthusiasm and budgets long before benefits materialize.

St. Michael’s Hospital: What Canada forfeits when data stays in silos

GEMINI, Canada’s largest hospital-data platform for research, was established to facilitate the creation of large health data sets to improve healthcare.

Despite successfully integrating more than 60% of Ontario’s hospital medical care within its platform and supporting more than 1,000 clinicians and researchers through $140 million in combined grant funding, challenges persist. A disparate web of hospital systems with incompatible data formats slow governance processes, and infrequent data refresh cycles block progress. These barriers highlight what Canada will miss out on if data integration efforts are not improved.

Platforms like GEMINI can automate patient matching into trials and efficiently capture health outcomes, reducing the cost of trials by up to 80% and enhancing Canada’s attractiveness as a clinical trial hub. Large-scale, richly detailed datasets are critical for health AI. GEMINI and its partners in Alberta and Quebec have started taking steps to overcome barriers, aspiring to build a 100-hospital near real-time data sharing network called ‘VITAL.’ Large and detailed datasets like GEMINI are critical for health AI and accelerating their development will be key to Canada‘s ability to be a leader in this field.

5. Blind Spots: Overlooking the Unknown

It is common to invest in AI to automate the known knowns (repetitive tasks) or to analyse the known unknowns (questions we can articulate but cannot answer). Yet, some of the biggest wins came from the unknown unknowns—insights managers didn’t realize they were missing until they were unearthed by the model.

AI models can ingest years of sensor data, call logs, or shipment records, which can lead to the surfacing of correlations and anomalies that may have otherwise escaped human analysis. For example, excess energy use on a single production line, chronic micro‑stoppages in a distribution network, or an unexpected cross‑sell pathway in e‑commerce. Budgets, KPIs and risk reviews are designed for defined problems, the ability of an AI to augment ‘discovery value’ widens a firm’s operational possibilities.

Linamar: Turning ‘Unknown Unknowns’ into Competitive Advantage

Uncovering hidden inefficiencies and unexpected solutions in complex manufacturing environments is transforming Linamar’s approach to overlooked data, revealing tangible competitive advantages.

When Linamar piped 10 years of shop‑floor data into Acerta’s LinePulse Industrial AI and Analytics platform, the first surprise was a set of micro‑fluctuations in pump pressure that engineers had never tracked. By fixing it, the company was able to eliminate what had been a silent cost in its manufacturing process in parts for EV gearboxes. The software’s machine learning root-cause analysis tool then flagged the single upstream variable most responsible for ‘noise, vibration, and harshness’ from one of more than 100 parameters that no human could have correlated in real time. On another manufacturing line, the model showed that a non‑bottleneck station within the assembly line was slowing throughput.

By adopting an industrial AI platform that can solve problems in virtually any discrete manufacturing environment, Linamar has re‑positioned AI as a continuous diagnostic instrument rather than as a one‑off cost‑saver. Each unexpected insight frees capacity, trims launch challenges and even wins business.

6. Digital Infrastructure: Canada’s Compute‑Capacity Deficit

Much like how railways or electricity grids fuelled economic growth in the past, robust AI compute capacity—supercomputers and GPU clusters—underpin innovation. Currently, Canada’s compute capacity significantly lags the growing demand for training and deploying cutting-edge AI models. Canada trails every other G7 nation in AI computing infrastructure, possessing only one-eighth to one-tenth of the available compute performance per capita compared to countries like the U.S. Without sufficient domestic compute capacity, Canadian innovators may be held back in comparison to other countries that are providing subsidized and extensive compute capacity to their leading AI firms and researchers. And Canadian institutions may rely on foreign cloud providers which, in the context of sensitive data or government-facing AI applications, could heighten risks to sovereignty, security and economic resilience.

AI leaders shared that waiting in domestic compute queues can extend training cycles from hours to days—killing iteration speed. Procurement rules and cautious public‑sector buying also slow the build‑out of sovereign clusters that could attract anchor tenants. Without targeted ‘compute credits’ or pooled infrastructure, even world‑class research talent cannot fully commercialise models at home.

Provincially, initiatives like Alberta’s Artificial Intelligence Data Centres Strategy help to align more localized strengths, such as skills or energy, with the economic opportunities offered by AI compute infrastructure. Such initiatives are valuable complements to federal strategies which broadly incentivize compute infrastructure development.

