All eyes were on the election this week—but something else remarkable was taking place, too. Many of the country’s top Indigenous leaders came to Toronto, and Bay Street, to see how we can better mobilize capital for Indigenous-partnered projects. These conversations are central to the questions we’re grappling with as a country–including reimagining our relationship with our closest ally and building up our economic strength.

The two outcomes—of the election and economic reconciliation—are closely related. Indeed, our economy and trade won’t grow and diversify if we don’t ensure a lot more Indigenous ownership. That was the focus of the annual First Nations Major Projects Coalition Conference, in Toronto, which drew nearly 2,000 people to explore the future of Indigenous capital—and how it is a source of strength for Canada in an increasingly competitive world.

Here’s some of what we took away, and questions we need to keep asking:

From critical minerals to hydro and natural gas, Canada’s ability to build resource projects at speed and scale will come down to 3Cs: capital, capacity and consent. Can we develop those together?

Our research shows that there is an Indigenous equity opportunity of close to $100 billion over the next decade. How can governments mobilize concessional tools to attract more private capital?

Government loan guarantees are in fashion, with the Carney government committing to double its program to $10 billion and Ontario using the conference to announce a tripling of its program to $3 billion. How can those programs be better coordinated and implemented at a faster click?

Equity may not be the most appropriate tool for some communities. Can we also promote new debt instruments, royalty models and procurement agreements for communities to invest in?

Indigenous capital is being built up quickly–from project participation to trust settlements. What structures can help us pool this capital–and reinvest returns back into Indigenous Nations?

Most communities need a lot more capacity—from finance to engineering and legal—to make these deals and projects work. In fact, our research suggests close to 85% of these projects may be unrealized without plugging the capacity gap. How can we invest more in scholarships, training, work placements and exchanges—for companies as well as communities?

Capital and capacity are useless without consent, which is more than a one-off vote, or signature. Can we develop accepted, non-binding approaches to consent that allow both parties to develop and deepen their trust and confidence?

Voice is a critical part of consent. How do we know if each partner feels they have a respected voice?

Time is of the essence. Can companies and communities create clearer approaches to timelines, and time expectations, for projects?

Uncertainty is the enemy of investment. Can co-developed models for Indigenous consent become one of Canada’s advantages with global investors?

Indigenous priorities are not diversity issues—they undergird the Constitution of our country and how our country is constituted. How can we more boldly state that Indigenous partnerships are a foundational part of operating in Canada?

Small businesses and projects tend to be excluded from these major project conversations, and yet are crucial for the success of our economy. How should we better raise capital for small business collectives and projects?

John Stackhouse, Senior Vice-President, Office of the CEO, RBC

Varun Srivatsan, Director, Policy and Strategic Engagement

The first 100 days for any new government are filled with a flurry of activity. For Mark Carney’s Liberal minority government that will include tabling a budget, trade talks with the Trump administration and hosting the G7 in June. Zoom out, and the key priorities come into focus. Here are five that RBC Thought Leadership has been keeping a close eye on and ones we believe will have Parliament’s full attention in the coming months—and beyond.

Securing an economic and security pact with the U.S.

During upcoming negotiations with the U.S., expect Canada to minimize concessions until duty-free trade is secured and the current trade agreement is honoured. The U.S., meanwhile, will seek to have a wide-ranging discussion that includes border and security concerns.

At a minimum, the agreement could include:

Energy and economic security: Negotiators will want to address longstanding irritants, including the digital services tax, attempting a resolution to the softwood-lumber dispute, and strengthening rules of origin. Expect movement and strategies on gas, nuclear and critical minerals, which dovetails nicely with the upcoming G7 meeting.

Defense and Arctic security: This includes everything from the plan to meet 2% defence spending targets, to NORAD modernization, dual-use accounting, social and economic infrastructure investments in the North, including an Arctic port, and expanding shipbuilding/icebreaker commitments.

Border security: Although Canada has made investments in border security, further collaboration, especially on money laundering, immigration and drug/arms trafficking, will likely come up during negotiations.

This won’t be the first attempt at a comprehensive continental economic and security agreement. In the mid-2000s, the Security and Prosperity Partnership of North America included the private sector in an effort to enhance continental competitiveness. While it didn’t come to fruition, many ideas—cooperation on infectious diseases, emergency management, and border security—have persisted. This attempt has a better chance of succeeding if it is targeted and time bound.

Address the housing affordability crisis

In The Great Rebuild, we outlined seven ways to address Canada’s housing shortage and affordability. When comparing the recommendations in our April 2024 report to the Liberal election platform, a number of key items line up:

Focus on prefab: Factory-built dwellings can be more time and cost-efficient. And the government has promised $25 billion in financing to prefab home builders—as well as a focus on sustainable building materials.

Cut red tape: Project approval timelines in Canada, as we noted, “can be among the lengthiest in the world.” Simplifying national building codes, streamlining regulations and leveraging standardized designs are all part of the Liberal platform.

Build affordable options: Government has pledged $10 billion worth of low-cost financing for lower- to middle-income Canadians.

None of this gets done, however, without shovels in the ground. We estimate that more than 500,000 additional construction workers are needed to build the homes required between now and 2030. The Liberal’s plan to incentivize companies to hire recent grads and offer apprentice programs is a start. But finding half-a-million construction workers requires more. Options include prioritizing construction skills of new immigrants, growing the enrollment of trade schools, and enticing older construction workers from retiring.

The affordability crisis has made it an imperative that Canada acts promptly and with more streamlined coordination across all levels of government.

Build Energy Corridors

Building out major energy infrastructure enhances economic resilience through the diversification of key commodity exports. In 2024, Canada’s major resource exports (minerals, metals and fuel) were among Canada’s largest, generating $175 billion in aggregate net exports–almost offsetting Canada’s global trade deficits across all other goods categories.

Success in taking projects from blueprint to buildout depends on policies directed at mobilizing private capital and reducing red tape. To date, existing key Liberal policies around Bill C-69, Bill C-48, the Oil and Gas Emissions Cap have not been conducive to large-scale investment. An ‘amended’ approach with a greater focus on pragmatism could establish a climate more conducive to attracting capital. Key focal points for Ottawa include:

Industrial carbon pricing: ‘Axe the tax’ likely shifts the burden of carbon pricing onto large industrial producers. A rising industrial carbon price likely remains, presenting competitiveness challenges relative to U.S. leadership focused on deregulation. A 50% carbon capture investment tax credit derisks capital costs, but projects need revenue certainty. To date, The Pathways Alliance, a consortium of Canada’s largest oil sands producers, has been unsuccessful in negotiating carbon credit guarantees from Ottawa. Of course, this comes at a time of competing fiscal priorities. Ottawa is already on the hook for 50% of CCUS capital costs (conservatively estimated between $60-75 billion). Contract for differences for Pathways would likely require tens of billions in additional funding (10-12 million tonnes at $125-150/t for 10 years).

Regulation/Permitting: Regulatory delays has led to drawn out timelines, leading to cost overruns and/or cancellation of key projects, as capital is ultimately redistributed to shareholders rather than towards growth-enabling infrastructure. Policies such as ‘One Project, One Review’ and declaring more energy projects as in the ‘National Interest’ are helpful. This is likely most beneficial to natural gas pipelines and LNG infrastructure, given the greater political alignment on the LNG file (B.C. and Ottawa).

Provincial trade barriers: East-west trade through greater use of interties yield a more resilient, flexible and efficient grid system—increasingly important given rising load growth over the next 25 years (up to 3x) and the need for cheap power for industry/manufacturing.

Safeguard federal finances

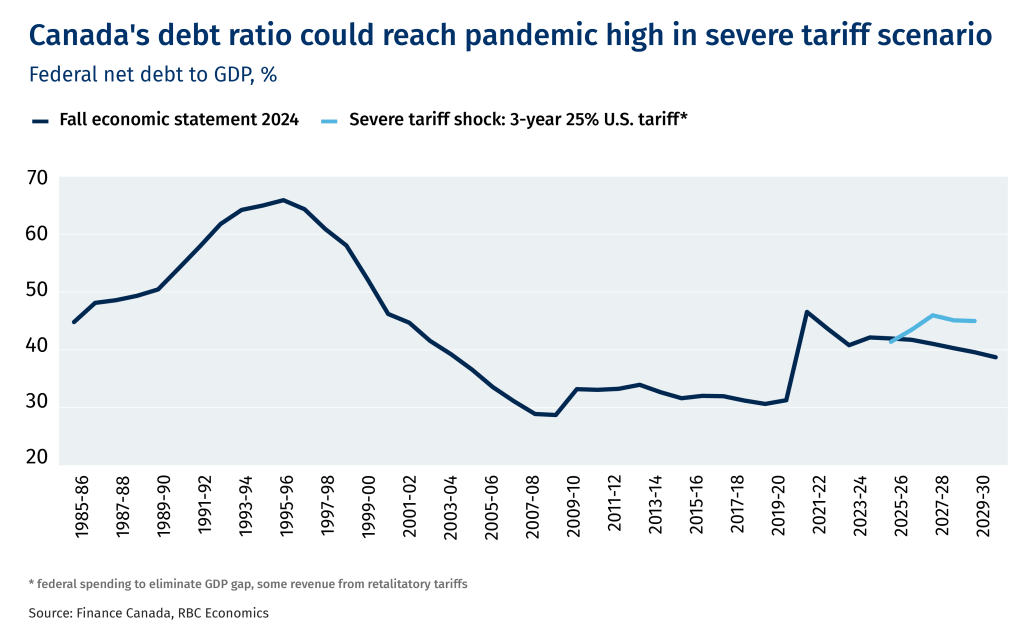

As RBC Economics wrote recently, a lot will be demanded of fiscal policy. A slowing economy and the risk of a greater trade-linked recession imply fiscal supports of varying degrees. And structural challenges loom–weak productivity, strained affordability, an aging population, export concentration, and shifting geopolitics could trigger more federal spending. Monetary policy has its limits—and won’t be able to address the areas of greatest need. As a result, Ottawa will need to keep the following in mind to keep the federal debt burden sustainable:

