A. Methodology and Data Sources

Oil and Gas

For the oil and gas industry, the capital required includes:

-

Brownfield investment to incrementally increase conventional oil and the oil sands output;

-

Greenfield investment to develop new oil sands production capabilities;

-

New oil pipeline infrastructure to strengthen export capacity;

-

New investment in natural gas extraction;

-

New LNG export facilities;

-

Investments for carbon capture projects.

Our Trend Growth Scenario for oil borrows production forecasts from RBC Capital Markets.

-

Production grows from 5.1 million barrels per day (Mb/d) in 2024 to 5.9 Mb/d by 2030, then plateaus. The incremental output is proportionately split between conventional oil and the oil sands.

-

Pipeline optimization and improved efficiency enables more oil to flow through existing infrastructure. We assume either the Enbridge Mainline adds 300,000 barrels per day or the Trans Mountain—via pump stations—adds 245,000 barrels per day beyond 2027. We assume no major greenfield production sites are built; increased output is sourced from current sites.

-

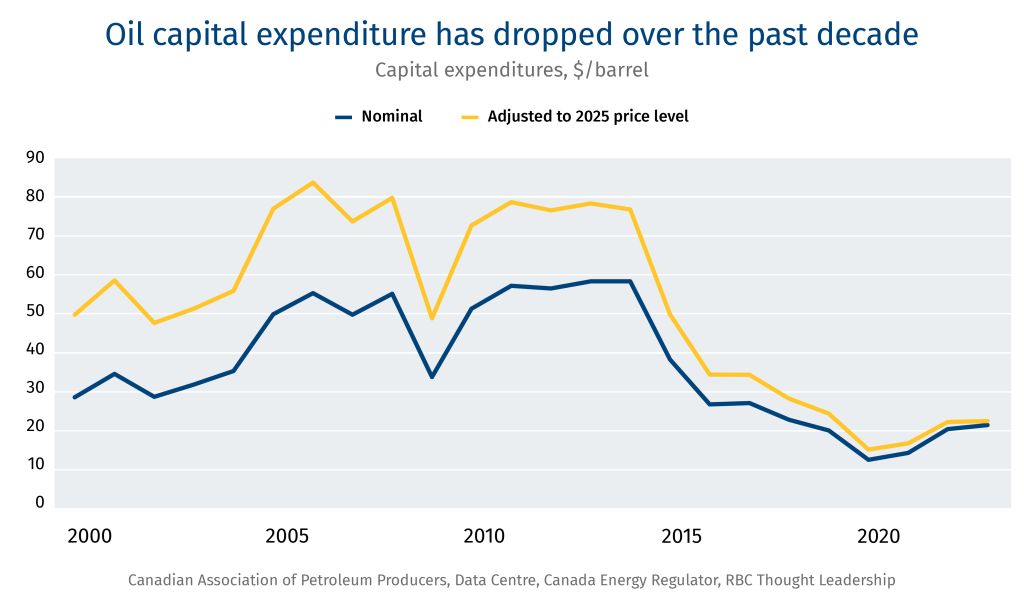

Capital spending figures come from the Canadian Association of Petroleum Producers and the Canadian Energy Regulator. To calculate an annual capex estimate for the coming decade, we took the average capex spent per barrel of oil production from 2017 to 2023 for conventional oil ($38.80) and for the oil sands ($9.90).

-

Our Trend Growth Scenario for natural gas includes completion of the Woodfibre and Cedar LNG facilities. Drawn from Natural Resources Canada, the combined cost is estimated to be $11.5 billion. This enables an additional 0.7 bcf/d of new export capacity.

In our Step Change Scenario, we assume two new oil pipelines are approved:

-

Keystone XL adds 0.83 Mb/d and a pipeline from Alberta to British Columbia (loosely inspired by Northen Gateway) adds 1 Mb/d in capacity. To generate an estimated cost for each pipeline, we took the cost-per-kilometre for the original Northern Gate pipeline (provided by the National Energy Board) and adjusted it for inflation and cost overruns. We estimate that each pipeline costs approximately $30 billion. We assume that pipeline construction begins in 2028 and will take four years to complete. This adds ~1.2 Mb/d in oil sand production capacity. This estimate includes a 70:30 split between bitumen and condensate in the pipelines themselves.

-

The added pipeline capacity enables greenfield investment in oil sands at a cost of ~$56,000 per barrel per day. This enables total Canadian oil production to grow to 7.1 Mb/d by 2035.

