Our new US Monthly Executive Briefing separates signals from noise—addressing what’s changed each month, but within a semi to annual context.

There’s a growing list of “never before seen” shocks hitting the US economy— and, yet the unemployment rate sits at an extraordinarily low 4.3%, and GDP growth is running just slightly below 2%—far from a boom, but a long way from a recession.

It’s still “stagflation-lite” in many ways—an anomalous term we’ve used to describe growth running slightly below comfort, and inflation slightly above it.

But even with all this, the US is still likely to produce the strongest growth in the G7 in 2026. On the surface, it seems capable of absorbing all types of disruptions.

However, hiding behind topline growth are three powerful crosscurrents within a larger structural shift.

First, is a reminder 2026 started with the economy set to receive a significant tailwind from a major fiscal spend—the One Big Beautiful Bill Act. It cut taxes and produced consumer windfalls that we, and many others, expected to support the consumer and growth during the year.

Unfortunately, that windfall is likely to be offset by the second crosscurrent: The energy shock from the conflict in the Middle East.

Our view, covered in depth, has been that higher energy prices will nudge headline inflation above 3% this year, but more importantly, they will eat up tax refunds, particularly for lower-income consumers. Bulls can argue there was an existing buffer to absorb the energy shock. Bears may argue it cancels out an important tailwind. Ultimately, both are right.

Third, repercussions from 2025’s trade war are holding even more of our attention even though geopolitical headlines dominate 2026.

Inflationary pressure from tariffs is showing up more consistently now in pricing activity as producer prices climb, and trade-exposed core goods pressures start to follow.

In the post pandemic era, we’ve become used to the notion of corporate pricing power, and consumers “paying up” for higher prices. However, unlike 2022-2023 when stimulus checks and excess savings meant consumers could pay more, real wages are running below -1% year-over-year and the savings rate is falling. Stay tuned.

These three cyclical crosscurrents fit within a much larger structural theme in our the 2026 outlook. As GDP chugs along between 1-2% throughout the year, it comes with a curious development of virtually no job creation in the past year, inciting increasingly popular descriptors like “no hire no fire” or “jobless growth.”

The former is a bit of a misnomer given there’s been plenty of job creation in health care, but also plenty of job destruction in trade-related sectors.

The “jobless growth” descriptor might also be missing the mark on another count, particularly when it paints the economy with a negative slant. A US economy that is not reliant on job creation to accelerate is, in our view, a blessing in disguise. Instead of hiring, America is squeezing more growth out of each worker, which is just another way of saying the economy is growing on the back of productivity.

Thank goodness, because America is increasingly short workers—a theme we’ve explored in depth. If the economy needed labor to accelerate right now, it would either generate a further uptick in inflation as wages rise in competition for a thinning labor supply. Or, it faces a very hard ceiling on how fast the economy could grow.

Indeed, productivity is now the name of the game in the US (and many other major economies). It is the main driver of growth, and more critical to the US outlook than it has been for decades. We’ll likely write more on the topic in the coming months (years), but it’s worth highlighting a few quick points:

-

Productivity is hard to measure and forecast, and prone to significant revisions. Without passing the buck, expect growth forecasts to have wider margins of confidence in a productivity-led growth economy versus a job-led one. For more on the complexities of productivity calculations, see our in-depth primer.

-

We aren’t yet convinced we’re seeing AI-generated productivity growth. Instead, our current take is that businesses are extracting more out of the labor force from existing workers and tools, and there has been some composition shift in the US towards more productive sectors. The silver lining is the AI-driven productivity surge is still likely ahead of us. Read more about that view.

Growth outlook

Growth is still slightly below comfort levels, but a long way from a recession as stronger productivity, robust high-income consumers, and sizeable government spending keeps a floor under growth. Higher tax returns in Q2 (the greatest tailwind) will be offset by higher gasoline prices for consumers (the largest headwind). That said, US growth is still likely to surpass all developed markets in 2026.

