Why we wrote this

Canada is on the edge of a building boom. With our housing stock already severely strained, we’ll soon need to find a way to accommodate a record surge in new Canadians. That’ll mean building nearly six million new homes.

Constructing these homes sustainably—as we must if we are to hit our climate targets—brings with it economic opportunity. Canada can lead North America’s construction sector into a new greener era, one defined by novel building materials, smart building systems and the rapid deployment of low-carbon heating and cooling. In addition to the buildings themselves, we’ll need to construct new supply chains, skilled workforces and critically a retrofit economy to support the transition.

This challenge compelled the RBC Climate Action Institute and George Brown College’s Brookfield Sustainability Institute to launch a collaboration that begins with this paper. High Rise, Low Carbon: Canada’s $40 billion Net Zero Building Challenge aims to help inform and inspire Canadians to see both the urgent need and growing opportunity that will come with more sustainable buildings.

John Stackhouse, Senior Vice President, Office of the CEO, RBC

Luigi Ferrara, Chair and CEO, Brookfield Sustainability Institute

Key points

-

By 2030, Canada will need 5.8 million new houses—a 40% increase—as the current housing affordability crisis and immigration boom accelerate demand.

By 2030, Canada will need 5.8 million new houses—a 40% increase—as the current housing affordability crisis and immigration boom accelerate demand. -

If built with current practices and prevailing codes, these structures will add up to 18 MT (million tonnes) of greenhouse gas emissions to our carbon footprint annually.

If built with current practices and prevailing codes, these structures will add up to 18 MT (million tonnes) of greenhouse gas emissions to our carbon footprint annually. -

Emissions from production of the cement and steel used to build them will add even more.

Emissions from production of the cement and steel used to build them will add even more. -

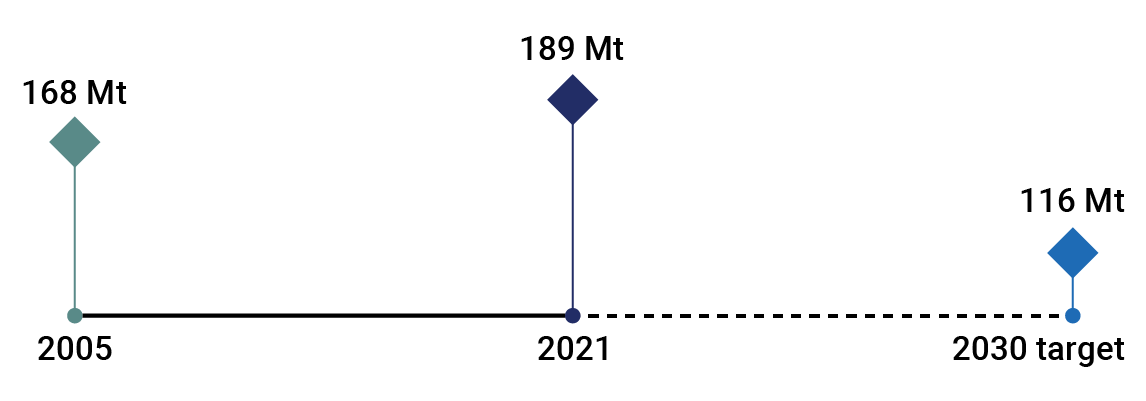

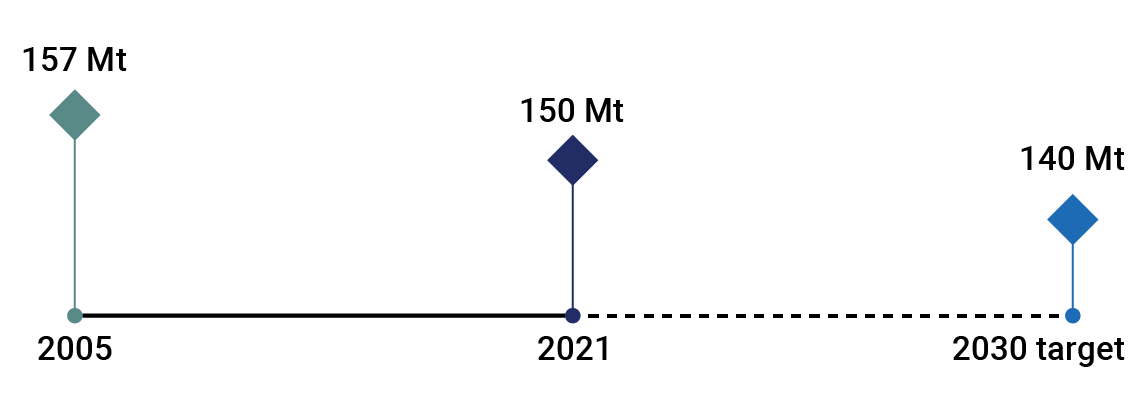

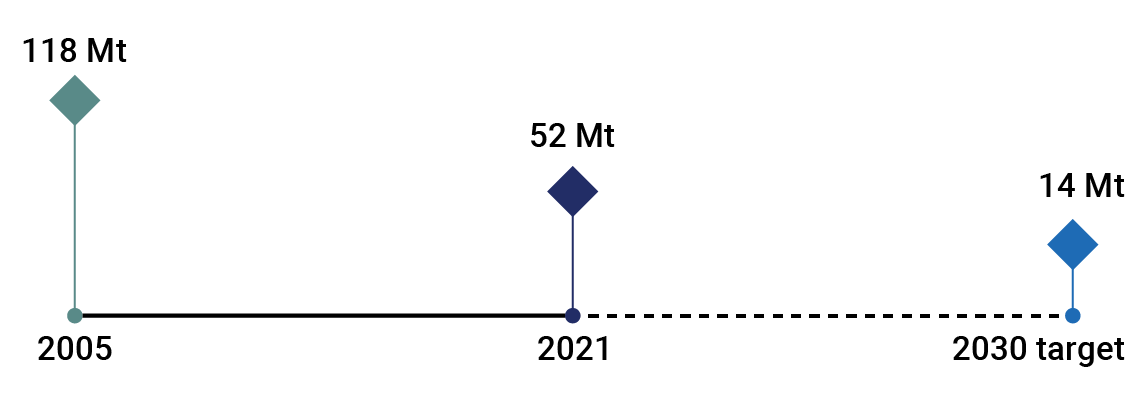

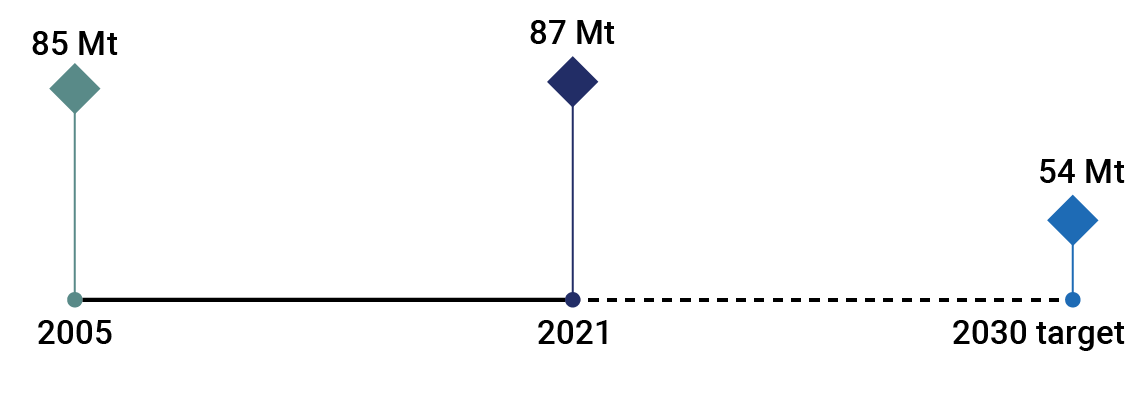

Canada’s existing buildings are already among our biggest emitters, releasing some 90 MT of greenhouse gases annually.

Canada’s existing buildings are already among our biggest emitters, releasing some 90 MT of greenhouse gases annually. -

To meet our Net Zero targets, we’ll need to change how and what we build. We’ll also need to re-visit our current buildings—retrofitting some 16 million homes and 750 million m2 of commercial space.

