Here’s some of what we heard:

1. Climate ambitions are being reset with a focus on what’s doable

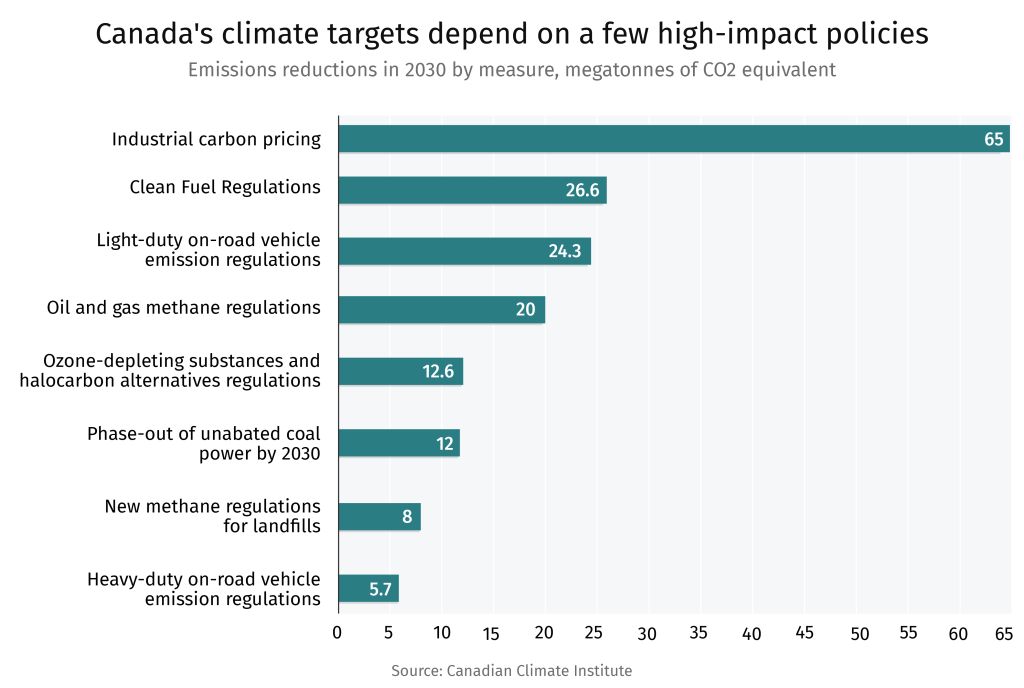

Many of the climate targets set in the early 2020s for 2030 and beyond are becoming harder to achieve – not because ambition has faded, but because short term pressures are colliding with long-term decarbonization plans. Across advanced economies, governments and businesses are recalibrating, prioritizing delivery and near-term feasibility over headline ambition. The result is not retreat, but a reset: a sharper focus on what can realistically be built, financed, and scaled this decade.

While climate change is still on the mind of Canadians, concern truly intensifies when climate impacts intersect with immediate issues of health and safety—in particular, when it comes to wildfires. The intersection of climate risk and daily life is reshaping policy debates and what climate actions need to be prioritizing in the short-term. Governments are increasingly exploring how to align climate policy with how Canadians are experiencing environmental effects, as well as macro issues including affordability, energy security, and industrial competitiveness, rather than treating climate action as a separate agenda.

2. There’s plenty of climate capital. The challenge is deploying it.

There are $100 billion of government incentives budgeted between now and 2035 for clean-tech and climate programs, according to our estimates.1

The problem is that industry leaders find many Canadian climate funds “untouchable” or with transaction costs that are too high. For example, stakeholders in the mining and clean technology sectors struggle to access programs like the Low Carbon Economy Fund, citing bureaucratic hurdles such as complex granting processes. Stakeholders said this challenge is systemic across climate programs and incentives. Notably, the Auditor General found that the federal government’s recently retired Net Zero Accelerator, an $8-billion fund, attracted only 15 out of the 55 largest-emitting companies in Canada and resulted in just two signed agreements by late 2024. The biggest barrier cited was the lengthy and complex application process, averaging 407 hours.2

Leveraging AI applications was suggested by industry as one option to help streamline project review processes and synthesize project data, reducing the administration burden for governments and applicants. AI powered government administration is a trend that has a growing list of working examples, like DAISY, the Development Application Information System, in New South Wales in Australia that helps local councils and project developers accelerate approval processes.