And recent federal initiatives, notably the $2 billion Canadian Sovereign AI Compute Strategy, represent important steps toward addressing this gap. The program’s first project—a domestic supercomputing partnership between Cohere and CoreWeave—will provide Canadian AI firms access to essential computing resources on Canadian soil. Accelerating and expanding such strategic investments can significantly enhance Canada’s domestic AI infrastructure, enabling solutions to be securely and swiftly developed without reliance on external providers.

7. Regulation and Policy: Duplicative and Uncertain

Regulatory responsibility is currently divided among several bodies—including Innovation, Science and Economic Development (ISED), Office of the Privacy Commissioner (OPC), Competition Bureau—as well as sector-specific regulators (e.g. Health Canada, and Transport Canada). Plus, provinces are increasingly drafting their own distinct guidance (e.g., Québec’s Bill 25 privacy amendments), creating what some describe as a ‘mini-EU’ landscape of 13 distinct regimes.

A major regulatory obstacle cited in most of the interviews was the absence of federal leadership. Recent attempts, notably the Artificial Intelligence and Data Act (AIDA), ultimately failed amid political challenges. AIDA drew criticism not only for its overly cautious, burdensome compliance demand, but also for procedural shortcomings and inadequate stakeholder engagement. Canada could benefit from a clear regulatory framework that facilitates innovation, involves meaningful public participation, and enables practical AI implementation.

This absence of clear federal guidance disproportionately affects SMEs—Canada’s economic backbone. Smaller businesses typically have limited resources to independently navigate regulatory ambiguities, leading to hesitation around investing in AI. Many technology leaders interviewed by RBC lamented how repeated announcements without substantive guidelines have created persistent uncertainty, pushing companies toward overly cautious approaches. As a result, organizations often limit their AI implementations to conservative use cases, wary of significant future compliance costs if regulations become stricter. Clarity would help.

Conclusion: Five Lessons for Leaders

Despite the obstacles, there are many examples of Canadian firms successfully embedding AI in their operations and reaping the competitive benefits. Successful firms:

Quantify the costs associated with both action and inaction to ensure decisions about capital allocation are informed by both the risks and the rewards of AI adoption.

Educate employees about the benefits of AI and teach them how to utilize the technology, both to advance their careers and to improve operational effectiveness.

Address the problem of ‘too many ideas, too little focus’ by pulling employees into the evaluation process, empowering them to drive solutions.

Invest in data governance, ensuring data is standardized, consolidated, and AI-compatible.

Formalize an ‘exploration budget’—a portion of annual AI spend reserved for open-ended data mining to ensure that hard-to-find opportunities are discovered. Embedding that mindset among employees turns every new dataset into a hunting ground for hidden efficiencies and growth opportunities.

Project Lead

Reid McKay, Director, Technology Policy Lead, RBC Thought Leadership

Contributors Jordan Brennan, Head of Thought Leadership, RBC Jaxson Khan, Special Advisor Nicole Harris, Graduate Student, Munk School of Global Affairs & Public Policy Nora Bieberstein, Director of Strategic Programs, RBC Thought Leadership Niki McKeown, Research Associate, RBC Thought Leadership

Shiplu Talukder, Digital Publishing Specialist

Special thanks to Daniel Diamond, Daniel Ebrahimpour, Janelle Gunaratnam, Anya Haldemann, Nikhil Konduru, Patrycja Maszlejak, Georgia Maxwell, Andrew Scarlato, Sabreena Shukul, Avaani Singh, Mia Sunner, Sydney Wisener

Executive Sponsors John Stackhouse, Senior Vice President, Office of the CEO, RBC Janice Stein, Founding Director, Munk School of Global Affairs & Public Policy

The past few years have been incredibly hard for many Canadians. The pandemic caused massive disruptions to the job market and the highest rates of inflation in decades, which was intensified by the war in Ukraine. And now comes a trade war with the U.S., with its own set of shockwaves, including job losses and supply-chain upheaval, sending the price of goods even higher. Many can’t keep up.

