In this week’s edition: Trade signals at the G7, why it’s so hard for steel and aluminum manufacturers to diversify from the U.S., and how long it typically takes to get a major trade deal done.

The week that was

Reports surfaced (here and here) that Canada and the U.S. have a working trade document, including details of a potential deal. No timeline yet.

With Mexico’s Claudia Sheinbaum and India’s Narendra Modi in Kananaskis for the G7, could moretrade talk with Canada be on the agenda?

According to the World Bank, we’re about to experience the slowest decade of growth since the ’60s–the result of uncertainty caused by tariffs.

While Trump celebrates a “done deal” with China after two days of negotiations, word from China is more muted—Beijing’s official news agency called it an “agreement in principle.” China is said to only be lifting restrictions on rare earth minerals exports for six months leaving open the possibility of future escalation.

In the next week or two, Trump plans to send letters outlining unilateral tariffs to many countries.

Tariffs have yet to generate the inflation jump in the U.S. that many expected. Just wait, say economists.

Dominican Republic has become a hot spot for U.S. companies seeking alternative manufacturing hubs. The country’s 92 free zones and proximity to the U.S. are two key factors.

Trade signals at the G7

While there may not be a major breakthrough with the U.S. on tariffs and trade at the G7, there are certainly a couple things to keep an eye on:

Critical Minerals: The U.S. trade war with China exposed major dependencies on critical and rare earth mineral supply chains, which Beijing dominates. To feed its lofty energy and tech ambitions, the Trump administration needs a reliable supply. Collectively, the G7 possesses massive untapped resource potential, and the capital needed to fund projects.

USMCA: Claudia Sheinbaum’s attendance will mark the first time since Trump’s inauguration that all three North American leaders are participating in the same multilateral meeting. This unlocks the potential for a sideline meeting to chart a course for the 2026 USMCA review and discuss ongoing efforts to combat the issue of fentanyl that remains the core justification for the U.S.’s IEEPA tariffs on Canada and Mexico.

Noteworthy

By Jordan Brennan

I was in Ottawa this week at Canada 2020, where the general sentiment among attendees was cautious optimism. The focus was on reigniting growth through nation-building projects. And while opportunities abound—in energy, mining, housing, infrastructure, AI—a rebooted operating model is needed. A few themes stood out:

Internationally, Canada is seen as a high-risk jurisdiction thanks to regulatory delays (i.e. impact assessments that can stretch over a decade) and political instability (think rising separatist sentiment in Alberta). It was noted that international investors routinely add a 20% risk premium to capital allocation decisions involving Canada. Then there’s the broad political discretion cabinet holds over major projects. To unlock capital at home and abroad, we’ll need more regulatory and political certainty.Could a national trade corridor strategy help reduce Canada’s perceived risk profile?

Building export infrastructure assumes we’ll develop the resources to fill it—but many projects remain stalled or cancelled. So how do we responsibly move resources from Canadian soil to global markets? Here, treaty rights and the duty to consult First Nations come into focus—not as a hurdle, but as a competitive advantage. Successful companies build full economic partnerships with First Nations early in the process—on everything from impact assessments, employment and procurement agreements and equity stakes. If we want more projects approved—and faster—this kind of partnership is essential.

Same goes with Arctic security. With the retreat of sea ice, the Northwest Passage is being contested by foreign powers in part because it dramatically shortens the shipping time between North America, Europe and Asia. As one panelist put it, there’s no better way to assert Canadian sovereignty in the north than by developing the region. That means infrastructure—digital and physical—as well as the jobs and skills tied to mineral development.

Another challenge is timing. While resource prices are set on volatile global spot markets, projects like LNG terminals or major mineral developments have multi-decade lifecycles. Development must be aligned with future demand patterns, yes, but we must also be hyper-focused on cost competitiveness. Forecasting global energy and mineral needs in 2050 is daunting, but essential if we’re to attract the patient capital needed for big projects.

Three questions…

With the U.S. doubling tariff rates on steel and aluminum, Jake Silverthorn on RBC’s Capital Markets Diversified Industrials team, helps us understand the current landscape.

Q: Why are Canadian steel and aluminum producers more impacted from U.S. tariffs than vice versa? A: There is a structural difference between U.S. and Canadian markets. Canadian producers mostly operate in spot markets while U.S. producers use contract-based transactions, which makes it difficult for Canadian companies to effectively pass through tariff costs. Additionally, the tariffs have created a demand and pricing imbalance between the U.S. and Canadian markets.

Q: Why is it hard for Canadian producers to diversify away from the U.S. market? A: Given high shipping costs, the U.S. represented the most profitable destination. Canadian producers have strategically placed their operations near U.S. ports to make shipping easier.

Q: What can Canadian producers do to maintain their U.S. market share? A: To remain competitive with the domestic U.S. producers and maintain existing operations, Canadian producers are expected to absorb part of the tariff costs, impacting margins and cash flow.

Bottom line

917

The number of days a typical trade deal takes to complete from start to finish (The USMCA took 896 days). In April, Trump promised 90 deals in 90 days. With just a couple weeks remaining on that self-imposed deadline, the U.S. has signed 1 deal (U.K.) and has scored a tariff truce with China.

Tackling Canada’s housing shortage will require $2 trillion in capital deployment over the next 5 years—that’s a 5X increase from current levels

Two taxation tools—tax-free municipal bonds for housing and infrastructure, and tax credits for affordable housing—have spurred housing supply in the U.S., attracting $5 in private capital for every $1 of foregone taxation revenue

Municipalities could cut housing costs by 20% by financing infrastructure with municipal bonds.

The housing shortage in Canada has reached a crisis point.1 An estimated 3.5 million new homes are needed to keep up with demand.2 A staggering number, especially compared to the U.S., where the shortage is 12 times smaller, on a per capita basis, despite having eight times the population.3 Canada’s growing housing shortage has contributed directly to affordability challenges. Average home prices have sky-rocketed in recent years—particularly in Ontario and British Columbia, which accounts for two-thirds of the country’s shortage—such that prices are now nine times household income.4

The federal government proposed a National Housing Strategy in 2017. But the program has only delivered 10% of its commitment to build 131,000 affordable rental homes.5 Mark Carney’s government has now pledged to spend the bulk of its $36-billion housing commitment on prefabricated homes. Tax cuts and concessionary financing for developers round out the government’s policy package.

It’s a start, but more can be done. The U.S. approach to housing can be instructive in how to attract continuous private capital into homebuilding. Canada and the U.S. both provide government subsidies to encourage developers to build more affordable rental and ownership housing. Canada’s preference is grants or concessionary financing, for rental housing, and waiving of government fees, and downpayment support for first-time homebuyers.6 This policy playbook requires the federal government, and provincial governments to a more limited extent, to fund these programs through direct capital outlay.

The U.S. relies more on federal tax incentives to draw in money from corporate, institutional, and mom-and-pop investors to finance housing and housing related infrastructure, including roads and stormwater sewers. At the heart of the U.S. taxation playbook are two tax tools: tax-free municipal bonds and a low-income housing tax credit for affordable housing.7 In 2024, these tools cost the U.S. Department of the Treasury a combined US$59.1 billion—1.2% of all federal revenue—but crowded in nearly US$500 billion in direct-equity investments.8

The introduction of similar federal income tax changes in Canada could achieve a housing trifecta: increased supply, improved affordability, and more sustainable homes. By our estimates, housing costs could decrease by 20%. These savings would allow developers to free up more capital, enabling them to build twice the number of projects with the same amount of equity financing. An acceleration of building activity that could help the Carney government fulfill a key priority: making housing in Canada more affordable.9

Tax-free Municipal Bonds

U.S. local governments have the power to raise debt in public markets, through bond issuances, to finance operating and capital needs, including housing. Local governments have US$4 trillion in outstanding municipal debt, and the U.S. municipal bond market is the largest, globally.10

The demand for local government debt can largely be attributed to the tax shield it provides investors. Holders of municipal debt, mainly institutional and retail investors, do not have to pay income tax on interest earned on these bonds.11 Since investors are willing to accept a lower rate of return in exchange for lowering their tax obligations, local governments can borrow from the public debt markets at lower costs, typically 100 to 160 basis points lower than taxable bonds with similar risk characteristics.12

To prevent the misuse of proceeds, the federal government places restrictions on what can be financed. Proceeds are principally used to finance projects where the benefits flow to public rather than private interests. To be considered for public purposes, bonds must meet one of the following criteria: more than 90% of the proceeds are used by a government entity, or less than 10% of the proceeds are secured for a property that is used in a trade or business. Municipal bonds that satisfy either of these conditions are classified as government bonds and the federal government does not impose a cap on the amount of debt that can be issued.

Activities that fail to satisfy either of these tests but provide both public and private benefits, such as multi-family residential housing projects, green buildings, and sustainable design projects,13 are eligible for financing with a type of municipal bond classified as a private activity bond (PAB). Unlike government bonds, PABs are subject to capital raising limits, which is US$48 billion in 2025.14 While PABs are used to fund a variety of initiatives, they are critical for developers building affordable housing projects. About 44% (or US$18 billion) of PABs are used to finance affordable rental housing projects, in 2022.15

Low-Income Housing Tax Credit for Affordable Rental Housing

A second tool in the U.S. tax code playbook are low-income housing tax credits (LIHTC). Since its inception in 1987, the LIHTC has been responsible for the development of 7.8% of new U.S. housing stock, or 3.65 million units of affordable housing.16

Two types of credit exist, a 4% and a 9% tax credit.17 The 9% tax credits are allocated to states annually by the Internal Revenue Service (IRS). In 2025, credits are capped at $49.6 billion. States distribute these credits to eligible projects, and eligibility criteria is refreshed annually, to remain aligned with each state’s affordable housing priorities, including the construction of greener or more energy efficient homes. The 4% tax credits are awarded automatically to projects that receive 50% of funding through tax-exempt municipal bond financing. There’s no ceiling on the amount of 4% tax credits available each year, since developers apply for the credit directly with the IRS.