To meet our Net Zero targets, we’ll need to change how and what we build. We’ll also need to re-visit our current buildings—retrofitting some 16 million homes and 750 million m2 of commercial space. -

This will require more than $40 billion a year in capital investment, with 60% going to retrofits and the rest to new builds.1

This will require more than $40 billion a year in capital investment, with 60% going to retrofits and the rest to new builds.1 -

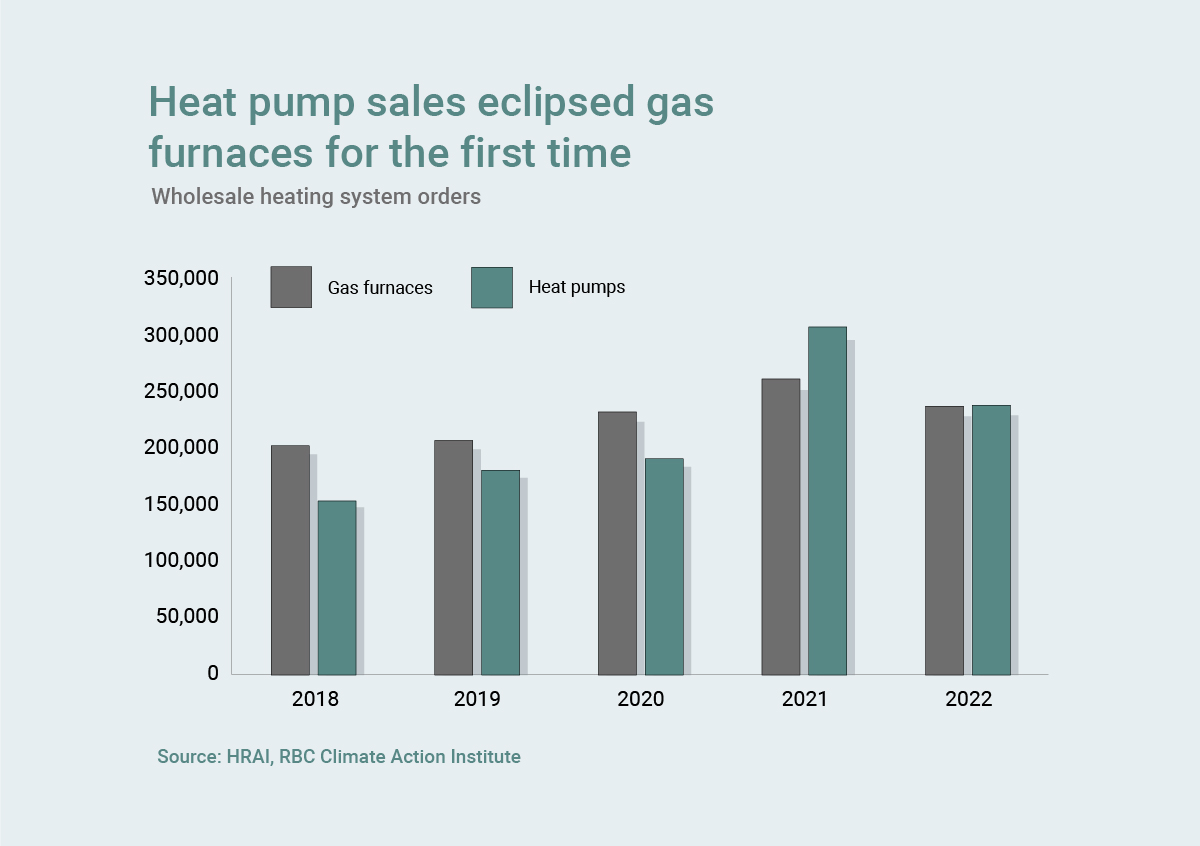

New technologies will be essential. Heat pumps—already gaining traction in Atlantic Canada and B.C.—must become mainstream, augmenting and eventually replacing gas furnaces that are the largest source of building emissions.

New technologies will be essential. Heat pumps—already gaining traction in Atlantic Canada and B.C.—must become mainstream, augmenting and eventually replacing gas furnaces that are the largest source of building emissions.

Key Charts

Seven Ideas

Provinces should set progressively tighter emissions standards for new and existing buildings.

Codes for new construction must tighten quickly, and emissions permitted in existing structures should decline gradually according to a transparent but ambitious schedule. Sales of emissions-heavy technology and materials should be phased down according to that schedule.

Building owners must collect and share emissions and retrofit data.

A national open-access database showing the impact of various retrofits across all building types can help owners make capital plans to meet the aforementioned standards. Governments at all levels should help share the cost of the database.

Utility commissions must send the right price signals.

Provinces can use electricity rates to encourage the installation of heat pumps in large buildings and conservation and demand shifting in small ones.

Target affordability with mortgage insurance, lending, and land-use regulations.

Ottawa should allow longer maximum amortization for insured green mortgages and fund larger direct subsidies for low-income heat pump buyers. Municipal governments should lower development charges and increase allowed density for green buildings. Banks should study how lending criteria can evolve to help homeowners afford more expensive green homes.

Municipalities should create low-carbon design districts.

Designate areas, rather than specific sites, for low-carbon building types (e.g., mass timber, innovative concrete, prefabricated homes) to rapidly scale pilots.

Upskill workers, boost labour supply, and adopt innovative new designs.

Unions and employers can collaborate to train workers in labour-saving building methods. The federal government can better target immigration policy to attract newcomers with the right building skills.

Industry can partner to secure heat pump innovation and supply.

Industry groups can target other cold countries to improve and lower the costs of cold-climate heat pumps. Governments can support trade missions and encourage domestic production of pumps and components, in part through synergies with other existing Canadian manufacturers and innovators (e.g., auto parts makers).