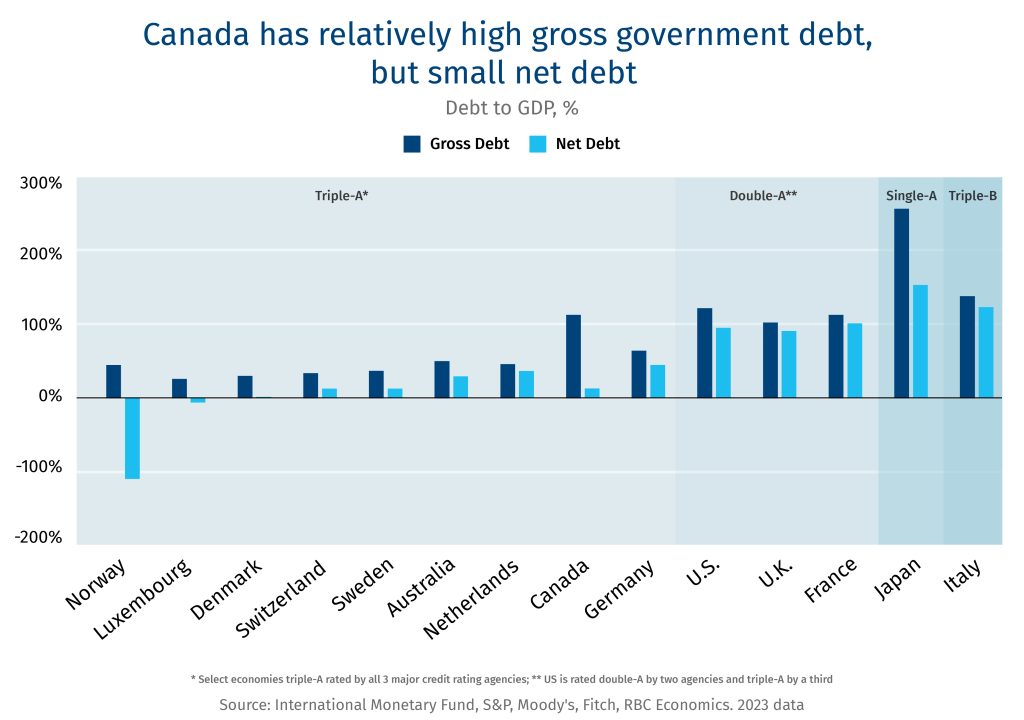

It’s not unlimited, but Canada has some fiscal space. Canada’s gross debt burden (debt-to-GDP-ratio) is high, but its net debt burden is the lowest in the G7.

Supporting the economy through a potential recession is expected by markets, and unlikely to raise red flags if sized and targeted appropriately. COVID-style supports that ‘bridge’ the economy is not the correct playbook in a trade shock where the economy, structurally, could look quite different in the aftermath.

Growth-positive investment is key to keeping federal debt levels sustainable. The more that each dollar of public spending delivers greater growth dividends, the more the federal debt burden will remain in check, even with higher spending.

Rebalance social and business investment measures. Canadians have benefited in recent years from an expansion in federal government spending on often broad-based social programs without absorbing the costs. Now, the feds have a new laundry list of to-dos, including kick-starting business investment. Non-spending measures like removing red tape help, but fiscal space will be needed for spending, as well.

Make social and other ‘must-do’ spending more growth positive. Major investment needs across the economy beg the question of sufficient capital and labour resources to achieve timely results without crowding out. Public spending in essential areas like housing, defence, and healthcare can promote efficiencies, innovation, and other growth drivers to ensure the economy can grow in multiple areas.

Transform AI into a productivity engine

Canada is rich in AI talent but short on the three things that can translate that talent into prosperity: modern computing infrastructure, large-scale deployment, and robust domestic demand. Only 26% of Canadian firms report having implemented AI—eight points below the global average—and the country continues to slip in AI-readiness indexes. With labour-force growth flattening and labour costs rising, closing the AI adoption gap is Canada’s most direct route to higher productivity, greater economic efficiency, and continued competitiveness.

Ottawa could pursue a three-pronged approach—acting simultaneously as facilitator, champion, and early adopter—to transform AI from a fragmented set of R&D bets into a nationwide productivity engine.

Facilitator: Treat compute capacity as critical infrastructure, marshalling patient capital, procurement guarantees, and partnerships with global players to facilitate access to GPU clusters. Further, government might consider targeted tax credits and grants favouring projects that embed Canadian IP and high-value jobs at home.

Champion: Ministers could become visible ambassadors for domestic AI successes, weaving them into every productivity, healthcare and defence announcement. Demand-side tools—procurement quotas that reserve, say, 25–30% of relevant contracts for qualified AI firms, first-reference-customer letters, accelerated tax refunds for AI pilots—have the potential to generate the domestic demand needed to keep promising startups from fleeing south.

Early Adopter: In the immediate term, the government could equip frontline analysts, auditors and service agents with secure co-pilots to yield productivity gains and build AI fluency. Longer term, the government could work to re-engineer programs around models that learn across departmental silos, enabled by a U.S. Department of Defense-style fast-lane tech funding agreement, a shared sovereign large language model stack, and performance incentives for senior bureaucrats who are able to effectuate AI solutions.

Contributors:

Cynthia Leach, Assistant Chief Economist, RBC

Varun Srivatsan, Director, Policy and Strategic Engagement

Shaz Merwat, Energy Policy Lead, RBC Climate Action Institute

Welcome to the first edition of Trade Zone. It’s in beta testing, so please let us know what you think. Every week, our team at RBC Thought Leadership will share what we’re hearing from governments, learning from clients and seeing in our research. We’ll also give you a cheat sheet on the week, to help you keep pace.

Notebook

By John Stackhouse

If Mark Carney’s Liberals are re-elected on Monday, as polls are suggesting, expect them to shift their focus South and West by the end of the week.

To the South, expect a crew of newbies across the bureaucracy, as well as PMO, with experience in the U.S. A call with Donald Trump will top the To-Do list, with more than trade on their minds. “Comprehensive partnership” is one term floating about—to cover border security, immigration, Arctic and defence issues. And yes, trade, even if USMCA may not be long for this world in its current form.

Expect to see a highly structured and strategic Canadian approach, colliding with a highly unstructured American approach. The Trump team had been telling Canadians to avoid working groups or outside “experts.” Side note: American negotiators are driving the Mexicans batty with demands for them to control tomato shipments before any deal is reached.

The Trump team has been losing in the courts and in the markets. If that continues, Canada may opt for the long game, following Napoleon’s advice: “Never interrupt your enemy when he is making a mistake.”

To the West, watch for outreach from Ottawa to Alberta and Saskatchewan, with a focus on diversification of exports. That will take a lot more than a new pipeline (which may be on the table), as our resource-driven provinces think about new markets. Dow Chemical’s bombshell decision this week to delay its Alberta plant is just the latest trade warning. (I wrote about the Big Pivot on our Trade Hub, drawing on conversations this week at Public Policy Forum’s annual Growth Summit, which is a bit of an Olympics for policy wonks.)

Caught between the Potomac and the Prairies is Ontario, but not for long. Doug Ford stole the show at the PPF Summit with a feisty attack on Trump (“Sometimes the cheese seems to fall off the cracker with that guy”) and a passionate shout-out for Progressive Conservatives. Ford seems ready to play bad cop to the next PM’s good cop. He may be warming up for another role, too.

Get ready to hear more about Europe as a new (old) partner, for military procurement, AI standards and, yes, trade. Those conversations will grow ahead of the G7 summit in Alberta in June, when we’re expecting LNG and data centres to be front and centre. If the Trump team shows up—no bets there—they’ll want to ensure some alignment on LNG finance, especially for emerging markets, and access to gas-powered electricity for their hyperscalers (the latest euphemism for Big Tech).

Climate is creeping back into the trade conversation, although not in North America. Europe is marching ahead with border carbon adjustments (just don’t call them carbon tariffs). Japan is also advancing an emissions trading system, including cross-border carbon credits and a surcharge on fossil fuels (just don’t call it a carbon tax). Expect Canada’s Balkanized industrial carbon pricing system to be part of a likely discussion on the G7 sidelines. (Did we tell you that will be in Alberta?)