While there are several approaches to accessing the 9% tax credit, the most common is for a syndicator, typically a bank, to play match maker between developers and investors. A limited liability corporation (LLC) is formed in which investors are the limited partners owning 99.99% of a housing project, and the developer as the general partner owns 0.01%. The developer flows to investors the tax credits they receive from their state housing finance authority once a project is occupied. Investors in return provide equity financing to developers, that’s generally $0.90 on the dollar for a credit. These investment partnerships are structured to last 15 years, which is the mandated affordability period in the tax code. At the end of the 15-year holding period, the investors, who are mainly corporations, have the option to sell the housing project back to the developer or enter a new deal for the same property.18

Investors in LIHTC are mainly motivated by the after-tax returns on their equity investments. As a result, they are comfortable with providing 80% equity financing for a project where they will receive lower returns because their contributions will be used to lower rents. Investors internal rate of return (IRR) of after-tax savings range from 350 to 800 basis points which on the upper end of the IRR range is almost twice the yield of a 12-month U.S. treasury bond.19 Two forms of tax savings exist—general tax savings and income tax savings. The former is realized through asset depreciation and operating losses. Income tax savings are realized by using the tax credits to offset federal income tax liability for 10 years, although the credits can be recaptured if the housing project fails to comply with rent and income requirements.20

Tax credits, while benefiting investors and businesses, come with a downside cost: foregone taxation revenue, which, as noted above, cost the government US$59.1 billion in 2024. On the positive side, the LIHTC is estimated to crowd in US$2 of investment spending for every dollar in foregone revenue. The multiplier effect is even more staggering for municipal bonds, crowding in US$10 of private investor capital for each dollar in foregone tax revenue.21

What’s required to adopt the U.S. tax playbook in Canada

Investment tax credits and tax-free capital gains are not novel taxation concepts in Canada. The federal government’s Multiple Unit Rental Building (MURB) program, which ran from 1974 to 1981, permitted retail investors in rental apartments to lower their income tax obligations by claiming capital depreciation and other costs against their income. The program, which cost the federal government between $1.3 and $2.1 billion in foregone taxation revenue in today’s dollars, was eventually discontinued due to its ineffectiveness in creating below market rental housing and lowering rental construction costs.22

The U.S.’s LIHTC program is like Canada’s MURB program in providing tax incentives to attract private capital to finance affordable housing projects. But it differs in its prescriptiveness, governance, and tax-incentive design, which draws in more corporate and institutional rather than retail investor capital. By imposing thresholds for income and rent levels, along with a 15-year compliance period, the program has been successful in ensuring a steady supply of affordable rental housing that’s privately owned. The effectiveness of the program is further enhanced because states are given the flexibility to tailor the program to meet regional priorities, such as Washington state’s preference for projects that are located near mass transit.

Adopting the U.S. affordable housing taxation playbook in Canada will require all orders of government to tweak or introduce new legislative or governance changes in how they deliver and fund housing, and housing-related infrastructure. The greatest shift will be required at the local government level. There, long-standing capital budgeting practices will need to modernize to leverage debt financing that’s available from institutional investors.[1] The crowding in of private capital, however, hinges on the federal government making the necessary changes to its tax code, as the quantum of benefits of similar tax code changes at the provincial level are insufficient for investors.

Federal Government

The federal government would need to enact tax code and governance changes to implement a low-income housing tax credit and a tax-free municipal bond regime in Canada.

For tax-free municipal bonds, changes are required to the Income Tax Act to exempt interest earned on municipal bonds. Guardrails would be needed to ensure bond proceeds are earmarked for housing related infrastructure projects, such as watermains and sewers. To encourage green infrastructure, the government could also impose a requirement that proceeds be used to build low-carbon infrastructure, such as district energy systems using waste heat. Both guardrails could be achieved by defining the circumstances when interest earned on municipal bonds is not income. For these changes to work, municipalities would need to develop borrowing frameworks, such as a social debenture framework or a green debenture framework, which specifies how bond proceeds will be used.

Changes to the Income Tax Act would also be required to create an investment tax credit for the financing of affordable housing, along with corresponding eligibility criteria of what constitutes affordable housing. To encourage the construction of greener homes, the Department of Finance could replicate the IRS’s approach of defining a range and type of eligible projects.

The final broad change that may be required at the federal level is the expansion of the Canadian Mortgage and Housing Corporation’s (CMHC) mandate to administer the income and rent limit elements of a LIHTC program, if its current remit related to core housing need does not include these activities.

Provincial Governments

Canadian provinces do not have housing financing agencies but could leverage housing ministries or departments to administer the provincial components of an LIHTC program. The mandate of these ministries and departments may need to change to encompass all provincial-level elements of a program, such as setting housing priorities, scoring applications, allocating tax credits, and monitoring compliance.

Municipal Governments

For decades, municipalities have been permitted to raise capital through bond issuances and loans to fund capital projects, but rarely for affordable housing.24 This is partly because the federal government along with the provinces are the key funders of market and non-market housing programs, aimed at housing affordability and more recently at climate change. Ontario is the only province where municipalities are actively engaged in funding affordable rental housing, mainly government-owned community housing.25 Funding for these initiatives is primarily paid for by revenue generated from municipal property taxes and user fees, and, in rare cases, municipal bonds, with the latter confined to the largest cities with a growing population and stable economic base, such as Toronto.

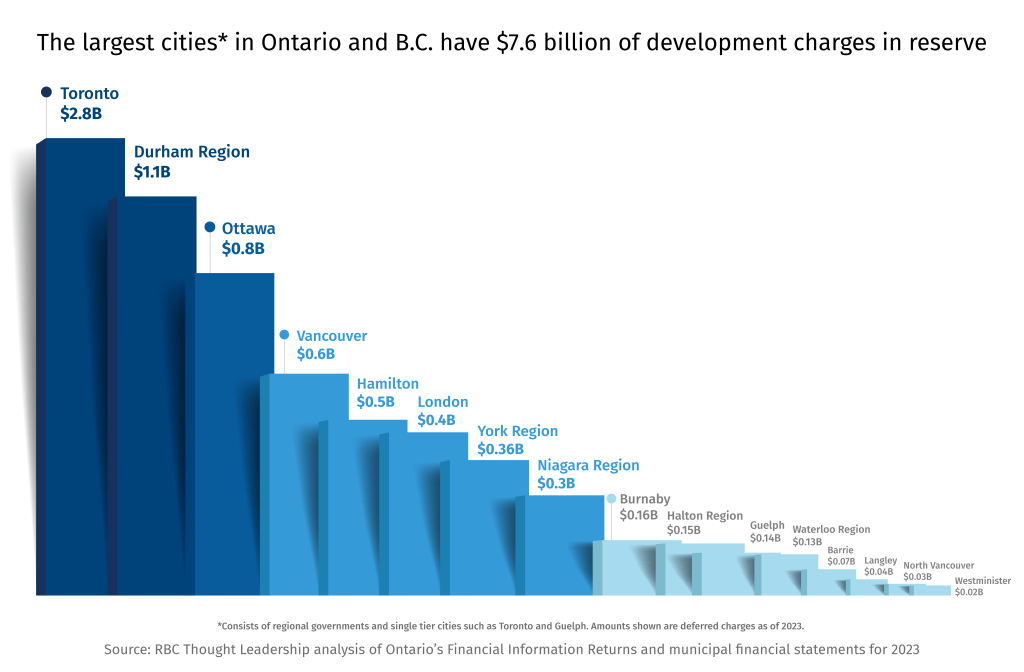

We are not proposing municipalities adopt the U.S. municipal bond playbook wholesale, whereby municipalities directly fund affordable housing with bond proceeds.26 Such a proposal may be unworkable in provinces that require public money to finance only public assets. Instead, we encourage municipalities, especially those in Ontario and B.C., to study the costs and benefits of paying for infrastructure with long-term public debt financing instead of development charges.27 Our analysis of proposed and under construction housing projects found that removing the cost of infrastructure from the price tag of homes can potentially reduce the per-unit construction costs of new homes in the Greater Toronto Area and Metro Vancouver by an average of 20%.28

Moving to a debt-financing model does not change who pays for housing related municipal infrastructure–renters, homeowners and ratepayers. The conduit for this cost pass-through however changes from developers to municipalities. Because municipalities can borrow at a cheaper rate than developers or homeowners, the interest costs that are passed through are lower.29 Fundamentally, the proposed change addresses a structural housing affordability problem that’s rooted in having renters and homeowners of new construction pay for infrastructure costs upfront, rather than spreading the cost over many decades, through monthly utility fees.

