Also in this edition: Untangling North America’s biofuel supply chain

Beyond the Barrel

The Strait of Hormuz has long been treated as an oil story. When it closes, energy markets move, tanker rates spike, and the headlines follow crude. But it remains a slow-moving shock to the cost of moving goods, which becomes more entrenched over time.

First-Order: Crude and Tankers

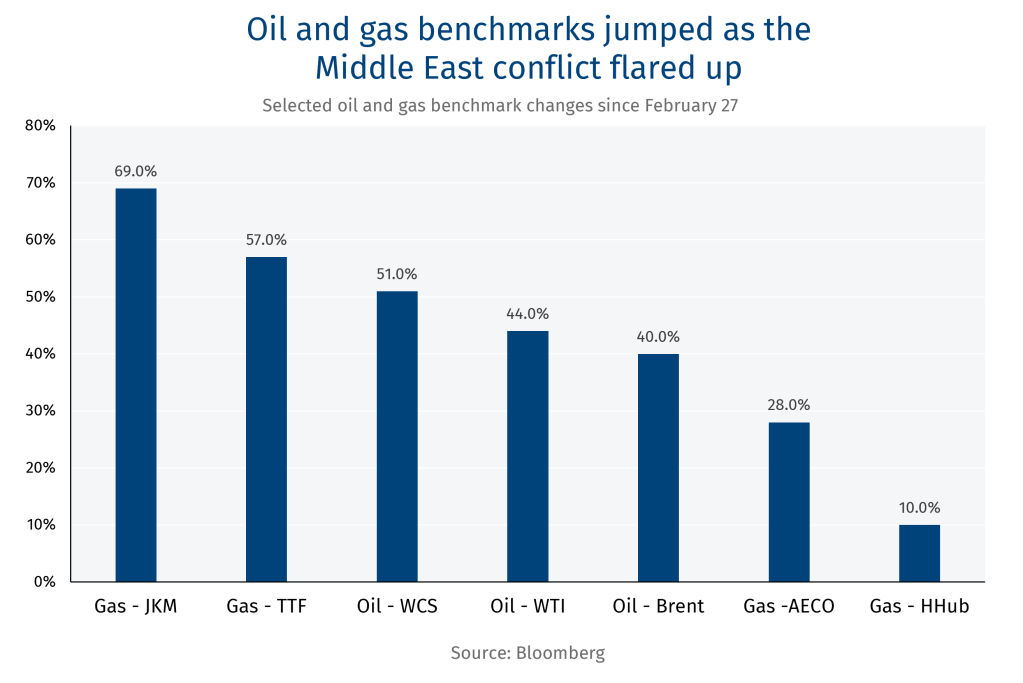

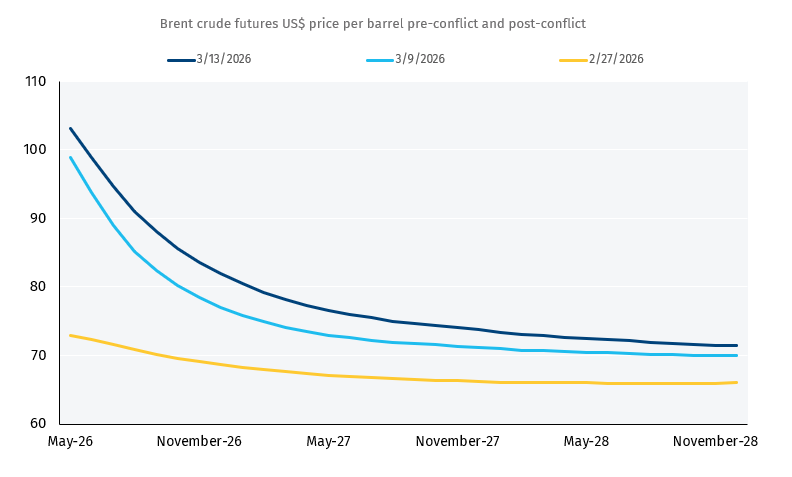

The most direct impact is exactly where markets expected it. Benchmark Very Large Crude Carrier (VLCC) spot rates have surged six-fold since early January and are currently priced at US$98/t (US$13-14/bbl). Tanker volumes through Hormuz (and Suez) have essentially collapsed, with more than 500 vessels stranded in the Persian Gulf.

Second-Order: Products and Fuel

Refinery outages and export constraints tied to Hormuz have fractured global bunker supply chains, forcing vessels to seek fuel at alternative ports at elevated war-zone premiums. Charted below is the Singapore marine fuel indexed price, up 66% since the crisis began. Not charted but equally telling is the spread between Freight on Board (FOB) and delivered prices, typically <5% but well over 50% in mid-March, reflecting genuine physical dislocation in how marine fuel reaches vessels.

Maersk, a Danish shipping company, formalized this disruption on March 25 with a global Emergency Bunker Surcharge, entrenching a products shock into shipping economics worldwide.

Third-Order: Container and Dry Bulk

The Shanghai Containerized Freight Index (SCFI) fell gradually ahead of the conflict and has since rebounded (see chart), but the moves are likely seasonal. Chinese New Year brought port throughput to 40-50% of normal capacity in mid-February. How much of the SCFI March recovery is supply related in contrast to stronger demand is likely unclear until official port data is reported at month end.