Indigenous equity will be an important aspect of any new trade relations, much more so than even five years ago. We’re part of the big First Nations Major Projects Coalition conference in Toronto next week and expecting both Ford and possibly a new PM to use the platform to advance their investment strategies. (No investment, no trade.) Other key guests will include Indigenous leaders from Alaska and Utah— hello, Republicans—who may offer a different kind of cross-border relationship.

Need to know

➔ We estimate that $125 billion is at risk for Canada as U.S President Donald Trump eyes 5 strategic sectors.

➔ In a bid to escape tariffs and wait out the trade war, third-party sellers on Amazon and Walmart are shifting stock from China to tariff-free warehouses in Canada.

➔ Coke vs. Pepsi: Who’s the winner of the ultimate taste, er, tariff test?

➔ Where we see Canada’s debt ratio headed over the next three years in a worst-case tariff

Final Word(s)

“All eyes right now are on the Arctic. We are the gateway to the Northwest passage and at the forefront of the conversation when we’re talking about security and sovereignty.” —P.J. Akeeagok, Premier of Nunavut

“People are not going to race to build manufacturing in America. With the policy volatility, you actually undermine the very goal you’re trying to achieve.” —Ken Griffin, Citadel CEO

“The renegotiation of the USMCA included a very forward-looking digital-trade agreement. I think there is meaningful opportunity there, and that’s in contrast with what you have seen in some other countries, where data sovereignty has been more restrictive.” —David Schwimmer, CEO of the London Stock Exchange

“The EU is working on a targeted and measured response in case we cannot reach a deal [with the U.S.] rapidly.” —Eric Lombard, France’s Minister of Economy, Finance and Industry

The Public Policy Forum is one of Canada’s premier think tanks, and hosts an annual Growth Summit that tends to be at the pointy end of some pretty big issues.

This year’s summit, in Toronto, was all about what I’d call the Big Pivot — and how we can make our economy more independent and resilient. Great conversations about investment, Indigenous equity, AI-adoption and more.

Here’s a few of the questions I took away:

1. Do we need to win back investor confidence?

The answer seems to be yes. Too many of these conversations assume Canada is amazing in the world’s eyes. Rhetoric is cheap. Credit is costlier. Keep an eye on how money is priced for Canada in the coming months.

2. Can we increase competition while reducing reliance on America?

The U.S. tends to be the primary driver of competition, directly or indirectly. And there are not a lot of easy alternatives. European firms aren’t likely to add a lot of juice to Canadian markets, and Chinese entrants are probably a non-starter. Perhaps our new competition needs to come more from within.

3. Can governments play a more active economic role without wrecking the economy?

We have decades of mixed results but will likely give state corporations one more try, whether it’s to build houses or expand pipelines.

4. What the heck is “national interest”?

A lot of those government investments will be made in the name of an ill-defined national interest. We’re a nation of many regions, and one’s interests are often not another’s

5. Why do Canadians shy away from risk?

I was struck by the number of conversations that eschewed risk. No country clamours to “de-risk” like this one, as if the key role of government is to bear the risks of the private sector and of individuals.

6. How can we develop the Arctic without compromising it?

The summit included several key northern voices that stressed the need to not militarize the North the way we did in the 1950s and ‘60s. They’re eager to defend Canada, on the ground and in the sky, but not at all costs, especially to their culture.

7. How much do we want to exclude China?

Reducing our dependencies on the U.S. will require new markets and new sources of capital — and Europe won’t be the answer, not on its own. Yes, there are plenty of options. It’s a big world! But China is the biggest option, and one we need to develop a clearer relationship with.

8. How do we balance economic ambitions with climate commitments — and the world’s climate expectations?

We’ve become so consumed with All Things Trump that we seem to forgot how the rest of the world is not turning itself upside down. Indeed, climate remains a serious concern from Japan to Germany — the markets we now eagerly want to serve — and we will have to ensure we’re not misaligned.

9. How can we align our duty to consult Indigenous communities with our ambition to build more faster?

There may never be a formula for consultation and the resulting consent — but we may be able to establish norms that will be widely accepted. Watchwords: “speed and certainty.”

10. How can we pool institutional capital for major projects?

We can continue to let market forces determine what gets financed, with a range of government supports and incentives. I don’t think Canada will ever have a sovereign wealth fund. Or will we? Alternatively, can we move toward dedicated public-private investment vehicles that may draw inspiration from the Quebec model?

The next few years will be unlike any few years we’ve seen. So a lot of new thinking will be needed.

Canada could be on the verge of a historic investment boom. The trade war with the U.S., an increasingly divided global economy, concerns over Arctic security and an AI revolution that comes with enormous energy requirements—all point to the need for more economic and security infrastructure. But those diverse ambitions, from northern ports to West Coast LNG to critical mineral plants, have a common requirement: Indigenous partnerships.

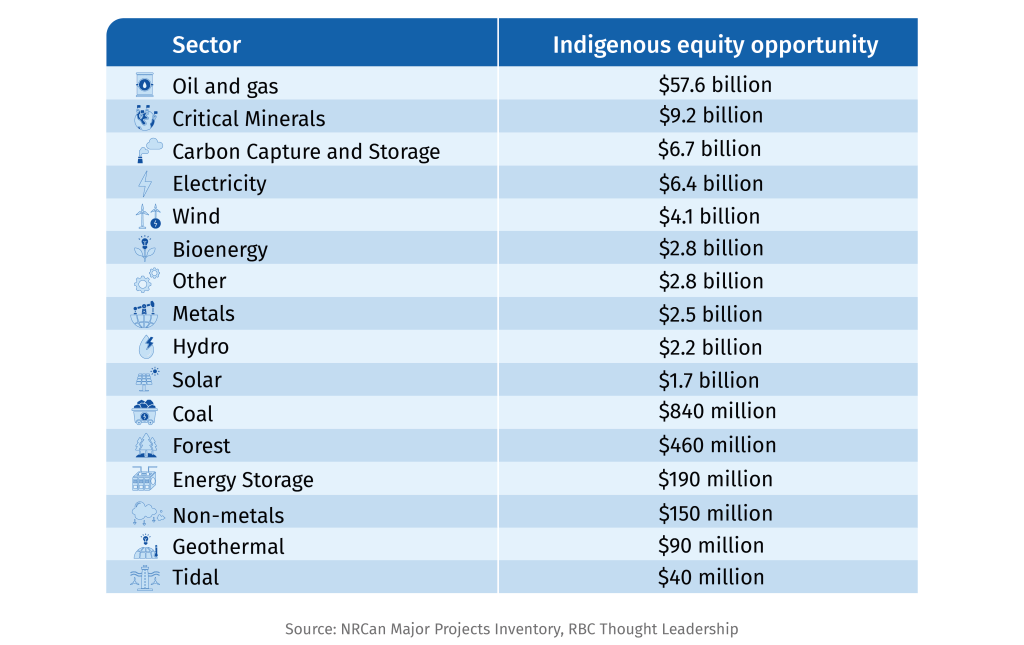

Canada’s future growth and prosperity depends heavily on getting Indigenous economic reconciliation right. If not, the country’s ability to diversify our resource exports, enjoy independence and resiliency in strategic sectors, and improve productivity, which has lagged that of other countries for years, are all at risk. And that’s not the only thing at stake. As RBC Thought Leadership’s research indicates, 73% of the 504 major resource and energy projects planned or currently underway in Canada run through, or are within a 20-kilometre radius of, Indigenous territories—namely, treaty, title unceded and consultation lands. The value of the Indigenous equity opportunity of those projects alone is $98 billion over the next 10 years.

Canada can’t afford to miss out on the opportunity. Fortunately, examples of Indigenous economic reconciliation in action span the country, including:

In Kitimat, B.C., the Haisla Nation and Pembina Pipeline are working on the Cedar LNG project, a four-year partnership that will result in a $4-billion facility. Once operational, this majority Indigenous-owned facility is expected to generate $85 million in GDP annually.

In several Manitoba and Nunavut communities, the Kivalliq Hydro-Fiber Link seeks to provide clean energy through a proposed 1,200-kilometre energy and telecommunications corridor connecting Nunavut with Manitoba’s grid.

In the small southwestern Ontario town of Jarvis, the Oneida Battery Storage Project will be one of North America’s largest battery-storage facilities when it comes online. Partly owned by Six Nations of the Grand River Development Corporation, Oneida will provide much-needed capacity to Ontario’s strained electricity grid.

While these projects illustrate progress, more can be done. Centuries of treaties, Nation-to-Nation and business agreements, and case law have underscored the centrality of Indigenous peoples in Canadian decision-making, particularly in building up infrastructure and resource projects. The Constitution Act of 1982, particularly Section 35, recognized and affirmed Aboriginal and treaty rights in the Canadian legal and political fabric. Supreme Court cases, including Calder, Delgamuukw and Tsilhqot’in, further affirmed Aboriginal rights and title—the inherent right to use and jurisdiction over an Indigenous Nation’s traditional territory.