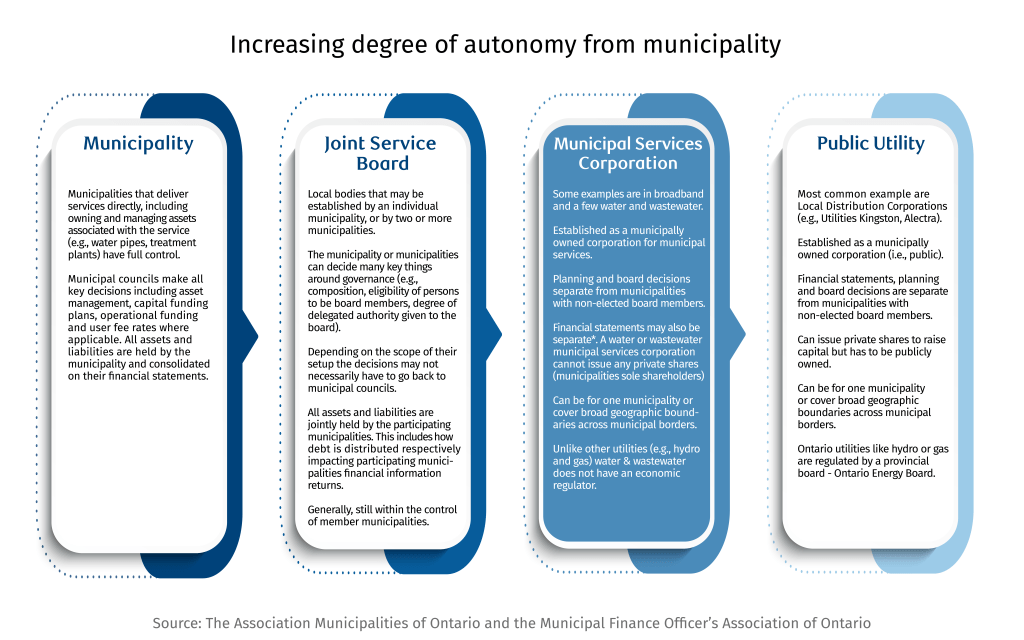

Public-debt financing can occur either as on-book or off-book financing. On-book financing requires municipalities to stay within their annual debt repayment limit, which is generally 25% of own revenue sources.30 Off-book financing provides municipalities greater borrowing flexibility, as annual debt repayment limits are not applicable.31 This form of financing, however, is more administratively complex, as municipalities would need to establish a municipal services corporation (MSC) or a public utility, and scope out the services they want to provide. The most common uses of MSC, or public utilities, are for water/wastewater and local electricity distribution. Both types of corporations operate arms-length from municipalities and take on the public debt used to finance an infrastructure project, in addition to owning and operating the asset.

The strong fiscal position of Canada’s largest municipalities indicates that shifting to a public debt model to finance housing related infrastructure is achievable. Based on regulatory filings32, the 13 largest single-tier and regional governments in Ontario that are also active in the municipal bond market have the fiscal room to take on at least $4 billion in debt, either as loans or bonds, without breaching their annual debt repayment limit. That’s two times greater than the $2 billion they collected in development charges in 2023.33

About 20 Canadian municipalities actively borrow from the public debt market to finance their hard infrastructure projects.34Municipal bond issuances totaled $5.4 billion, in 2024, with $53 billion in outstanding debt.35

Given the mostly AA to AAA credit ratings of Canadian municipalities, the low risk of default, and the attractive risk-return profile, it’s likely that based on the U.S. experience,changes to the federal tax code to exempt the interest earned on municipal bonds will result in greater investor demand.36

While Canada’s municipal bond market is unlikely to grow 75 times, to $4 trillion dollars, which is the size of the U.S. municipal bond market, the $4 trillion figure is proof that tax incentives can be an effective tool in drawing in private capital into desired forms of infrastructure.37

Municipalities have a range of governance options in how to deliver their services, and ownership and management of these services. The most common model that exists in Canada are for municipalities to have full ownership of service delivery. Within the past 30 years, as more responsibilities are shifted onto municipalities from provincial governments, there’s been a slow evolution to explore different and more cost-effective forms of service delivery.

Municipal services corporations (MSC) and public utilities are the two most common alternative forms of service delivery.38 The creation of these arms-length municipally owned corporations provide greater flexibility to plan for and finance the full lifecycle of assets.

In a MSC or public utilities service delivery model, these corporations take on debt to pay for the upfront capital expenditure costs of an infrastructure project. Debts are paid off over several decades through monthly user fees derived from homeowners and businesses using the infrastructure. The continued economic viability of these systems is ensured through mandatory utility connections, typically required by provincial or municipal planning regulations.

Turning ideas into action

We encourage all levels of governments to study and consider the taxation and financing ideas proposed in this policy brief, as they refresh their housing strategies.

Our policy brief does not model the utility rates impacts were municipal governments to adopt a debt financing model for infrastructure. These economic and taxation studies are complex, requiring a deep understanding of capital budget and service delivery models, which is not uniform across Canada. Given the domain expertise required to execute these studies there’s an opportunity for provincial and municipal governments to jointly co-fund these studies to understand the costs and benefits of our proposed ideas.

At the federal level, policy and program design work is likely underway for the government’s affordable housing tax credit proposal, and its commitment to reduce municipal development charges by 50%.39 We encourage the Department of Housing, Infrastructure and Community to consider the ideas put forth, as they move deeper into the policy analysis, program design and consultation stage of their work. Since changes to the Income Tax Act are at the crux of our two ideas, we encourage the Department of Finance to evaluate the cost and benefits of our two tax proposals on the government’s balance sheet.

Conclusion

An estimated $2 trillion will be required over the next five years to build the additional 3.5 million homes required to alleviate the country’s housing affordability crisis.40 A crisis that in the past few years have led to several studies by the federal and provincial governments analyzing the root causes of the country’s housing supply and affordability problem, and recommendations for action.

The taxation ideas proposed above advance some of these recommendations. The Ontario Housing Affordability Task Force recommended the creation of an arms-length municipal services corporations that would build, own and operate housing related infrastructure.41 As well as finance the infrastructure using debt rather than development charges. And the Canada-British Columbia Expert Panel on the Future of Housing Supply and Affordability recommended increasing the supply of below-market rental housing through a long-term funding commitment.42

The urgency to leverage and enlarge the pool of capital available for new housing construction—five times the current level of deployment—is becoming greater, as provinces and the federal government take on unplanned new spending to support businesses and communities impacted by U.S. tariffs. The net effect on both levels of government is less fiscal room to support other priorities, including housing. Restoring housing affordability needs to be a short and long-term strategic priority for all levels of government. Doing so will free up household disposable income that can be re-invested to grow other sectors of the economy. It will be a sustainable outcome that can help safeguard today’s standard of living and economic prosperity for current and future generations of Canadian renters and homeowners.

This figure is based on Scenario 1 in the Canadian Mortgage and Housing Corporation (CMHC) 2023 Canada’s Housing Supply Shortage: Restoring affordability by 2030 study. In this scenario housing affordability is restored to 2003-2004 levels, housing cost to income ratios range from 30% in many smaller provinces to a high of 44% in British Columbia. Scenario 2 would introduce a uniform housing cost-to-income ratio of 40%. In this scenario, an additional 2.27 million units of housing would be required, and only three provinces would be required to increase housing supply beyond current levels. These provinces are Ontario (1.63 million units), B.C. (0.62 million units), and Saskatchewan (0.02 million units).

Legal Disclaimer3

Analysis based on RSM estimates using Freddie Mac data. The base case is 1.3 million units, annually, and an additional 400,000 units arising from new household formation. CMHC’s 3.5 million units are additional units required that are in excess of the existing annual housing completions, which averaged 195,000 between 2000 to 2022. For our analysis we prorated the 3.5 million units over 6 years, starting in 2025, for an annual average of 588,333 units. The population figure for the U.S. is 340 million based on April 2025 data from the Federal Reserve Bank of St. Louis. Canada’s population estimate of 42 million is from Statistics Canada, as of April 2025.

Legal Disclaimer4

This is a weighted value for household incomes and home prices in the Greater Toronto Area and Metro Vancouver. Analysis based on data from the Canadian Real Estate Association, the Toronto Region Real Estate Board and CMHC’s Real Average Household Income (Before-tax) by Tenure report. Home prices are for Metro Vancouver and the Greater Toronto Area (GTA) as of April 2025. The average composite home price for Metro Vancouver was $1,184,500 and $1,107,463 for the GTA, and their weighted value is $1,147,276. The pre-tax household income in Vancouver was $127,500 and$137,400 in Toronto, and their weighted value is $132,635.

Legal Disclaimer5

Latest available data as of June 2024 for the Apartment Construction Loan Program. To achieve the government’s goal of 131,000 units by 2031/32 requires the completion of an estimated 70,000 units by 2024, based on the assumption that an equal numbers of unit are built each year, and the first wave of units were completed in 2020, 3 years after the program was introduced. Data source: Housing, Infrastructure and Communities Canada – Progress on the National Housing Strategy – June 2024.

Legal Disclaimer6

Government fees waived include land transfer tax and the federal portion of the harmonized sales tax. Downpayment support include the RRSP Home Buyers Plan and the Tax-Free Home Savings Account (FHSA). The Home Buyers Plan allows first time homebuyers to withdraw money from their registered retirement savings plan, without a tax penalty, if repayment is made within 15 years. The FHSA allows individuals to contribute to savings account where contributions are tax-deductible and withdrawals for first time home purchases are tax free. There’s a $40,000 limit to the FHSA.

Legal Disclaimer7

The tax credit is aimed at the development of below market rental housing that’s privately owned, and not so-called community or social housing.

Legal Disclaimer8

Analysis of data from the Congressional Budget Office; Cohn Reznick 2024 LIHTC Equity Market Volume Survey.

Between 60 to 70% of bond proceeds are used to fund municipal infrastructure and housing capital projects. Source: LSEG

Legal Disclaimer11

Institutional investors that are pension funds are exempt from paying income tax on their capital gains, in both the U.S. and Canada. Pension funds invest in municipal bonds for two primary reasons: to diversifying their portfolio and obtain a low-risk steady cash flow. Retail investors are so called mom and pop investors.

Legal Disclaimer12

Analysis by Charles Schwab found that the spread between taxable and tax-exempt municipal bonds as of February 2025 was 160 basis, and the 15-year average, since 2010, is 100 basis points. Provincial regulations require municipalities to create a reserve fund that is used to pay off debt issuances. While statistics on municipal debt default is not available in Canada, analysis by Fidelity Investments found a 0.04% default rate for U.S. municipal bonds. In comparison, the default rate for corporate bonds with similar risk profile was 1.44%.

Legal Disclaimer13

These types of facilities are prescribed in section 142 of the tax code.

Legal Disclaimer14

The per capita allocation for private activity bonds is $130, in 2025.

Legal Disclaimer15

Based on 2022 data, which is the latest data available. Source: Novogradac.

Legal Disclaimer16

Latest data available from the U.S. Department of Housing and Urban Development, for homes built between 1987 and 2022.

