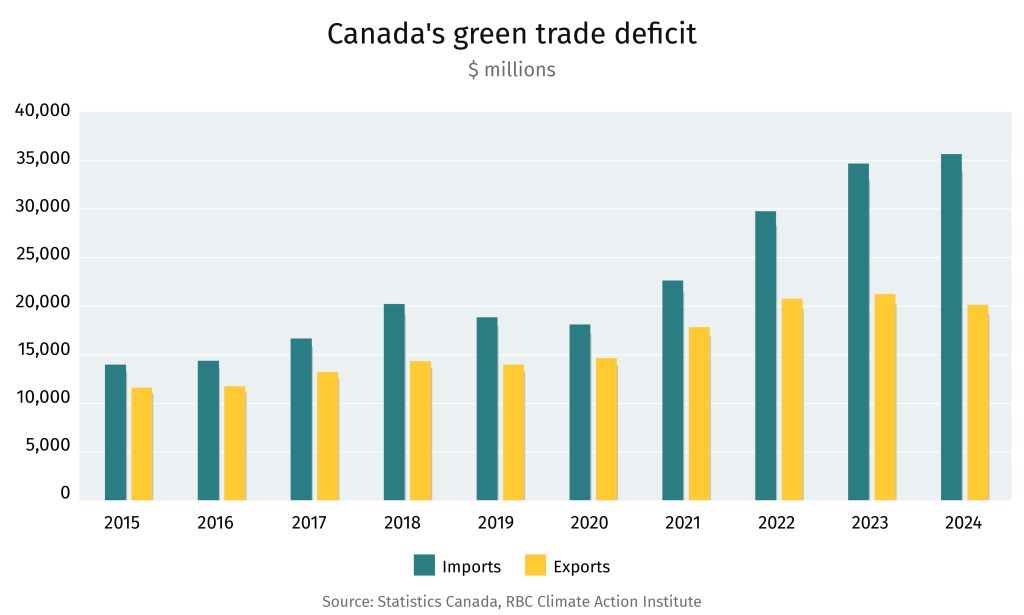

➔ The big fight over methane

➔ Canada is going global with its nuclear ambitions

➔ Why a Canadian municipality paused a data centre project

Signals

Corporates are returning to the fore: Corporate sustainability appears to be turning a corner, with companies demonstrating renewed commitment propelled by the tailwinds described above, says Brian Hong, RBC Director, Environmental Markets Solutions Group, who attended London Climate Week. The breadth of representation across the events—spanning large corporates, financial institutions, investors, government representatives, and NGOs—was another positive indicator. Read his full impressions of #LCAW2026 here.

Canada is an Energy Transition Index laggard. The country, ranked 32nd, dropped one spot in the World Economic Forum’s 120-country index and trails most of its advanced peers (the U.S. is ranked 19th and Australia 26th).Canada’s step down was part of a more sweeping decline in advanced economies on rising energy prices and weaker climate policies.

El Niño is fuelling a cooling crisis. Space cooling is already the fastest-growing energy demand in buildings globally (4% annually), straining power grids. As temperatures remain oppressive, expect AC adoption—and demand for power—to ramp up: only 52% of Canadian renters have AC access, while only 15% of the 3.5 billion people in hot climates worldwide own air conditioners.

Transmission in transition

By Vivan Sorab, Clean Tech Lead

Canada’s electricity strategy is at a critical juncture with policymakers and industry grappling with the push and pull of managing growth and keeping it—mostly—clean.

At the electricity strategy summit in Ottawa, hosted by Natural Resources Canada and Smart Grid Innovation Network, I came away with the following insights:

The action is at the distribution end: New housing is driving a wave of transformer and metering demand, while rooftop solar, EVs, and other inverter-based resources are climbing sharply. Data centres, squeezed by caps such as Alberta’s 1.2-gigawatt limit and global chip shortages, are increasingly seeking to connect at the distribution level.