-

Our Step Change Scenario includes three additional LNG export terminal projects: LNG Canada Phase 2, Tilbury, and Ksi Lisims. The estimated costs are drawn from publicly available sources. Collectively, these export terminals require ~$55 billion in capital spending. These terminals add 3.75 Bcf/d of export capacity. We assumed $10 per barrel of oil equivalent (BOE) in capex cost for the added natural gas extraction.

-

Our step change scenario imagines heavy investment into carbon capture and sequestration (CCS) infrastructure. We assume major projects go forward, including the Pathways Alliance’s Phase 1, at a cost of $24 billion. We assume two additional projects of a similar scale go forward. We loosely estimate the total investment for CCS projects amounts to $80 billion over 10 years, based on publicly available estimates. We source project-level CCS data from the BloombergNEF Carbon Capture Capacity Database and include approximate costs from various sources, including news articles.

Electricity

For the electricity sector, the capital required includes:

-

Initial project costs to build power plants that are already in various stages of development or have been announced;

-

The costs to replace or upgrade the power grid, including transmissions and distribution lines, enabling new connections and reinforcing systems.

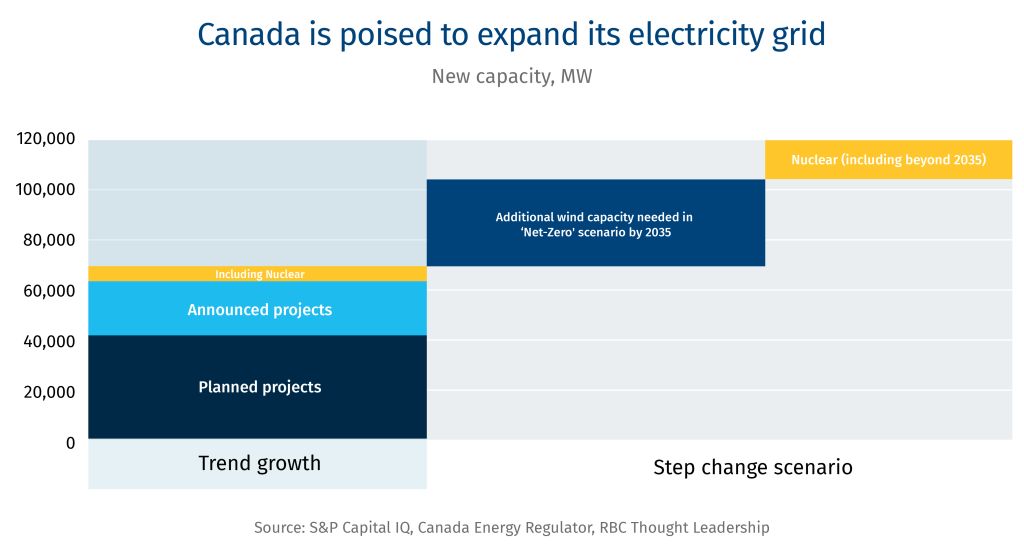

Our Trend Growth Scenario sees projects in various stages of development proceed to the construction phase.

-

Electric capacity grows by ~69 GW across all energy sources. We account for projects where permitting processes have started, where projects have secured financing, and where projects are already in construction phase, and power projects that have been announced. We rely on the S&P CapIQ power projects database. The data provides capacity and construction cost measures for projects by technology type.

-

We also include the Bruce C and Darlington SMR nuclear projects in our trend growth scenario. Combined, they provide 6 GW of new capacity. OPG estimates the cost of the Darlington SMR at ~$21 billion. For Bruce C, we rely on MIT’s Center For Advanced Nuclear Systems to cost AP1000 reactors, which come in at US$8,300-$10,375 per kW.

-

We use an illustrative deployment schedule of large-scale nuclear from Ontario’s integrated energy plan, evenly allocating construction costs over time. For projects where deployment is expected to take place beyond 2035, we assume a portion of the cost by 2035.

We compare this capacity buildout to the Canada Energy Regulator’s (CER) Energy Futures 2026 projections. Our trend growth scenario is largely in line with new capacity requirements under CER’s ‘Current Measures’ scenario, which assumes a limited additional policy-driven push towards electrification and greening of the grid.

Investments for grid maintenance and enhancement are from BloombergNEF’s projections. These include investments in both transmissions and distribution power lines, and grid substations, as related to replacing aging assets, building new connections, and conducting system reinforcement.

While BloombergNEF’s scenarios do not directly correlate to scenarios developed by CER (‘Economic Transition Scenario’ (ETS) used for our trend growth), they also assume no further policy support for the energy transition beyond existing measures, similar to CER’s ‘Current Measures’.