3. Policy friction and geo-political uncertainty threatens Canadian climate competitiveness

In an era marked by protectionism, shifting alliances, and supply-chain risk, the idea that Canada can compete globally on climate ambition alone can feel aspirational. Yet, for emissions-intensive, trade-exposed sectors, climate competitiveness is less about idealism and more about whether decarbonization can tangibly support growth, resilience, and market access.

Canada’s steel sector illustrates that tension. Over the past year, steel sector exports fell 24%, as the industry saw reduced revenues and demand, and more than 1,000 direct jobs lost, moving long-term 2050 net-zero targets lower on the priority list for companies.3 Yet, decarbonization opportunities that are clearly aligned with growth and market prospects help make the case for climate competitiveness. The U.S.’s 50% tariffs on Canadian steel accelerated plans for Algoma Steel to transition production from traditional blast furnaces to electric arc furnaces, which use electric power instead of coal, allowing for a more flexible, lower-cost operation that is more competitive under trade pressure. Yet, this switch did not come without tradeoffs, including large upfront investments and scaling down employment.

British Columbia’s timber industry exemplifies a sector hit hard by tariffs, but with the potential to bolster Canada’s climate competitiveness ambitions. After a long downturn fuelled by mill closures, pest outbreaks and wildfires, the timber industry is seeking bounce back opportunities through new markets that can boost demand. Mass timber could be an option.

As a low-carbon material, mass timber can reignite domestic production, feed the modular housing boom, and decarbonize the building sector. To succeed, federal, provincial, and municipal governments must prioritize low-carbon procurement, adopt “tall wood” building codes, and streamline project permitting.

Canada climate competitiveness in other sectors hinges on getting major projects off the ground. Despite holding the world’s sixth-largest lithium reserves, and substantial deposits of nickel, cobalt, and rare earth elements, Canada is not a major player in producing the materials that are essential to batteries, wind turbines, and electric vehicles.4 While Natural Resources Canada has identified critical minerals as central to economic growth and climate strategy, mining projects remain hindered by capital gaps and long permitting timelines. Geopolitical fragmentation complicates market access and financing for Canadian projects. For investors, climate alignment alone is insufficient. They require regulatory clarity, infrastructure readiness, Indigenous partnership certainty, and long-term offtake agreements. Without streamlined approvals and coordinated federal–provincial policy, Canada risks failing to leverage its mineral wealth for the global energy and industrial transformation.

Climate competitiveness could be a fantasy if Canada can’t pass the test of reducing policy friction and mitigating geopolitical uncertainty fast enough to make climate alignment the simplest path to growth in resource-based sectors.

4. A national electricity strategy requires a major shift in priorities

An imminent pan-Canadian electricity strategy is set to map a plan for expanded power generation and remove barriers between provincial markets.

According to our estimates, expanding electricity generation by 2050 by low-emission sources including nuclear, hydroelectric and abated natural gas in addition to solar and wind, would cost over $1 trillion.5 Canada’s surging electricity demand is a hot topic as industry leaders and consumers grapple with the current bill to meet demands, like Toronto Hydro’s $5.9 billion investment plan for 2025-2029. The pressing upgrade highlights the strain on existing infrastructure to support electrification (e.g., heat pump adoption).

The availability of reliable renewable power to meet rising demand is a central concern, particularly as the economics of developing low-carbon generation are not consistently viable across Canadian jurisdictions, challenging the national goal of fully decarbonizing electricity systems by 2050. Existing infrastructure and cost barriers mean natural gas continues to play a significant role and is expected to remain the dominant heating source in many provinces including Alberta, Saskatchewan and some Atlantic provinces. On the demand side, affordability is often the primary driver for households considering a switch to low-emitting technologies such as heat pumps. However, in provinces like Saskatchewan, where subsidies for fuel switching are limited or unavailable, homeowners often cannot justify the upfront investment required to adopt low-emission solutions. Without supportive policy measures or improved economic incentives, the financial case for transitioning to cleaner technologies remains challenging for many households.

Scaling energy supply to meet demand and deliver on a pan-Canadian vision requires a shift in priorities to “build big things,” focusing on infrastructure like the East-West energy grid and major climate projects. However, projects have yet to get off the ground raising questions if big and bold is possible, or if the small and fragmented tradition of Canada’s federation will persist.