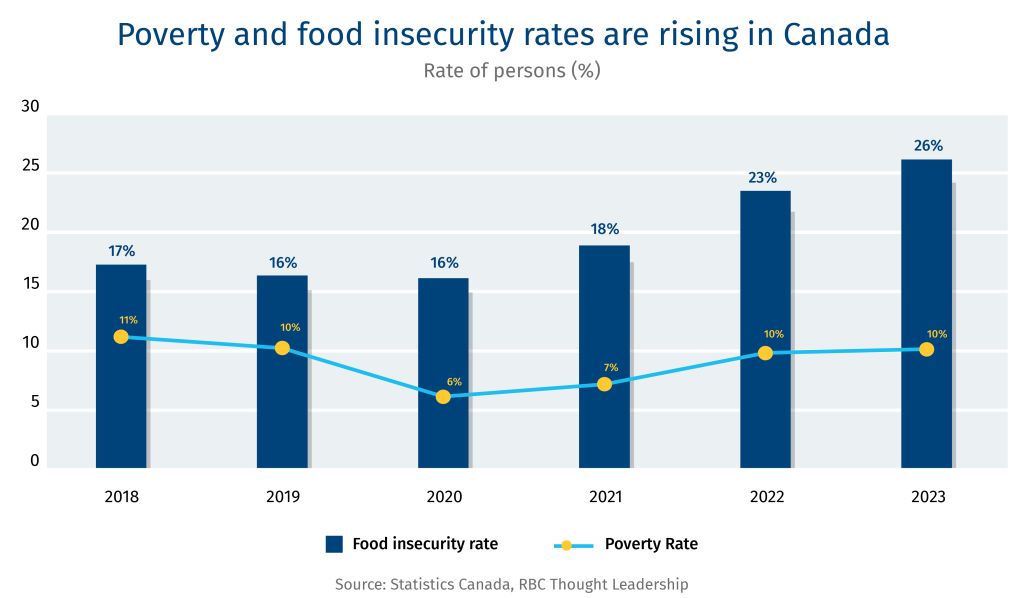

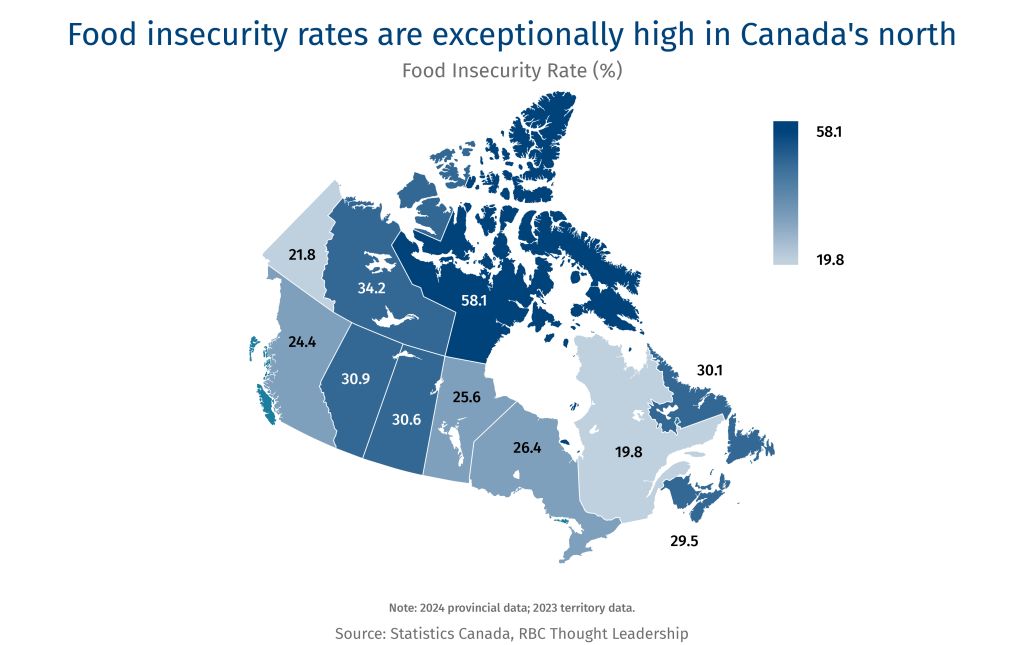

Today, one in four Canadians are experiencing food insecurity. That’s 10 million people—a level never seen before in this country.1 Ultimately, it’s an issue of affordability. There is an abundance of food available. But for an increasing number, it’s out of reach. In March 2024, more than two million visits were recorded at Canadian food banks. That’s a 90% increase in just five years.2 And food banks are a last resort, signalling how dire things have become. Properly supporting and resourcing food banks is critical. However, addressing food insecurity longer term, relies on building a stronger Canadian economy. This includes addressing the affordability crisis, improving productivity, and advancing durable economic development in Canada’s rural and remote areas.