In our Step Change Scenario, we incorporate the additional capacity needed for Canada to remain on the net-zero track as projected in CER’s ‘Net-Zero’ scenario. We also include four additional nuclear projects—Wesleyville, Saskatchewan SMR, Point Lepreau and Peace River—which add an additional ~13 GW at an estimated cost of $149 billion, of which $43 billion is allocated by 2035. Under the step change scenario, total capacity grows by 98 GW.

| Technology | CER ‘Current Measures growth 2025-35 (MW) | CER ‘Net-Zero’ growth 2025-35 (MW) | Projects in development (MW) | Announced projects (MW) | Additional capacity in Step-Change scenario |

|---|

| Solar | 10,826 | 10,175 | 9,461 | 4,003 | – |

| Wind | 36,128 | 58,526 | 17,745 | 3,493 | 37,288 |

| Hydro | 6,318 | 6,338 | 1,016 | 6,111 | – |

| Natural Gas | 982 | 5,039 | 7,075 | 4,438 | – |

| Battery | 4,842 | 5,413 | 5,713 | 3,455 | – |

| Nuclear | 2,112 | 2,112 | 6,000 | – | 13,175 |

Similar to the Trend Growth Scenario, we use BloombergNEF’s projections for investments related to grid infrastructure. The Net Zero Scenario describes a challenging yet achievable stretch to get on track for net zero by 2050. While it doesn’t directly map onto CER’s ‘Net-Zero’ scenario, it offers a directional pathway.

| Project | Case | Capacity

(MW) | Cost ($B) | Estimation | Timeline |

|---|

| Darlington SMR | Base | 1,200 | 20.9 | OPG19 | 2029-3520 |

| Bruce C | Base | 4,800 | 58.3 | MIT CANES21 | 2031-4122 |

| Peace River | Growth | 4,400 | 39.3 | Derived estimate23 | 2029-4224 |

| Point Lepreau | Growth | 300 | 5.2 | Derived estimate25 | 2030-3426 |

| Sask. SMR | Growth | 315 | 5.5 | Derived estimate27 | 2030-3428 |

| Wesleyville | Growth | 8,160 | 99.1 | MIT CANES | 2033-4729 |

Mining

Capital requirements for mining sector includes a combination of:

We use a combined approach: general economic modelling to estimate capital spending for the Trend Growth Scenario; and a bottom-up, project-based approach that draws on data from S&P Capital IQ for the Step Change Scenario.

In our Trend Growth Scenario, we utilize the Cobb-Douglass production function using trends over past 10 years, assuming the relationship between investment and output matches historical patterns. The Cobb-Douglas production function quantifies the interaction between labour, capital and productivity in relationship to GDP. We use Statistics Canada Table 36-10-0217-01 to establish the relationship between multifactor productivity (MFP), capital (K) and labour (L) inputs, and real GDP, expressed as follows:

First, we derive a general value for elasticity the factor α, which is ~0.7 on average during 2012-2021. We use the following tables for data on mining and quarrying (except oil and gas) – NAICS 212:

Once the model is set, we apply a 10-year CAGR rate for real GDP, labour, and productivity to extend projections under the Trend Growth Scenario. Real GDP grows at page of 0.6% annually into 2035, which implies ~$139 billion total investment flows into the industry over the next decade, based on historical depreciation rate of ~16%.

Investments here are in reference to fixed non-residential capital flows. This includes construction of industrial buildings such as plants, machinery and equipment, and intellectual property products that are the result of R&D and similar activities.