Legal Disclaimer17

The 4% and 9% represent the amount of eligible costs that can be counted towards the low-income housing tax credits.

Legal Disclaimer18

States generally impose another 15-year holding period on top of the federal requirement, bringing the overall affordability period to 30 years. The new equity investments are typically used to finance capital improvements. Banks in the U.S. are subject to the Community Reinvestment Act (CRA), which requires them to serve the credit needs of the communities in which they do business, including low to moderate income neighborhoods. Investments in LIHTC deals are viewed favourably by banking regulators when evaluating a bank’s CRA performance.

Legal Disclaimer19

RBC Capital Markets. The yield for a 12-month zero coupon US Treasury Bond is 412 bps on May 23, 2025.

Legal Disclaimer20

The LIHTC provides a direct dollar-for-dollar reduction for federal tax liability. The credits provide investors with the flexibility to offset prior year’s federal tax liability. They can also be carried forward for 20 years if tax credit flow exceeds actual federal tax liability.

Legal Disclaimer21

The 5 to 1 ratio referenced in the key takeaway is a weighted average of both tax incentives.

Legal Disclaimer22

See Clayton Research Associates Limited CMHC sponsored study Tax Expenditures – Housing published in March 1981 and CMCH’s Assessment Report Evaluation of Federal Rental Housing Programs, published in 1988. The Clayton study was commissioned by CMHC to evaluate the costs, benefits, and effectiveness of select tax expenditures targeted at housing.

The approach used by municipalities to access the public debt market varies. B.C. and Quebec have provincial financing authorities who borrow from the debt market on behalf municipalities. A similar approach is taken in Ontario where regional governments exist. Regional governments borrow from the public debt market for their own needs and the needs of their constituent municipalities.

Legal Disclaimer25

This funding relationship emerged in the 1990s when the Ontario government devolved responsibility of housing onto municipalities, in exchange for taking on responsibility for education.

Legal Disclaimer26

The amount of bond proceeds used to fund housing varies from year to year. About 5% of outstanding issuances as of April 2025 are used to fund housing according to analysis by FTSE Russell.

Legal Disclaimer27

Development charges, also known as capital cost charges, infrastructure charges or offsite levies are most common and the highest in Ontario and B.C. While development charges exist in other provinces to pay for growth related infrastructure, such as Alberta, they generally are a smaller proportion of total construction costs. Analysis based on data from the following sources: client data, BILD’s Comparison of Government Charges on New Homes in Major Canadian and U.S. Metro Areas, CMHC’s Housing Market Insight, July 2022, and scenario modelling using the City of Calgary’s building and development permit fee calculators.

Legal Disclaimer28

This figure is a weighted average of development charges for single detach and row homes, and low and high-rise multi-unit residential buildings.

Legal Disclaimer29

Developers borrowing costs is typically 100 basis points or one percentage above the prime rate. Residential mortgage rates are generally 200 basis points above the prime rate, exclusive of any promotional discounts. Using the latest prime rate of 4.95%, a developer’s cost of borrowing would be 5.95%, while for a homeowner, it would be 6.95%. Municipal bond borrowing costs range from 2.55% to 4.90%, for bonds issued in 2024.

Legal Disclaimer30

The 25% threshold applies to municipalities in Ontario, BC, and Alberta. The City of Vancouver debt service ratio is limited to 10% of its own revenue sources, i.e., revenues from sources that it has direct control over, such as property taxes, user fees, and development charges.

Legal Disclaimer31

Municipalities in Canada are required to establish a reserve fund for bond issuances. The reserve fund is used to pay interest payments and the principal outstanding. Monies required for the reserve fund comes from municipal operating budgets. The creation of reserve funds and risk-based lending practices is one of the reasons why municipal debt defaults are rare, in both Canada and the U.S.

Legal Disclaimer32

Ontario Municipal Affairs and Housing’s Financial Information Returns.

Legal Disclaimer33

Latest year of available data. Ontario municipalities collected $2.7 billion dollars in development charges in 2023 based on analysis carried out by the Ministry of Municipal Affairs and Housing.

Legal Disclaimer34

RBC capital markets.

Legal Disclaimer35

Ibid.

Legal Disclaimer36

Analysis by RBC Capital Markets found that 90% of municipal bond issuances in the U.S are single rated -A or higher.

Legal Disclaimer37

Analysis of Federal Reserve data by Fidelity found that retail investors account hold 44% of municipal bonds and the balance is held by institutional investors and corporations.

Source: Liberal Party’s Building Canada Strong election platform commitments. Based on costing documents, the Federal government plans to spend $1.5 billion annually, over 4 years, on reducing development charges and supporting infrastructure.

Legal Disclaimer39

Source: Liberal Party’s Building Canada Strong election platform commitments. Based on costing documents, the Federal government plans to spend $1.5 billion annually, over 4 years, on reducing development charges and supporting infrastructure.

Legal Disclaimer39

Source: Liberal Party’s Building Canada Strong election platform commitments. Based on costing documents, the Federal government plans to spend $1.5 billion annually, over 4 years, on reducing development charges and supporting infrastructure.

Legal Disclaimer40

Estimate based on a weighted average construction cost for single-detached, row/townhouse, low and high-rise multi-residential housing where construction is underway in the Greater Toronto Area. The calculation includes hard and soft construction costs, and land development costs, but excludes land purchase price, and fees, such as interest charges and management fees. In our analysis, per unit construction cost ranged from $462,000 to $577,000, and the weighted average development charges was 20%. The estimated development charges outlay is between $323 to $403 billion.

Legal Disclaimer41

Recommendation 44 calls for the Ontario government to “Work with municipalities to develop and implement a municipal services corporation utility model for water and wastewater under which the municipal corporation would borrow and amortize costs among customers instead of using development charges”. Source: Report of the Ontario Housing Affordability Task Force.

Legal Disclaimer42

Recommendation 17 calls for “the federal government make long-term funding commitments, as was done until the mid-1990s, rather than offering short-term capital grants.”

In this week’s edition: Canada-U.S. in two phases, Trump’s three recurring trade narratives, and how businesses are handling the uncertainty

Noteworthy

Ottawa played host this week to some high-profile guests, from a gaggle of U.S. senators to King Charles—plus the first session of Parliament in 161 days.

Five U.S. senators, including one Republican, met with senior government officials to reinforce the Canada-U.S. relationship. A two-phase deal is being considered.

Phase 1: The climbdown of Section 232 (steel, aluminum and auto tariffs on national security grounds) in exchange for an increase in Canada’s defence spending commitment, which explains the ‘Golden Dome’ missile system talk. There’s some optimism that this can be done before or during the G7 Summit—though time is running out as that begins in two weeks.

Phase 2: The broader renegotiation of CUSMA. Expect that to start as early as this summer and conclude just before the review deadline of July 1, 2026.

The economic and security agreement got a shout out in the King’s Speech from the Throne, as did Carney’s trade diversification priorities. The legislative agenda, and the work that will happen during the summer session of the House, will likely be more domestically focused, including fast-tracking projects in the national interest and resolving federal barriers to internal trade. Expect Canada-U.S. negotiations to happen in the background—as was the case with Minister Dominic LeBlanc’s meeting with Secretary Howard Lutnick and USTR’s Jamieson Greer last week.

The week that was

A day after the U.S. Court of International Trade ruled that Trump overstepped by using the International Emergency Economic Powers Act (IEEPA) to impose tariffs, a federal appeals court reinstated them, at least temporarily.

The sluggish labour market in China may get a whole lot worse: Nine million manufacturing jobs in China could be lost due to the trade war.

Clear Seas estimates that by 2040, if all planned projects pan out, there will be a 60% increase in ship traffic on Canada’s Pacific Coast. The main driver: LNG projects.

Japan’s biggest businesses are getting hammered, prompting the government to step up with a US$6.3 billion package to protect its economy.

Trade-related crime is spiking in the U.S. And it’s proving tough for the government to stop.

India is playing hardball with the U.S. on key commodities (rice, wheat, maize) and dairy.

A UN agency predicts that trade-war-induced instability will lead to seven million fewer jobs in 2025 than first predicted. And U.S. consumer demand is connected to another 84 million jobs. Canada and Mexico, with 17.1% of roles tied to the U.S., are the most exposed.

The view from Washington

Washington’s word of the week is TACO—Wall Street shorthand for “Trump Always Chickens Out.” A phrase that underscores growing skepticism regarding the White House’s resolve to maintain tariffs in the face of market pressures and retaliatory actions from trading partners. The reality is more complicated. To justify trade policies, the administration relies on a rotating carousel of narratives:

A negotiating tactic to achieve other foreign-policy objectives. The White House applies this reasoning when implementing fentanyl-related tariffs on Canada and Mexico and frequently uses it as a crutch to justify cancelled or postponed tariffs: mission accomplished, claim victory and move on. Tariffs are short-lived in this line of thinking, and often resolved or scaled back by minor concessions from the target nation.

An industrial policy lever. They’re meant to encourage firms to reshore supply chains and production lines, which aligns with Trump’s promise to restore U.S. manufacturing to its former glory through sector-specific tariffs on autos, steel, and aluminum. Under this reasoning, tariffs are all about pointing to new production plants and other significant investments.

A tool for government revenue generation. Although the hype around Trump’s External Revenue Service has died down (for now), this narrative dominated the first weeks of the administration’s trade policy strategy. When this is the goal, foreign countries have few carrots to offer that would change the President’s mind.

The challenge is discerning which justification Trump is leaning towards on any given day. When asked about TACO this week, the President embraced the negotiation narrative. The narrative may change next week as the administration’s battle in court over IEEPA tariffs continues.

Three questions…

With Andrew Skinner, RBC’s VP of Trade Finance.

Q: How are businesses diversifying—both in terms of sourcing and selling? A: Two key observations: In April, we had a record number of customers and prospective new users of our RBC Global Connect tool, which provides resources such as best countries to buy and sell and other trade intelligence. Secondly, some clients have found better margin opportunities in Europe for products historically shipped to the U.S. And importers are ensuring resiliency of supply by finding new suppliers.