Affordability is a binding constraint: A hyper-focus on lowest cost is choking the investment the electricity system needs to grow. Yet affordability is also the single greatest threat to political continuity, and with it the durability of any national strategy.

Planning needs to extend beyond the kilowatt-hour. Integrated resource planning optimizes for capacity and energy, but distributed energy resources and demand-side management deliver more than power, boosting local economic development, customer comfort, and household savings. Today, those benefits are not priced properly, some say, and so the distributed solutions that could ease the system are systematically undervalued.

Workforce and supply chains limit what can be deployed and how fast. Deployment forecasts, such as for heat pumps, assume trajectories that available labour and supply chains cannot deliver. The achievable pace will be more modest than headline targets imply. The skills gap compounds this: every retirement removes 30–40 years of expertise, with no systematic upskilling regime to replace it.

Interties and an East-West grid are back on the table. Shifting geopolitics has revived interest in regional integration, but Canada’s grid remains dominantly north-south. Cross-time-zone interties could materially raise the value of renewables by offsetting peaks across the country, though deeper modelling and feasibility work are necessary.

The biggest export opportunity may not be physical. The export conversation fixates on hardware such as small modular reactors and large nuclear components. But Canada has an underused advantage in electrification expertise and grid software.

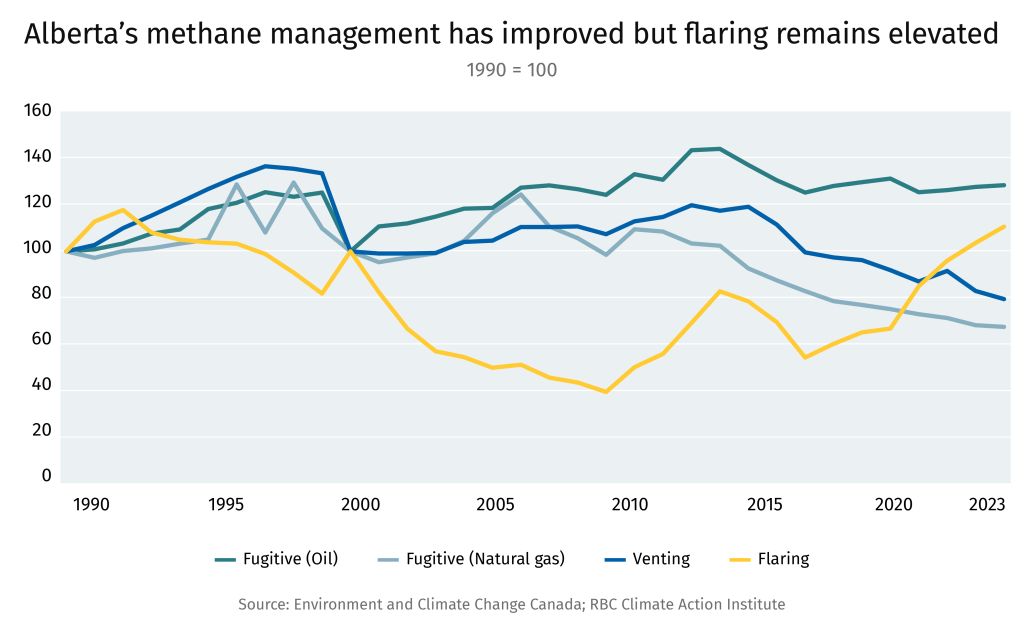

Methane wars

By Shaz Merwat, Energy Policy Lead

The U.S. and Qatar are at odds with the EU over methane import rules. Brussels is holding the line—while quietly suspending enforcement. The framing is now familiar: energy security versus climate ambition.

That could prove to be an advantage for Canada, given its high methane compliance standards. Most major global sources of gas supply anxiety right now have a Canadian answer, says Shaz Merwat, our energy policy lead.

