Key findings

Canada’s Indigenous loan guarantee programs have totalled $1.8 billion across 26 deals1. While utilization remains low at 11%2, it is a meaningful start, reflecting deal complexity and a challenging macro environment.

A core gap exists as a first-mile problem, not a last-mile one. Guarantee programs activate at financial close. Many projects now central to Canada’s economic agenda require Indigenous participation well before that point— before commercial viability is established and long before a community could table a term sheet.

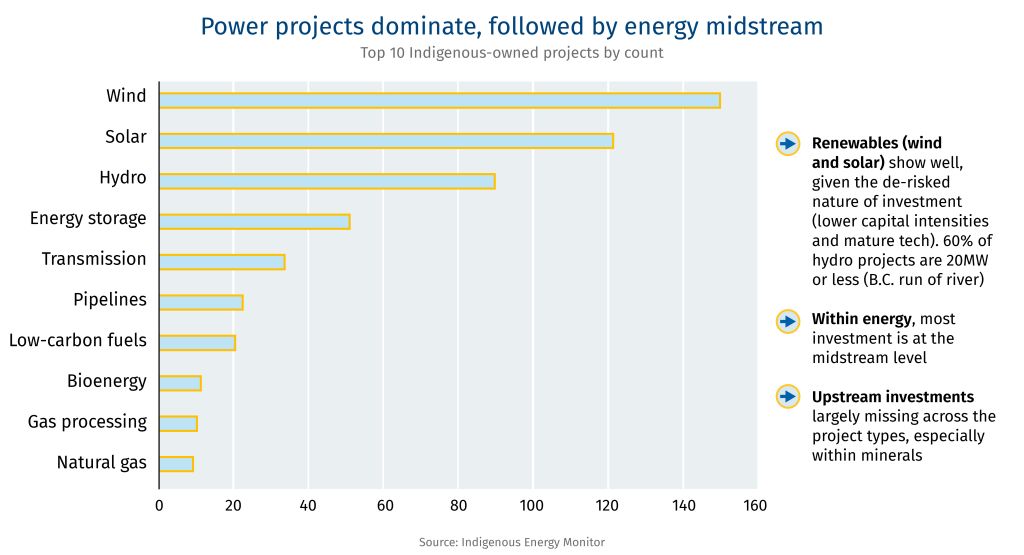

Current programs work best for contracted, rate-of-return assets. Over 80% of prior Indigenous equity transactions are in the power and utilities sector3, often smaller deals supported by dedicated procurement at the provincial level (e.g., power projects in Ontario).

Canada’s next project wave presents a risk profile these programs were never designed to manage on their own. This includes capital-intensive liquefied natural gas (LNG), higher-risk mining, and first-of-its-kind projects like carbon capture and small modular reactors.

Only experienced communities are realistically able to tap the programs. Middle-tier communities that are less transaction-ready remain structurally underrepresented; the programs’ current design risks only reinforces that gap.

Equity is not inherently equivalent to consent. Free, Prior and Informed Consent (FPIC) is a process of informed, voluntary decision-making; equity is a financial structure. Conflating the two creates pressure on communities that is counterproductive—and the regulatory environment reflects that distinction.

Two sovereignties, one economy

Canada is in the middle of a significant economic reorientation. A trade war with the United States, the emergence of new strategic partners, the demands of energy transition, and a renewed focus on sovereignty and security have produced a political consensus that the country needs to build, and build quickly. The federal government has set a target of $300 billion in additional non-U.S. trade over the next decade4. The Major Projects Office has referred 17 projects worth $126 billion for accelerated approval5. Loan guarantee programs at the federal and provincial level now represent more than $17 billion in combined authority to support Indigenous equity participation6. And the capital markets have broadly accepted that meaningful Indigenous partnership is not a regulatory checkbox—it is a condition of project viability.

These are genuine advances. But they share a common assumption worth examining: the tools, timelines, and structures being assembled around Canada’s major project agenda are built for the communities being asked to participate in them. That assumption is not wrong, but it is not always right either.

Indigenous communities are not passive participants waiting to be mobilized into Canada’s economic agenda. They are sovereign entities with their own economic priorities, their own definitions of what is an attractive investment, and their own timelines for building the institutional capacity complex transactions require. Communities generally want an equity interest in projects that serve them directly—assets that provide tangible, direct benefits to their members, that they feel genuine ownership over.

There is appetite among communities to own a share of a pipeline or an LNG terminal. But the nature of that ownership matters—a financial stake in a large (and perhaps distant) infrastructure project is not necessarily the same as owning assets proximate and community-relevant. The fit between the asset, the community, and the nature of participation matters—and it is not a fit Canada’s national project list was necessarily designed around.