Trade war on food: Rising job loss, costs, and disruptions

Job loss and insecurity is forcing many to make difficult choices

U.S. President Donald Trump’s trade war has caused widespread uncertainty. Launches have been delayed. Production has been paused. Layoffs have been announced. Between January and May, Canada’s manufacturing sector lost 54,000 jobs and the country’s unemployment rate rose to 7%, the highest it’s been since 2016, excluding the pandemic.3 4 Trade exposed industries, including manufacturing, continue to scale down jobs, and now there is greater uncertainty in steel and aluminum jobs with Trump’s 50% tariff on the industry. All this volatility can leave workers in precarious financial situations.

The average Canadian household spent about $76,750 on goods and services in 2023, with 15% and 32% of their money spent on food and shelter, respectively. The lowest income quintile spent $40,080 annually—nearly half that of the average household—with 18% spent on food and 35% on shelter.5 In the event of a job loss—or the fear of potential layoff—Canadians in higher income brackets can cut spending on discretionary items (e.g., new clothes, meals out) in the short term. Lower-income households don’t have that luxury and are left with difficult choices between what basic needs—utility bills, medication, food—they’ll cover. These choices can also impact the quality of food purchased, with lower income households opting for cheaper, lower-nutrient-rich foods.6

Like downturns in the job market, swings in international commodity markets impacted by tariff wars can impact Canadians whose income is directly tied to market prices. Farmers are often price receivers—unable to pass rising costs onto buyers and consumers. And China’s tariffs on agri-food products including canola oil and seafood have recently taken a toll on Canada’s rural economy. Nova Scotia is thought to be the hardest hit by China’s 25% duties on aquatic products, which represented 9.2% of the provinces total export value in 2024. Farmers and fisherpersons are familiar with volatility in the marketplace from bad weather to shifts in demand. Still, ongoing disruptions can erode stability in rural and remote regions that are already at a disadvantage in accessing economic opportunities and services.

And the impact of tariffs is not just about job security. Windsor, Ontario, for example, is reliant on automotive and advanced manufacturing, food processing, and grains and oilseed handling and shipping. This exposes the entire city and surrounding area to Trump’s tariffs on auto as well as China’s retaliatory tariffs on Canada’s agri-food products. Unemployment in Windsor is higher than the national average at 10.8% in May 2025, up from 7.8% in May 2024.7 And the knock-on effects from multiple pressures on employment within a region and rising costs of living can trickle down to local retail and services. As consumer spending tightens, all sectors and their workers are impacted.

Rising cost of living threatens to further deepen the food insecurity crisis.

With rising costs in Canada, a job is no longer a precursor for meeting basic needs. More than 60% of Canada’s food-insecure households rely on wages, salaries, or self-employment income as their primary source of income.8 Workers experiencing moderate to severe food insecurity often occupy low-wage or precarious jobs that are not keeping pace with the cost of living. Visible minorities, women and new immigrants in Canada earn less than the national average. As a result, food insecurity is disproportionality experienced by these groups. More than 46% of black households and 39% of the Indigenous population living off-reserve are food insecure.9 Single-mother households also have higher rates of food insecurity at 52%.10

The effects of food insecurity further marginalize vulnerable groups. Food insecurity is associated with higher rates of chronic diseases, including diabetes and cardiovascular disease. This means more visits to the doctor’s office and the hospital. Severely food insecure Canadians incur health costs that are more than double those who are food secure.11 Food insecurity also impacts the physical and mental development of children, as well as academic performance and behaviour.12 These impacts underline the health and socio-economic costs to families and the Canadian economy.