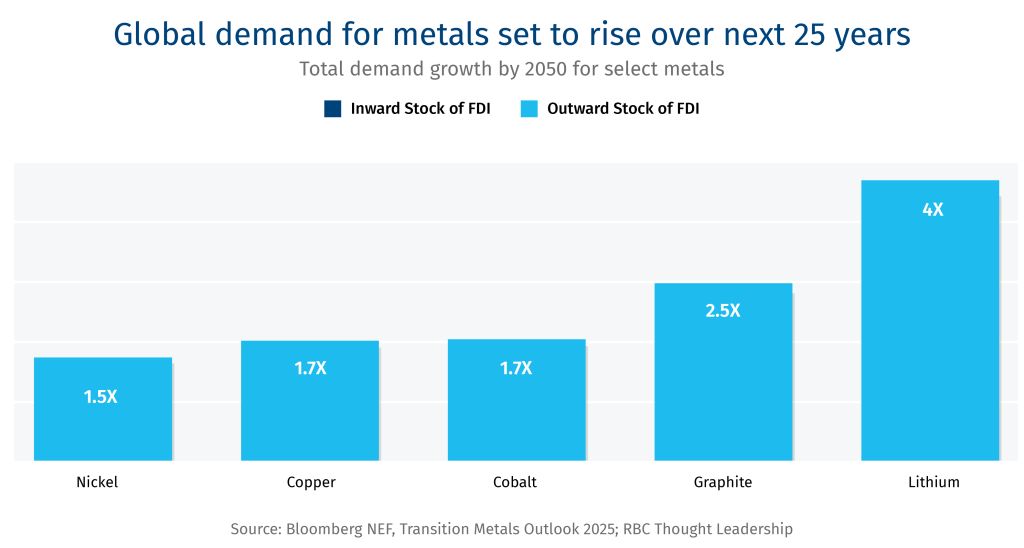

In our Step Change Scenario, we stack the cost of constructing more mines in Canada across a range of metals and minerals: gold, zinc, iron ore, potash, U3O8, copper, lithium, graphite, nickel, rare earth elements (primarily lanthanides), and cobalt. We obtained a dataset of 1,000+ projects currently operating or in various stages of development. To model the Step Change Scenario, we took a bottom-up approach by examining:

-

More than 1,000 active and inactive mining sites across Canada;

-

50+ late-stage projects across base metals (zine and copper, for example), precious metals (gold, silver), and critical minerals (lithium, graphite);

-

100+ early-stage opportunities with known costs or reserves.

We refer to projects in their pre-feasibility stage (reserves development, advanced exploration, prefeasibility and scoping) as ‘early stage’ projects, and those already in feasibility stage or where construction has started as ‘late stage’ projects.

As mining projects move further along the development pathway, more information becomes available. As such, we narrow the focus to 228 active projects with information on initial capital costs or production capacity estimates. Some 95% of late-stage projects have information available.

For projects where only production capacity information is available, we apply an estimated average cost per production capacity for the respective metals or minerals. The Step Change Scenario sees development of all late-stage projects, as well as 10% of early-stage projects proceed to completion over 10 years.

| Metal | Total count | Active projects | Early Stage: Projects with cost or capacity info | Late Stage: Projects with cost or capacity info |