This is the tension at the centre of Indigenous economic participation. A tension between two legitimate forms of nation building—Canada’s imperative to diversify its economy and build at scale, and Indigenous communities’ imperative to participate in ways that best serve their people—that overlap but do not always coincide. Given the majority of identified projects exist on or adjacent to Indigenous lands7, getting that overlap right is a key determinant in whether Canada is able to build over the next decade.

Indigenous Loan Guarantees: An early perspective

When Canada’s loan guarantee programs were announced, they generated genuine excitement—and genuine ambition. The federal program alone carries a $10 billion mandate8. Provincial programs in Alberta, Ontario, Saskatchewan, Manitoba and B.C. add another $7 billion9. Together they represent something Canada had not previously offered at scale: a systematic mechanism for Indigenous communities to access capital for equity participation in major resource and energy projects.

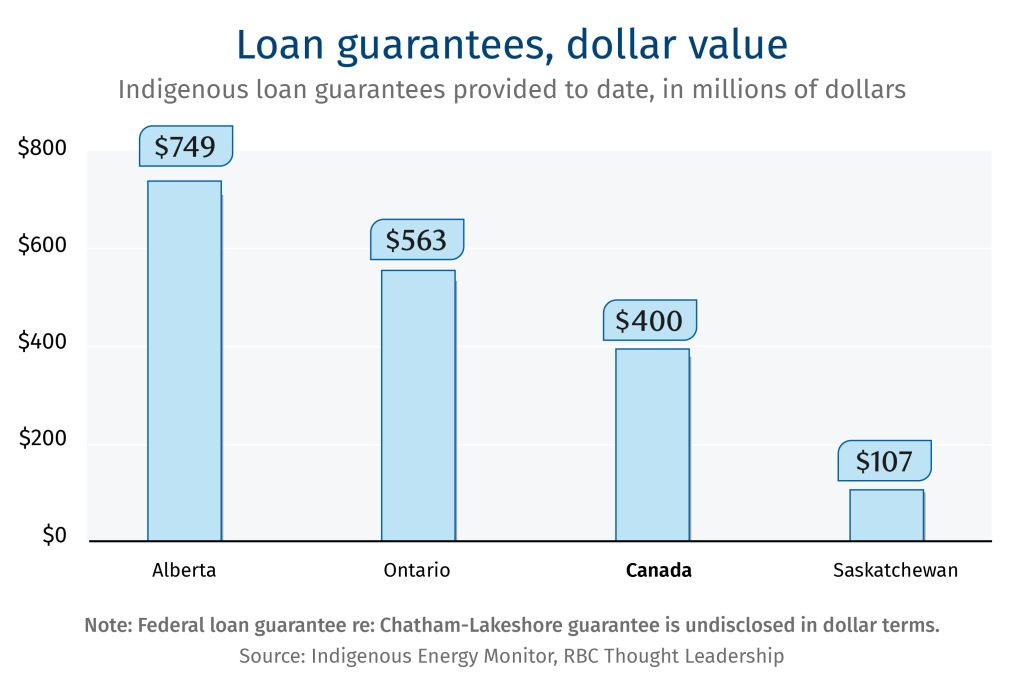

The utilization numbers, viewed in isolation, look modest. To date, 26 deals have been completed across four guarantee programs totalling approximately $1.8 billion deployed, or roughly 11% of combined program authority. Ontario leads by deal count: 13 deals valued at $563 million, running since 200910. Alberta leads by dollar value: 9 deals totaling $749 million since 201911. The federal program, the largest by mandate at $10 billion, has completed two transactions: a $400 million guarantee on a $740 million pipeline deal covering 12.5% of the Enbridge Westcoast system across 38 First Nations in B.C., and a second transaction involving a 20% interest in the Hydro One Chatham-Lakeshore line (dollar terms undisclosed)12. Saskatchewan has completed two deals worth $107 million13. Manitoba has also launched a program.

But the utilization rate deserves context before it invites criticism. These are still young programs. Deals within the resources sector are complex, involving large consortia of communities, evolving project economics, leadership transitions, and trust-building that cannot be compressed by any government instrument. The current macro environment has added further drag: a trade war with the United States, tariff uncertainty, elevated interest rates, and commodity price volatility.

This context matters because it points to something important about what loan guarantees are, and what they are not. A guarantee is not a grant, not direct funding, and not free money. The guarantee is a mechanism that often makes loans possible in the first place, while also reducing the cost of capital by an estimated 50 to 150 basis points (anecdotal evidence suggests)—meaningful when Indigenous communities typically borrow 100% of the acquisition price to take an equity stake.