The case for greening Canada’s built environment

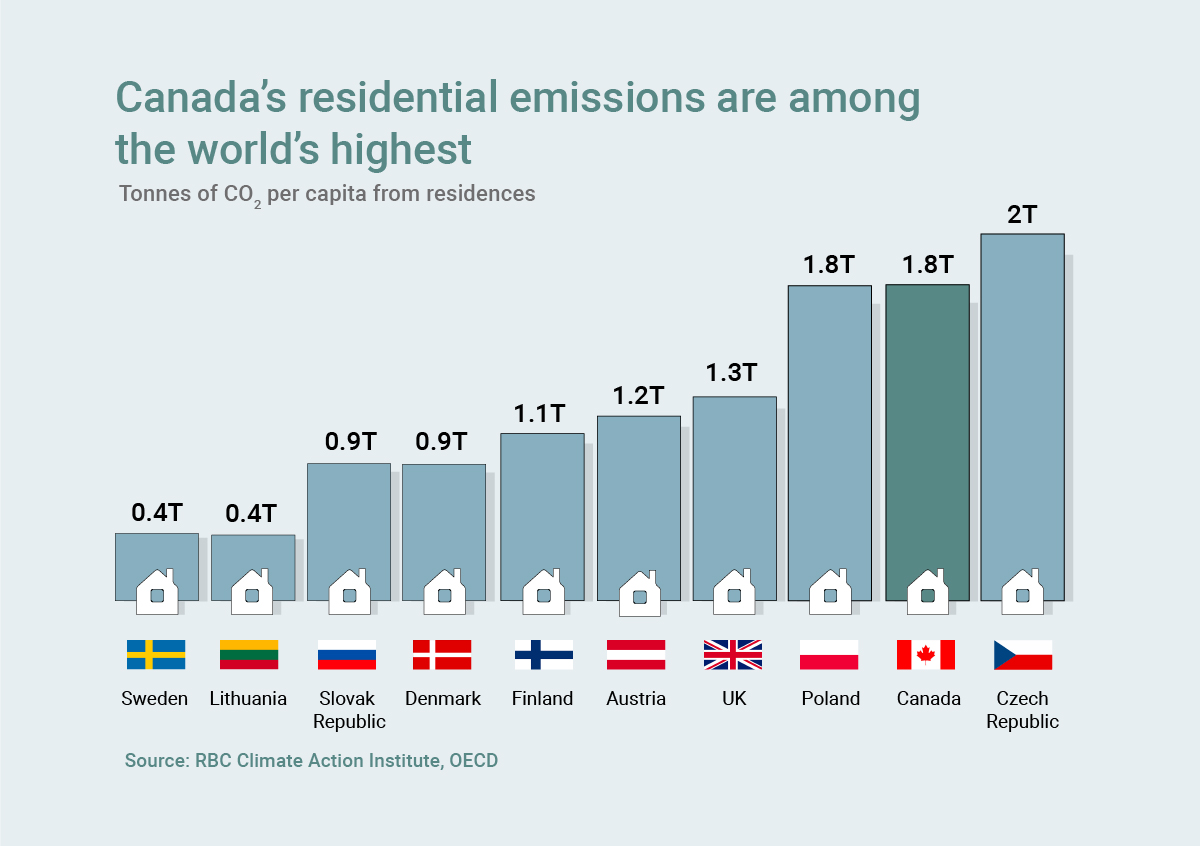

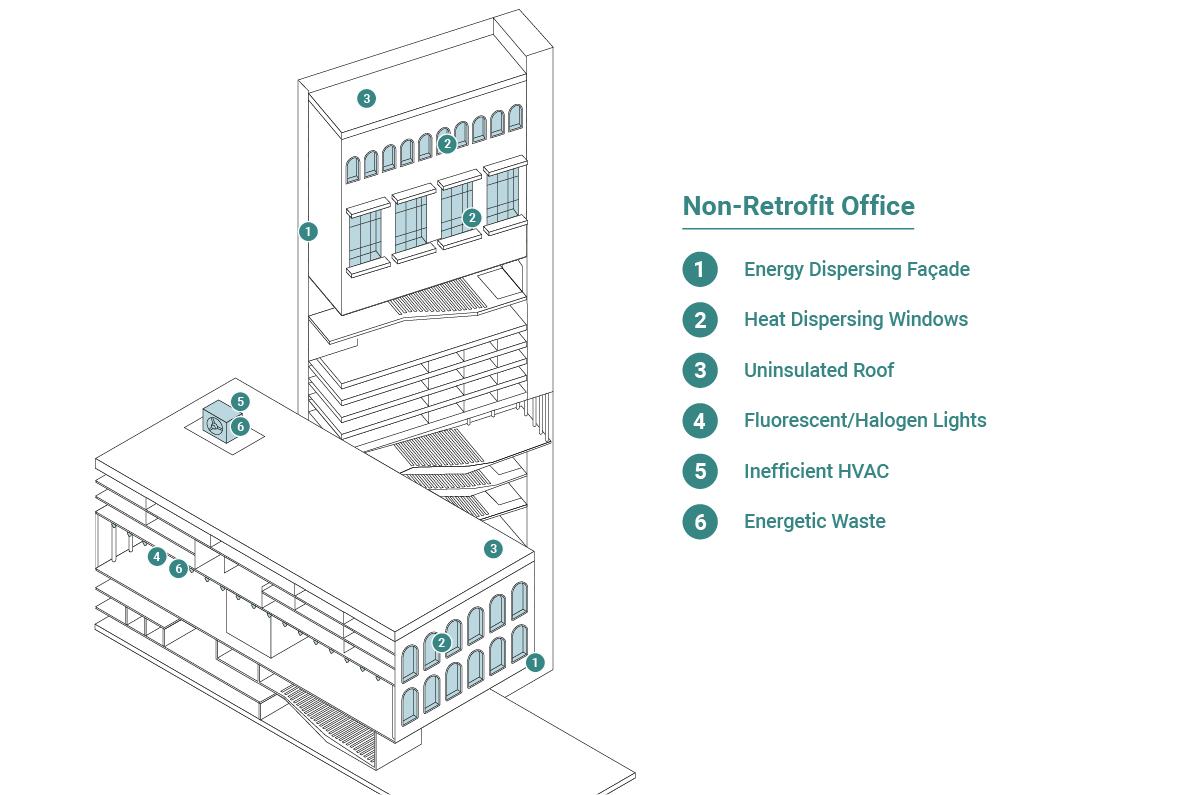

Buildings have long been at the heart of Canada’s emissions problem.

Heated by gas furnaces, powered by coal-fired electricity, and supported by emissions-heavy concrete foundations, our buildings are the third largest source of greenhouse gases after the energy and transportation sectors. In all, they generate an eighth of our emissions, or some 90 million tonnes (MT) of carbon dioxide each year. And those emissions are rising, as more houses and commercial spaces heated with natural gas are built.

To reach our climate targets, we must build in a new way. Through design and retrofits, we can do more than cut emissions. We can turn our buildings into powerful drivers of the green transition, acting as charging stations for electric vehicles, generators of solar power, and carbon sinks that protect emissions stored in raw materials.

Canada’s “built environment”—the shopping malls, homes and office towers central to our lives—is critical to the economy. Construction and real estate services directly account for a fifth of GDP, with commercial buildings supporting broader economic activities ranging from retail stores to assembly lines. But nearly half of our housing stock was built prior to 1980, when energy efficiency wasn’t a top priority. What’s more, Canada’s frigid climate and abundance of natural gas has long led us to heat our homes generously, with little need to focus on emissions.

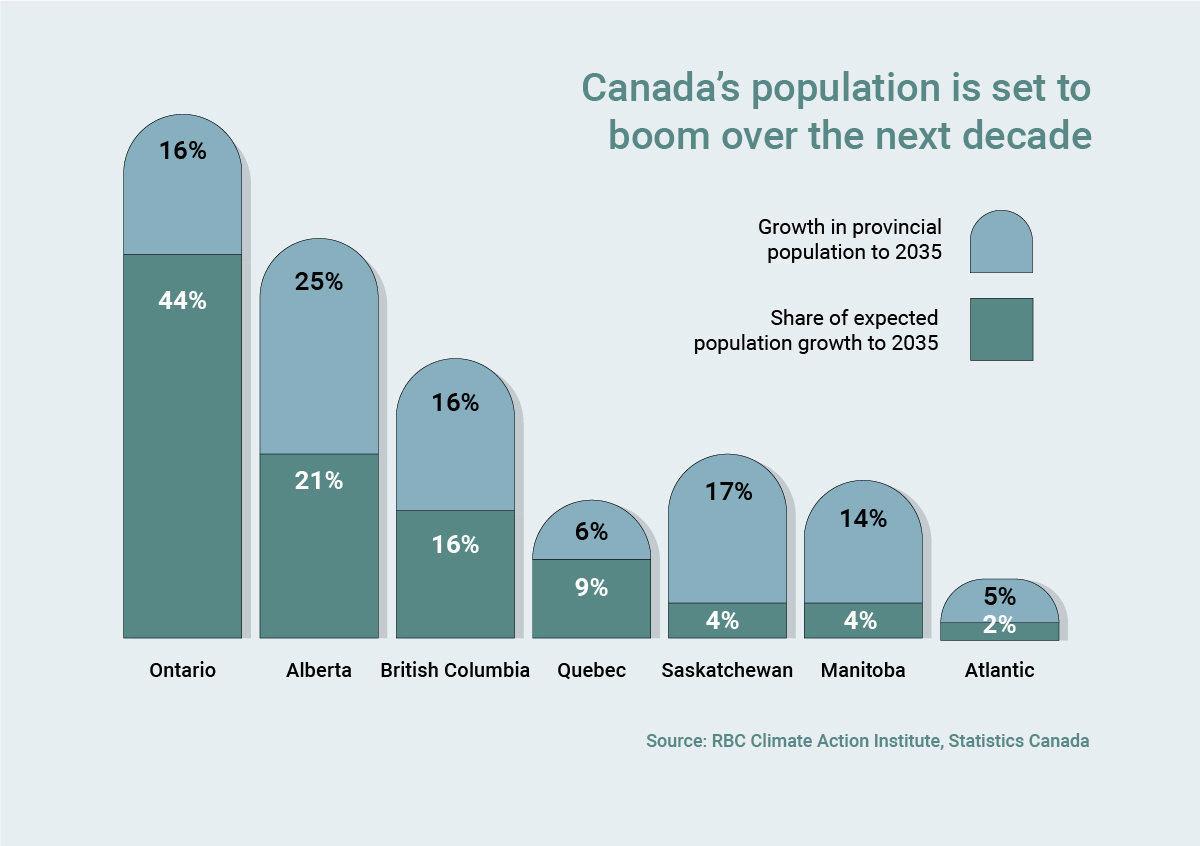

Until now. Our existing housing stock is already well short of what Canadians need and soaring prices are placing home ownership increasingly out of reach. With record immigration targets set to bring 5.5 million newcomers to Canada by 2035, we’ll need to expand our housing supply by 40% in the next 10 years—without raising emissions.