|---|

| Gold | 446 | 296 | 69 | 24 |

| Silver | 32 | 17 | 2 | – |

| Zinc | 91 | 51 | 8 | 7 |

| Copper | 163 | 96 | 24 | 3 |

| Lithium | 32 | 32 | 12 | 7 |

| U3O8 | 47 | 21 | 7 | 3 |

| Graphite | 22 | 14 | 5 | 2 |

| Nickel | 69 | 39 | 11 | 5 |

| Potash | 13 | 7 | 4 | 2 |

| Lanthanides | 14 | 13 | 6 | 2 |

| Iron Ore | 53 | 34 | 11 | 9 |

| Diamonds | 11 | 5 | 2 | – |

| Platinum | 5 | 2 | 1 | – |

| Cobal | 3 | 3 | 1 | 1 |

| Total | 1,001 | 630 | 163 | 65 |

Defence

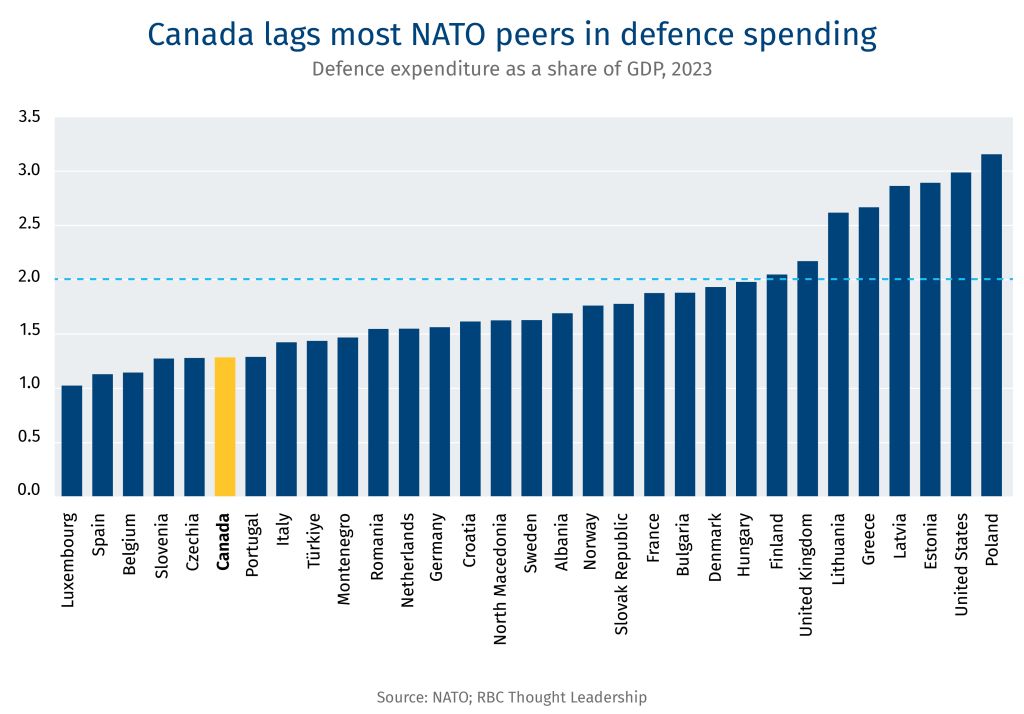

Capital requirements for the defence industry are comprised of a mix of R&D and machinery & equipment, all tethered to different assumptions of government defence spending. According to data from Innovation, Science and Economic Development Canada’s (ISED) State of Canada’s Defence Industry report, the industry generates revenues from domestic sales and exports, with an equal split between the two. And sales to the federal government make up ~two-thirds of domestic revenues.

We assume spending on capital equipment by the federal government is the primary source of the revenue for the domestic industry, and one that varies between the scenarios. We assume other revenues expand at a nominal GDP growth rate of 3.5%.

Historically, M&E and R&D spending have made up ~5.5% of revenue. We harness this ratio to derive the capital expenditure needed by the industry to meet new revenue trajectory.

In our Trend Growth Scenario, we assume Canada reaches only 2% of NATO spending. Spending is allocated across personnel (50%), operations and readiness (25%), capital equipment (20%), and infrastructure (5%), which is the historical mix, with the ‘Buy Canadian’ provision boosting the Canadian content share from 30% to 50% by 2035 (in a linear rise). The federal government has signaled that, historically, some 70% of defence spending was allocated to foreign producers, leaving 30% for the domestic market. Ottawa wants to invert that ratio over the coming decade, tilting the balance 70/30 towards Canadian firms.

In our Step Change Scenario, the primary difference is that Canada is on trajectory to meet 5% NATO spending requirement, of which 3.5% is spend on core defence goods. We assume the spending mix remains the same. Personnel spending remains similar to the Trend Growth Scenario, and readiness and infrastructure spending grow proportionally at the historical allocation mix of 25% and 5%, respectively. The remainder of defence spending focuses on acquiring new (or replacing ageing) capital equipment, which offers increased revenue for the industry, requiring further investment to meet the higher demand.

Space

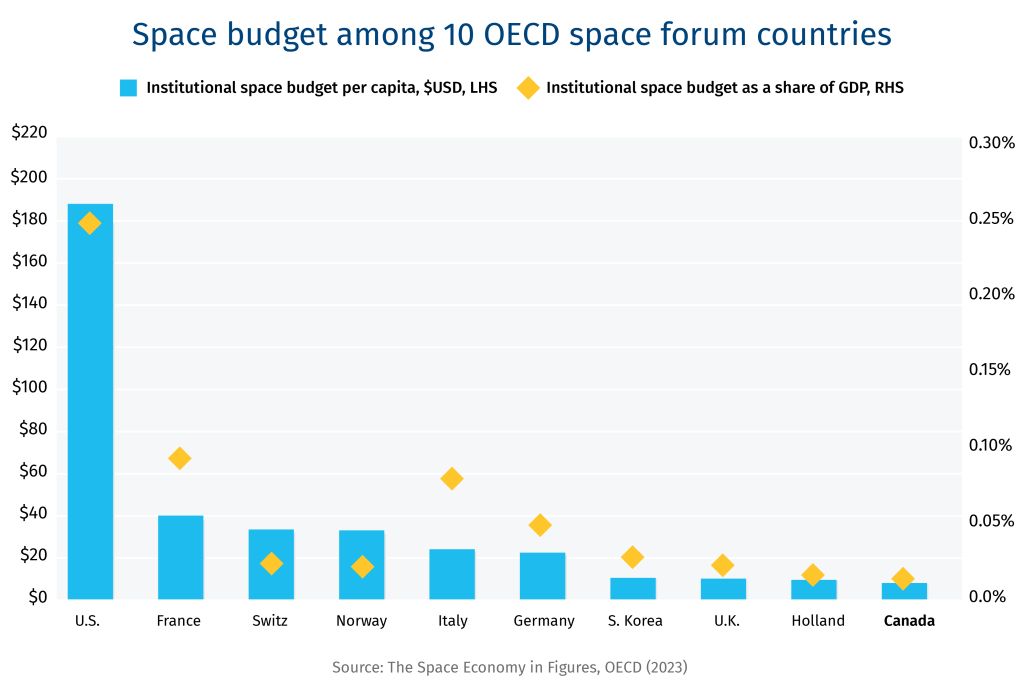

Data on the Canadian space economy is limited. The Canadian Space Agency (CSA) publishes an annual State of the Canadian Space Sector Report, including revenue, gross domestic product, employment and exports. Company-level data is available for publicly traded firms. Our method blended data from both sources to model sales revenue, GDP and capital expenditure across the Trend Growth and Step Change scenarios.