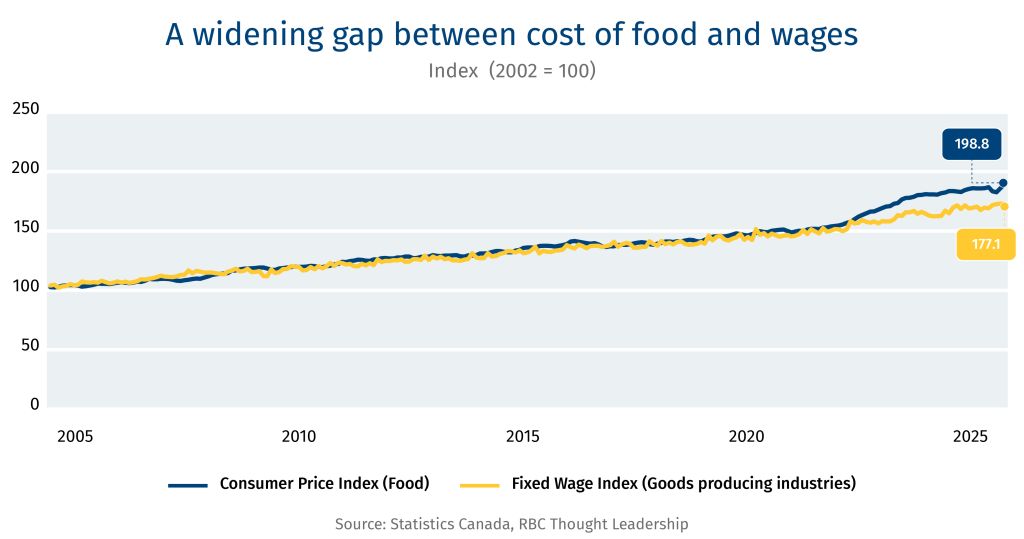

Over the past five years, the affordability crisis has been acutely experienced by households whose wages are not keeping pace with the rising price of goods and services. With pre-tariff inventory coming off grocery store shelves, tariffs are starting to intensify the unaffordability of products in Canada, especially food. Since January 2025, food prices have been a notable driving factor growing the Canadian Consumer Price Index. In April 2025, food prices increased by 3.8% from last year.

Supply chain disruptions impact food consistency and costs

Food companies and retailers reported loses in the first quarter—a direct result of the tariff wars.13 On top of mitigating losses, Canada-U.S. agri-food supply chains are now tasked with additional administrative demands in proving the Canada-United States-Mexico (CUSMA) trade agreement compliance as only two-thirds of Canada’s agri-food exports in 2024 were traded under CUSMA. These stacking complexities and added costs cannot only be absorbed by agri-food suppliers, wholesalers, and retailers, who often operate on thin margins. Eventually rising costs are passed onto the consumer. In the U.S., the impact of tariffs is estimated to increase food prices by 2.6% in the short run, disproportionately impacting fruit and vegetables, that are expected to rise 5.4%.14

Trade wars have sparked a diversification movement. And while trade diversification is a strategy to grow and strengthen Canada’s agri-food exports, it can also result in trade-offs such as short-term uncertainty in quality and cost for consumers while supply chains are being established. Stability and consistency in trade is a key factor in keeping transportation, logistics and operational costs down for traders, wholesalers and retailer, which helps ensure consumers have consistency in price, quality, and availability. Now, uncertainty from tariffs jeopardizes these benefits that North American consumers have become accustomed to through Canada and the U.S.’s interconnected supply chains.

The next step: Tying food solutions to Canada’s growth ambitions

Solutions to food insecurity in Canada are well documented but the issue remains on the sidelines when it comes to large-scale policy and funding commitments.

Potential solutions include:

Address the disparity between Canada’s rural and urban as it relates to access to resources, living wages, and economic development opportunities.

Rebuild Canada’s social safety net to better support low-income households and proactively respond when a household has lost income or has experienced a disruption that impacts its budget.

Improve the affordability of housing.

A food security target may be the catalyst needed to pull these solutions together to drive action across Canada and track progress. This is not a new idea. Food security experts in Canada have called for a 50% target by 2030.15 16 But now is the time to implement a bold vision for food security in Canada as the country sets out to build back a better economy. A key challenge is identifying where food security solutions can be aligned with existing landmark commitments to build momentum. A food secure plan for Canada must also consider how it proportionally improves rates in regions and among groups that are the worst impacted.