The scale of this task may be daunting, but it also gives us a chance for a fresh start. And some Canadian companies are seizing it, taking a lead in the development of climate-smart building technologies. Element5, in St. Thomas, Ont., produces mass timber technology that glues wood together in layers strong enough to replace traditional steel and concrete in buildings. B.C.’s QuadReal is turning a Toronto warehouse into a solar farm, fitting the roof with reams of panels that will ultimately power electric delivery trucks. And Toronto’s Morgan Solar is designing window blinds that double as solar panels. Canada can lead North America by exporting these smart building solutions, growing the economy, and cutting our own emissions along the way.

The challenge for our builders will be to make such low-carbon innovations part of business as usual. They’ll also have to work with living spaces that are larger compared to most developed countries.

Labour shortages, strained electricity systems and stressed supply chains for new technologies will present significant barriers. So too, will the added consumer cost of building green. As living costs rise, every added dollar will weigh on Canadian households.

But building the way we always have will bring its own financial burdens, in the form of future retrofits and heftier carbon prices. We can’t afford to wait any longer.

Creating climate-positive communities

New communities are a chance for designers to develop neighbourhood-scale solutions that move us more rapidly toward Net Zero.

A “climate-positive community” adopts nature-based solutions, circular economy practices, and renewable energy. It designs for durable, flexible buildings, and the conservation of ecosystems. And it supports residents in adopting simple living philosophies, sharing economies and communal smart systems.

These communities typically favour public transport, smaller homes, and higher-density neighbourhoods that allow residents to live, work and play within a walkable radius. They usually integrate a variety of uses and tenancies, develop a network of natural and human-scaled paved spaces, adopt community-run co-housing features, and incorporate renewable energy systems and smart solutions to cut energy use.

London’s Bedzed, among the world’s first climate-positive communities, features 100 homes, a college, offices, and various community facilities. Local and recycled materials were used in its construction and its district heat system and passive house design have helped cut emissions by half for transportation and a third for heating. Water use was reduced by two thirds. That’s led to significant savings for the residents, whose annual bills are £1400 lower than that of the average Londoner.

Source: The Bedzed Story

New builds vs. retrofits:

A new pathway and a long grind

New buildings offer a unique chance to reimagine our built environment.

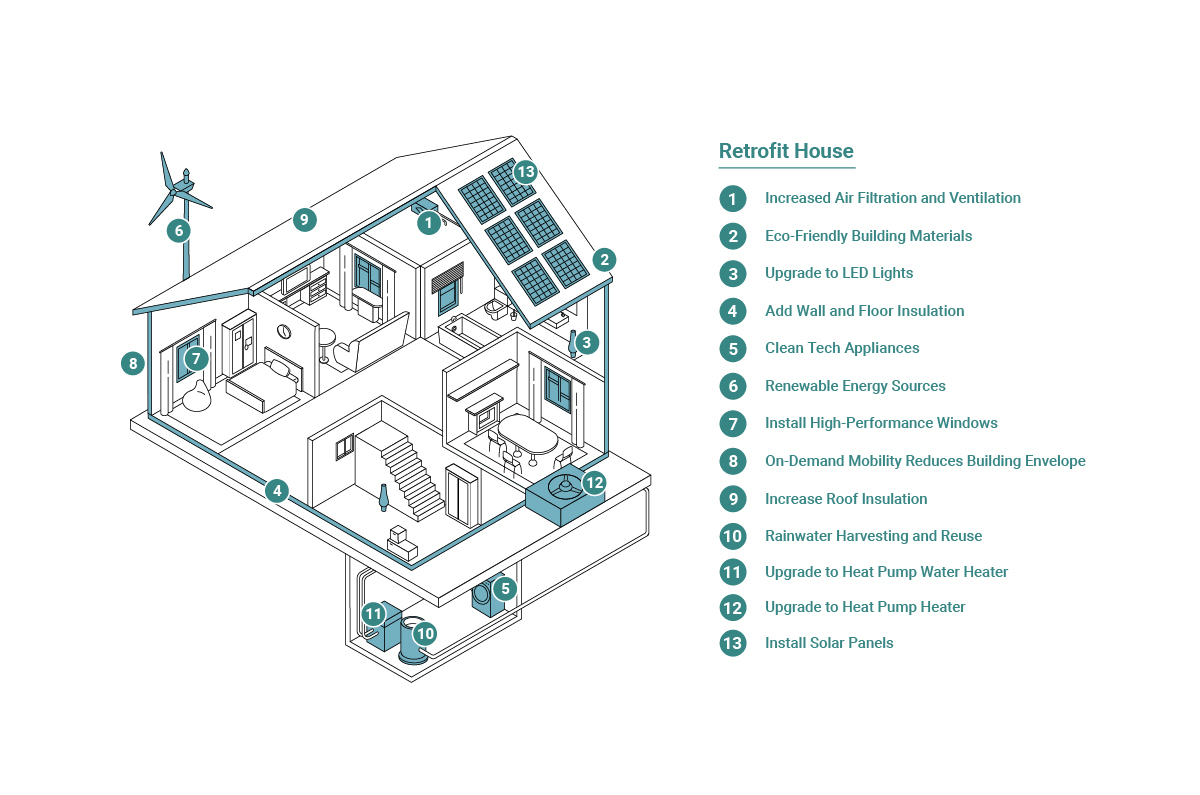

From the outset, communities and structures can be designed to be more energy-efficient and resilient to the physical threats and costs of climate change—like heat, floods, and wildfires. Starting from scratch, developers can more affordably create tighter “envelopes” or structures that allow less air and heat to escape. They can also design around more energy-efficient technologies like heat pumps, which move heat from the outside air, water or ground and transfer it for use inside. This allows savings to materialize faster. And since heat pumps can both heat and cool spaces, this technology can also eliminate the need for both a furnace and an air conditioner in many parts of the country, cutting costs even further.

These operating savings can do much to offset the added 5-10% upfront cost of constructing sustainable buildings. Mortgage policy changes (think longer amortization for insured mortgages on zero emission homes) can do even more. Meantime, a level regulatory playing field across municipalities, where building codes are equally supportive of Net Zero buildings, can ensure all builders face the same costs and meet the same standards.

A bigger challenge rests in what’s known as “embodied carbon”. These are the emissions produced in the manufacture of building materials (such as cement for new foundations and glass for new windows). By some measures, these account for 11% of global emissions,2 and can add up to nearly two decades of emissions from operating the building.

Fortunately, some of the most exciting innovation is happening in this arena. Using wood in tall buildings allows the carbon stored in trees to effectively be locked up for 100+ years, and studies suggest it also reduces heat loss, making it easier to cut operating emissions, too. Innovations in concrete can increase the carbon it stores and 3D-printed or prefabricated buildings can dramatically reduce the amount of materials wasted. More materials are currently in development: researchers in the UK, for instance, are growing structures out of mycelium, sawdust, and wool. Not all of these innovations will be scalable, but we need to invest heavily in the most promising ones.

Current regulations are a significant barrier. To build a ten-story mass timber building, architects at George Brown College in Toronto needed special exemptions from building codes. That took four years, much longer than the expected total construction time of the building itself. We’ll need to accelerate timelines and learn from global peers. The Europeans, for example, have three times as many tall mass timber buildings under construction.