The calculations were made through a series of steps.

-

To forecast sales revenue and GDP to 2035 in the Trend Growth Scenario, we derived the longest possible compound annual historical growth rate using CSA data (2014-2022), which we assume will govern the future growth of sales revenue (-0.8%) and GDP (1%) going forward.

-

To forecast sales revenue under the Step Change Scenario, we assume Canada doubles its global market share by 2035, rising from ~1.1% of the global market in 2022 to 2% by 2035. In partnership with McKinsey & Company, the World Economic Forum projects the global space market will grow to $755B USD by 2035, putting Canada’s share at CA$21B. This scenario thus sees the space market grow 4x in 10 years.

-

To infer the capital required under the two scenarios, we used data for publicly traded space firms. From 2020-2024, Canada’s publicly traded space firms had a capex-to-revenue ratio of 36% (on a weighted average basis). That figure was skewed by heavy investments from a few key firms that are unlikely to be repeated in the future, even under the Step Change Scenario. To better anchor the capex-to-revenue ratio, we included a few mature aerospace companies, which have lower capital requirements. On a weighted-average basis, this brought the capex-to-revenue ratio down to ~10%.

-

Across the Trend Growth and Step Change scenarios, we multiplied annual sales revenue by 10% to determine the annual capex, aggregating the figures over 2025-2035 to determine the total capital required

Agriculture and Food Processing

For the agriculture industry, the capital required includes:

-

Public and private sector support for agricultural knowledge and innovation through expenditure on R&D and IP;

-

Among food processing and manufacturing, capital expenditures on non-residential construction, machinery and equipment to optimize processes at the plant-level;

-

Among large commercial farmers, capital deepening through the adoption of ag-tech solutions.

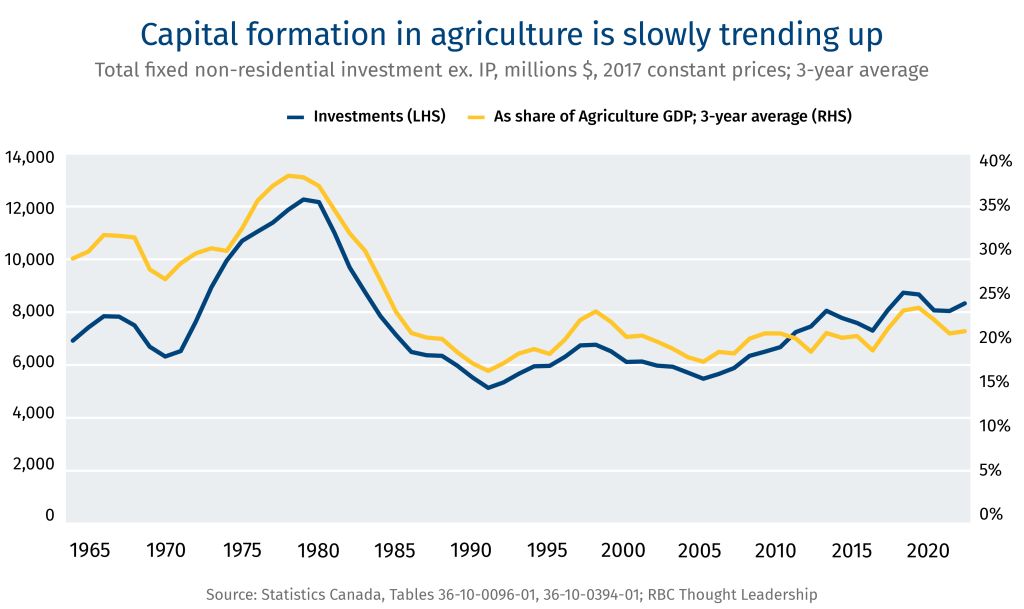

With data from USDA, we explore Canada’s agricultural productivity across multi-decade periods. The trend suggests productivity growth peaked in 1990s-2000s and declined thereafter. From Statistics Canada’s Table 36-10-0096-01 we chart investment trends over the same period. We compare real investment flows over time as well as investment flows relative to the industry’s GDP. We observe high investment rates (both in real terms and as share of GDP) in the mid-1970s and mid-1980s, which are associated with leading productivity gains in the decades that followed. From the OECD’s Agricultural policy monitoring database we track public support for research and development activities dating back to 1986. The trends show declining spending in real terms, as share of industry revenue, and relative to agricultural GDP.