Q: How have things changed in the past couple of months for companies that have maintained their business with U.S. customers? A: Compliance with CUSMA rose to 50% in March from 33% in February. From client discussions, we expect this will be much higher now based on the noted estimate that 94% Canadian exports to U.S. are likely to comply. Clients have maximized U.S. inventory storage and distribution channels to meet short-term demand and minimize tariff impacts. They are also regularly reviewing timing of shipments and location of delivery to navigate U.S. tariffs. Some clients have been able to pass on higher tariff costs where alternative supply is unavailable, and demand persists. Others are pausing transactions to ensure certainty of pricing and demand, especially if they can’t cover tariff costs.

Q: What advice do you have for companies navigating the uncertainty? A: We are encouraging clients to review their key buyer and seller trade cycle—order to payment, contract terms and documentation available—and identify opportunities to renegotiate terms. The aim is to maintain long-term relationships and avoid Back-to-School, Black Friday, and Christmas peak sales cycles disruptions. There are a range of solutions available to minimize payment risk, improve cash flow and enable cost/ return efficiencies as new markets, suppliers and buyers are being considered.

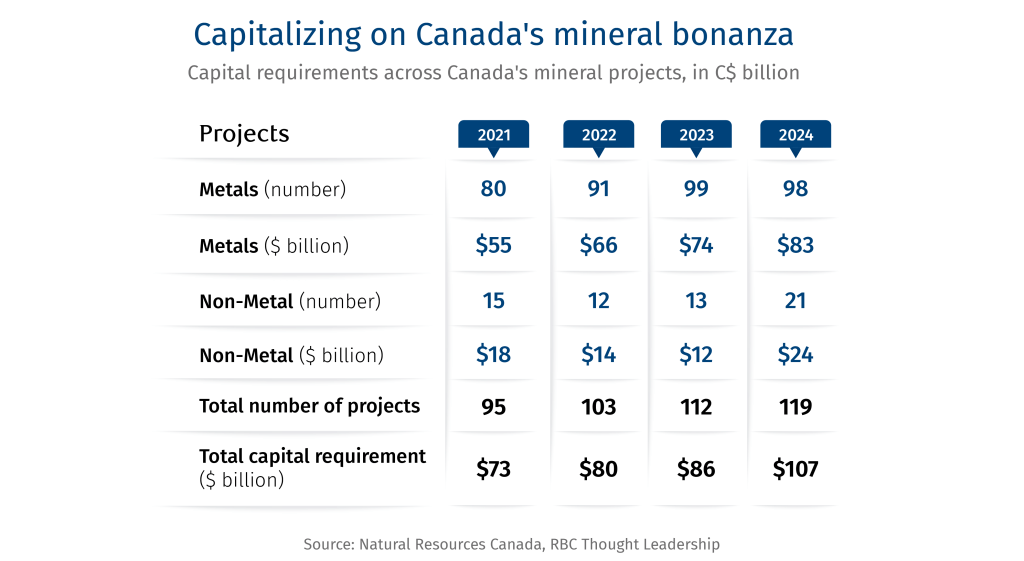

More than 100 mineral projects, valued at $107 billion, are at various stages of development in Canada over the next ten years. Unlocking that potential requires diversified capital flow, both domestic and foreign, for Canada to emerge as a commodity powerhouse.

With Chinese capital constrained by stricter federal rules, American capital is the natural partner to help develop Canada’s mineral resources, given the two countries’ geo-strategic alignment. Still, recent bilateral trade tensions with the U.S., suggest Canada should be clear-eyed entering into new partnerships and diversify capital sources to derisk projects.

If part of a broader security framework, Canada can position itself as a key pillar of the U.S.’s focus on breaking China’s hold on the supply chains of several commodities critical for defence, energy and high-end manufacturing. New cross-border commodity supply chains could serve as the bedrock of a North American high-end manufacturing, defence and energy infrastructure revival.

Building metal and critical mineral projects requires patient, long-term investors who can guarantee either long-term offtake agreements or security of demand to ensure their economic feasibility. To derisk projects, Canada could broaden its capital base beyond the U.S. and tap various global sources of foreign capital that are on the hunt for strategic assets—provided they meet Canada’s national interest and energy security thresholds.

Canada in the Great Resource Game

Canada’s vast natural resources present compelling investment opportunities. Crucially, they’re becoming strategic assets for G7 and other allies in a fragmented world.

Mineral development also gives Canada an opening to service several core verticals—automotive, energy equipment, defence, and high-end manufacturing. With the right strategy, Canada can position itself as a new manufacturing supply chain hub in a geopolitically-charged world, as we wrote in The New Great Game.

But injecting geopolitics into the minerals development space is a double-edged sword.

This was evident in recent years with China, a major supplier of foreign direct investment (FDI) in the global mining sector. Its involvement in Canadian minerals over the past few years have come under strict scrutiny on security concerns—coming to a head in 2022 when Ottawa ordered three Chinese entities to divest from three Canadian mining companies. The move has largely frozen Chinese interest in Canada’s minerals’ sector.

American companies are seen as more natural partners for Canada to develop mineral resources, given the countries’ long-standing geopolitical alignment. Despite the U.S. trying to squeeze Canada on trade, defence and several sectors such as lumber, automotives and steel and aluminum, the synergies on metals and minerals could be strategic for both countries. Recent U.S. rhetoric aside, there is a sense that collaboration on several metals and minerals supply chains would fortify North American energy and national security.

Trump charts a new direction

Washington’s approach to minerals development is still being laid out.

Signals indicate that the U.S. is poised to act decisively on critical minerals1 and other resources it considers vital for defence, technology, and semiconductors. The White House has fast-tracked 10 mining projects, signed an executive order aimed at stepping up deep-sea mining within U.S. and international waters, and floated the prospect of investing directly in mining companies, including through a proposed U.S. sovereign wealth fund.

U.S. President Donald Trump’s hawkish stance on resource-rich Greenland, the recent signing of a minerals deal with Ukraine, and interest in one with the Democratic Republic of Congo, suggests minerals are a strategic asset in the U.S. quest to counter Chinese dominance.

Canadian Prime Minister Mark Carney’s interest in connecting trade talks with U.S. national security, dovetails with American interest in energy and minerals development. As recently as December2, the two countries had invested in a critical mineral project in Yukon, part of a broader bilateral collaboration under the Canada-U.S. Joint Action Plan on Critical Minerals Collaboration and the Canada-U.S. Energy Transformation Task Force.

The U.S. and Canadian governments have already injected billions in capital into the space. Between 2021-2024, the U.S. government funded at least 24 critical minerals and materials projects, including five in Canada jointly with the Canadian government. Ottawa has also funded at least another five projects as of early 2024.

While Canada is keen to partner with its American counterparts on mineral development, it has taken measures in recent months to place some guardrails over its assets in a world that’s become more transactional and unpredictable. In March 20253, the Innovation, Science and Industry Ministry, responsible for Canada’s investment review, expanded the criteria for national security review to include economic security, in a move seen directed at the U.S. And in April 2025, the Government of Ontario introduced new measures “to prevent foreign governments or corporations from claiming Ontario’s critical minerals.”4

Securing geo-strategic capital

To further derisk its resource base, Canada should tap into a wide variety of capital that’s on the hunt for strategic assets.

The Canadian mining sector is already a major capital magnet. There are currently more than 100 mineral and mining major projects underway in Canada at various stages of development (announced, in review, approved or under construction) valued at more than $107 billion in capital, according to the Natural Resources Canada’s major projects database. And the list has ballooned in recent years as interest in Canadian resources has grown. But where will the capital come from?

As miners gear up for future development, they could tap four sources of capital: self-financing, global equity markets, foreign state-owned entities, and sovereign wealth funds (SWF)— each aligned to different investment horizons and risk appetites.

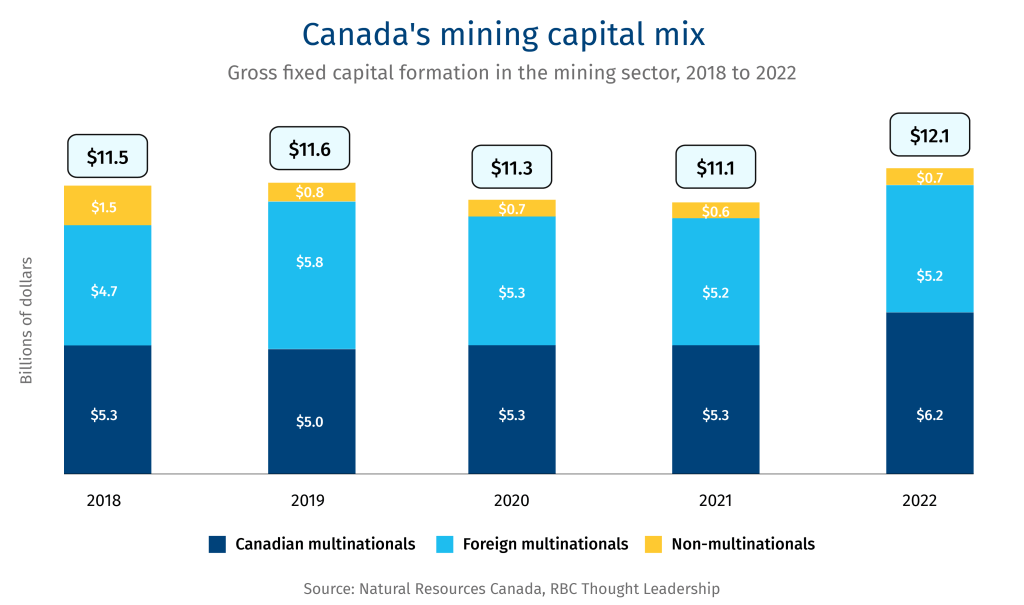

Foreign capital is already a well-established feature of Canadian mining, making up around 40-45% of investments flowing into the sector over the past few years.