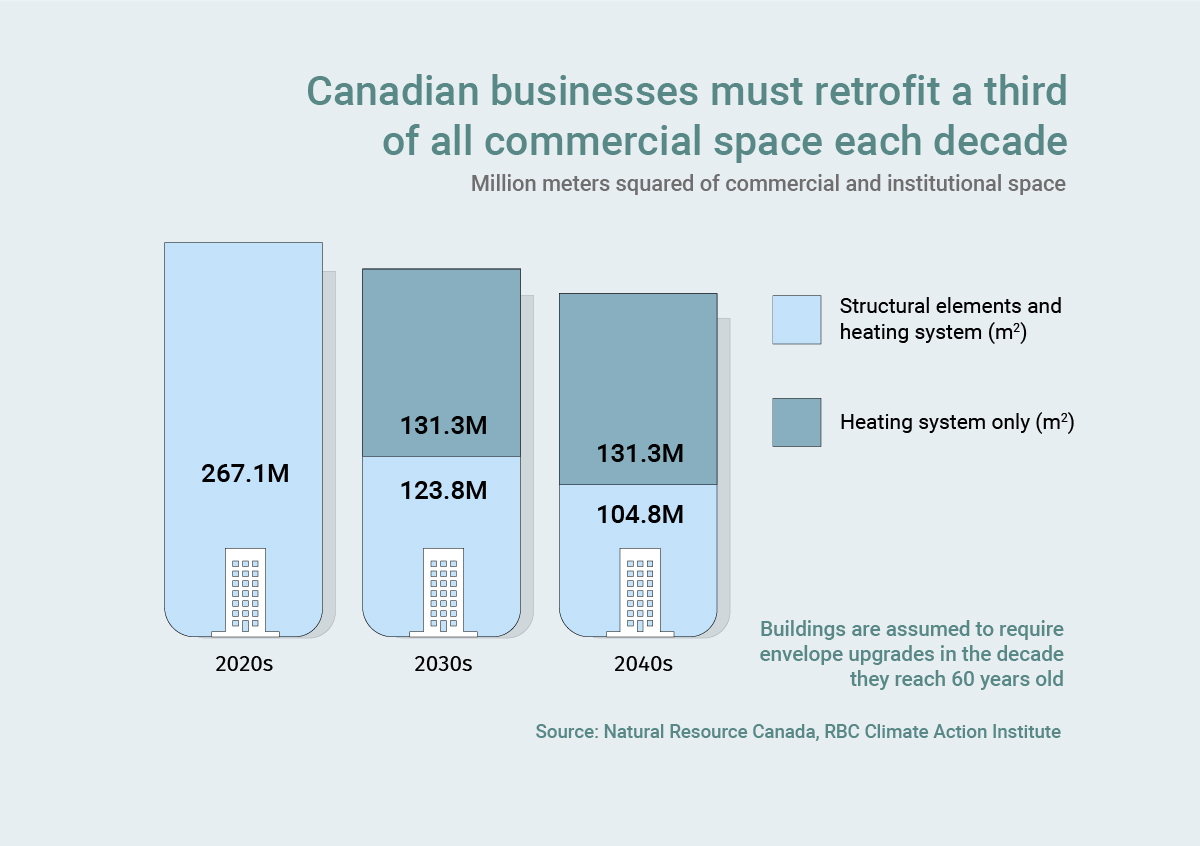

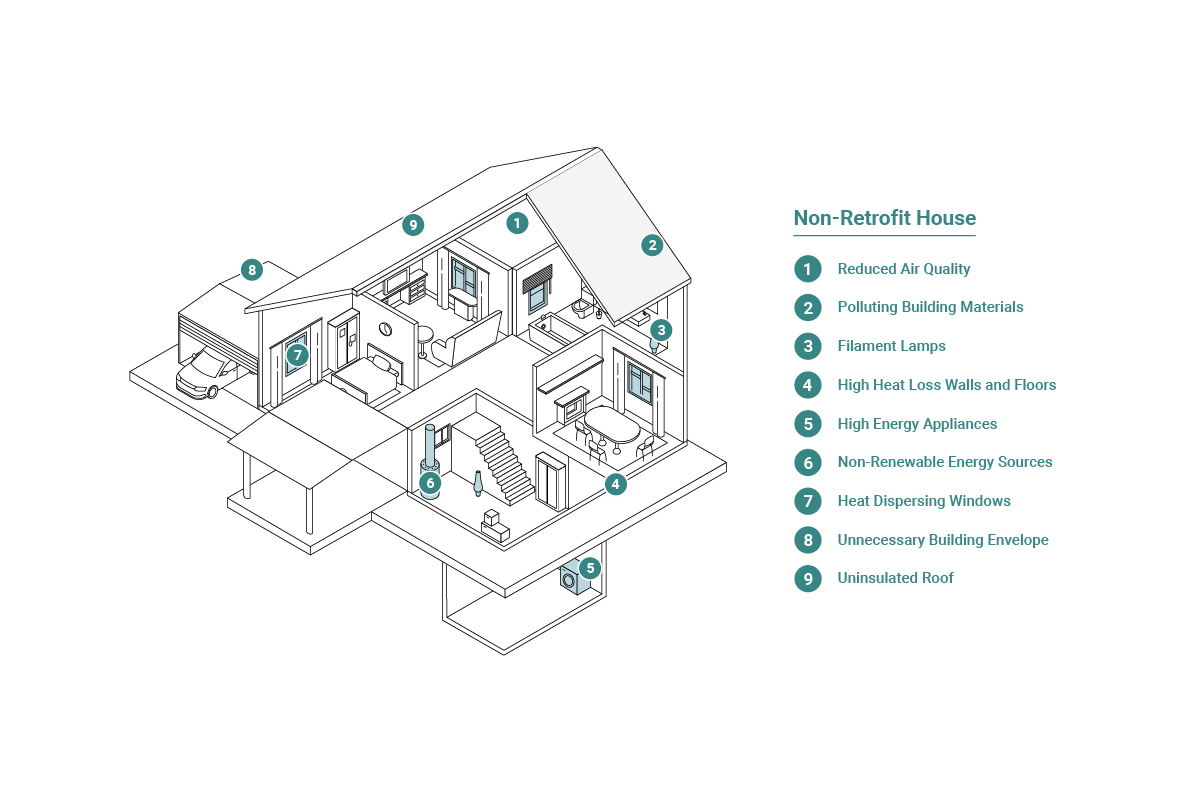

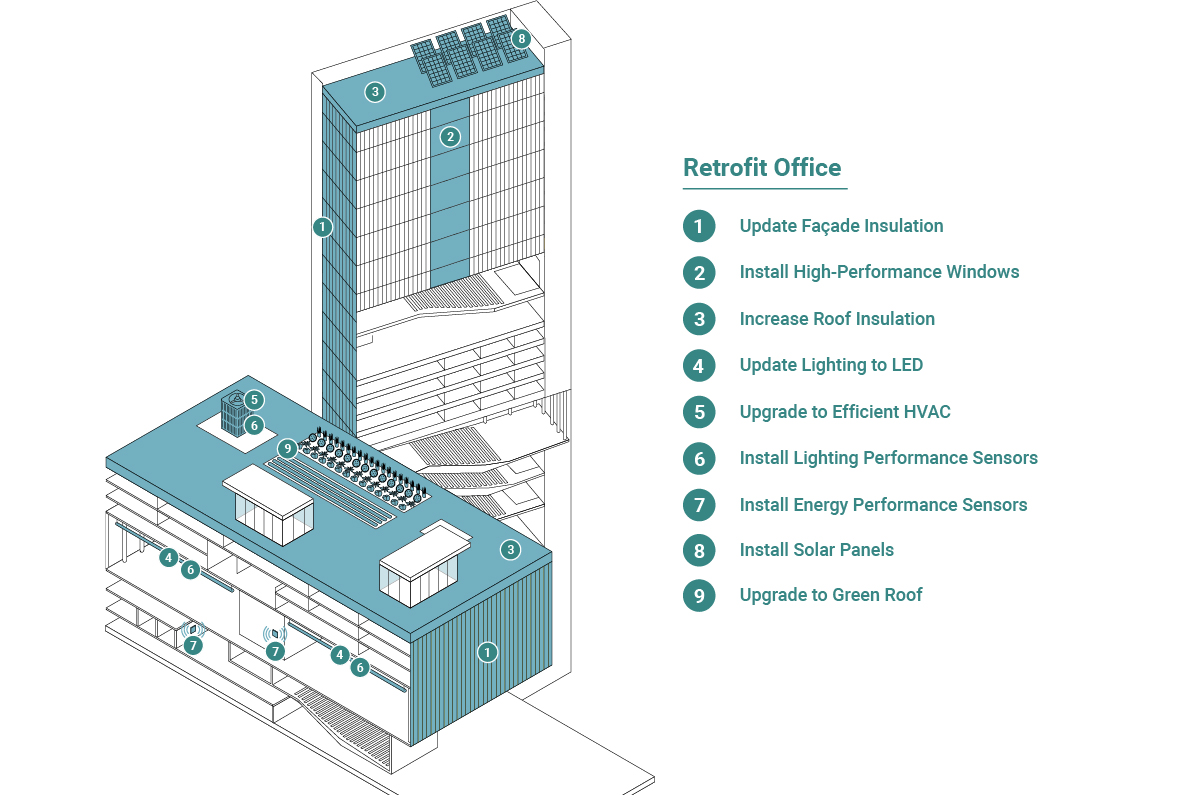

Building from the ground up is one thing. Refurbishing spaces we already have—many of which were built decades ago—will be harder. To meet our 2050 targets, we’ll need to convert 57 million m2 of residential space (400,000 units) and more than 25 million m2 of commercial space to low-carbon heating each year. For housing alone that would mean nearly tripling our current pace of conversion.