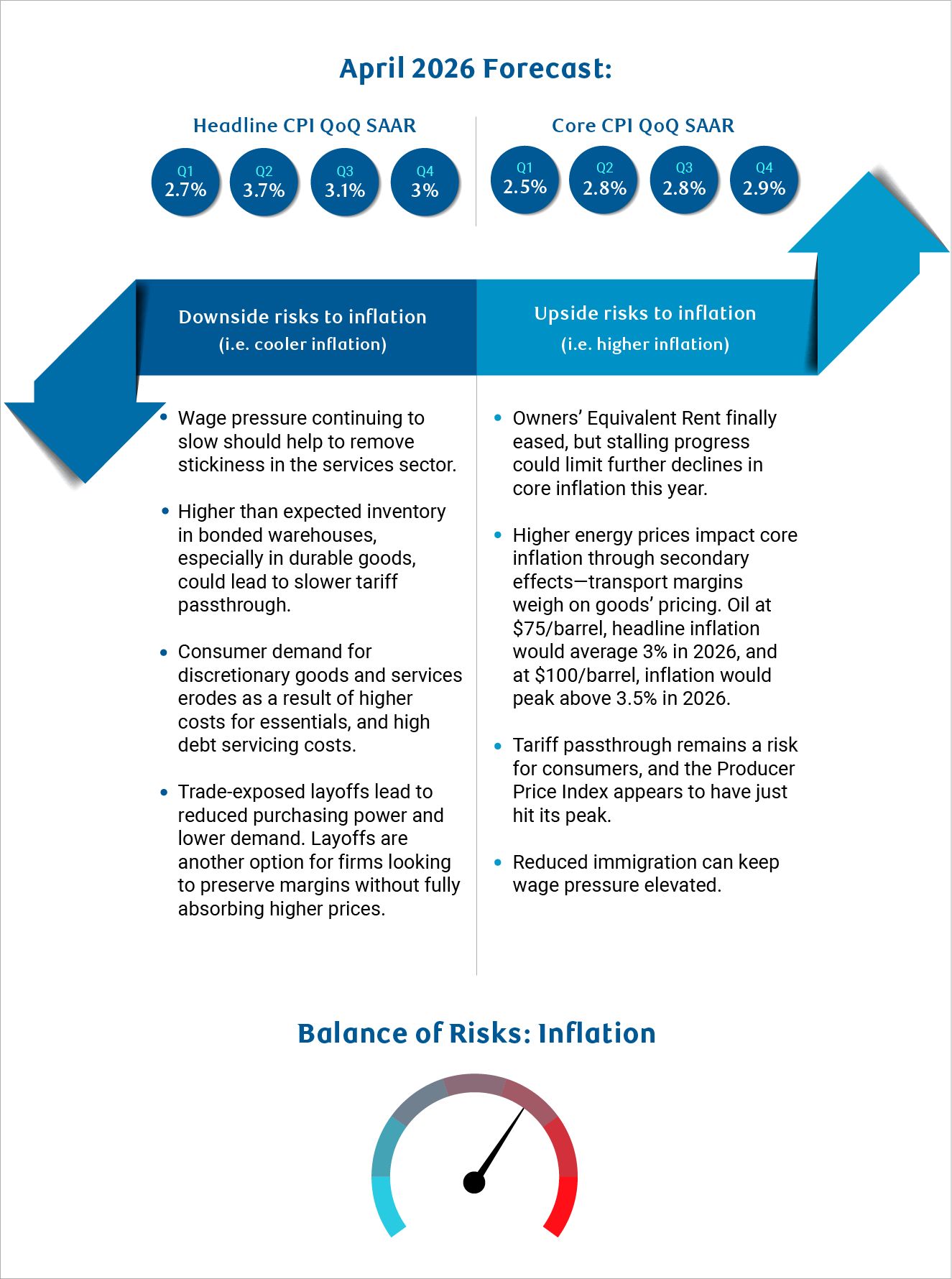

Inflation outlook

Inflation may no longer be a catastrophic problem like 2022, but it remains fundamentally sticky around 3% with upside risks. The energy shock will, of course, bolster prices, but challenges extend beyond oil and fertilizer. For one, now that inventories have been run down, tariffs are showing up more prominently in producer and consumer prices. Meanwhile, services’ prices are also sticky, supported by a structurally tight labor market. That inflation profile (coupled with a tight labor market) will keep the US Federal Reserve on the sidelines for 2026.