One of the key principles enshrined through the Constitution and case law is maintaining the Honour of the Crown—a legal concept characterizing the fiduciary duty imposed on the Government of Canada toward Indigenous peoples. One of the duties that this principle imparts on the Crown is the duty to consult and accommodate. When the Crown engages in an activity that could have a negative effect on an Aboriginal right or title, it must consult with the relevant Indigenous groups and accommodate these infringements. This duty has been affirmed through case law and is characterized in the Nation-to-Nation relationship between Indigenous peoples and the Government of Canada.

The United Nations Declaration on the Rights of Indigenous Peoples (UNDRIP) advanced the concept of free, prior and informed consent (FPIC). This is a pro-active means for governments (and businesses) to seek and achieve consent on developments occurring on Indigenous territories. UNDRIP is now law federally, as well as in British Columbia and the Northwest Territories.

Together, the duty to consult and FPIC provide the framework and requirements for the way governments and businesses engage with Indigenous Nations on projects happening on their lands or implicating their interests.

What’s needed now is bold, innovative thinking. And it starts by finding ways of unlocking three critical elements:

CAPITAL: Indigenous ownership in major projects requires a mix of private and concessional financing tools, including loans, loan guarantees and grants. Without access to capital, a historic challenge for Indigenous Nations, many equity opportunities, and indeed, entire projects, may not get started.

CAPACITY: Rights-based negotiations, along with commercial and legal discussions around major project development, are complex and requires investing in capacity for everyone at the table—Indigenous Nations, governments and business—to ensure project success.

CONSENT: The constitutional duty to consult and accommodate, UNDRIP, case law, and decades of legal and political developments have cemented how important free, prior and informed consent is to project development. The downpayment needed to seek and achieve FPIC is long-term, trust-based relationships across all parties, which requires going beyond transactional project discussions.

Advancing all three elements—capital, capacity and consent—in parallel is necessary to bringing Indigenous Nations along as true partners in economic development. Through a collective call for action, led by Indigenous Nations and closely supported by businesses and governments, there is an opportunity to generate shared prosperity—and get Canada building at speed and scale.

Capital

Access to affordable capital is a persistent challenge for members of Indigenous communities, caused in part by institutional barriers set up by Canadian governments. Risk premium for Indigenous borrowers is impacted by rating agencies, and by extension, financial institutions’ risk and liability considerations. This is partly due to First Nations communities being unable to collateralize reserve land under Section 89 of the Indian Act; Metis communities being unable to leverage a land base and access federal funding; and Inuit communities finding it challenging to secure project funding in remote, rural areas. As we outlined in previous reports, loan guarantees and other financing tools can help address access to capital and risk issues.

Historically, the speed of implementation and scaling of these tools has been slow, while capital needs are only growing. This ranges from an infrastructure capital gap of up to $270 billion1, a $30-billion gap in critical minerals2, and a $60-billion gap related to climate-aligned investments in carbon capture, electricity and renewables3. The support of both private and public lenders is needed to meet demand.

The Canada Infrastructure Bank (CIB) stepped up recently, committing $1 billion to its Indigenous Equity Initiative. CIB’s equity grants, ranging from $5 million to $100 million, have a 15-year repayment target. And in early 2024, the money started to flow. That’s when CIB issued its first Indigenous equity loan, committing up to $18 million to Wskijinu’k Mtmo’taqnuow Agency Ltd. (WMA), a limited partnership owned by 13 Mi’kmaw communities. The financing allowed WMA to take an equity stake in the Nova Scotia Energy Project, Canada’s largest planned battery storage initiative.

Another important source has been the First Nations Finance Authority (FNFA), which has enabled First Nations economic development through a pooled borrowing facility. By issuing debentures on behalf of First Nations (certified by the First Nations Financial Management Board for a clean balance sheet and good financial management practices), the FNFA has borrowed $3 billion for its members toward critical, revenue-generating projects—creating an economic output of $6.3 billion.

These aren’t the only examples of progress when it comes to unlocking capital. Last year, three loan-guarantee programs were announced. One at the Federal level (recently increased from $5 to $10 billion) and two at the provincial level—B.C. ($1 billion) and Manitoba ($500 million).

The various access-to-capital tools currently available amount to about $20 billion. And based on the amount of private investment these concessional financing tools have crowded-in, there is potential to mobilize close to $48 billion in Indigenous equity investments. This leaves a concessional financing gap of $20.7 billion and a private financing gap of $28.7 billion4.

While gaps remain, there’s more capital flowing than ever. And it’s leading to action. Between 2022 and 2024, 111 Indigenous communities announced that they had acquired an equity stake in an infrastructure project, according to a report by the Toronto-based law firm Fasken Martineau DuMoulin LLP last April. More than a quarter (26%) of those were in Alberta, home to the $3-billion Alberta Indigenous Opportunities Corporation Loan Guarantee Program. Wind generation projects resulted in a spike in Nova Scotia (23%). And B.C. rounded out the top 3 with 18%. And that was before the launch of the province’s loan guarantee program noted above5.

From a private financing standpoint, approaches to risk management need to accommodate unique Indigenous concerns, with banks recognizing that if project economics are sound, Indigenous borrowers should have an opportunity to be treated on equal footing to other market borrowers.

For existing and announced access-to-capital tools, prioritize speed to implementation, a risk-accommodative approach, and broader sectoral scope, spanning not just resource and energy projects, but infrastructure, transportation, agriculture, fisheries—essentially, any sector with a nexus between Indigenous interests and a national economic imperative.

Capacity

The added complexity of major project development requires capacity building on all sides. This includes education and training required for businesses and governments to better understand Indigenous histories, economies, cultures and priorities. For Indigenous Nations, this can include everything from financial, legal and engineering capacity required for commercial negotiations, to the environmental, historical and legal support needed to participate in regulatory and rights-based discussions. It is important to recognize that Indigenous capacity has always existed, whether through trade networks, economic systems, governance models and traditional knowledge that Indigenous Nations have built up over centuries.

Two (imperfect) measures of fiscal and economic capacity are the ability of Nations to be able to raise own-source revenues (revenues not generated through governmental transfers) and maintain financial and governance controls. We assume two proxies for these measures—own-source revenues greater than 25% of total revenues in a First Nation, and a First Nation receiving the Financial Performance Certification. The FPC is a voluntary, independent assessment by the First Nations Financial Management Board certifying good financial health and ability to borrow from the First Nations Finance Authority.

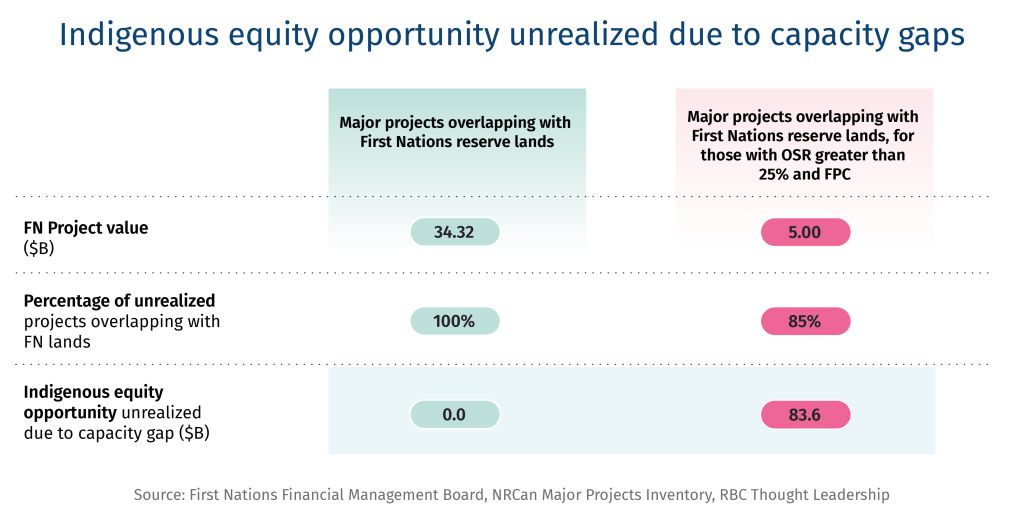

Our research indicates that capacity gaps put 85% of projects that pass through First Nations territory at risk. That’s an estimated $83.6 billion in project value.

Project Rocket, a partnership between 23 First Nations and Metis communities and Enbridge, resulted in capacity building that benefits all parties. The partnership involved the creation of Athabasca Indigenous Investments, the special-purpose vehicle behind the Indigenous Nations taking on an 12% equity stake—valued at $1.1 billion—in seven pipelines. In addition to the potential economic benefits, the dealmaking process provided technical, legal and commercial capacity for Indigenous Nations, as well as the proponents and financial intermediaries. Agreements that include multiple Nations, like this one, allow better resourced and experienced Nations to share their expertise, ultimately making it more replicable and scalable.

Indigenous-corporate partnerships, including secondments, knowledge sharing, and leader-to-leader forums can help hone capacity.

By bridging corporate and Indigenous Canada, organizations such as the First Nations Major Projects Coalition and the Canadian Council for Indigenous Business enable relationship and capacity building, and uplift Indigenous businesses and governments. Organizations like FNMPC and CCIB are positive models to emulate and scale across the country, to provide mentorship, skills-development, environmental and economic tools, procurement strategies and project-level negotiation support for and with Indigenous Nations.