But simply replacing aging buildings is costly and could create further upfront emissions. And there are ways to work with the structures we’ve got. Retrofits that improve air tightness and insulation can make heat pumps more cost efficient, though landlords may need to vacate tenants, losing rent, and homeowners may have to sacrifice space to add insulation. For owners, the savings from retrofits may not make up for the cost, except when replacements were due anyway. And embodied carbon means early retrofits can even be bad for emissions in some cases.

Still, every time our aging buildings need an upgrade, we must seize the opportunity. And there are enough commercial buildings nearing the end of life to keep us busy until the 2030s. We need to scale up a retrofit economy quickly, lest we miss the chance to ease the stress on our already overburdened electricity system.

Enablers

Finance

Finance Electricity Infastructure

Electricity Infastructure  Labour force

Labour force Supply Chains

Supply Chains

Cleantech may be the best available solution for cutting emissions. But for homeowners and commercial landlords, the numbers make it a hard sell. Modern buildings are as much complex mechanical systems as they are spaces in which we live and work. Large commercial buildings have complicated capital budget plans. And homeowners’ budgets have many competing priorities. Some retrofits can make good financial sense, with reasonable returns (though they’re still less exciting than a shiny new kitchen renovation). But in many cases, and especially for important changes like replacing a gas furnace with a heat pump, the numbers don’t add up. Indeed, though heat pumps do slash utility bills over time, the cost of warming a home with one remains higher than with a gas furnace.

Homeowners in Toronto will pay roughly $2700 per year to heat their homes with a new, high-efficiency gas furnace and to cool it with air conditioning.3 To do the same with a cold climate heat pump,4 accounting for its higher sticker price, would cost $3,300 to $3,800. A carbon tax over $200 would be needed to make heat pumps the clear financial winner.

The highest costs are attached to the most desirable heat pumps which, like existing furnaces, are largely invisible, and push air through ducts. By comparison, the most affordable versions heat homes less evenly. As global adoption accelerates, the cost of making heat pumps (and the consumer price) should fall. But how much, and how quickly, are critical uncertainties.

Another problem: heat pumps use less energy, but they rely on electricity, which costs four times more than natural gas.5 Retrofits that tighten a building’s envelope can allow for smaller, cheaper pumps. But the cost of those retrofits may exceed the lower pump price. If smaller heat pumps gain traction, we could avoid the cost of building a much larger electricity system—but this may not be enough to convince consumers.

To overcome this, governments have turned to household subsidies like the Canada Greener Homes program, which includes grants and interest free loans that can close cost gaps. But households have been reticent to join. In almost 18 months, just 19,000 homes (of a total 16 million) have taken advantage of the Greener Homes program of 196,000 applications (less than half as many retrofits than we need to do annually). Just $69 million has been distributed of a potential $2.6 billion.6 City-level programs like Toronto’s Home Energy Loan Program are even less successful (245 homes since 2014).7

Atlantic Canada offers some hope. Between a fifth and a third of households in the three maritime provinces use heat pumps as their primary source of heat (though often with wood or electric backup). That’s risen from less than 10% in the last decade, a strong growth rate compared to the rest of Canada. The driving force is provincial funding for energy-efficient homes, especially via grants and rebates for heat pumps.8 A well-developed provincial system for delivering retrofits and educating homeowners has also helped.

Haíłzaqv First Nation

The Haíłzaqv First Nation in Bella Bella, B.C. has undertaken major retrofits, with an eye to reducing its reliance on diesel, cutting emissions, and creating equitable access to clean energy.

The program has already retrofit 154 homes with heat pumps powered by clean hydroelectricity, reducing the high cost of heating oil for residents. What sets the Haíłzaqv project apart is its approach. Community leaders have bolstered engagement, both virtually and in person, for example by helping residents fill in energy surveys. The program distributes “eco kits” so residents can install LED lightbulbs and undertake air-sealing in their homes and offers training for associated work (like energy audits). Local residents were also trained by Coastal Heat Pumps to install new heating systems, enabling them to develop skills for the long term.

This bottom-up approach, with assistance from B.C. Hydro energy efficiency subsidies, has drawn nearly $20 million in investment from the community.

Programs that offer a path to commercial building retrofits are even more scarce. These tend to lean on low-cost finance from government entities like the Canada Infrastructure Bank. And even then, the lack of commercialized large-scale heat pumps makes the economics unattractive. To make the numbers more appealing, landlords will often reduce the scale of their decarbonization strategy. Simplified, standardized retrofit services that guide owners through an efficient process will be critical.

In their absence, we’ll either need larger subsidies or more stringent regulations. This is already happening. New York will ban fossil fuels in new buildings by 2029. In the UK, existing buildings with poor emissions performance can’t be rented with standards tightening over time.

Even after we retrofit buildings, electrifying them could quadruple peak demand in the system—meaning higher electricity rates for everyone.

To decarbonize the economy by 2050, we’ll need to invest $350 billion in electricity distribution networks (the wires that bring power directly to buildings), according to BNEF. About 40% of this spending will be on upgrades to existing infrastructure.9 Some of that is needed to ensure our grids can withstand the physical effects of climate change (heat waves can damage electrical transformers and lines), but most will be needed for electrifying buildings and EV charging.

Drawing the power stored in EV batteries (and compensating the vehicle’s owner) could meet at least 8% of expected new peak demand.10 Ontario’s new ultra-low overnight rate design—which encourages EV drivers to plug in when demand is lower overnight—can create savings for EV owners and relieve burdens on the grid. But to make a bigger dent, we need to do this across many other electricity-dependent devices. Supporting building owners who conserve power is critical too.

We can electrify many more buildings before we run into these problems. But without change, we run the risk of electrifying them in the wrong ways. If forced to decarbonize, big buildings may opt to avoid expensive heat pumps in favour of cheaper electric boilers. Those systems will add stress to grids.

In the interim, there’s a good case for using hybrid gas and electric systems to stem costs. Gas is already available and heating systems replaced today will need to be replaced again by 2050—giving us another chance to fully decarbonize. A heat pump with renewable natural gas backup, a route being explored by Hydro Quebec and Energir, cuts costs by two thirds even with the added cost of renewable natural gas.

Hybrid systems also address another issue. Buildings often can’t get all the electricity they need to fully decarbonize. Two recently built Toronto residential towers with 700 parking spaces could only secure power to support ten EV charging stations.

By around 2030, we’ll need to determine if hybrid systems will get us to Net Zero, or if we need to push harder to electrify buildings. If it’s the latter, we’ll need to rethink electricity pricing structures—which don’t currently cover peak charges or time of use evenly or transparently across the country.