In our Trend Growth Scenario, we extend the average investment trends of the past 10 years. This suggests ~$10 billion annual investment in non-residential construction, machinery and equipment purchases and ~$1.3 billion combined industry IP investments and public support for R&D.

Our Step Change Scenario assumes Canada repeats the investment surge witnessed in the 1970s-1980s, which could raise productivity through more innovation, stronger advanced tech and practice adoption, and investments into efficiency gains. Industry capex increases to ~$13.8 billion annually to match peak levels in 1970s, and combined public and private R&D-related investments rise to $1.6 billion, matching peak levels in 1980s.

Combined total rises to ~$18.9 billion if instead investment levels are calibrated on proportional size to industry GDP – where industry capex investment stood at ~34% (vs 21% currently) as the share of industry GDP on average during 1973-1982, and combined public and private R&D spending was 4.2% (vs 2.7%) during 1986-1995.

For the food manufacturing industry, we tailor the Trend Growth and Step Change scenarios to Canada’s share of global exports aligned with pathways developed in Food first: How agriculture can lead a new era for Canadian exports. Canada’s current market share of global agriculture and agri-food exports stands at 3.7%, and by 2035, global agriculture and agri-food export market (HS codes 1-24) is projected to grow by 0.6% annually. In our Trend Growth scenario for the food manufacturing industry, we assume Canada only maintains it current global standing. This implies 0.8% annual growth in exports of food manufacturing products. Our Step Change scenario for food manufacturing industry assumes Canada increases its export market share by 50%, capturing about US$66 billion by 2035.

In both scenarios, to estimate overall production levels (Statistics Canada table 36-10-0488-01) we combine projected exports with domestic consumption. Domestic consumption is based on historic per capita levels – ~$2500 of real output (adjusted to 2025 price levels) per person, and by 2035, Canada’s population is expected to reach 44.3 million. Overall, food manufacturing production is projected to grow from an estimated $144 billion in 2025 to $155 and $173 billion by 2035 for Trend Growth and Step Change scenarios, respectively. We use a recent spike in investments since 2018, which led to 20% increase in estimated real output, compared to the historic average of 1.9 investment per output ratio during 2007-2017 to derive capital requirements for production capacity increase aligned with our Trend Growth and Step Change scenarios.

B. References

Ampofo, K. et. al. 2024. Transition Metals Outlook 2025. New York: Bloomberg New Energy Finance.

Ashton, Lisa. 2024. Food first: How agriculture can lead a new era for Canadian exports. Toronto: RBC Thought Leadership.

Baskaran, G., D. Wood. 2025. Critical Minerals and the Future of the U.S. Economy. Washington: Center for Strategic and International Studies.

Bataille, M., J. Francis and J. Potin. 2025. The (Re)Convergence of Europe’s Space and Defence Industries. ESPC Report 94. European Space Policy Institute: Vienna.

Bloomberg NEF. 2024. Transition Metals Outlook. New York: Bloomberg Finance LP.

Bryce Tech. 2025. Start-Up Space: Private Sector Space Investment Activity in 2024. Alexandria, VA: Bryce Tech.

Canadian Space Agency. 2023. What we heard report: Consulting Canadians on a modern regulatory framework for space. Ottawa: Government of Canada.

Cembalest, M. 2025. Heliocentrism: 15th Annual Energy Paper. New York: J.P. Morgan Asset Management.

Chollet, D. and S. Kapnick. 2025. Power Rewired: The New Map of Energy and Geopolitics. New York: JPMorganChase Center for Geopolitics.

Competition Bureau Canada. 2023. Competition in Canada, 2000–2020: An economy at a crossroads. Ottawa: Government of Canada.

Conference Board of Canada. (2024). Innovation report card 2024: How Canada performs. Ottawa: Conference Board of Canada.

D’Souza, C., T. Grieder, D. Hyun, J. Witmer. 2020. The Canadian corporate investment gap. Staff Analytical Note No. 2020-15. Ottawa: Bank of Canada.

Globerman, S. 2024. The weakness of corporate investment in Canada, 2001–2021. Vancouver: Fraser Institute.

Gulab, S., and G. Lhermie. 2025. ‘A Case for Reinforcing Agri-food Research and Development Spending: Where Does Canada Stand Internationally?’, The Simpson Centre, 18 (3). Calgary: University of Calgary School of Public Policy.

International Energy Agency. 2023. Emissions from Oil and Gas Operations in Net Zero Transitions. Paris: IEA.