Expedite the development of rural and remote community and health services alongside efforts to expedite Canada’s major infrastructure projects. Canada’s ambitions to accelerate major infrastructure projects from the Port of Churchill to the Ring of Fire are primarily concentrated in northern rural and remote Canada. Canada’s rural and remote areas account for 25% of Canada’s GDP but are grossly underserviced when it comes to health care, housing, and other basic needs, including access to healthy food.17 Food insecurity is high across Canada but is highest in northern and remote areas. More than 58% of people in Nunavut experience food insecurity. Further, only 7% of doctors work in rural areas despite the fact Canada’s rural population accounts for 18% of the total population.18

Much of Canada’s plans to build its economic security and sovereignty hinges on having a productive workforce in rural and remote Canada. But getting people to stay in rural and remote areas or relocate for these projects is a tough sell if they can’t access resources needed for their families to lead a healthy life. Canada can help flip the trend of urban areas growing 15 times faster than rural by mitigating brain and resource drain through investments in community resources including access to healthcare, food and housing that match the ambitions of major infrastructure projects.19

Improving access to household financial supports and benefits through policy reform. It is especially timely to advance such reform efforts as the Liberal government has committed to review and reform the process of applying for the Disability Tax Credit (DTC). The DTC is the gateway to key federal programs, including the Canada Disability Benefit, the Canada Child Benefit for children with disabilities, and the dental benefit. This review process is an opportunity to engage Canada’s network of food banks servicing families that rely on DTC benefit to develop practical solutions that work for households, especially those experiencing housing and food insecurity.

On top of qualifying for benefits, Canada’s most vulnerable groups, including those with disabilities and houseless people, are often the hardest to reach populations for tax returns, and have filing rates below Canada’s national average of 92%.20 Unfiled taxes and unclaimed returns account for more than 8.9 million uncashed Canada Revenue Agency (CRA) cheques, totaling $1.4 billion.21 The value of household tax credits won’t solve a household’s financial challenges, but it’s a start.

Building upon CRA’s automatic tax filing pilot and approaches to streamline and simplify tax filing, there is an opportunity to explore support services that better position Canadians to navigate administrative processes to qualify and access credits. And to learn from community organizations including food banks who offer “wrap around services” such as food and financial literacy programming for Canada’s most vulnerable and marginalized populations.

Align food security objectives with Canada’s home building boom. Cutting housing costs can transform a household’s budget. The new federal Liberal government’s plan to build 500,000 homes a year would boost the economy and address a critical need: one of the priority functions of Canada’s forthcoming entity “Build Canada Homes” (BCH) is to build affordable housing at scale. This priority includes a $6 billion commitment for deeply affordable housing including supportive housing, Indigenous housing, and shelters. Complementary to building these homes rapidly and setting homelessness targets with provinces, government could also consider aligning with national food security targets and activities as a measure of their success in affordable housing and enabling people to achieve a healthy, more productive lifestyle that in turn contributes to growing Canada’s economy.

Food insecurity is a systemic problem, requiring systems-based solutions. As Canada embarks on its pro-growth era, it is opportune to consider how its unified approach can be applied to address the most chronic symptoms of a poor economy—food insecurity and poverty.

Experiences and approaches from around the world

Food insecurity affects every country, and over 295 million people worldwide face acute hunger.1 Countries are taking different approaches to measure, monitor, and mitigate the issue, which extends far beyond food programming and policy into income, housing and social equity domains. However, advanced economies like Canada are increasingly expanding food programming to counter the short-term impacts food insecurity is having on communities.

More than 7 million people, or 11% of the population, in the U.K. are living in food insecure households.22 And one-third of children in the U.K. are living in poverty. To tackle this challenge, the government launched a Child Poverty Taskforce.23 The U.K. also has a few notable programs that directly relate to food access such as:

Free school meals program provides meals for children and young people during school with standards on the nutrition of food offered. Complementary to school meals, the UK launched Holiday Activities and Food (HAF) in 2022 to improve access to food and resources during school breaks.24

Healthy Start vouchers in England, Wales, and Northern Ireland support people on low incomes to access pre-natal vitamins, infant milk formula, and healthy food for young children. In Scotland an equivalent Best Start Foods program launched in August 2019.

Household Support Fund: Allocated £1.5 billion in 2022/23 to help with household essentials, including food, energy and housing bills.