Other countries are finding ways to meet their economies’ rising power needs. In 2024, China added approximately 543 gigawatts of new electricity capacity, according to their National Energy Administration. The power generation added since the end of 2021 in China now exceeds the size of the entire U.S. power system. While Canada’s needs are proportionally smaller, the comparison highlights the speed required to compete in clean energy manufacturing, supply chains, and technology deployment.

5. Too many shovel-ready carbon removal solutions are waiting to scale

Canada’s forests, wetlands, and agricultural lands can reduce Canada’s emissions by up to 78 megatonnes of CO2e in 2030 if sustainable management and conservation are enabled.6 Unlocking these nature-based solutions requires scale. Projects must achieve economies of scale to go through the costly process of being verified on functioning markets to deliver real value to land stewards, such as farmers. Projects must also provide the value of scale to investors looking for large single purchases of credits or claimed impacts. It’s ironic that despite Canada’s vast natural landscape, a lack of operational scale remains the primary barrier to delivering market-based incentives.

Aside from the Conservation Cropping Protocol in Alberta that has since been retired and the Great Bear Rain Forest, there are few Canadian examples of scaled market-based approaches to incentivize nature-based solutions. Fragmented carbon pricing systems and rigid protocol design are key hinderances that have slowed progress in Canada. However, the current review of Canada’s industrial carbon pricing benchmarks, and bilateral agreements such as Alberta’s memorandum of understanding with the federal government, present an opportunity to test policy designs that can unleash investment for nature-based solutions.

6. Capitalizing on climate-conscious consumers critical to decarbonization

Despite rising national security threats, affordability concerns, and an economic downtown, roughly 33% of Canadians still list climate change as one of their top three concerns, according to our consumer survey.