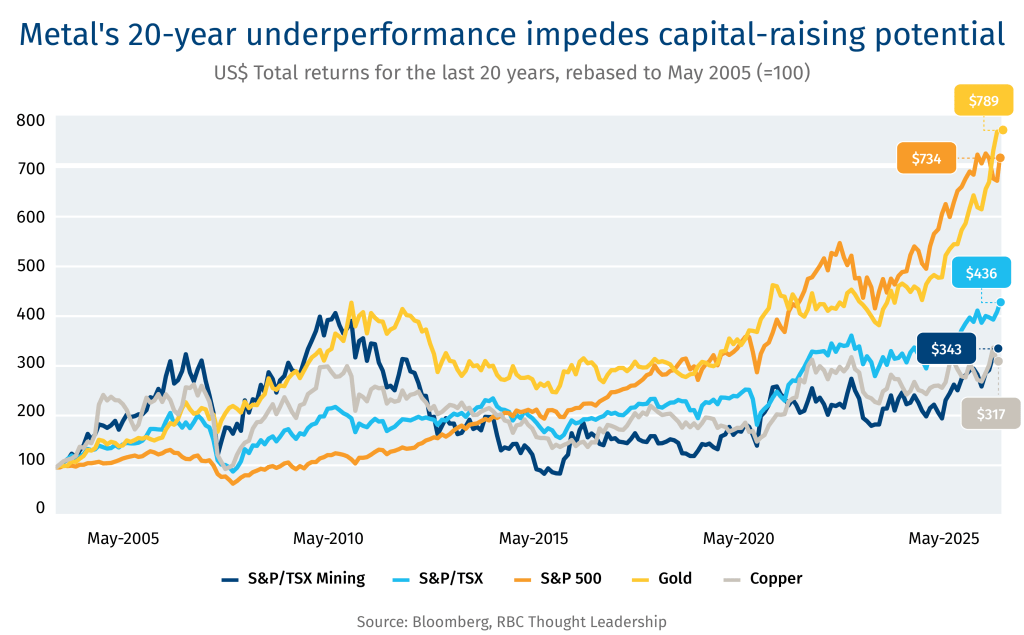

Self-financing: Over the past two decades, capital raising for the minerals sector has been challenged as mining and mineral companies have lagged both the underlying commodity and the broader index. Across equities specifically, this underperformance is even greater on a risk-adjusted basis given the lower volatility in returns for both the S&P/TSX Composite and the S&P 500.

This has emerged as a key financing challenge for companies. Yet a new commodity super cycle, driven by geopolitical and energy transition dynamics, could drive renewed investor interest in the sector. Despite the market underperformance, Canadian miners are generally in good shape to partially fund projects. The sector enjoys financial strength and discipline as evident from its 0.7x capex-to-cash-flow over the past 12 months (compared to 1x in the past 10 years), indicating that funds are available to invest, while the debt burden has also fallen considerably in recent years5.

All told, the S&P/TSX metals and mining firms have accumulated as much $14 billion in excess cash flow over the past 12 months, ready to be deployed globally6. While Canada could attract a portion of that, companies will still need to tap into a variety of other capital sources to finance projects.

Equity markets: Public equity markets remain a viable capital source. New corporate equity issuance is also an attractive option from institutional and Western capital, majority of which is composed of passive or long-only funds. While investor risk appetite has been lukewarm, new macroeconomic and geopolitical drivers, coupled with strong company balance sheets could shift investor sentiment.

State and SWFs: Sustaining some of these projects with long gestation periods require geopolitical actors that take a long-term view on strategic resources. They are already on the hunt: between 2022-2024, we estimate that about 20% of global mining M&A originated from sovereign wealth funds (SWFs). The share of state-linked transactions was almost certainly higher, since the majority of China’s 18% share of global deals would have been done through its state-linked corporates.

State capitalism extends beyond sovereign wealth funds, and could include corporations that are linked to or championed by governments.

Among such state-owned entities, not all actors would be classified as high geopolitical risk like those from China, in terms of threatening market control or transferring minerals’ intellectual property (IP). Clean energy infrastructure funds linked to public pensions funds, sovereign wealth funds or large private equity firms are also eyeing opportunities in mining. Canada’s well-capitalized pension funds could also play a role here.

Other deep-pocketed investors—such as Middle Eastern sovereign wealth funds and state-owned entities—could be more active in the future. While an important source of capital, they could pose security challenges, ranging from shifting geopolitical alliances or bilateral diplomatic spats, such as Canada’s diplomatic fight with Riyadh in 2018 over Saudi Arabia human rights record.

Containing China

The issues around security of strategic assets cannot be underestimated, and will only gain more traction, as evident with Washington and Beijing locking horns over supply chains. As President Trump embarks on signing trade deals with several countries, he may pressure those nations to purge Chinese capital from their mining supply chains.

That wouldn’t be entirely without precedent. Concerns over Chinese capital compelled the prior U.S. administration of Joe Biden to enhance its internal review of new Chinese investments in critical minerals and other strategic sectors7. In the past, Washington has also raised concerns more broadly about new Chinese investment in its allies, putting pressure on close trading partners Canada and Mexico to fortify their review processes.

Bolstering the Investment Canada Act That has already triggered a shift in how Canada has handled Chinese investments in recent years. In 2022, the Investment Canada Act (ICA) national security provisions were enforced to require the divestiture of Chinese investment in three Canadian critical minerals companies with lithium mining activities. In doing so, the critical minerals sector was flagged for enhanced government scrutiny8.

Further amendments over the past year give the federal government enhanced scope to complete a national security review for any new foreign investment in Canada, not just those with controlling interests, and greater scrutiny of investments by state-owned entities (SOE), which primarily targets China.

Amendments also asserted quasi-extraterritorial powers of the ICA – that the foreign assets of Canadian businesses were within scope of ICA review in case of foreign SOE acquisition.

Canada’s expanded reach Combined with the fact that Canada has major mining concentration—the Toronto Stock Exchange and the TSX Venture Exchange represent 40% of the world’s public mining companies and are home to more than a 1,000 listings—, the ICA’s quasi-territorial means it’s a powerful tool for policing some Chinese investments abroad. Canada has recently asserted this authority, with two Canadian companies attempting to re-domicile to avoid the ICA review.

In the case of a more significant break with China, President Trump may seek a broader Chinese investment purge by Canada as the cost of participating in U.S.-centric supply chains. For one, it could push Canada to test its powers under the ICA. It could also take issue with some legacy investments by Chinese state-owned companies in large Canadian miners (see Managing legacy Chinese investments).

However, a provoked China could retaliate against Canada by closing its markets to certain exports, similar to its tariffs on Canadian canola in March, or by further weaponizing its supply chain.

Even as China’s capital or long-term supply agreements may no longer be welcome in the Canadian mining sector, it remains a major supplier of industrial equipment and parts. Western governments could replace Chinese equipment over time, but it is sand in the gears of further developing resources. Trump’s recent backtracking on Chinese tariffs at the behest of American corporations points to the importance of Chinese materials in the global economy.

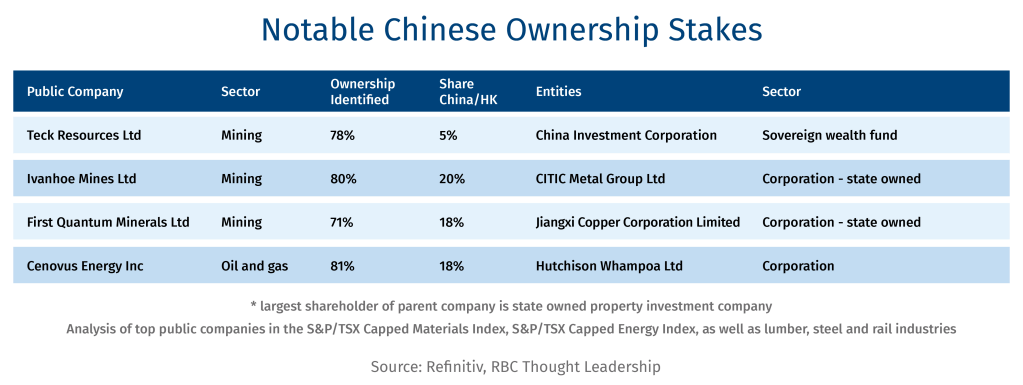

Managing legacy Chinese investments

Analyzing the largest public Canadian mining companies reveals three with material Chinese ownership from state-owned entities. No major U.S. mining companies have similarly significant or state-sponsored Chinese interests.

Given that these are legacy investments, the Canadian government lacks the legal authority to compel their divestiture, notwithstanding the shifting national security lens.

In the U.S., President Trump’s recent political pressure may have compelled the planned sale of Hong Kong-based Hutchison Whampoa’s stake in Panama Canal and other ports to an American-led consortium (currently paused while under review by China). Ergo, other tools may be within the Canadian government’s control to achieve its aims, but they could come at the cost of provoking China and damage to Canada’s reputation as an investor-friendly jurisdiction.

Canada’s investment opportunity

The world’s looking at Canada as a stable and dependable commodity player to help diversify its commodity supply. It’s also a generational opportunity for the provinces and the federal government to unlock resource developments that are rich in gold (vital as a safe haven commodity), copper, iron and critical minerals. The right strategy, investments and security measures can help power Canadian mining.

Contributors: Cynthia Leach, Assistant Chief Economist, RBC Economics Shaz Merwat, Energy Lead, RBC Thought Leadership Vivan Sorab, Senior Manager, RBC Thought Leadership Yadullah Hussain, Managing Editor, RBC Thought Leadership

[5] The sector’s capex-to-cash flow of 0.7x over the past 12 months and debt-to-cash flow ratio of 1.1x are both well below their 10-year averages of 1.0x and 2.1x, respectively.