The U.K. is also undergoing its largest home building campaign since World War II. The lack of affordable housing and its impact on household stability and spending is a key driver for this building boom. The campaign goes as far as outlining a plan for creating a dozen new towns of approximately 10,000 homes each.25

In New Zealand, 27% of households with children ran out of food often or sometimes in 2023, up from 14.4% in 2021.26 In response to rising rates of food insecurity, New Zealand led the development of a 10-year food security roadmap for the Asia Pacific Economic Cooperation (APEC) covering four key areas: digitalization, productivity, inclusivity and sustainability. APEC includes 21 member countries across the Pacific Rim, including Canada.

Food security research, policy and programming are delivered under multiple ministries in New Zealand, including health, education, and social development ministries, signalling the recognition of food insecurity’s impact on human health and wellbeing. Within New Zealand there has been a growing movement to improve access across its four main regions to resources for basic needs and to improve healthy living standards:

Launch of the Public Health Advisory Committee in 2022, which was asked in 2023 to review New Zealand’s food system and provide advice and recommendations, which are presented in the 2024 report, Rebalancing Our Food System.

New Zealand provides some government funding to maintain community food distribution infrastructure and support regional community food hubs under its Food Secure Communities program, which was established in 2020.

Ka Ora, Ka Ako (Healthy School Lunches Program) was launched in 2019 to provide free lunches to students attending schools in low-income areas. The program is active in over 1,000 schools and provides meals for nearly 240,000 students every day.

Food insecurity affected 47 million Americans in 2023. The U.S. has experienced a similar post-pandemic trend to Canada with the rate of food insecure households rising from 10% to 14% between 2021 and 2023.27 Among those in the OECD, only Costa Rica has higher levels of income inequality. And proposed legislation such as, One Big Beautiful Bill Act, risk worsening inequality in the U.S. by raising national debt and potentially triggering cuts to programs that are designed to reduce food insecurity and improve food access, including:

The Supplemental Nutrition Assistance Program (SNAP) provides a restricted subsidy to purchase food. SNAP serves an average of 42.2 million people per month (12.6% of the US population).28 Participating in SNAP for six months has been shown to decrease food insecurity by 5-10 percentage points and is even more effective for children and those with very low food security.29 30 SNAP has also shown to positively impact local communities’ economic activity and job creation.

The Special Supplemental Nutrition Program for Women, Infants and Children (WIC) provides a restricted food subsidy for pregnant and post-partum people, infants and children up to five years old who meet both income- and nutrition-based eligibility criteria.31 In 2023, the federal government spent US$6.6 billion on WIC program, reaching an average of 6.6 million people per month.32

Statistics Canada. Food insecurity by economic family type, 2025.

Food Banks Canada. HungerCount 2024, 2024.

Statistics Canada. Labour force characteristics by census metropolitan area, three-month moving average, seasonally adjusted, 2025.

Statistics Canada. Employment by industry, monthly, seasonally adjusted and unadjusted, and trend-cycle, last 5 months (x 1,000), 2025.

Statistics Canada. Household spending by household income quintile, Canada, regions and provinces, 2025.

French et al. Nutrition quality of food purchases varies by household income: the SHoPPER study, 2019.

Statistics Canada. Labour force characteristics by census metropolitan area, three-month moving average, seasonally adjusted, 2025.

Li T, Fafard St-Germain AA, Tarasuk V. Household food insecurity in Canada (2022), 2023.

Statistics Canada. Food insecurity by selected demographic characteristics, 2025.

Statistics Canada. Food insecurity by economic family type, 2025.

Statistics Canada, Canadian Community Health Survey (CCHS) 2005, 2007-2008, 2009-2010, Ontario administrative health databases. Adapted from: Tarasuk, Cheng, de Oliveira, Dachner, Gundersen & Kurdyak (2015)

Gallegos et al. Food Insecurity and Child Development: A State-of-the-Art Review, 2021.

The Budget Lab at Yale. State of U.S. Tariffs: April 15, 2025

Food Banks Canada. Joint Open Letter: Cut Food Insecurity in Canada in half by 2030, 2025.

Beardsley, McCain, and Saul. Let’s commit to cutting food insecurity in half, 2022.

Innovation, Science and Economic Development Canada. Rural Economic Development.

Canadian Institute for Health Information. A profile of physicians in Canada, 2025

Statistics Canada. Census in Brief, 2022.