Also in this edition: Canada’s trade with non-U.S. markets is hitting all-time highs and the U.S. looks to create a critical minerals trading bloc to rival China

Ottawa’s Big Wheel Deal

The Liberal government’s much-anticipated auto-sector strategy reinstates electric vehicle incentives, eliminates EV sales mandates, invests in expanding the EV charging network, and offers incentives and tax breaks for global auto makers to build in the country.

It’s all in response to U.S. tariffs, and the looming threat that President Donald Trump might tear up CUSMA in the coming months.

Of course, Prime Minister Mark Carney is hoping to preserve CUSMA and build on its North American supply chain advantages to a new set of investors. But even if Canada’s access to the U.S. market is no longer unfettered, Ottawa can point to several reasons why European and Asian countries may want to set up their auto shop in Canada:

-

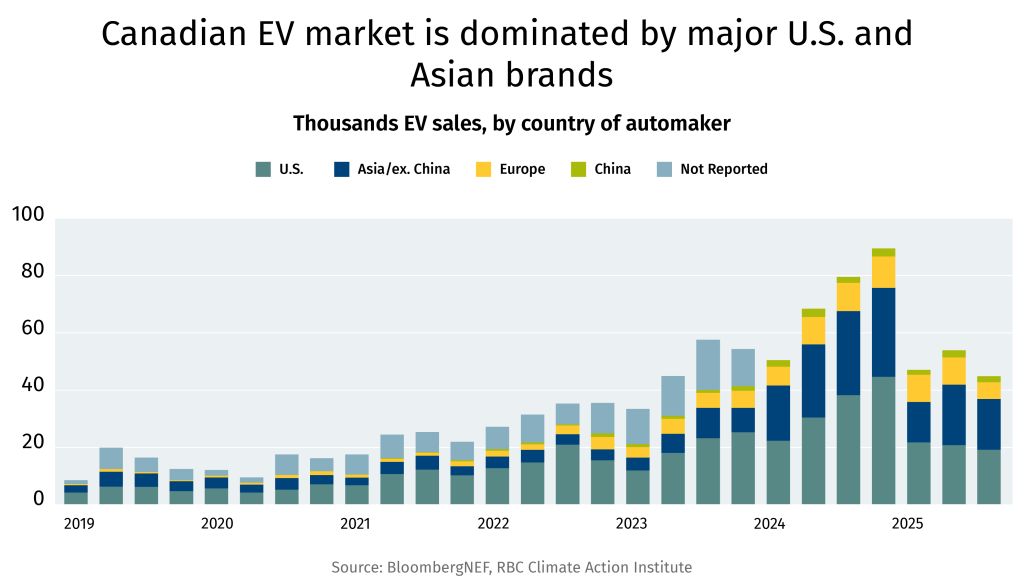

Canadians buy a lot of pricey cars and SUVs: Canada is the world’s 9th-largest auto market, with ~1.9 million vehicles sold annually—skewed toward higher-value SUVs and trucks, with a robust servicing and after-market (courtesy of our harsh winters). OEMs also now compete for high-margin customers, not volume. Canadians buy a lot of cars, including a lot of expensive (read: high margin) cars.

-

Asian carmakers want a North American hub: With 7.2 million global sales in 2024, the combined Korean power of Hyundai-Kia edged out GM and Stellantis for the third spot in the global rankings. However, the companies’ manufacturing footprint and market share remains Asia-heavy, creating an incentive to rebalance toward North America. Canada could become a second North American production zone, hedging geopolitical, climate, and labour risks.

-

Canada is critical to global supply chains: Our store of critical minerals (nickel, cobalt, lithium, graphite), batteries, parts ecosystem, and reliable, clean power offer supply chain integrity at low cost. Just ask Volkswagen.

-

The Ontario-Quebec corridor is an auto-tech Silicon Valley: Canada’s strengths in AI, autonomy, and software—the frontier of future value creation for the auto industry—further enhances the offering.

-

Canada is a free-trade haven: It stands to reason that Canada will secure some form of market access to the U.S. that makes an auto trade possible. We shouldn’t forget the 14 other free trade agreements we’ve signed that cover 50+ countries, 1.5 billion consumers, and 60% of global GDP.

— Jordan Brennan

Look What’s Trending

According to RBC Economist Claire Fan:

“Despite the deteriorating trade balance, Canadian exporters continue to show signs of partial diversification into non-U.S. markets. Goods exports to non-U.S. destinations were 29% above year-ago levels in November, while goods imports from non-U.S. markets rose 18%—both near or at all-time highs.”

Trade Posts

U.S. looks to create a critical minerals trading bloc rivalling China

-

At a Washington summit, attended by representatives from more than 50 nations, the U.S. outlined a vision for a rare earths trade zone, using tariffs to create a price floor for minerals and drawing on the respective strengths of partner countries across the value chain, to counter Chinese dominance.

-

Several bilateral deals were struck, including U.S. “Action Plans” with Mexico, the EU and Japan, to develop coordinated trade policies.

-

Foreign Minister Anita Anand said more details were needed before agreeing to such a framework, which would play a role and potentially give Canada some leverage in upcoming CUSMA negotiations.

Trump and Modi broker trade truce

-

Washington committed to cutting tariffs on Indian goods from 50% to 18%, in return for New Delhi stopping its purchases of Russian oil.

-

While details on the timing of the tariff changes and other trade barrier reductions remain vague, the amelioration of some of Trump’s most punitive tariffs gave a boost to U.S.-listed shares of Indian companies.

Red Sea reopening adds to shipping overcapacity pressures

-

As Houthi attacks on the critical shipping lane subside, and Suez Canal transit rises, container companies are bracing for pressures on their bottom line if freight rates lower and oversupply worsens.

-

Danish group AP Møller-Maersk, the world’s second largest container shipping company, announced its first operating loss in years and plans to cut jobs to insulate these impacts.

-

Naval escorts have become a necessity for container ships passing through the Red Sea, and tensions between Iran, the U.S. and Israel remain a threat to the stability of the passage.

Ottawa indicates foreign aid will be increasingly tied to trade objectives

-

Randeep Sarai, Secretary of State for International Development, said Canada’s development and humanitarian spending will focus more on opportunities that create “mutual prosperity.”

-

As it reduces the foreign aid budget, the government will look to use the distribution of these dollars as a tool with countries that Canada wants to increase trade with.

— Thomas Ashcroft