Capacity building with lending or M&A teams for proponents and financial institutions must be prioritized. This can help ensure lending team members are educated on Indigenous history, economic-development priorities, and the lens through which teams must engage with Indigenous Nations.

An important consideration for businesses is whether to build capacity internally—through targeted hiring and training—or to enhance capacity through acquiring existing organizations with the right mix of commercial knowledge and Indigenous community-level expertise.

Governments should consider dedicating 2-5% of grants, loans and guarantee funds toward capacity, to empower Indigenous Nations with the right information and ability to negotiate agreements with better-resourced private-sector counterparts. Between 2% and 5% is a guideline based on past transactions.

Consent

The nature of consent varies from community to community, and project to project. Getting to a shared understanding of consent is challenging and intersects with constitutional (Section 35 and the duty to consult) and international legal obligations (UNDRIP). However, there are some necessary, but not sufficient, conditions for achieving and maintaining consent, which include engaging early and often, economic partnerships, and inclusion of Indigenous Nations in the regulatory process.

A big part of getting projects built is the permitting and regulatory process. Part of the process is seeking informed Indigenous engagement, and, where required, consent. The Government of Canada has a duty to consult and accommodate Indigenous groups when its actions may impact potential or established Aboriginal or treaty rights—a duty that has been affirmed by the courts and the constitution. As such, expediting permitting timelines, although an important objective to speed up project development, cannot be done in a vacuum without the Crown discharging its duty to consult. Proponents have an important responsibility and role to play in building deep trust-based relationships with Indigenous Nations, and through that process, seek and achieve consent.

The Cedar LNG project illustrates how federal, provincial and Indigenous Nations can expedite the permitting process. The federal government, through a process called substitution, eliminated the duplication of two assessments for a single project. And the B.C. government worked in close partnership with the Haisla Nation to identify and mitigate environmental, social, health and economic impacts—a process that was accelerated in no small part because Haisla Nation is a co-owner in the project—resulting in a shorter and less contentious permitting process (notwithstanding ongoing concerns of the project by other Nations).

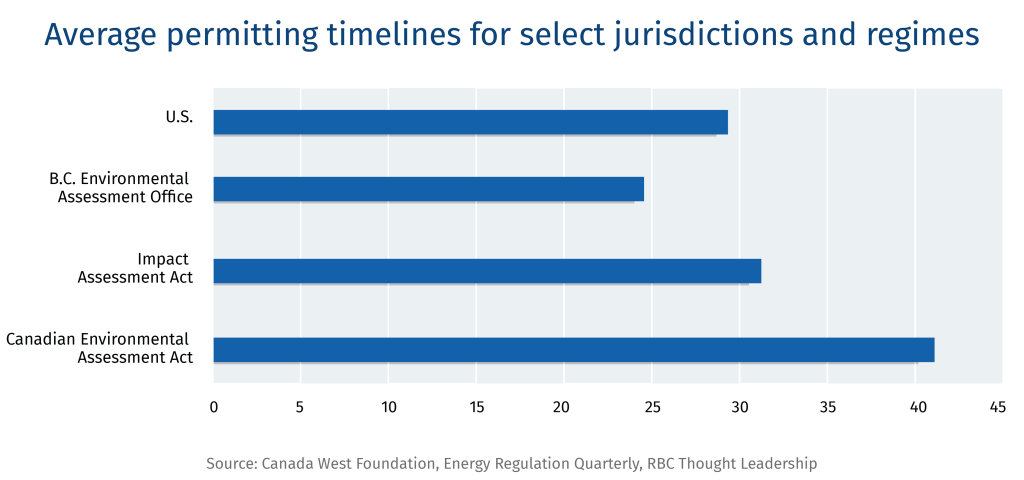

While equity ownership by the Haisla Nation on Cedar LNG likely moved things along more quickly, average assessment timelines in B.C. are, generally, some of the shortest in the country. This is partly due to proponents engaging early and often with Indigenous Nations, and provincial regulators increasingly empowering Indigenous Nations to lead assessments. The B.C. Environmental Assessment (EA) process, can integrate Indigenous-led assessments through substitution, delegation or other mechanisms. It yields a process that is 5 to 15 months shorter than the average timelines of two long-standing federal regimes and the U.S. permitting process. Federally permitted projects, particularly those that cross provincial boundaries, are complex, requiring longer permitting times. Still, the B.C. experience suggests a permitting process that incorporates Indigenous views, processes and knowledge can facilitate trust and social license.

The Eskay Creek Consent-Based Decision-Making Agreement, and the Squamish Nation Environmental Assessment Agreement both provide blueprints for how consent can be operationalized through the environmental assessment and permitting process.

The agreement, pertaining to the reopening of the Eskay Creek gold and silver mine in northern B.C., was set up under section 7 of the Declaration Act (B.C.’s legislation aligning its laws to UNDRIP). As part of the deal, the modified EA process seeks consensus through a collaboration team between the Tahltan Nation and B.C., a Tahltan risk assessment, free, prior and informed consent on the final decision, and independent dispute resolution. The agreement provides a unique model for joint decision-making, a shared environmental assessment and sustaining social license.

The Squamish Nation EA process involving the Woodfibre LNG plant and export terminal in B.C., was the first-of-its-kind legally binding, Indigenous-led EA process in Canada. A framework agreement enabled the Squamish Nation to set up a process outside the provincial and federal EA regimes. What enabled success was a parallel process of environmental and socio-economic information collection and analysis, with the final decision-making resting with the Squamish Nation Chief and Council, enabling accountability at both the technical and political levels. Buy-in for the Indigenous-led EA from federal and provincial governments, and the proponent, was crucial. And all three parties could be confident that the review addressed Squamish Nation’s concerns and interests—important for consistency of social license and support.

These approaches are not without challenges—as other Nations may seek to assert jurisdiction over those that are leading the EA process, or substantially support project development. Furthermore, this does not obviate the opposition of other interest groups, such as environmental or social groups. Nonetheless, they provide useful models of operationalizing consent through a collaborative assessment process.

Some key principles for businesses and governments when seeking and maintaining consent:

Indigenous-led assessments is one way. So is including Indigenous legal orders, traditional knowledge, values and priorities into the regulatory and assessment process through a co-assessment of projects, or the meaningful delegation of certain aspects of a project to Indigenous governments.

Relationships take investment—both time and money. Governments and businesses cannot engage on project-related issues without meaningfully building relationships to maintain consent, trust and social license for project development.

Information sharing and transparent discussions between proponents, government and Indigenous Nations is imperative.

This is challenging as it depends on both legal definitions on which First Nations the government has to discharge the duty to consult and accommodate, as well as relationship-based measures that can provide an indication of which Nations to consult. Building strong and lasting relationships with Nations, regardless of having to discharge the duty of consult, is a best practice.

Moving forward: Considerations for Canada

The geopolitical tensions with our closest ally have exposed the fault lines of Canada’s economic strategy. Trade diversification, massively building up our resource and infrastructure base, resolving internal trade once and for all, and moving up the product value chain have all become economic imperatives. Advancing Indigenous economic reconciliation is a keystone to meeting these goals. Other considerations that will drive the conversation in Canada in the months ahead will include:

What’s on the fast-track list: Both major political parties in Canada have promised to speed up development, permitting and financing of certain trade, infrastructure and resource projects in the national interest. Virtually all of the projects that will be fast-tracked will impact Indigenous interests and run through Indigenous territories. Fulsome Indigenous engagement and partnerships will determine the federal government’s ability to move at speed and scale.

The renewal of the continental security agreement: The incoming federal government will likely enter discussions with the U.S. administration on renewing the economic and security framework between the two countries. The investments needed will include surveillance, domain awareness and trade infrastructure to strengthen the North. Beyond trade and security, the social infrastructure, including housing, education and healthcare facilities, need to be built up. These discussions need to happen in close collaboration with territorial governments, Inuit birthright corporations and communities in the Inuit Nunangat.

The impact of the geopolitical contest between the United States and China: As we have explored previously, critical minerals have emerged as a key element in the new great game between the two superpowers. Canada’s ability to step in as a pinch-hitter on critical minerals mining and processing will depend on our ability to tap into mineral-rich regions such as the Ring of Fire in Ontario and the Golden Triangle in B.C. The Tahltan Nation, whose traditional territories cover 70% of the Golden Triangle, have been supportive of mineral exploration. But Indigenous claims and partnerships are yet to be resolved in the Ring of Fire—a question that will challenge other mining regions in Canada.

Generational changes in the global trading system: Changes in international trade and investment flows have countries seeking sources of economic resilience. That includes diversifying markets, but also reshoring parts of their value chain. Canada is no less immune. While these changes take effect, it is useful to remind ourselves that Indigenous Nations, as our youngest and fastest-growing population, are a source of strength and comparative advantage.

Our ability to move fast depends on our ability to move collectively. As the late Murray Sinclair, chairman of the Truth and Reconciliation Commission, said at the release of the Commission’s final report: “We have described for you a mountain, we have shown you the path to the top. We call upon you to do the climbing.”