Still, dry bulk was structurally underexposed to Hormuz to begin with–only around 55 dry-bulk vessels were transiting the strait weekly before the conflict and the Baltic Dry index is largely flat, if not marginally down. Nonetheless, large container vessel average speeds have edged marginally lower (see chart) since late February, a modest signal consistent with routine rerouting at the edges of the conflict zone.

–Shaz Merwat, Energy Policy Lead

Untangling North America’s biofuel supply chain

North America’s once integrated biofuel supply chain is splintering along national lines.

U.S. federal incentives, state-level programs, and Canada’s Clean Fuel Regulations (CFR) are increasingly pulling in different directions, leading to a fragmented market with implications for Canadian biofuel producers and farmers growing oilseeds and grain including canola, soybeans, and corn.

Policy shifts triggered a continental divide

Changes to U.S. policy under the Renewable Fuel Standard (RFS) and new production tax credits have led the shift. Proposed 2026–27 RFS rules significantly increase domestic biomass-based diesel blending targets, reinforcing demand for oil-based feedstocks like soybean oil.

-

At the same time, newer incentive structures—particularly the transition from blender credits to production-based credits—are explicitly favouring domestic fuel production in the U.S.

-

The change eliminates the US$1 per gallon incentive Canadian biodiesels and renewable diesel received in the U.S. market as biofuels must be produced in the U.S. to earn the production-based credits. The result: an approximate 13% decline in value of Canadian imports into the U.S. between 2024 and 2025, according to Canada’s trade portal. It’s a meaningful departure from the bump Canadian biofuels received from U.S. subsidies.

What’s the impact on Canadian oilseed and grain markets?

Biofuel is a policy driven market and regulatory certainty is not a guarantee. Incentives for biofuel feedstocks under U.S. policy are still evolving as the U.S. Environmental Protection Agency (EPA) establishes its Renewable Volume Obligations (RVOs) for 2026 and 2027.

The pending U.S. policy uncertainty for Canadian farmers is that the EPA has proposed reducing the number of Renewable Identification Numbers (RINs) generated for imported renewable fuel and renewable fuel produced from foreign feedstocks, which would financially discourage U.S. biofuel refineries to use Canadian feedstocks. However, rising domestic Canadian demand could partially offset the export risk.

Canola: It’s the most exposed. Canola oil exported to the U.S. is primarily used for renewable diesel production. Exports of canola oil volume to the U.S. fell by 26% between 2024 and 2025, after climbing in each of the previous five years. The drop occurred while the Canadian canola industry spent more than a year in regulatory limbo, waiting for the U.S. Department of the Treasury and the Internal Revenue Service to clarify how production credits would work, confirming the inclusion of North American feedstocks in January this year.

Soybeans: Canadian soybean farmers may benefit from supportive U.S. policy. According to the U.S. Department of Agriculture’s 2026 outlook, biofuel mandates and tax incentives are expected to drive a 17% increase in U.S. soybean oil use for biofuels. Rising demand for soybeans is supporting prices, yet the commodity still faces potential downsides on trade with the U.S. if the EPA’s proposed RVOs are confirmed.

Corn: It remains anchored in U.S. ethanol production under the RFS. Yet, Canadian ethanol producers are now disadvantaged under the Clean Fuel Production Credit (45Z) that’s designed to encourage U.S. production of finished biofuel via incentives.

Bottom line

The Canadian outlook is mixed with domestic market demand hinging on the federal government’s forthcoming CFR amendments, where policy levers to shore up domestic demand are being considered, including minimum domestic content and credit multipliers for local producers.

–Lisa Ashton, Agriculture Policy Lead

The week that was

Canadian beef producers raise concerns over potential Mercosur free trade deal

-

As Ottawa looks to secure a free trade agreement with the South American bloc this year, the Canadian Cattle Association (CCA) expressed concerns.

-

Brazil is the world’s largest beef producer, and the CCA worries that a Mercosur free trade deal would flood the Canadian market with cheap beef, harm the industry’s efforts to recover amid the tightest cattle supply in 40 years, and risk accusations from the U.S. of Canada enabling a “back door” into North American markets.

Fertilizer costs are leaping just as planting season gets underway

-

Disruption to shipments of fertilizers and commodities essential to fertilizer production through the Strait of Hormuz has increased prices, while North American farmers prepare to embark on their spring planting season. Urea, for example, has seen a ~40% price increase since the conflict began. The surge is quickly becoming a political issue for Trump who met this week with American farming groups, an influential political lobby.

-

Meanwhile, Russia, whose shipments remain unaffected by the Hormuz blockade, has deep reserves of fertilizers and commodities. Earlier this week, Russia halted its exports of ammonium nitrate, to shore up its domestic supply. But the conflict potentially raises the specter of Russia looking to increase its leverage on having restrictions on Russian fertilizer exports to Europe eased.

European parliament approves trade deal with U.S.

-

EU lawmakers had previously delayed approving the Turnberry agreement over U.S. President Donald Trump’s threats to annex Greenland, but on Tuesday the European parliament cleared the way for its implementation—with additional conditions attached. Prior to the vote, the U.S. threatened that the EU would lose favourable access to LNG shipments from the U.S. if the deal was further delayed, as Europe feels the bite of disrupted LNG shipments from Qatar.

-

The deal would eliminate EU tariffs on American industrial goods and some agricultural products and reduce U.S. tariffs on most EU goods to 15%. However, MEPs attached safeguards, such as delaying the EU’s tariff eliminations until the U.S. reduces its levies. These safeguards must be approved by EU member states, with negotiations commencing April 13th.

–Thomas Ashcroft, Geo-Politics Lead