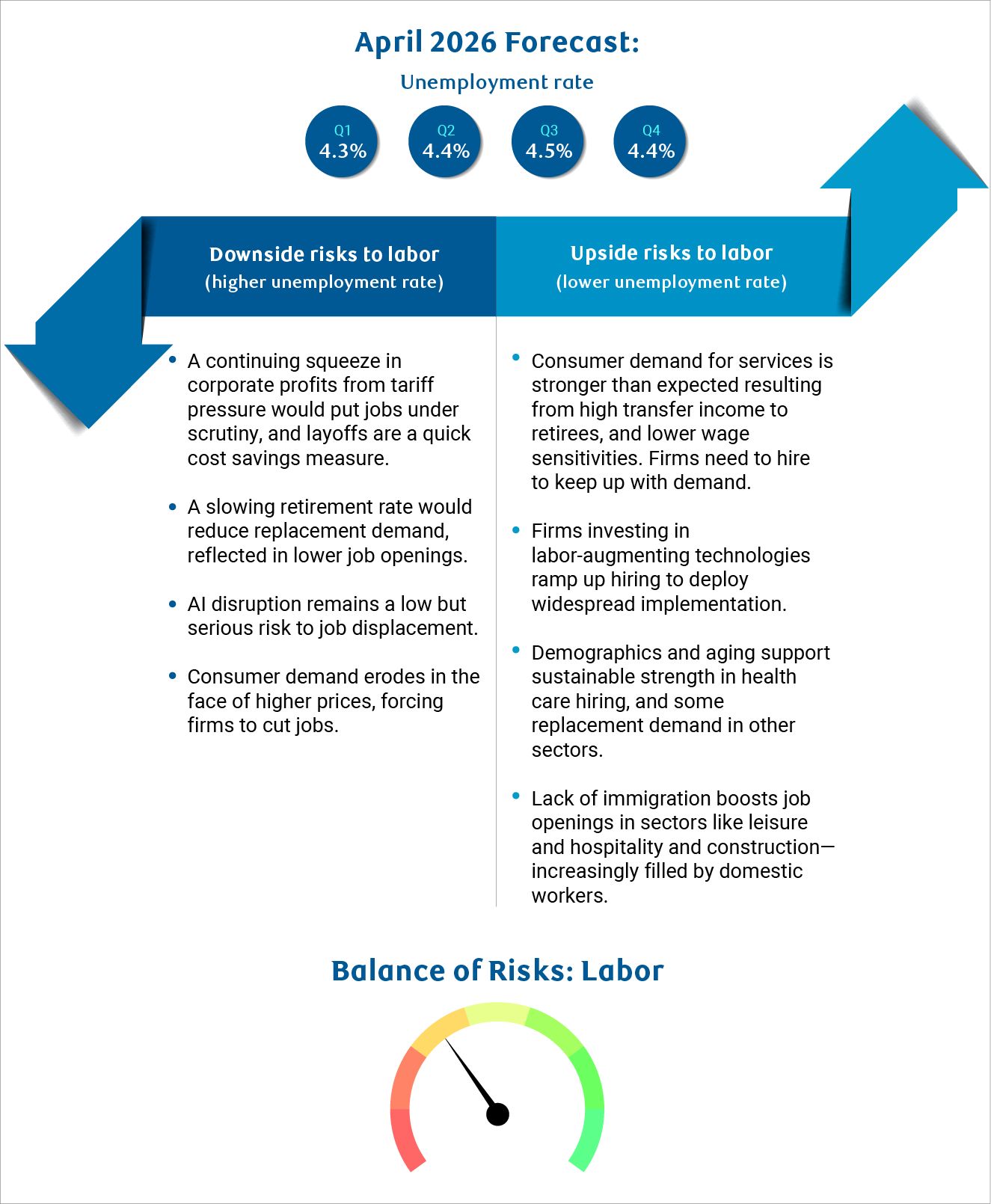

Labor market outlook

The US labor market is treading water in a low-hire, low-fire environment. Job creation has slowed meaningfully and is likely to remain low. However, falling labor supply amid rising retirements mean the economy can generate far fewer jobs to keep the unemployment rate stable—perhaps as few as zero a month. Meanwhile, the composition of hiring has aggressively shifted towards health care, a structural trend, while trade-exposed sectors continue to shed jobs. These trends are likely to continue. Structurally reduced labor supply should mean there’s a floor under how weak wages can decelerate, keeping real wages slightly positive for households. Indeed, the new measure of the American consumer is no longer whether they have jobs, but if they earn enough from them.

Download the report

About the Authors:

Frances Donald is the Chief Economist at RBC and oversees a team of leading professionals, who deliver economic analyses and insights to inform RBC clients around the globe. Frances is a key expert on economic issues and is highly sought after by clients, government leaders, policy makers, and media in the US and Canada.

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. Carrie is responsible for projecting key US indicators including GDP, employment, consumer spending and inflation for the US. She also contributes to commentary surrounding the US economic backdrop which she delivers to clients through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.