4. Financing gap calculations are based on the capital cost of projects implicated under treaty, title and title-like, and unceded lands, multiplied by average debt-equity ratios by sector, and industry-specific assumptions on the ratio of capital that would be Indigenous-owned. The aggregate figures across sectors are multiplied by the ratio of concessional to private capital through existing loan guarantee programs, to arrive at the concessional and private capital gap. It is important to note that of the $17 billion in concessional financing tools, about $11.5 billion has not yet been implemented.

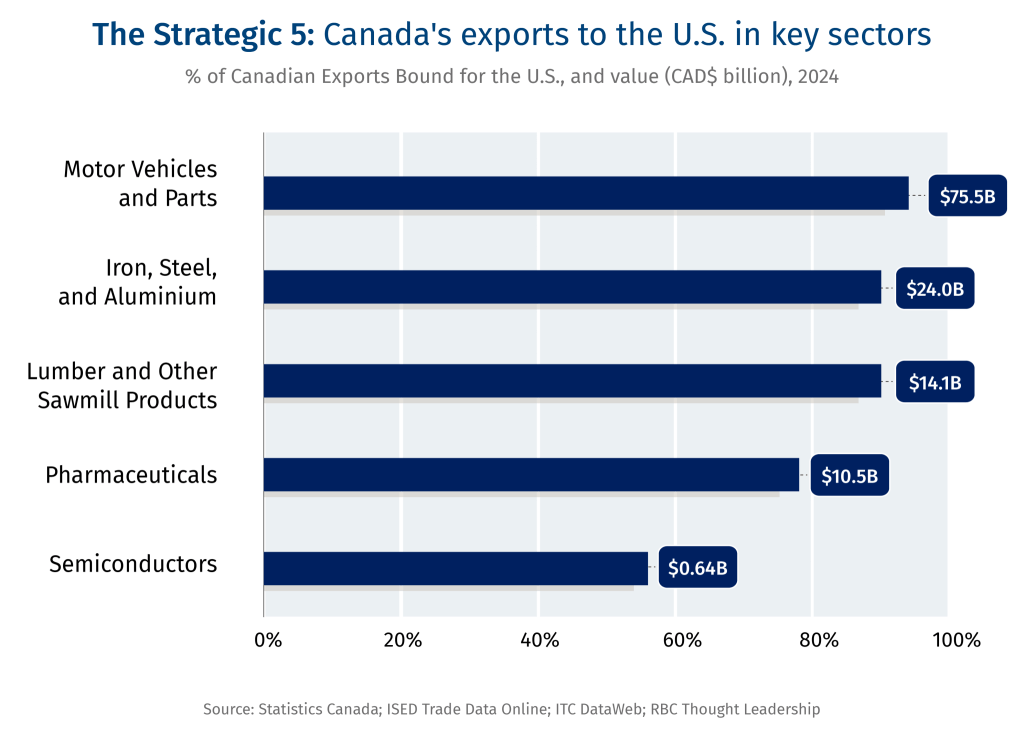

U.S. President Donald Trump believes autos, steel and aluminum, lumber, pharmaceuticals and semiconductors are the five strategic sectors that will drive American industrial revival. His overarching plans involves cutting imports (and trade deficits) and onshoring domestic production in each of the sectors and related industries. That’s emerging as a challenge for some of the U.S.’s top sector suppliers, including Canada. These five domestic sectors rely heavily on shipments south of the border and are of strategic importance to Canada.

U.S. tariffs on the Strategic 5 will likely hurt Canada’s economic prospects and could trigger layoffs and flight of capital in sectors that are vital for our energy and national security.

Here’s a look at the importance of each of these sectors to the Canadian economy:

Automotive

Exposure to the U.S. market: $75.6 billion in exports (2024)

Total U.S. market: Sales of new vehicles in the U.S. reached 15.8 million units in 2024—second only to China’s 31.3 million.1

Global market: Just over 88.2 million vehicles2 are estimated to have rolled off assembly lines worldwide last year.

Canada’s role: Domestic auto- and part- makers’ market share in North American auto manufacturing has fallen over time, with Mexico gaining ground. However, 92% of Canadian auto exports are still shipped south of the border.

Tariff status: For CUSMA-compliant vehicles, the 25% tariffs are currently in force and apply to the value of non-US content.

Canada’s response: Ottawa’s countermeasures focus on 25% tariffs on all U.S. auto parts not compliant with CUSMA. The federal government and Ontario are also easing tariffs for U.S. auto parts for companies that remain committed to the Canadian auto supply chain.

The fallout: Stellantis and General Motors temporarily laid off staff in Ontario assembly plants.

What’s next: The Trump administration is mulling a potential pause on auto tariffs—primarily to give carmakers more time to onshore supply chains.

Aluminum, steel and iron

Exposure to the U.S. market: 91% of Canada’s aluminum and 89% of its steel exports were shipped to the U.S.

Total U.S. market: The U.S. consumed 93 million tonnes of steel in 2024—with Canada supplying 6.4 million metric tonnes of the total.3

Global market: Global aluminum demand has steadily increased over the past decade, driven mostly by growth in Chinese demand and from sectors like construction and transport.

The U.S. has had an average trade deficit in aluminum with Canada of about US$7 billion annually over the past five years.4

Canada’s role: We are a top foreign supplier of aluminum and steel to the U.S., ahead of China and Mexico.

Tariff status: The 25% U.S. tariffs on aluminum and steel imports from Canada are triggered by American efforts to bolster its domestic industry. The first Trump administration had also imposed tariffs on Canadian aluminum for 14 months, lifting them after USMCA was ratified in 2019.

The fallout: Hundreds of workers in the aluminum and steel industry have already been laid off since the latest tariffs came into effect.6 Ottawa is taking several measures to support Canadian workers and businesses.

What’s next: Commerce Secretary Howard Lutnick says reprieves on steel and aluminum tariffs are unlikely. With aluminum featuring on the USGS Critical Minerals list and a new probe on U.S. critical mineral imports underway, Canada’s aluminum industry may need to gear up for further uncertainty.

Lumber and other sawmill products

Exposure to the U.S. market: $14.1 billion in exports—90% of Canada’s total lumber exports.

Total U.S. market: The U.S.’s trade deficit against Canada in softwood lumber averaged US$5.8 billion annually over the past decade, according to the U.S. International Trade Commission.

Global market: The US$788 billion global wood products market is expected to nearly double in value by 2033. We wrote recently on how Canada can capture a greater share of the global opportunity.

Canada’s role: Canada’s domestic consumption of softwood lumber has fallen 11% from a decade ago. Domestic demand, which has generally followed housing starts, reached a 23-year low in 2023.

Tariff status: Under the Biden Administration, the U.S. raised duties charged on Canadian softwood lumber imports to 14.5% in August 2024. These tariff rates remain in place with additional hikes on the horizon.

The fallout: The lumber industry is already facing regulatory headwinds that have forced closures of sawmills in B.C.

What’s next: U.S. tariffs on softwood lumber imports are set to increase to 34.5% and could come into effect in the fall.

Pharmaceuticals

Exposure to the U.S. market: $10.6 billion in exports.7

Total U.S. market: Prescription drug sales in the U.S. were $716 billion in 20228 , or about 2.8% of U.S. GDP.

Between 2019 and 2024, the U.S. has run an annual $1.2 billion trade deficit in pharmaceuticals with Canada, according to U.S. International Trade Commission data.

Global market: Pharma R&D spending is expected to top US$200 billion9 this year.

Canada’s role: The U.S. is Canada’s primary pharmaceutical export market, accounting for 78% of its pharma exports in 2024. Japan, the next largest export market, received 5% ($720 million) of exports, followed by China, at 2% of exports, or $276 million. The Canadian pharma industry employed 35,367 workers in 2024.

Tariff status: Originally exempt from the April 2 reciprocal tariffs, the White House has now officially launched an investigation into the national security impacts of pharmaceutical imports.

The fallout: Industry is warning of a spike in costs of drugs and even shortages of key medicines.10

What’s next: Major tariffs on pharma could be on the horizon.

Semiconductors

Exposure to the U.S. market: $637 million, or 56% of Canadian semiconductor exports, in 2024.11

The U.S. runs a trade surplus in semiconductors with Canada, reporting a surplus of $764 million in 2024.

Global market: Global semiconductor sales were estimated at $627 billion in 2024.12

Total U.S. market: Companies involved in the semiconductor ecosystem plan to invest nearly US$450-billion in more than 90 new manufacturing projects in the U.S. across 28 states, according to an industry association.13

Canada’s role: Canada is emerging as AI hub with its clean and cheap electricity seen as a competitive edge. A recent RBC Thought Leadership report, published before the trade turmoil, estimated Canada could attract nearly $100 billion across 20-30 data centres. Disruptions to the nascent chip supply chain could disrupt that potential capital flow.

Tariff status: The U.S. announced probe into chip and electronics imports in early April, paving the way for new tariffs.

The fallout: Several tech companies have seen their stocks drop.

