Field Notes: How Canadian businesses are navigating trade tensions

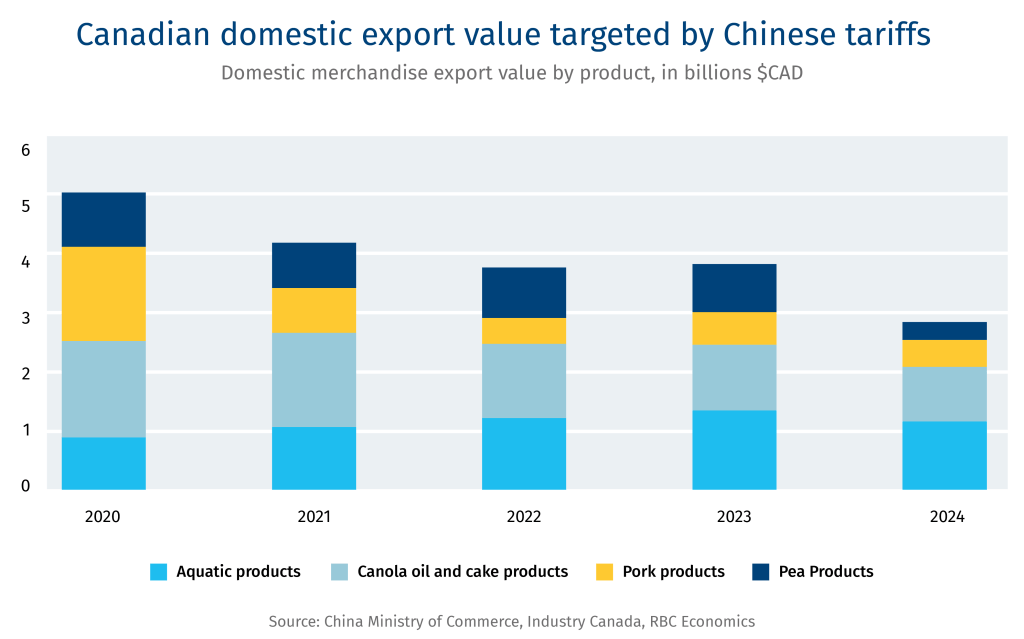

China’s 100% tariff on canola oil and meal has Canadian farmers concerned. That stress level could climb, as China also has its eye on Canadian canola seeds—the largest segment of our canola exports to China—, which have been spared for now. “That would be the other big shoe to drop,” said Rick White, CEO of the Canadian Canola Growers Association (CCGA), which represents approximately 40,000 farmers across Canada.

Canola was developed by Canadian scientists in the 1960s—hence the name. It’s considered healthy oil as it’s low in saturates (an unhealthy fat) and high in monounsaturates (considered good). Canada is the world’s largest canola producer and counts, with 40,000 farmers generating $43.7 billion, with the U.S., China and Japan—in that order, its three biggest export markets. Australia is among Canada’s biggest canola rivals.

As the Chinese tariffs hit Canadian canola farmers, they are freezing investments and need support. White shared some ideas on ways to soften the blow:

Canola is a popular China target

-

White says the tariffs were not a surprise, as past disputes with China (2019-2020) had targeted canola.

-

China has once again targeted the agriculture sector in direct response to Ottawa implementing tariffs on Chinese EVs, aluminum and steel.

-

The industry feels the Canadian government “absolutely bears the responsibility” of that action and should compensate farmers for the financial losses that they will incur.

-

Other major canola seed exporting countries include Australia, Ukraine, Russia. Canada specifically grows canola, which is defined as having low erucid acid and low glucosinolates. Australia and the EU are also significant growers of canola or double low rapeseed, which is of comparable quality.

Canola seeds in the crosshairs

-

A looming Chinese anti-dumping investigation on Canadian canola seed could trigger more tariffs. That’s “the big shoe to drop.”

-

Canola seed is Canada’s primary canola export to China, with canola oil and meal accounting for a smaller portion. In 2024, China imported six million metric tonnes of Canadian canola seed, worth $4 billion.

-

The Chinese are following World Trade Organization (WTO) rules around anti-dumping. WTO challenges take time but provide legal recourse. The CCGA has registered as a party to China’s investigation.

Farmers are looking to freeze investments

-

Farmers rotate crops for agronomic reasons, but canola is a Canadian staple crop, which limits alternatives. Agronomics involves soil and crop management and helps optimize distribution, management and productivity of land.

-

Farmers are already expressing concerns about market risks from China and the U.S. with some suggesting delays in capital investments and equipment purchases due to uncertainty.

-

Plus, purchase of new equipment could possibly come from the U.S. that could be subject to countervailing duty by Canada.

-

“Farmers are not going to take that risk of investing big pieces of capital into renewing infrastructure … there’s going to be a big chill on investment, at least this year.”

Across the border, more trouble is brewing

-

The U.S. is Canada’s largest canola export destination, valued at $7.7 billion in 2023. The U.S. has not yet imposed a 25% tariff on canola, as CUSMA (the Canada-U.S.-Mexico Agreement) remains in effect. But once exemptions expire, new U.S. tariffs could further harm Canadian canola exports.

There are ways to build a tariff-less ecosystem

-

Last December, the CCGA sent a letter to the federal government, forecasting farm gate losses of between $1.76 billion to $4.33 billion for 2025-26 due to the Chinese tariffs.

-

Ottawa has announced new loan products to sustain the industry, but farmers argue they cannot borrow their way through this crisis and need cash compensation.

-

“The federal government needs to compensate farmers commensurate with the losses that they will incur because of China… farmers can’t, nor should they, be expected to borrow their way—they need to be compensated.”

-

The CCGA is advocating for the development of a domestic biofuels and sustainable aviation market.

-

It could be a new domestic market for at least 2-3 million tonnes of canola seed. It would help soften the blow for canola farmers, as the risk and uncertainty around U.S. and Chinese markets is going to remain for a long time. It is an opportunity to help diversify and reduce Canada’s heavy dependence on China and the U.S. markets.