Years of work on methane are yielding results. The Montney is among the lowest methane-intensity gas plays in the world. Enhanced federal regulations finalized in December target 72% below 2012 levels by 2030. The compliance burden the U.S. and Qatar are lobbying against is already baked into Canadian operations.

Chokepoints? Kitimat ships west. No concerns around the current conflict in the Strait of Hormuz, blocked traffic in the Suez Canal, the Panama Canal is running dry, or the future of the Taiwan Strait.

For Canadian operators, methane performance is turning out to be a quieter, cheaper way, with a growing list of buyers who are starting to make it a condition rather than a preference.

A new nuclear ambition

By Vivan Sorab, Clean Tech Lead

Canada’s new Nuclear Energy Strategy leverages its civil nuclear energy legacy for energy security, industrial policy, and exports.

Here are six insights into the scope and depth of Canada’s new nuclear ambitions:

-

New reactors: The strategy targets up to 10 new large reactors (two under construction by 2035, five more planned by 2040), at least one deployment outside Ontario (Canada’s current nuclear stronghold), by 2035, a modernized CANDU design by 2030, and a doubling of the nuclear workforce.

-

A fleet approach: The strategy concentrates regulatory, supply-chain, and construction effort behind specific reactor designs for every use case, helping to standardize deployments, drive down costs, and build a construction track record.

-

It’s about Team Canada: The strategy emphasizes nuclear exports and envisions a unified “Team Canada” export posture with several goals: securing CANDU in at least four new markets by 2040, engaging six to 10 new-entrant countries, and capturing supply-chain share in at least five non-CANDU projects globally. A dedicated Export Financing and Commercial Framework is meant to let Canada compete on sovereign financing, a key driver of nuclear technology exports.

-

Leveraging uranium: Canada is the world’s second-largest uranium producer, and CANDU reactors run on natural uranium, insulating it from the enrichment supply chains that are dominated by Russia. The strategy aims to double uranium exports by 2035. While Canada’s current reactors do not require enriched uranium to operate, Canada’s SMR fleet will require enriched fuel, which the strategy says remains under consideration but will be secured for reactors that require it.

-

Leading with innovation: Nuclear fusion, a defence-led advanced microreactor, and a medical isotope push are also key components of the strategy.

-

The next steps: Execution hinges on financing, supply chain, and jurisdiction. Federal financing policy that defines terms isn’t due until April 2027, and the plan aims to attract private and pension capital that has been hard to mobilize for Western nuclear projects. On the supply-chain side, heavy-water production capacity closed in the 1990s and would have to be rebuilt, alongside heavy forgings and nuclear-grade materials. And provinces, not Ottawa, choose the technology and manage downstream effects, with the federal role being one of signalling and supporting de-risking.

Conversations

➔ Can Canada build more homes and build more defence infrastructure in a climate-smart way? RBC’s John Stackhouse offers some thoughts on the triple play that’s about to be tested as Canada embarks on a new housing expansion.

➔ When municipalities fight back.In a sign of municipal backlash against data centres, Hamilton, Ont., councillors unanimously paused a data centre project on the grounds that it could impact the environment, water use, and affordability. Councillor Nrindr Nann, who led the initiative, said 21 other municipal councils have requested her motion letter.

➔ It’s 25% by 2035. That’s the new proposed climate target for energy consumption intensity in the building sector under the COP31 Presidency of Türkiye. It could strike a chord—and build momentum as rising power bills has emerged as a critical challenge for businesses and consumers.

Curated by Yadullah Hussain, Managing Editor, RBC Climate Action Institute.

Climate Crunch would not be possible without John Stackhouse, Jordan Brennan, John Intini, Farhad Panahov, Lisa Ashton, Shaz Merwat, Vivan Sorab, Caprice Biasoni, Lavanya Kaleeswaran and Joelle Schonberg .

Have a comment, commendation, or umm, criticism? Write to me here (yadullahhussain@rbc.com)

Climate Crunch Newsletter