What’s next: Some reports suggest Trump will announce new tariff rates on imported semiconductors next week, with flexibility for certain companies. Secretary Lutnick said it would likely come in “a month or two.”15

To check the pulse on the agri-food industry, RBC’s Thought Leadership team met with farmers from across Canada last week—from pork producers in Manitoba to members of the fruit and vegetable industry gathered in Montreal for their annual tradeshow.

What’s clear is that the industry is highly motivated to keep up the momentum; last year, Canadian agri-food export value was a record $106 billion. And all eyes are on commodity prices, U.S. farm policy and, of course, the impact of U.S. President Donald Trump’s tariffs.

What we heard:

Many farmers are adopting a keep calm, carry-on approach. Farmers are accustomed to volatility, the result of managing through unexpected weather conditions, shifting commodity prices and equipment breakdowns. Trump’s tariffs are seen by many as just another disruption. That’s led some to ride out the resulting pricing swings (i.e. canola). Others, including grain and oilseed producers, are considering shifting the crops in rotation for the 2025 planting season, a direct result of China responding to Canada’s EV tariffs with their own on peas and canola products.

Meeting the moment for Canadian-made items. The increased demand for made-in-Canada products is leading to American-made spoilage at grocery stores. The movement adds to the push for expanding Canada’s greenhouse sector acreage and diversity of products to close our production-consumption gap for fruits and vegetables.

Canadian food producers and processors are working to bulletproof their USMCA-compliancy. Companies are preparing for scrutiny at the border to prove they are USMCA compliant and adhering to the rules within, such as country-of-origin. Just 0.1% of all agri-food products traded in 2024 were likely not USMCA-compliant but more than a third of Canada’s agri-food exports, albeit compliant, did not trade under the agreement.

Trade diversification is underway. It is, however, yet to be seen if Canadian retailors and traders are going to be able to get like-for-like on quality and price for food products. Exporters and retailors are exploring where else they can source the products they need for their customers. But will Canadians want to buy a Moroccan orange over one from Florida?

Can our ports handle our growth and diversification ambitions? Canada’s turn-around times are slower than key agri-food competitors, including the U.S., Australia and Brazil. The potential influx of product flow at Canada’s ports due to rising costs of moving goods through the U.S. may cause greater congestion and bottlenecks if Canada is not preparing for growth.

3 things to watch:

Emergency U.S. farm support and its impact on Canadian farmers’ competitiveness. The USDA’s Emergency Commodity Assistance Program (ECAP) is a $10 billion one-time economic assistance payment program to help farmers mitigate the impacts of increased input costs and falling commodity prices. For example, U.S. farmers can receive upwards of $77.66 per acre of oats and roughly $30 per acre for soybeans and wheat.

Cuts to U.S. agriculture research programs and services. The dismantling of USAID and cuts to its funding to 19 land-grant university-based innovation labs across 17 states, as well as proposed cuts to NOAA’s climate research can undermine agriculture innovation and risk halting essential services such as weather monitoring.

Risk of rising costs and disruptions for supply chains running through U.S. ports from New Orleans to Philadelphia. Trump’s April 9th executive order, Restoring America’s Maritime Dominance, instructs U.S. Trade Representatives to proceed with a proposal that includes a $1M docking fee at US ports for any ship that is part of a fleet that includes Chinese-built or Chinese-flagged vessels. On top of cost risk, U.S. custom services could slow down these just-in-time supply chains needed to bring Peruvian blueberries to Canada.

This month marks the 100th anniversary of the publication of The Great Gatsby, the F. Scott Fitzgerald novel set in the Jazz Age when American wealth and power soared, and yet the characters clung to the vestiges of an earlier golden age.

Sound familiar?

A couple of weekends ago, I spent some time not far from the mythical Gatsby home, at another estate left by the Whitney dynasty to a foundation that the family created to support peace and sustainability. About three dozen policy leaders from the U.S., Europe and Canada gathered at Greentree, on Long Island, to discuss how business can adapt to Donald Trump’s world—and his promise of a new golden age—and also shape it.

Some of my takeaways from our discussions, which began as global markets began a sharp decline:

1. China will become the defining force of this Administration, which may need to consider “managed interdependence.”

2. The U.S. dollar remains an enormous challenge to America’s trade competitiveness and will continue to be overpriced as long as Washington runs enormous deficits.

3. Trump Republicans hold a special dislike and distrust of Europe that will be hard to resolve, and a peculiar like for Britain.

4. Tariffs won’t fix underlying U.S. frustrations, which are rooted in long-term labour productivity and real wage stagnation.

5. While trade is being blamed for middle America’s economic malaise, technology has caused more job displacement over the last 25 years.

6. America, and others, need to focus on training and reskilling to improve wages and incomes in the coming age of AI.

7. Tariff execution will be a challenge if Trump reaches (or has reached) a political high-water mark, as he will have to spend more energy on opposition forces, including more than 100 lawsuits.

8. Major businesses in Europe and North America need to come together in a more united way to project the case for more economically rational policies.

Read the speech John delivered at the conference here:

All three topics were on full display at Columbia’s Global Energy Summit 2025. Tariffs and trade policy dominated the Summit, with significant implications to both the supply and demand of North American energy. Shaz Merwat, Energy Policy Lead of RBC’s Climate Action Institute, was in attendance and shares the five most pressing themes at this year’s event.

1. Energy risks becoming more complex

The push to re-orient trade flows to manifest specific economic outcomes (reduce a trade deficit, reshore production) likely increases price risk through a bifurcation of supply and demand in key commodities. At the most obvious, tariffs levied on steel, aluminum and possibly copper–all key inputs to energy infrastructure–result in regional pricing. As seen in the chart below, U.S. aluminum prices have largely decoupled from European pricing as a result of Trump’s tariffs. Similarly, price differences between U.S. Midwest hot rolled coil steel prices (US$1,075/tonne) and Northern Europe hot rolled coil steel (US$715) has increased to about $360/tonne, compared to $150/tonne at the start of the year.

Geopolitically, risks are also expanding beyond the simple ‘Middle East’ supply risk that we have known for the last half century. Spheres of influence can re-orient supply and demand relationships, especially in the case of LNG and critical minerals. These emerging geopolitical trade barriers ultimately weaken an otherwise more ‘global’ market to absorb supply and demand shocks–which likely are more deliberate at a time when weaponized trade is becoming increasingly more common (Russian gas, Chinese supply chains, the American market).

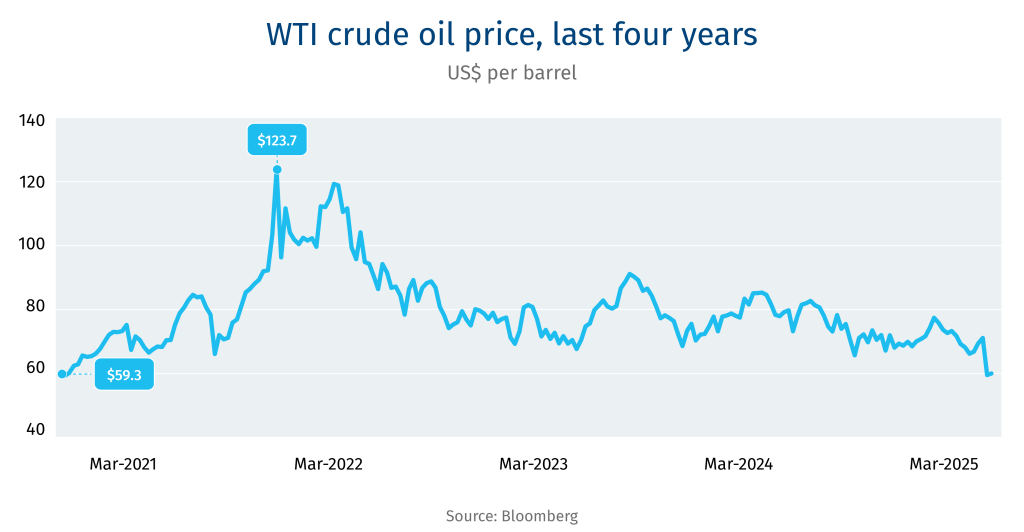

2. What is this energy dominance you speak of?

While the Administration has vowed to unleash U.S. energy dominance, to date, it appears to have done the exact opposite. On oil, Trump’s trade/tariff agenda has driven oil prices lower than those witnessed for most almost all of Biden’s presidency. WTI has twice dipped below US$60 per barrel in the past week–a level widely seen as U.S. shale’s breakeven–leading to increasing concerns of idled rigs and declining production; S&P Global estimates US$50/bbl oil could cause a U.S. production decline of 1 million bbl/d. All the while, OPEC is boosting production.

The continued desire to gut funding for the Inflation Reduction Act also stymies U.S. renewable energy, even for tax credits deemed friendly to the oil industry (such as the 45Q carbon capture tax credits). Lastly, concerns around supply inflation (steel/aluminum tariffs) and general market/economic uncertainly has created a very challenging environment to deploy capital.

3. Climate trade frictions remain alive and well

With the gutting of the WTO and Trump’s reciprocal tariffs, developing nations are increasingly seeing their preferential trade terms (higher ‘allowable’ tariff rates) erode. You can add climate to that list, as nations impose climate-related trade measures to enhance economic competitiveness.