International Energy Agency. 2025. Oil 2025: Analysis and Forecast to 2030. Paris: IEA.

Jurgens, J. and R. Brukardt. 2024. Space: The $1.8 Trillion Opportunity for Global Economic Growth. Geneva: World Economic Forum.

Kanji, S. and A. Parsons. 2024. State of the Canadian Space Sector Report. Longeuil, QC: Canadian Space Agency.

Khosla, J., Y. Kokkinos, C. Turner. 2025. Build big things: Accelerating major project delivery in Canada. Ottawa: Public Policy Forum.

Lindenmoyer, A. 2014. Commercial Orbital Transportation Services: A New Era in Spaceflight. Houston: NASA.

Manalo, P. 2023. ‘Discovery to production averages 15.7 years for 127 mines’, S&P Global, June 6.

Minister of Industry. 2014. Canada’s Space Policy Framework. Ottawa: Canadian Space Agency.

Minister of Innovation, Science and Economic Development. 2019. Exploration, Imagination, Innovation: A New Space Strategy for Canada. Ottawa: Canadian Space Agency.

Mintz, J. 2025. ‘Why Canada Needs ‘Big Bang’ Corporate Tax Reform’, Perspectives on Tax Law & Policy, 6 (4): 1-4.

Mollins, J., P. St.-Amant. 2019. The productivity slowdown in Canada: An ICT phenomenon? Staff Working Paper No. 2019-35. Ottawa: Bank of Canada.

Natural Resources Canada. 2024. 10 Key Facts on Canada’s Critical Minerals Sector. Ottawa: Government of Canada.

OECD. 2023. The Space Economy in Figures: Responding to Global Challenges. Paris: OECD.

OECD & FAO. 2025. Agricultural Outlook 2025–2034. Rome: OECD Publishing.

Pardy, G., R. Mann, C. Neibert, M. Harvey, R. Kwan, M. Choy, N. Ng. 2025. Energy Insights: Awakening the Northern Giant. Toronto: RBC Capital Markets.

Robson, W., M. Bafale. 2024. Underequipped: How weak capital investment hurts Canadian prosperity. Toronto: C.D. Howe Institute.

Sharp, A., T. Sargent. 2023. ‘The Canadian productivity landscape: An overview’, Canadian Tax Journal, 71:4, pp. 1125-47.

Smith, T., K. et. al. 2025. Missions for prosperity: Building Canada’s next era of economic growth. Toronto: Boston Consulting Group & Centre for Canada’s Future.

Space Capital. 2025. Space Investment Quarterly, Q3-2025. New York: Space IQ.

Theron, G. 2025. Raising business sector productivity: Economic Survey of Canada. Paris: OECD.

Mohamad Yaghi, 2023. Farmers Wanted: The Labour Renewal Canada Needs to Build the Next Green Revolution. Toronto: RBC Climate Action Institute.

C. Acknowledgements

The authors would like to thank the following people, whose insights informed our thinking and writing, as well as the numerous experts who wished to remain anonymous:

Agnico Eagle Mines: Alden Greenhouse

Arrell Food Institute at the University of Guelph: Evan Fraser

Bennett Jones: John Baird

Bombardier: Francis Richer De la Flèche

Brookfield Asset Management: Cyrus Madon

Bruce Power: James Scongack

Canada Pension Plan Investment Board: Andrew Alley, Bruce Hogg, Tara Perkins

Canadian Climate Institute: Kate Harland

Canadian Food Innovation Network: Richa Gupta

Export Development Canada: Sven List

MDA Space: Guillaume Lavoie, Patrick Nihill

NASA: Alex MacDonald (Alumni)

NordSpace: Rahul Goel

Ontario Ministry of Agriculture: Steve Duff

Ontario Teachers’ Pension Plan: Jonathan Hausman

Prospectors & Developers Association of Canada: Jeff Killeen

RBC: Tracy Antoine, Daniel Chornous, Louis Derlis, Chinyere Eni, Andrew Hay, Ken Herbert, Sara Gelgor, Stuart Kedwell, Robert Kwan, Eric Lascalles, James McGarragle, Lorna McKercher, Rob Nicholson, Greg Pardy, Chris Redgate, Hugh Samson, Michael Scott, Michael Siperco

Space Canada: Brian Gallant

Teck Resources: Jeff Hanman, Dale Steeves

The Simpson Centre for Food and Agricultural Policy: Sabrina Gulab

University of Calgary: Robert Johnston, Jack Mintz, Trevor Tombe

Volatus Aerospace: Greg Colacitti, Glen Lynch, Abhi Singhvi