As such, projects are often rate-of-return assets such as power and utilities projects, transmission lines, and pipelines. Projects with contracted cash flows, predictable debt service, and limited commodity exposure are such that the risk of default is more manageable and protects taxpayer dollars. These assets also suit communities well; levelized, stable payments that can service 100% debt financing without exposing communities to unmanageable volatility.

But what happens when the risk profiles of projects change? LNG is vastly more capital-intensive. Critical minerals have greater commodity exposure and often no contracted offtake. Carbon capture, hydrogen and small modular reactors are still technologically emerging or first-of-its-kind. This risk profile is in stark contrast to the historical transactions seen to date.

According to data from the Indigenous Energy Monitor (IEM), the median Indigenous-owned project is valued at approximately $175 million, and only 15% of projects cross the $1 billion threshold. The Major Projects Office (MPO) portfolio sits in an entirely different weight class, and very likely moves the risk profile well beyond what a loan guarantee was designed to absorb.

Loan guarantees are, by design, a last-mile instrument—they activate when a transaction is commercially viable and a community is ready to close. However, many of Canada’s future resource projects could require Indigenous communities to participate much earlier in the development cycle, before commercial viability is established and long before a community could table a term sheet.

This can create a timing gap: programs activate too late when communities may need support upfront. This first-mile problem is arguably the most important gap in the current architecture.

Five challenges the current architecture has not resolved

Across the ecosystem—programs, financial institutions, proponents, and communities—five structural challenges persist that no single instrument, loan guarantee or otherwise, has resolved and yet is likely required for the next generation of Canadian projects.

1. The banking gap

According to the Bank of Canada’s Survey of Indigenous Firms, only 8% of Indigenous businesses use institutional loans as their primary financing source, compared to 31% of non-Indigenous small businesses. Similarly, loan approval rates run at 58% versus 90%, respectively. This remains a structural impediment.

Financial institutions are still learning how to operate in this space. Deals are still processed individually rather than through standardized templates. Syndication norms are still being established. Banks are not yet fully recognizing the strength of federal and provincial guarantees in the rates they offer Indigenous borrowers—in some transactions, spreads of up to 50 basis points (anecdotal evidence suggests) persists even under loan guarantees.

The friction is most acute in the $5 to $100 million range, where deals tend to be non-recourse, whereas mid-market commercial banking operates on a recourse basis. The rate structure often compounds this–prescribed fixed rate term loans could carry significant interest costs for communities that are 100% leveraged. More flexible structures including floating rates or shorter reset periods could meaningfully improve affordability.

2. The reach problem

The communities most actively using the guarantee programs tend to be those with prior deal experience—established investment arms, legal capacity, and existing lender relationships. These communities return to the programs repeatedly. The less experienced communities with limited institutional capacity are often left behind. Even when capital does flow, many communities lack the internal governance structures needed to manage it effectively. As such, program operators have made meaningful efforts to bring less experienced communities along through consortia structures, in an attempt to offset these structural challenges. Even here, proximity to attractive assets/opportunities remains a key factor.

Many Indigenous communities depend on federal and provincial transfers to fund basic services—housing, education, and healthcare. A persistent concern is that generating own-source revenue through an equity stake can, over time, trigger reductions in those transfers. This is most tangible during pre-revenue when distributions from an equity investment may not arrive for years (construction-stage). That gap is a real deterrent to participation.

Most importantly, Section 89(1) of the Indian Act shields the real and personal property of a First Nation or band situated on reserve from seizure or other enforcement by non-Indigenous creditors, making these assets largely unavailable as conventional collateral. No loan guarantee program, in its inherent design, can alter this core constraint; rather guarantees exist precisely because of it and shape every dimension of how communities engage with capital markets.

3. The scale mismatch

The programs face a structural problem at both ends of the size spectrum. At the small end, sub-$25 million deals are effectively uneconomic. Legal and structuring costs consume a disproportionate share of the benefit at smaller ticket sizes. Yet a meaningful share of Indigenous-owned projects sit in this range. The programs, as currently structured, cannot serve them ‘efficiently’.

With larger deals, capital commitments and risk tolerances are categorically beyond what current guarantee structures were designed to support. Coastal GasLink is a case in point: a 10% equity interest was offered to 16 Indigenous communities in March of 2022, the pipeline entered commercial in-service in November 2024, but the transaction has still not closed. It reflects the complexity involved in managing large consortia of communities across years of changing project economics, leadership transitions, and evolving deal terms.

