Bottom Line:

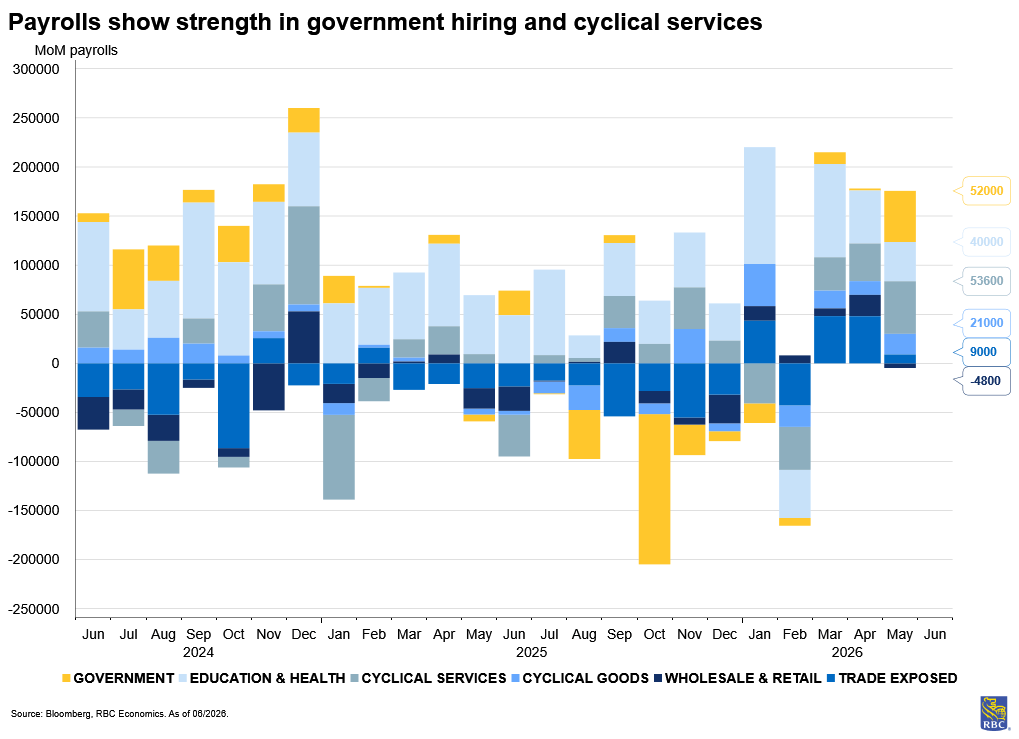

We’ve said many times that it’s hard to bet against the US economy and the May employment report confirms the labor market is strong, despite headwinds. The May payroll report came in with a sizeable upside at +172K, and a major revision to April data (to +179K from +115K). The bulk of job gains in May were concentrated in leisure and hospitality, health care, and local government hiring. The unemployment rate held steady at 4.3%.

While there appears to be some broadening of job gains and cyclical momentum, leisure and hospitality likely saw a temporary boost from the upcoming World Cup. Still, excluding leisure and hospitality, the US labor market added just over 100K jobs which is exceptionally strong in the context of a low breakeven employment rate.

Still, underlying trends persisted this month – AI investment continued to support nonresidential construction and durable goods manufacturing through the buildout of data centers. And the weakness was concentrated in white collar hiring: the insurance sector has shed jobs -45k jobs so far this year and the information sector remains in a multi-year hiring glut.

Labor traditionally has been viewed as a lagging indicator, but there are lots of clues about the economy in these numbers. Looking ahead, we do expect some of the momentum to slow: the World Cup ends in July and the AI buildout is slowing. And a new wave of tariff announcements likely means trade exposed sectors will start to shed jobs again, similar to the trend seen at the end of 2025. Nonetheless, we expect structural support will hold the unemployment rate steady for the remainder of this year and shift the Fed’s focus to the persistent inflationary pressures.

Here are the three themes that stood out in this morning’s labor market report:

1) Cyclically exposed sectors added back jobs after contracting in 2025 – but it’s too soon to say whether this will become a broader trend

-

Throughout 2025, strong payroll prints came with a caveat: nearly all gains were concentrated in health care. This has not been the case in 2026.

-

Cyclical goods (+99K) and cyclical services (+170K) have together added +269K jobs this year. Still, this only recoups about a two-thirds of what these sectors shed in 2025, but it’s a welcome shift.

-

In May, cyclical services hiring was entirely driven by leisure and hospitality (+70K). Outside of this, professional and business services employment registered positive while some white-collar sectors (notably insurance and information) declined.