In Europe, carbon border adjustments protect domestic carbon policy. In the U.S., a border pollution fee leverages America’s carbon advantage–especially in relation to China. The U.K. and Australia are also exploring carbon border adjustments of their own.

Domestic carbon policies without a climate trade measure (such as a CBAM), politically, is almost certainly bound to fail. Yet, expectations for developing nations to enact similar carbon prices as the E.U.’s emissions trading scheme–a system that has seen carbon pricing increase/expand over the last two decades–in a mere few years, seems unjust. This likely only accentuates climate trade tensions between North and South.

4. Reducing the trade deficit

In the eyes of U.S. President Donald Trump, reciprocal tariff rates yield a balanced trade relationship. For trade partners, a balanced trade relationship is as good as a ‘due north’ one can expect under Trump’s vision of America First. Trade partners will be served well if they can better house American (merchandise) exports.

In this world, U.S. LNG likely shines bright. The country is expected to surpass Qatar as the largest provider of U.S. LNG, globally, by 2030 according to RBC Capital Markets forecasts as seen below. For major LNG buyers that run large trade surpluses with the U.S. (the E.U., Japan, Korea, India), greater purchases of LNG supply can be the ‘easy’ win.

5. AI clusters and cross-border data flows

Nations with abundant, cheap electricity are best positioned in the race to build data centers. This likely results in supply ‘clusters’, especially torqued to renewable generation given the climate commitments of tech firms. Consensus is increasingly pointing to Canada, the U.S. and the Middle East as becoming cluster of American artificial intelligence deployment.

But what does that mean for data flows? Data protectionism towards data hosting (colocation) likely remains, but more alignment is needed on cross-border data transfers resulting from compute capacity (hyperscale). We expect more on this in the renegotiation of USMCA in 2026.

Shaz Merwat is the Energy Policy Lead of RBC’s Climate Action Institute

Starting April 5th, the U.S. is imposing 10% baseline tariffs, with most countries facing a tariff rate that appears to be based on a calculation of trade deficits as a share of exports from that country. Crucially, it exempts Canada and Mexico as it’s not applied to USMCA-compliant products.

Here are six impacts we’re watching out for:

1. Canada lives to fight another day, but not without some pain.

Existing tariffs remain, including those based on IEEPA/fentanyl , steel and aluminum and auto and auto-parts that went into effect just past midnight today. Duty-free trade still applies to products that are USMCA compliant—perhaps a signal that the President still takes the agreement he signed seriously.

Most, if not all, Canadian auto manufacturers have 50% S. content, which means an effective tariff rate of 12.5%. Combined with a 70-cent Canadian dollar, it puts Canadian auto and parts makers in relatively good stead, especially in comparison to Asian and European automakers facing up to 25% in tariffs.

The story on energy is similarly that of relief—RBC Capital Markets highlighted how most, if not all, oilsands producers are USMCA compliant, and not be subject to the 10% tariff on energy. A 10% tariff on other resource products and potash, although significant, is not enough to affect producers’ bottom lines.

While we may see specific provinces and sectors negotiating for exemptions, most will likely not want to rock the boat until the federal election is over on April 28, and an economic and security partnership can be negotiated. But Canada isn’t out of the woods yet—lumber is still in the U.S. administration’s crosshairs, and President Donald Trump alluded to a longstanding irritant of his in Canadian dairy.

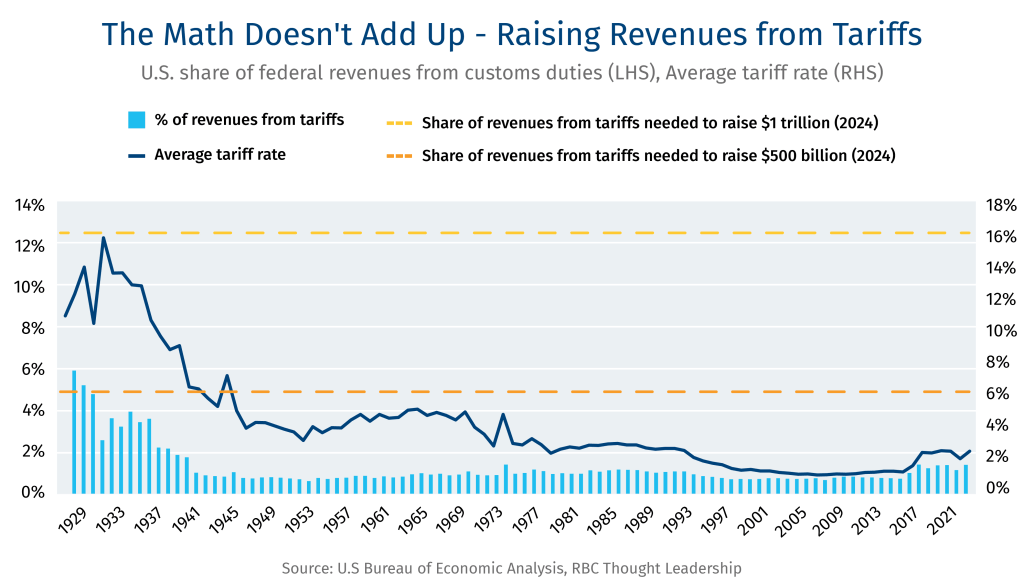

2. It’ll be hard to raise revenues (only) from tariffs.

To fund tax cuts, President Trump and Secretary Howard Lutnick’s stated goals are to raise US$1 trillion in revenues from tariffs and achieve another US$1 trillion with an aggressive program of cost-cutting through the Department of Government Efficiency. But the math doesn’t add up.

The government would have to generate 12.4% of total revenues from tariffs to raise US$1 trillion—something the U.S. government has not achieved in the past century, even during the height of the Smoot-Hawley tariffs in the 1930s. Even the more modest goal of US$500 billion seems hard to achieve given the U.S. federal government hasn’t raised 6.2% of its revenues from tariffs since 1929—when the Great Depression started.

3. Will China deviate from its targeted retaliatory approach?

China now faces an effective tariff rate of 54%, on top of tariffs on steel and aluminum and those levied under the IEEPA. The Chinese government has historically responded with targeted retaliatory tariffs, particularly on agriculture and geared toward swing states or those voting Republican. However, these are the highest effective tariff rates ever levied on China. It will be interesting to see if Beijing sticks to a strategy of targeted action, or one that will be more sweeping. Regardless, a trade war between the world’s two biggest economies will cause significant economic ripples and rejig supply chains.

Of note, China recently entered exploratory talks on a regional free trade and investment agreement with Japan and South Korea, two countries that are not traditional Chinese allies. This is an important signal that countries in Asia and beyond are creating bulwarks and buffers against a United States that they increasingly see as threatening and unpredictable. These developments may isolate Canada even further.

4. The price of the climb down may be steep.

Trump explicitly signaled to countries that he was willing to negotiate concessions in exchange for reduced trade actions. The cost of these concessions will be worth watching, with the countries first in line to negotiate exemptions (especially the ones most exposed to U.S. trade actions) likely getting a raw deal. Expect the coming few days, before the tariffs officially come into force, to be a lobbying frenzy in D.C. as countries most exposed to U.S. trade action try and negotiate lower rates.

Allied Retaliation: Trump explicitly warned countries that teaming up against the United States to retaliate would yield higher tariffs. Canada may not wish to gang up against the United States as the degree of integration between our economies does not favour Canada. But expect the Canadian government to partner with allies on strategic sectors, such as critical minerals or semiconductors, to press against U.S. trade action and to share a more unified message on the costs of a full-blown tariff war on sectors with strategic or national security importance.

5. Congressional rancor over the trade deficit emergency.

On the other side of Pennsylvania Ave., the Senate voted to pass a joint resolution to strike down the emergency Trump used to levy tariffs on Canada, with four Republicans joining the Democrats. The joint resolution is unlikely to pass the House, where caucus discipline is more strongly enforced, but it is still a repudiation of Trump’s trade policies against the country’s closest ally. The President used the same authorities, stemming from the International Economic Emergency Powers Act, deeming trade deficits as a national emergency. Expect to see another fight in Congress as the legislature seeks to regain control over trade and tariff policy, and as Democrats use the joint resolution as a cudgel to split the Republicans and a referendum on Trump.

6. Global macroeconomic and supply chain shocks.

The bigger channel of impact of these tariffs—and the biggest unknown—will come from governments and businesses completely reshaping the trading links that have been built over the past century. Some companies may choose to reshore production to the United States, while many others may avoid the U.S. completely. Regardless of how the tariffs are implemented, the macroeconomic effects of uncertainty are significant and dire, as our Economics team has noted, pushing up the U.S. effective tariff rate over 20%.

Trump appears to want to achieve multiple goals through his policy instrument of choice, including reshoring investment and trade flows, strengthening the greenback, raising revenues and using tariffs as economic leverage to achieve other policy outcomes. It is unclear whether he will be able to achieve all these goals. What is clear is that this is only the beginning of a rocky ride for the global economy, and for Canada.

Varun Srivatsan is Director, Policy and Strategic Engagement, RBC Thought Leadership