4. The geographic and sector mismatch

Recently, guarantee programs have been most active in Western Canada, where established infrastructure, mature frameworks, and communities with prior transaction experience have created ideal deal conditions. In northern and northeastern Canada, however, where many critical minerals projects, such as lithium, nickel and graphite are situated, communities are often new to major project participation, are further from existing program infrastructure, and operate without the commercial relationships that western communities have had for decades.

Of 546 Indigenous-owned projects tracked by IEM, only 13 are in mining and minerals despite critical minerals being a stated national priority14. The historically preferred form of Indigenous participation in the mining sector has been royalties and revenue-sharing arrangements—structures that communities have negotiated effectively but are not captured in equity ownership data and are not supported by guarantee programs.

The provincial map is also incomplete. Alberta, Ontario, Saskatchewan, Manitoba and British Columbia have large programs, but meaningful participation is lacking across other provinces. This compounds the geographic and sectoral gap. Generally, provincial support often moves quicker, better reflects regional resource priorities and can carry greater alignment between governments, proponents and local communities on the “acceptability” of desired projects—key benefits that are much harder for Ottawa to replicate.

5. Equity may not mean consent

Mainstream capital markets may have increasingly settled on Indigenous equity participation as a default measure of meaningful reconciliation and a proxy for project consent. Yet, Free, Prior, and Informed Consent (FPIC) is a process of informed, voluntary decision-making and equity is a financial structure. Conflating the two can create pressure on communities that is counterproductive: the sense that accepting equity means consenting to the project, or that declining equity means forfeiting a seat at the table.

Some communities genuinely prefer royalties, revenue sharing, or contracting as forms of economic participation without requiring communities to absorb project risk or service debt. These are legitimate structures that have worked effectively in the Canadian context and deserve to be treated as such. For higher-risk projects such as upstream mining or first-of-its-kind projects, equity is likely not the most appropriate form of project participation (excluding the possibility of investing in enabling infrastructure surrounding a project). Equity partnerships are better understood as a symptom of trust than a condition precedent to it—communities with trusted relationships with proponents move quickly.

Path Forward: Improving and building future tools

The programs that exist are not necessarily failing–they are working within the parameters of what they were designed to do. The question is whether those parameters are sufficient to manage the scale, pace, and risk profile of development aligned with the federal government’s $300 billion aspirations—a next wave of projects representing a category of capital intensity and risk the current architecture was never designed to address alone.

A streamlined template for smaller transactions (sub $25 million) would bring the middle tier of communities into the system without requiring bespoke structuring processes that consume most of the economic benefit (a cited example is how agricultural loan programs operate with standardized terms, allowing banks to more easily process small ticket sizes). Smaller deals done at volume also build institutional knowledge on both the community and lender side that larger transactions can build upon.

Federal and provincial guarantees are not being fully recognized in the rates offered to Indigenous borrowers—at 100% leverage, that gap meaningfully reduces the distributions a community receives. Banks offering improved loan terms would reduce interest costs and improve cash flows.

The most successful multi-community transactions demonstrate that experienced Nations can carry less experienced ones through a process, absorbing negotiation overheads smaller communities cannot manage. Formalizing and resourcing that role would extend the programs’ reach without requiring every participating community to independently develop full transaction capacity.

Capacity investment ahead of the deal cycle is underutilized. Financial literacy training, governance preparation, and pre-transaction advisory support delivered as standing preparation (rather than triggered by a live deal) would move more communities to the threshold where program access becomes realistic.

Budget 2025 allows the Canadian Indigenous Loan Guarantee Program to use convertible debt (e.g. committed at construction, converted to equity once cash flows begin), and it could become the standard approach for greenfield participation. In other instances, creative structuring solutions where proponents can carry communities’ equity during construction (community investments are often 100% leveraged positions) are being explored.

On the incentive side, an Indigenous investment tax credit could directly improve the economics of Indigenous equity participation for proponents. Greater flexibility around stranded tax pools could similarly improve deal economics; Indigenous communities do not pay corporate tax and therefore do not benefit from traditional tax shields, but those benefits could be structured to flow to the corporate partner.

The most significant gap is at first-mile risk. Loan guarantees activate when a transaction is commercially viable but many of the projects needing Indigenous communities’ participation will require capital commitment well before that point. Difficulty in approving and permitting greenfield projects at times is partly a function of Indigenous participation arriving too late in the development cycle.

The use of convertible debt and conditional guarantees (guaranteed financing once key project milestones are reached) are meaningful progress on the timing problem. Still, closing that gap may require a dedicated instrument or facility willing to be first dollar in, absorbing early-stage risk that neither banks nor guarantee programs are designed to take on.