[6] Float-cap weighted average trailing twelve month operating cash flow less capital expenditures less dividends less buybacks across the S&P/TSX Metals and Mining Index (GICS Level 3)

In this week’s Edition: On the ground in Canada’s “Pinnacles of Progressiveness,” How Trump’s ‘big, beautiful bill’ could impact Canada, and what major projects might be on the government’s fast-track list

Noteworthy

By John Stackhouse

This past week, I was in Quebec and B.C. — Canada’s “Pinnacles of Progressiveness” — to gauge how the conversation is shifting around resource development, particularly oil and gas exports. Here are a few of my takeaways:

In Quebec, which has generally opposed fossil fuel pipelines and LNG, Premier Francois Legault is expressing more and more support for a national East-West pipeline.

A senior Quebec official told me that more public pronouncements in favour of gas may come in the weeks ahead.

B.C. is about to become a global LNG player, which is why Premier David Eby is headed to Japan and Malaysia in the first week of June.

I spent time with the province’s Energy and Climate Solutions Minister Adrian Dix who says B.C. will continue to expand its electricity to power more LNG plants.

The LNG industry believes as many as six more LNG plants could be built, which would meet about 20% of the world’s projected growth in demand.

But the clock is ticking. I keep hearing people say that Canada has about an18-month window to get these major projects going.

Week in numbers

1

Number of times the word ‘trade’ was mentioned in the joint statement made by the G7 finance and central bank chiefs following three days of meetings in Banff, Alberta this past week. There wasn’t a single mention of ‘tariffs’ in the statement.

400

Companies in the S&P 500 that mentioned ‘tariffs’ in Q1 earnings calls.

$1.5 billion

What Foxconn, Apple’s long-time supplier, is spending to build a production facility in southern India. Apple continues to shift production from China to India, which prompted Trump to end the week with a 25% tariff threat on iPhones not made in the U.S.

$3,500

One estimate on what an iPhone would cost consumers if it was made in the U.S. Another analyst landed on US$1,500, up about 25% from the current retail price.

View from Washington

Trump’s “One, Big Beautiful” Bill includes several policies affecting cross-border industries and supply chains that grew out of Canada-US trade talks under Biden.

LOSER: North American electric vehicles. Four years ago, Canada and Mexico successfully lobbied for an expansion of the Inflation Reduction Act’s EV tax credit to include North American products. The bill would end the US$7,500 credit (US$4,000 for used EVs), eliminating a major consumer incentive for a cross-border industry already grappling with tariff-related price increases. And the resulting consumer demand slowdown bodes poorly for Canadian EV supply chain projects.

WINNER: Continental defence spending. Canada has expressed interest in joining Trump’s “Golden Dome” missile defence program, which gets a US$25-billion injection if this bill passes. Canada could integrate the acquisition of U.S. defence products into a broader Canada-U.S. trade agreement. Trump is a proponent of using defence sales to rebalance U.S. trade relations and said this week that Canada will pay its “fair share” if it joins.

UNCLEAR: Canadian critical minerals. Critical minerals were a focal point of Canada-U.S. trade relations for several years; the countries even signed a Joint Action Plan on mineral supply chains in the final days of Trump 1.0. House Republicans have allocated an additional US$2.5 billion for critical minerals production. It’s too early to tell what impact that will have on Canadian critical minerals projects, which qualify for Pentagon funding through Title III of the Defense Production Act.

Major project list: What’s on the fast-track?

The upcoming discussions around a renewed economic and security agreement, and the broader imperative to diversify trade, cannot be advanced without expediting and realizing resource, energy and infrastructure projects.

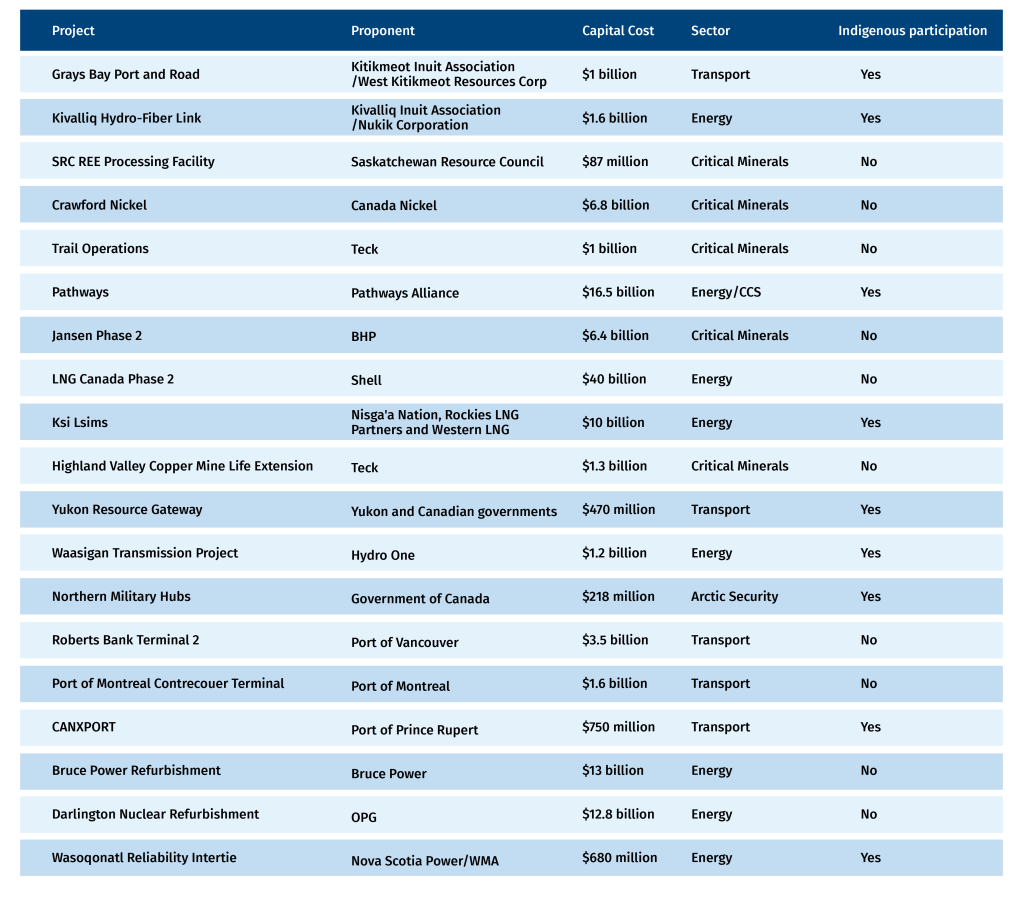

A big part of June’s First Ministers meeting in Saskatoon will be identifying nation-building projects the federal government has promised to fast-track in collaboration with provinces and Indigenous Nations. Besides regional and political considerations, a project list must cut across multiple sectors, contribute to important strategic objectives (including energy and Arctic security), and build Canada’s economic strength.

The 19 projects below help meet many of those objectives. They represent more than $120 billion in capital costs, covering major transportation, critical minerals, oil and gas, nuclear, carbon capture, utilization and storage (CCUS) and Arctic security infrastructure. They span the regulatory lifecycle-from pre-feasibility to under construction. Most if not all will require Indigenous partnerships. And they bolster Canada’s clean and conventional energy, trade diversification and Arctic security capabilities.

This is the 50th anniversary year of the G7, and when its leaders meet in Alberta next month, many will wonder if the group has another 50 years in it.

Their finance ministers may have the same questions this week when they meet in Banff, asking if the champions of democratic capitalism can overcome a tariff war, threats of stagflation and growing concerns about the U.S. debt.

The fate of democratic capitalism may hang in the balance.

I spent part of last week in Ottawa, with a group called the B7, made up of business leaders from across the seven leading democratic economies, and didn’t come away feeling enthusiastic about the West’s great project. Since 1975, when the world was struggling with oil shocks and monetary crises, the G7 has helped maintain economic and financial stability. Most of the heavy lifting was done by the U.S., with assists from Germany and Japan, but the coordination of economic and monetary policy across the broader group was essential, too.

Now that’s fading. You just need to look at Donald Trump’s visit to the Persian Gulf last week to see how much capital’s centre of gravity has shifted. China and Latin America are laying claims, too.

And if trade follows geopolitics, we can expect more disruption to come.

So what can the G7 do? Perhaps develop new ways to generate, attract and reinvest capital.

For too many years, the public and private balance sheets of the leading democracies have focused on short-term objectives. Meanwhile, the non-democratic world has amassed capital for decades-long projects.

With their economies struggling and debts growing, G7 countries now face a $15-trillion infrastructure gap, to rebuild supply chains, expand production of critical minerals, develop capacity for AI-powered economies, and decarbonize energy systems.

Canada can help shift the alliance’s thinking to those longer-term needs. That won’t be easy given political tensions between the Trump administration and most of the G7 allies. But with U.S. engagement, the G7 can create new approaches for democratic capitalism, including:

coordinated investments across countries.

more institutional capital for priority projects.

preferential approaches to procurement.

joint approaches to procurement, especially of energy, advanced technologies and critical minerals.

shared standards, measurements and principles.

You can read the B7 group’s final communique here.

Seesawing trade relationships between the U.S. and China have brought critical minerals to the forefront. In fact, Rare Earth Elements (REEs), the 17 elements with physical and chemical properties that make them key inputs to some of the world’s most critical technologies, were China’s latest weapon in its trade arsenal against the U.S.

Following recent trade talks with the U.S., China expressed a willingness to walk back the REE export restrictions it announced in April. However, the threat re-emphasized the West’s collective dependence on China. In September 2020, the first Trump administration signed an executive order warning of the country’s critical dependence on China for REEs and called for increased domestic production. Even if the U.S.’s attempts at re-shoring supply are successful, its production will be a fraction of China’s, making international collaboration, including with Canada, a critical requirement.

Seven numbers tell the current state—and Canada’s potential role.