-

Within leisure and hospitality, food services and drinking places accounted for the majority (80%) of hiring in May. This could be a story of one-off hiring ahead of major World Cup events in the US.

-

In April, revised data shows gains were more broad-based, with transportation and warehousing adding back jobs alongside retail. But these gains may be transitory, as the overturn of IEEPA boosts activity in the short term, but looming tariff announcements could reverse that trend.

2) Rising input costs do pose layoff risks, but so far, the risks are contained

-

We wrote before that the energy shock isn’t likely to trigger a US recession in 2026. We estimated that it would take nearly 1 million job losses to trigger the Sahm Rule, and if May data is any indication, we are not heading down that path.

-

We know that firms facing higher input costs may either pass off those costs to consumers or cut costs through layoffs. So far, recent PPI data suggests that firms are opting to do the former, as jobless claims remain exceptionally low.

-

If pricing power is limited, however, cracks could form in the labor market as collateral damage. We anticipate the Fed will be mindful of this when assessing their next move, which is why we anticipate that they will remain on the sidelines for the remainder of the year.

3) Hours typically fall before headcounts do – and we did not see this in May

-

We watch hours worked for the early signs of declining labor demand, and currently, we are not seeing any evidence that this is taking place.

-

Average weekly hours worked held entirely steady in May, across both goods and services sectors.

-

Aggregate hours worked rose in leisure and hospitality, but average hours worked declined, suggesting more workers are working fewer hours on average (which suggests more hiring of part-time workers).

-

Over the last three months, we have witnessed declines in average hours worked across mostly white-collar sectors that are less directly exposed to an energy shock: notably and consistently in information and insurance.

Beneath the Surface:

-

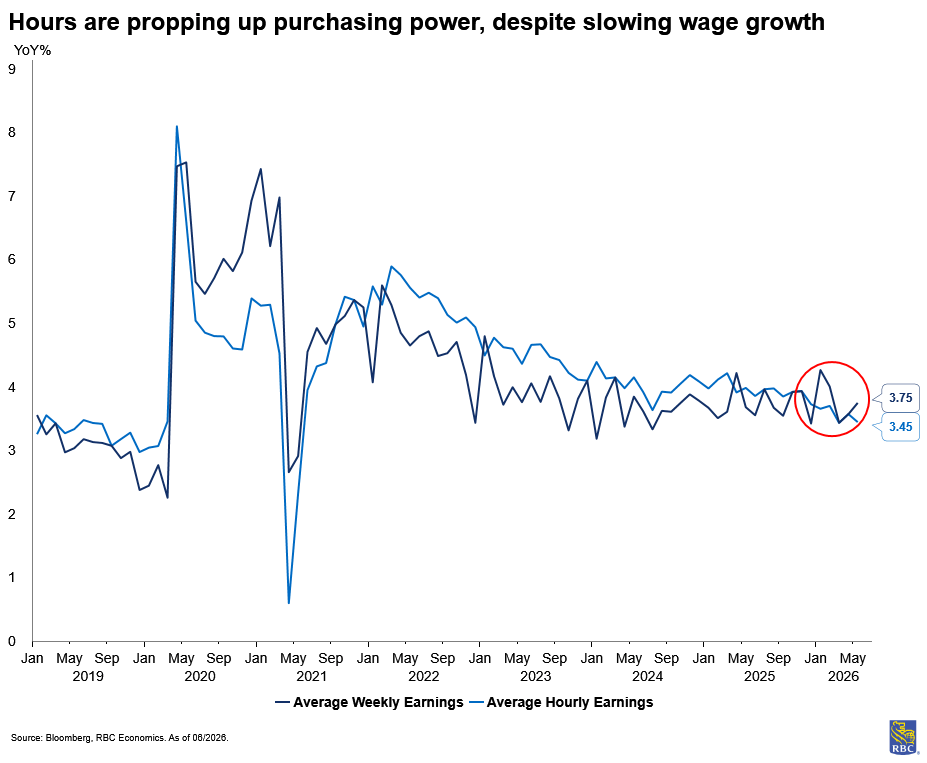

On a monthly basis, average hourly earnings rose +0.3% m/ in May, in line with expectations, but the y/y pace slowed to 3.4%. However, importantly, average weekly earnings in private sectors were up 3.7% year-over-year. This means purchasing power is supported by more hours despite wage growth not keeping up with inflation.

-

The labor force participation rate held entirely steady at 61.8% in May and roughly 28% of unemployed workers are considered long-term unemployed, up from 25% in April.

About the Authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s U.S. economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. She is responsible for generating RBC’s US economic forecasts across GDP, employment, and inflation, and providing macro commentary through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.