The Canada Growth Fund’s (CGF) role in critical minerals—providing patient sovereign capital to projects that markets alone would not finance—offers a potential model. A comparable mechanism oriented specifically around Indigenous participation in major projects does not yet exist. This would further complement the already existing layered capital stack from CIB financing, First Nations Finance Authority (FNFA) bonds and CGF equity.

Four milestone Indigenous transactions

Stonlasec8 and the Westcoast Pipeline | Federal | 2025

In July of 2025, Stonlasec8 Indigenous Alliance Limited Partnership—representing 38 First Nations in British Columbia—acquired a 12.5% ownership interest in Enbridge’s Westcoast natural gas pipeline system for approximately $736 million. The transaction marked the first loan guarantee issued by the federal Canada Indigenous Loan Guarantee Corporation. CILGC provided a $400 million federal guarantee, enabling the partnership to borrow at significantly reduced cost. The financing was structured in two tranches: the guaranteed senior secured bonds issued for $400 million notional, 30-year term, 4.517% coupon and a separate non-guaranteed senior unsecured bond issuance for $335 million notional, 30-year term, 5.168% coupon, demonstrating how the two instruments can sit alongside each other in the same capital stack. A fixed rate instrument protected communities from interest rate fluctuations over the life of the investment—a meaningful feature for communities that are 100% leveraged and depend on stable distributions.

Clearwater Infrastructure Partnership | Alberta | 2023

In December 2023, Wapiscanis Waseskwan Nipiy Limited Partnership—representing 12 First Nation and Métis communities in northern Alberta—acquired an 85% non-operating interest in Clearwater Infrastructure Limited Partnership for approximately $172 million, backed by a $150 million loan guarantee of the same size. Tamarack Valley Energy retained a 15% operated interest and committed to long-term take-or-pay volume agreements, providing the stable contracted cash flows that made financing viable. CEO-level commitment from Tamarack was central to the transaction. The deal performed well enough that a follow-on expansion closed in September 2024, adding approximately $51 million in additional midstream assets and bringing Bigstone Cree Nation into the partnership.

Wataynikaneyap Power | Ontario | 2024

In December 2024, Wataynikaneyap Power (51% owned by a partnership of 24 First Nations, 49% by Fortis Inc.) completed construction and successfully energized approximately 1,800 kilometres of transmission lines connecting 17 remote northwestern Ontario communities to the provincial grid. Total project cost was $1.9 billion, financed through $1.6 billion in federal support and $680 million in loans from a syndicate of five Canadian banks. Communities that had relied on diesel generation for decades gained access to reliable, lower-cost power. The project won multiple awards and is widely cited as having shifted industry norms, with Hydro One subsequently adopting a policy to offer First Nations up to 50% equity in new transmission projects over $100 million.

Cedar LNG | British Columbia | Under Construction

Cedar LNG is a floating liquefied natural gas facility under construction near Kitimat, British Columbia, within the traditional territory of the Haisla Nation. The Haisla Nation holds a 50.1% majority equity stake with Pembina Pipeline Corporation holding the residual 49.9% — making it the world’s first Indigenous majority-owned LNG export facility. Total project cost is approximately C$6 billion, financed through 60% asset-level debt and 40% equity, with the Haisla Nation funding its 20% equity contribution through the First Nations Finance Authority (FNFA) Agency in 2026—including the issuance of a sustainable bond ($350 million notional, 30-year term, 4.7% coupon) that won Environmental Finance’s Sustainability Bond of the Year. The facility will be powered entirely by renewable electricity from BC Hydro. Operations are expected in late 2028. Cedar LNG does not use a loan guarantee.

Download the report

Author

Shaz Merwat, Energy Policy Lead, RBC Thought Leadership

Editorial

Yadullah Hussain, Managing Editor, RBC Thought Leadership

Lavanya Kaleeswaran, Director, Digital & Production, RBC Thought Leadership

Caprice Biasoni, Design Lead, RBC Thought Leadership

All data sourced from Indigenous Energy Monitor (IEM) unless otherwise mentioned. Indigenous Energy Monitor data is sourced from IEM’s Indigenous Energy Ownership Tracker (IEOT) module.

Indigenous Energy Monitor, RBC Origins

Indigenous Energy Monitor

Indigenous Energy Monitor, RBC Origins

RBC Origins

Indigenous Energy Monitor

Indigenous Energy Monitor

Indigenous Energy Monitor

Indigenous Energy Monitor

Indigenous Energy Monitor

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates. This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/our-impact/sustainability-reporting/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.