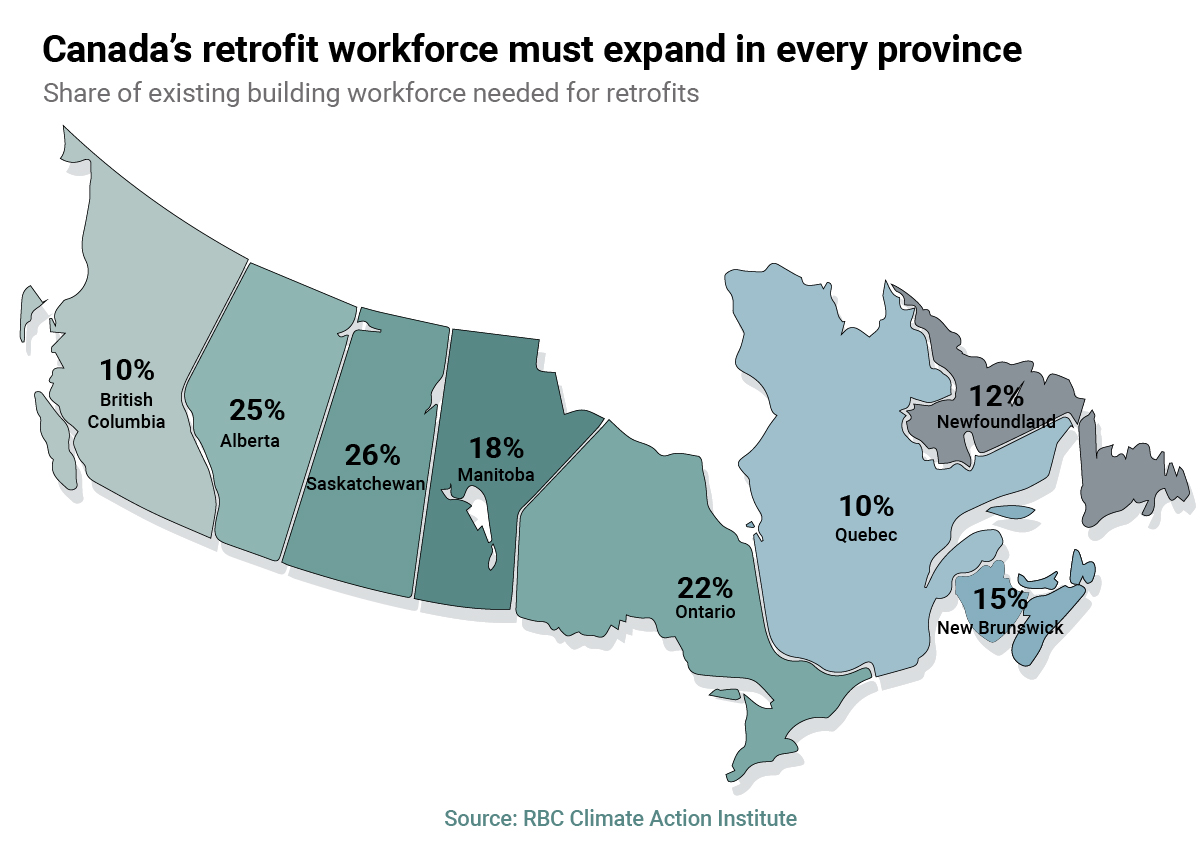

The new builds and retrofits we need could add significant demand to already tight labour markets. Our estimates indicate heating, cooling, ventilation and electrical tradespeople will be in highest demand. We’ll need 45% more HVAC tradespeople and 55% more electricians.

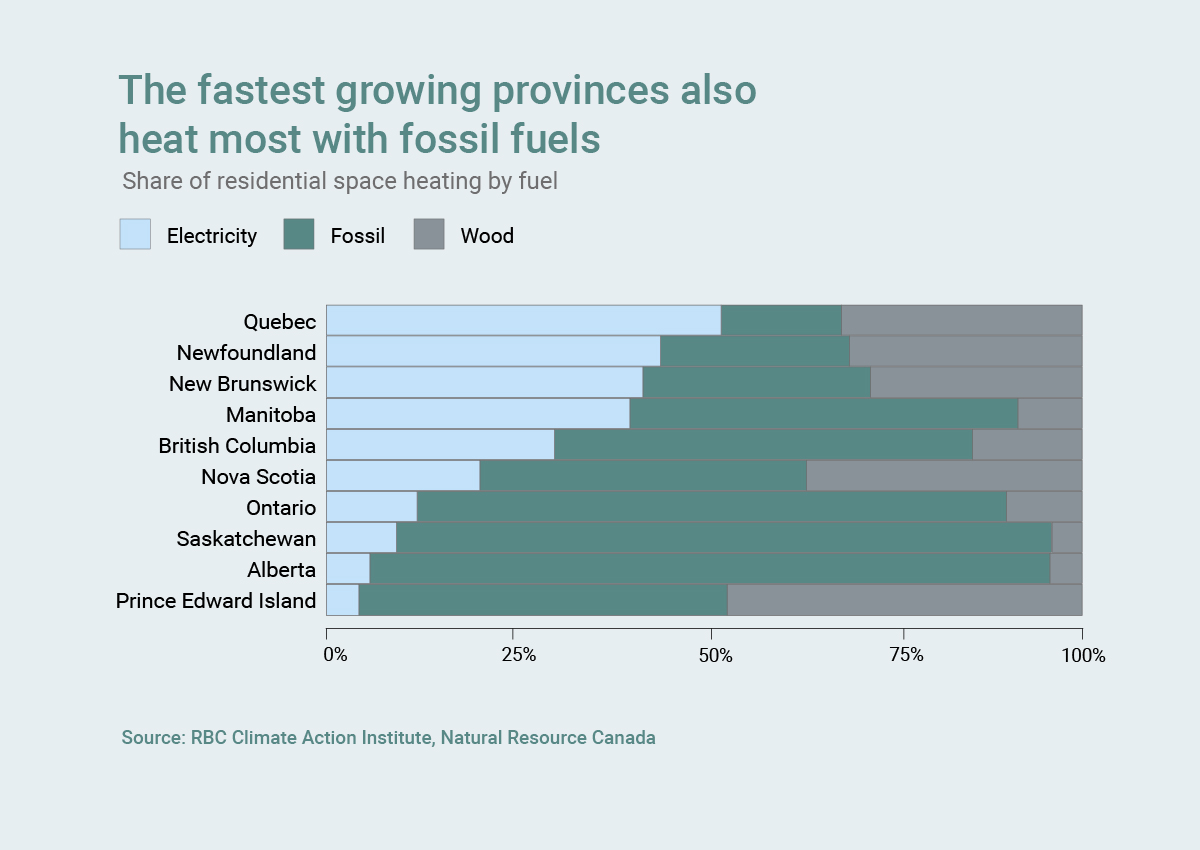

Some provinces will be more challenged than others. Inefficient electric baseboard heating can be replaced with heat pumps. But most of the emissions savings will be from replacing gas furnaces with heat pumps. Quebec and B.C., with larger existing trades workforces and less dependence on gas, will be best positioned for this transition. Ontario and Alberta, with a greater reliance on gas, the fastest growing populations, and largest skilled trades shortages, will struggle more.

As a quarter of Canada’s tradespeople approach retirement this decade, we’ll need new strategies to attract young workers. And we’ll need to upskill existing workers. Among trades, awareness about heat pumps and the retrofits needed to support them remains a barrier.

Innovation can also help. Mass timber buildings, for example, require 25% less time and use 40% less site labour than current building styles.11 But they also require workers experienced in 3D modelling and CNC machining to make wood panels. Wages for these workers are 30% higher than for construction labourers.12 Still unlocking the benefits of higher wages for workers, lower emissions, and sustainable design will depend on supporting education in the trades.

Building a retrofit workforce

Different skills are required to construct green buildings. Projects may require specialized expertise in areas such as solar panel installation, geothermal energy systems, rainwater harvesting, and green roofs. Building managers will need to collect and analyze data on energy use and greenhouse gas emissions and acquire new skills to manage retrofits. They’ll also need to operate smarter, more complex building systems. Architects will need to develop expertise in retrofits as well as sustainable design. And much greater focus must be paid to upskilling HVAC trades to deploy heat pumps and complex new systems to support them.

In Canada, Workforce 2030 is leveraging a network of community organizations, educators and industry experts to transition pandemic-impacted workers into green building work like energy retrofits and new low-carbon construction. More practical training will also be needed. Singapore’s “Green Skills at Work” program provides classroom-based and hands-on practical training for workers to gain skills and knowledge in low-carbon construction practices.