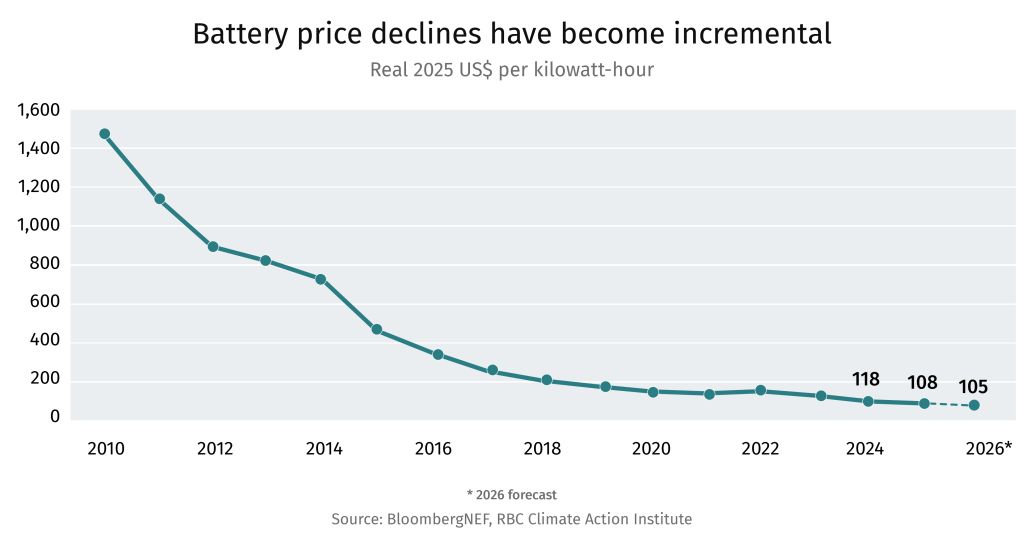

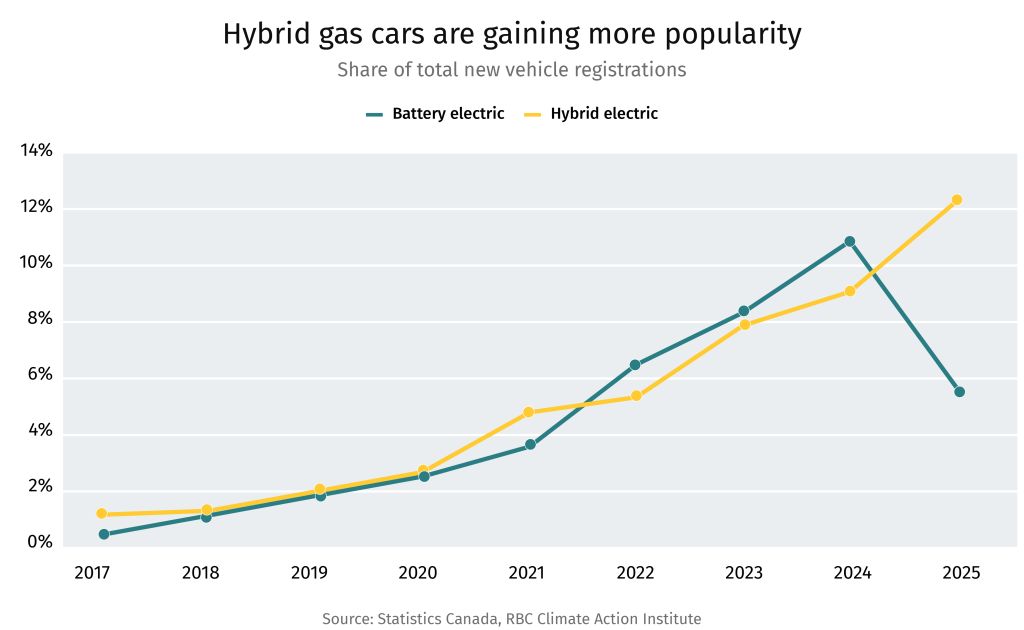

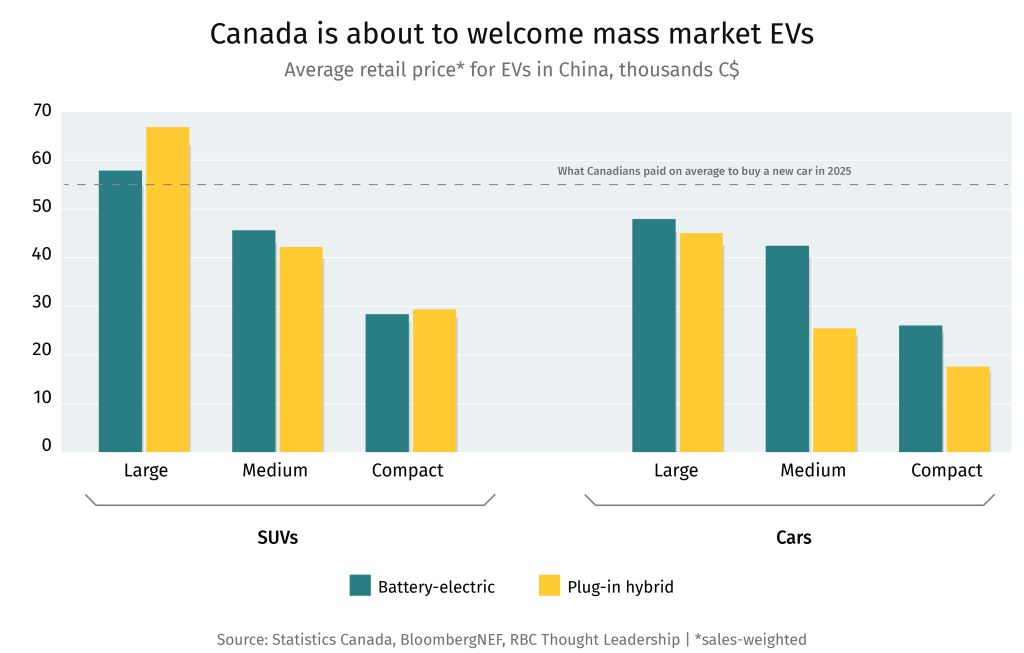

Consumer demand represents a critical lever. Adoption of technologies, such as heat pumps and electric vehicles, would accelerates once the economics make sense, in the form of rebates, clear price signals, and stable policy frameworks. Businesses and policymakers can harness this demand by aligning climate policy with affordability and competitiveness for consumers.

Major infrastructure projects—such as new transmission corridors, clean-tech manufacturing hubs, or carbon management systems—require public trust to move from proposal to implementation. Without social licence, even technically sound projects stall. Building that trust means demonstrating tangible benefits: job creation, lower long-term energy costs, improved reliability, and enhanced resilience to climate impacts.

Canada’s climate challenge is increasingly a question of scale and delivery. Ambition remains important—but execution, coordination, and trust will determine whether the country can translate targets into tangible outcomes.