67%

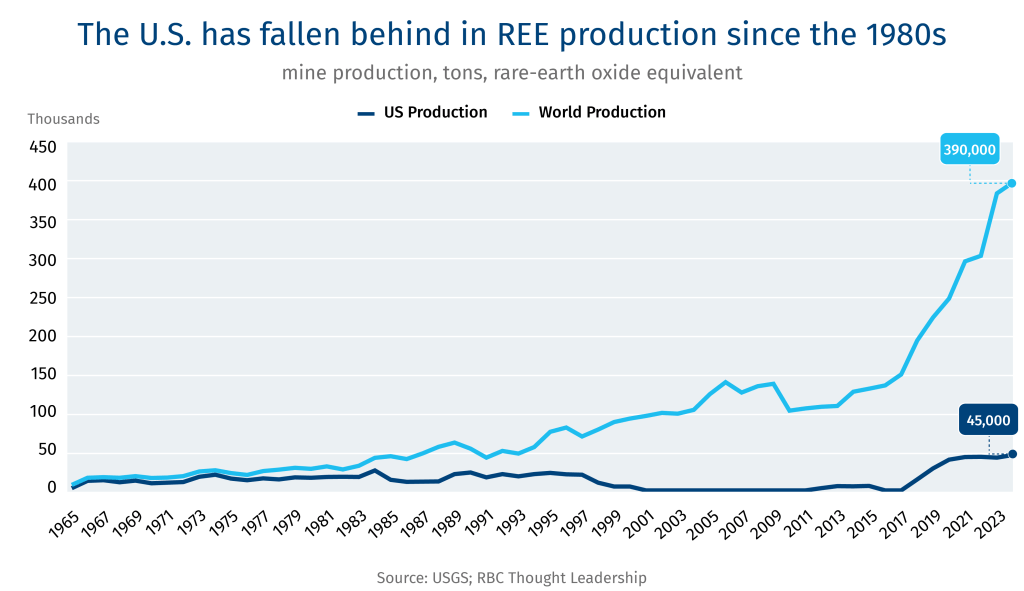

Share of global REE mine production that comes from China. While the U.S. produces 11% of the global total, the second highest, it exports nearly all its production for further processing. The U.S. was once the world’s leading REE producer but has been losing share since the 1980s, with China dominating global production since. Canada has produced REEs in the past, but currently does not have any domestic mining operations.

99%

Share of Chinese control over Heavy REE separation and processing. Heavy Rare Earths, such as terbium, enable REE magnets to work in higher temperature applications without losing performance. China also controls 90% of Light REEs, including neodymium, which are also key inputs to magnets. Countries like Estonia and Canada have or are developing LREE and HREE separation and processing capabilities.

92%

Share of Chinese control of global REE magnet manufacturing. While REEs are used in various forms (e.g., as powders for polishing optical equipment, and as catalysts in petroleum refining), they are also used to make the world’s most powerful permanent magnets. These magnets are used in high-performance technology including military aircraft, submarines, and electronics and are difficult to substitute.

16

The number of U.S.-entities to which REE exports were banned by China in April, as trade tensions between the two nations escalated. Fifteen of these entities were linked to the manufacturing of defense technologies.

US$439 Million

How much the U.S. Department of Defense has spent since 2020 to strengthen its domestic REE supply chain.

$22 Million

What the U.S. has invested in Canadian REE processing companies since 2023. Canada is considered a “domestic source” of critical minerals under the U.S. Defense Production Act (DPA), so Canadian companies are eligible to receive investments under DPA Title III.

12

REE projects in Canada currently active in the exploration, resource estimation, or preliminary economic assessment phases. There are also three separation and processing facilities and two REE recycling plants. To capitalize on the opportunity, a few things could speed things along. 1/ Government investment: Provincial funding in Saskatchewan, for example, has helped bring REE processing facilities closer to commerciality. Government support could also help fast-track projects. 2/ Secure offtake for REE products: As discussed in The New Great Game, decades of focused industrial policy and technology development have left Western manufacturers competing with lower-cost products while being bound to tighter environmental standards. Guaranteed offtake at competitive prices could help Canada’s REE industry get a foothold.

Vivan Sorabis Senior Manager, Clean Technology, at the RBC Climate Action Institute

In this week’s edition: Carney picks his main trade and security team; trade signals from Trump’s Middle East tour; and what to expect during U.S.-China negotiations

Noteworthy

By John Stackhouse

I was in Ottawa this week for something called the B7—a gathering of business leaders from the constituent countries of the G7, whose governments will be meeting in Alberta in a few weeks.

The most divisive issue: trade.

The mood was largely bearish. Despite the May bull run on markets, there’s a sense the democratic—i.e. free-trading—world is growing more divided. “Trade follows geopolitics” was how one speaker put it.

Europe is turning more inward, with a focus on its own economic security. Get ready for more industrial policy and state investing, which won’t help trade.

Canada is at a crossroads, needing to ease up on U.S. trade and expand trade with other markets, even as other markets get tougher to deal with.

A new age of “plurilateralism” is emerging, in which constant and continuous dealmaking is the norm.

Some U.S. speakers urged Canadians to look beyond Trump’s attacks, saying the country is going through a bit of a mood adjustment.

But for now, at least, the U.S. is looking to show some Elbows Up, American-style.

Incoming ambassador Pete Hoekstra will give his first big briefing to POTUS next week and will highlight “outrageous” Canadian actions like removing American liquor brands and banning procurement from U.S. firms.

Expect some media donnybrooks between Hoekstra, a blunt-talking former Congressman from Michigan, and Ontario’s blunt-talking Premier Doug Ford.

New Industry Minister Melanie Joly may have to round out the line, as the three work to save the U.S.-Canada auto sector from further damage.

One suggestion: they meet at the Gordie Howe Bridge, in tribute to the OG of Elbows.

How things are shaping up on the all–important Canada-U.S. file

Carney has been clear that he’s the boss—and will run point on Canada’s relationship with the U.S. Still, his team will play a major role in a new economic and security agreement.

The Core 5: In selecting a main negotiating unit of Dominic LeBlanc, Anita Anand, David McGuinty, Francois Philippe-Champagne and Gary Anandasangaree, Carney opted for veteran ministers who collectively hold substantial clout and relationships in the Beltway. Expect this group to be supplemented by Melanie Joly, Minister of Industry, who holds considerable experience on the file, and will lead domestic negotiations with critical industries, including steel, aluminum and autos. And, in a lower-profile way, by Lisa Jorgenson, Carney’s recently appointed Senior Advisor on Canada-U.S. Jorgenson brings experience from Public Safety and Justice and will provide advice and behind-the-scenes coordination across political and bureaucratic levels.

Committee shakeup: Trudeau’s Canada-U.S. Committee is out. And the ‘Secure and Sovereign Canada’ Committee is in. Chaired by McGuinty and Anand, the new committee has a couple noteworthy inclusions. Maninder Sidhu, Minister of International Trade, who is tasked with diversifying Canada’s trade away from the U.S., a key Carney promise. And Rebecca Chartrand, Minister of Northern and Arctic Affairs, a nod to the importance of Arctic security, one of the three legs of the economic and security pact.

Diplomatic and bureaucratic shuffle: The tenures of a few high-profile ambassadors—Kirsten Hillman in Washington, Ralph Goodale in London, and Stéphane Dion in Paris—are expected to end soon. Carney will likely prioritize a mix of experience, relationships, and political muscle, especially in filling the role in DC, as Hillman, well respected in Ottawa and Washington, leaves big shoes to fill. As for the public sector, Carney’s right hands in the Privy Council Office are Clerk JohnHannaford and Deputy Clerk Chris Fox, who both hold a depth of experience on national security, energy and trade files. A broader public service shuffle could be in the offing as the PM looks for near-term results.

The week in numbers

7

Lawsuits filed against Trump and his administration challenging the ’emergency’ used to levy tariffs under the International Economic Emergency Powers Act. The U.S. Court of International Trade held a first hearing earlier this week.

150

Number of countries that Trump says want to negotiate a deal. Without the time to meet with them all, his administration will send letters to a list of leaders in the next couple of weeks simply telling them “what they’ll be paying to do business in the United States.”

1,000

Products marked as being impacted by tariffs at Loblaw. The grocery chain expects that number to climb to 6,000 in two months. Meanwhile, Walmart, which saw profits decline in Q1, announced it will be raising prices in the U.S. because of tariffs.

60 million

iPhones that Apple plans to produce from India for the U.S. market. While on his Middle East tour, Donald Trump blasted Apple’s CEO (“I had a little problem with Tim Cook”) for building iPhones in India despite committing US$500-billion in the U.S.

The view from Washington

Details of Donald Trump’s Middle East tour offer a glimpse into how ongoing and future trade talks, including with Canada, could play out:

Spend big on U.S. Defense products: Saudi Arabia ($142 billion) and Qatar ($3 billion) signed defense sales and procurement deals that range from general upgrades to information systems to new air and missile defense capabilities. The Trump administration might push the purchase of U.S. defense products in its future trade deals, which is particularly relevant for Canada given the White House’s record of criticizing Canadian defense spending. Trump could use the U.S.-Canada deal to push Canada to get to 2% defense spending more quickly through deals with U.S. defense firms.

Don’t ignore Big Tech: Trump announced a $20-billion investment by a Saudi firm in AI data centers and related energy infrastructure in the U.S. And Qatar pledged $1 billion for a joint quantum technology venture between American Quantinuum and Qatari Al Rabban Capital. Data centres are particularly interesting in the U.S-Canada context because of Canada’s potential to be a strong partner (available land, renewable energy capabilities, cooler temperatures).

Creating sector-specific funds: The U.S.-Saudi Arabia deal included the creation of investment funds for energy ($5 billion), aerospace and defense ($5 billion), and sports ($4 billion). Investments in areas of shared interest could arise in other negotiations. The U.S.-Canada deal could include shared funds for energy, border security or continental defense.