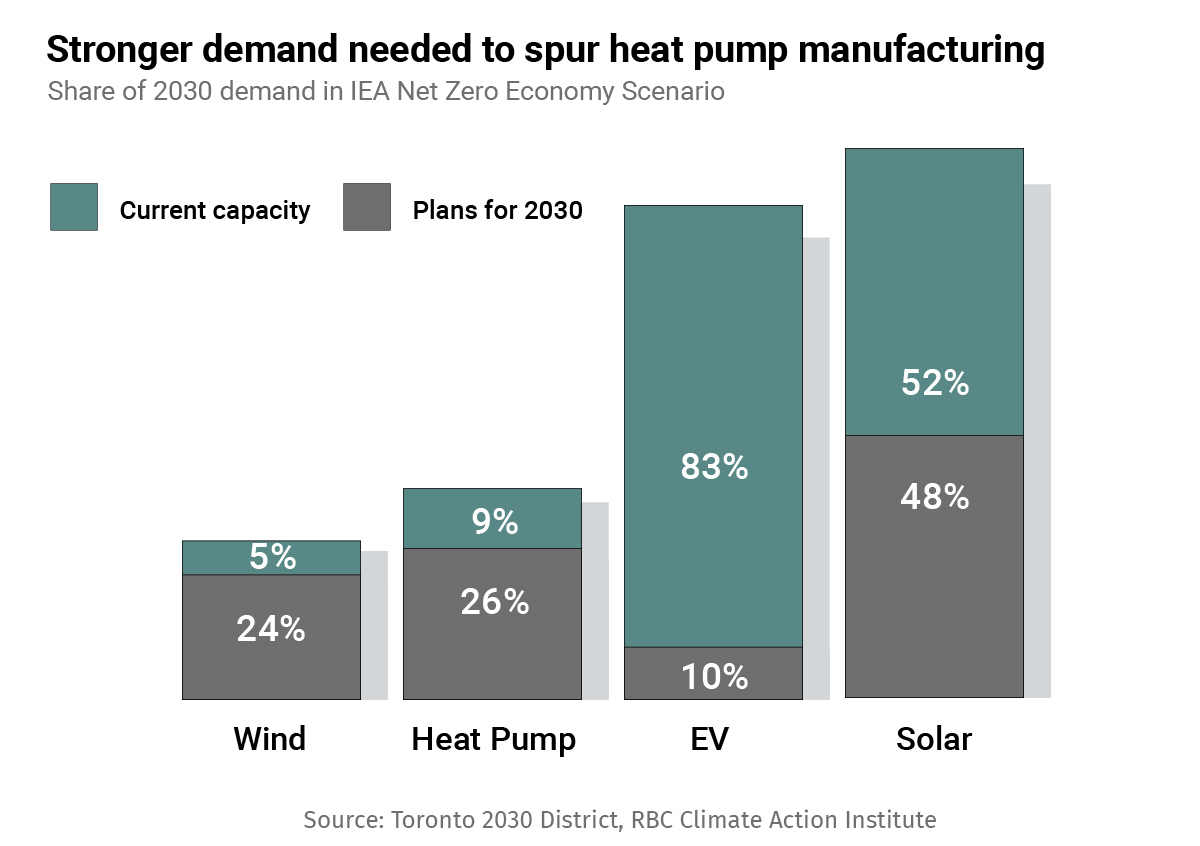

Canada isn’t the only country trying to decarbonize buildings. European heat pump sales have increased rapidly, with some 16% of buildings heated by this technology.13 Sky-high gas prices due to Russia’s invasion of Ukraine and major efforts by EU governments to drive gas conservation have helped this along.

The International Energy Agency warns sales might outpace supply.14 Companies in Asia and Europe have announced plans for new manufacturing plants, but these fall short of what’s needed. With just two years required to build these facilities, that could be quickly resolved. But robust demand will be important to spur investment.

Our cold climate and large living spaces make Canada’s needs unique—but also give us the incentive to innovate. Natural Resources Canada’s joint program with the U.S. Environmental Protection Agency and Department of Energy to develop cold climate heat pumps, is a good first step.

But with limited Canadian manufacturing, we’ll still need to compete for these critical goods. The Biden administration, for example, recently added heat pumps to the list of goods identified in the Defense Production Act identified as critical U.S. climate goals. Though Canada may benefit from more a robust U.S. supply, relying on foreign suppliers adds unnecessary risk to our transition. Canada’s collaboration with the U.S. should be paired with efforts to diversify our supply chains for this critical technology—and establish production at home.

For more, go to rbc.com/the-next-green-revolution-project.

Download the Report

Contributors:

Principal author: Colin Guldimann, Senior Economist, RBC Climate Action Institute

RBC

Naomi Powell, Managing Editor, Economics and Thought Leadership

Farhad Panahov, Economist, RBC Climate Action Institute

Ben Richardson, Research Associate

Trinh Theresa Do, Senior Manager, Thought Leadership Strategy

Darren Chow, Senior Manager, Digital Media

Shiplu Talukder, Digital Publishing Specialist

Brookfield Sustainability Institute

Luigi Ferrara, Dean, Centre for Arts, Design & Information Technology

Jacob Kessler, Director Account Management & Business Development

Matt Hexemer, Director, Global Design Studio

Joseph Enaje, Lead Designer

Chiara Alberti, Writer/Designer

Lucrezia Marsili, Writer/Designer

Finn Crockatt, Writer/Designer

Acknowledgements

We thank the following people for insightful conversations and support with technical analysis:

Julia McNally, Sheena Sharpe, & Cara Sloat, Toronto 2030 District

Jon Douglas, Director, Global Sustainability, Corporate Real Estate, RBC

Denise Gray, Director, Enterprise ESG Strategy, RBC

Brendan Haley, Executive Director, Efficiency Canada

Isabelle Smith, Director, Engineering Net Zero, SNC Lavalin

Stuart Galloway, EVP, SOFIAC

Aaron Berg, Director, Energy Efficiency Investments. Canada Infrastructure Bank

Julia Langer, CEO, TAF

Carl Pawlowski, Senior Manager, Sustainability, Minto Group

Joanna Jackson, Director, Sustainability & Innovation, Minto Group

Jeff Ranson, VP Sustainability & Stakeholder Relations, BOMA

Mark Hutchinson, VP, Green Building Programs and Innovation, Canada Green Building Council

Andrew Guido, VP, Sustainability and Innovation, Empire Communities

Luke Gilgan, Board Member, Mattamy Asset Management

Roya Khaleeli, Director, ESG, Mattamy Asset Management

Kevin Kruk, VP, Project Finance, Tridel

Graeme Armster, Director, Innovation & Sustainability, Tridel

Malini Giridhar, VP, Business Development & Regulatory, Enbridge

Participants at the RBC x BSI Net Zero Buildings research forum on March 15, 2023

Net Zero Buildings Forum:

Sandhya Casson

Kevin Santus

Graeme Kondruss

Jasraj Singh Narula

Wing Yan Chan

Tyana Van-Tang

Thanusha Kanagendran

Isabel Mactal

Carmen Skoretz

Wing Yan Chan

Monika Patel

Lakshya Verma

Yasaman Musician

Haylie Wong

Dhruv Sheliya

Samyuktha Vasudevan

Livy Morden

Ka Man Carmen Lau

Berk Ercan

Angelo Barletta

Mansi Bhojani

Shree Shivrajnagesh

- These estimates incorporate the incremental capital cost of new net zero buildings vs. current codes as well as the upfront capital costs of retrofits (insulation, heat pumps, etc). They do not present the overall cost increases or added annual spending on buildings over the life of these assets, which would be offset by savings from lower energy bills.

- https://www.rbc.com/en/wp-content/uploads/sites/4/2025/03/WorldGBC_Bringing_Embodied_Carbon_Upfront.pdf

- Based on natural gas at $10/GJ. In parts of the country where gas costs more, heat pumps can make more financial sense, but break-evens still require significantly higher gas prices.

- Cold climate heat pumps are much more efficient at cold temperatures, and unlike lower-cost heat pumps, convert to electric resistance heat only on the very coldest days, meaning they cost less to run and are friendlier to the grid than traditional heat pumps.

- Assuming gas costs of approximately 30 cents per m3 and electricity costs at about 14 cents per kWh

- https://natural-resources.canada.ca/energy-efficiency/homes/canada-greener-homes-initiative/canada-greener-homes-grant/canada-greener-homes-grant/canada-greener-homes-initiative-2022-quarterly-update/24712

- https://www.toronto.ca/news/city-of-toronto-offers-zero-interest-loans-incentives-to-accelerate-home-retrofits-and-emissions-reductions/

- https://climateinstitute.ca/publications/heat-pumps-are-hot-in-the-maritimes/#:~:text=As%20the%20Canadian%20Climate%20Institute,big%20switch%20to%20clean%20electricity.

- The balance is split evenly between replacement of end-of-life infrastructure and investment to facilitate new generation assets

- https://www.google.com/url?client=internal-element-cse&cx=002629981176120676867:kta9nqaj3vo&q=https://www.ieso.ca/-/media/Files/IESO/Document-Library/engage/derps/derps-20220930-final-report-volume-1.ashx&sa=U&ved=2ahUKEwikidLY3pL-AhUEk4kEHcHIAPUQFnoECAUQAg&usg=AOvVaw1rkiAVix-4islQ2Ehk9cs7

- Wood Products Council, “Mass Timber: Shifting Labor from Jobsite to Shop”

- Median wage for CNC machinists in Canada is $27.35/hr, versus $21/hr for construction labourers.

- https://www.ehpa.org/press_releases/heat-pump-record-3-million-units-sold-in-2022-contributing-to-repowereu-targets/

- https://www.iea.org/reports/heat-pumps