The past few years have been incredibly hard for many Canadians. The pandemic caused massive disruptions to the job market and the highest rates of inflation in decades, which was intensified by the war in Ukraine. And now comes a trade war with the U.S., with its own set of shockwaves, including job losses and supply-chain upheaval, sending the price of goods even higher. Many can’t keep up.

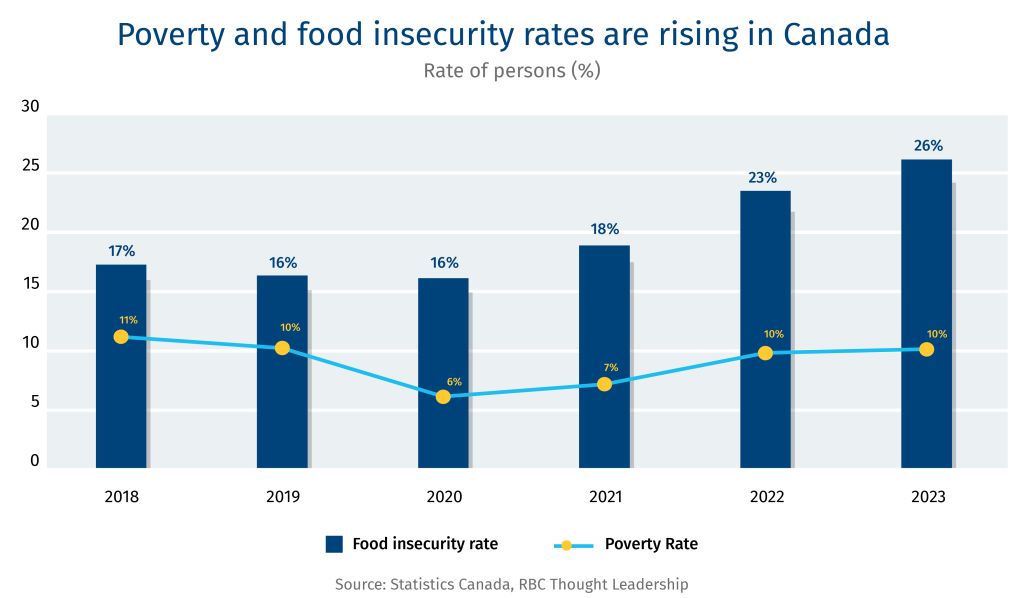

Today, one in four Canadians are experiencing food insecurity. That’s 10 million people—a level never seen before in this country.1 Ultimately, it’s an issue of affordability. There is an abundance of food available. But for an increasing number, it’s out of reach. In March 2024, more than two million visits were recorded at Canadian food banks. That’s a 90% increase in just five years.2 And food banks are a last resort, signalling how dire things have become. Properly supporting and resourcing food banks is critical. However, addressing food insecurity longer term, relies on building a stronger Canadian economy. This includes addressing the affordability crisis, improving productivity, and advancing durable economic development in Canada’s rural and remote areas.

Trade war on food: Rising job loss, costs, and disruptions

Job loss and insecurity is forcing many to make difficult choices

U.S. President Donald Trump’s trade war has caused widespread uncertainty. Launches have been delayed. Production has been paused. Layoffs have been announced. Between January and May, Canada’s manufacturing sector lost 54,000 jobs and the country’s unemployment rate rose to 7%, the highest it’s been since 2016, excluding the pandemic.3 4 Trade exposed industries, including manufacturing, continue to scale down jobs, and now there is greater uncertainty in steel and aluminum jobs with Trump’s 50% tariff on the industry. All this volatility can leave workers in precarious financial situations.

The average Canadian household spent about $76,750 on goods and services in 2023, with 15% and 32% of their money spent on food and shelter, respectively. The lowest income quintile spent $40,080 annually—nearly half that of the average household—with 18% spent on food and 35% on shelter.5 In the event of a job loss—or the fear of potential layoff—Canadians in higher income brackets can cut spending on discretionary items (e.g., new clothes, meals out) in the short term. Lower-income households don’t have that luxury and are left with difficult choices between what basic needs—utility bills, medication, food—they’ll cover. These choices can also impact the quality of food purchased, with lower income households opting for cheaper, lower-nutrient-rich foods.6

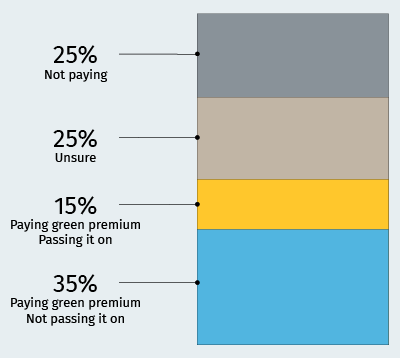

Like downturns in the job market, swings in international commodity markets impacted by tariff wars can impact Canadians whose income is directly tied to market prices. Farmers are often price receivers—unable to pass rising costs onto buyers and consumers. And China’s tariffs on agri-food products including canola oil and seafood have recently taken a toll on Canada’s rural economy. Nova Scotia is thought to be the hardest hit by China’s 25% duties on aquatic products, which represented 9.2% of the provinces total export value in 2024. Farmers and fisherpersons are familiar with volatility in the marketplace from bad weather to shifts in demand. Still, ongoing disruptions can erode stability in rural and remote regions that are already at a disadvantage in accessing economic opportunities and services.

And the impact of tariffs is not just about job security. Windsor, Ontario, for example, is reliant on automotive and advanced manufacturing, food processing, and grains and oilseed handling and shipping. This exposes the entire city and surrounding area to Trump’s tariffs on auto as well as China’s retaliatory tariffs on Canada’s agri-food products. Unemployment in Windsor is higher than the national average at 10.8% in May 2025, up from 7.8% in May 2024.7 And the knock-on effects from multiple pressures on employment within a region and rising costs of living can trickle down to local retail and services. As consumer spending tightens, all sectors and their workers are impacted.

Rising cost of living threatens to further deepen the food insecurity crisis.

With rising costs in Canada, a job is no longer a precursor for meeting basic needs. More than 60% of Canada’s food-insecure households rely on wages, salaries, or self-employment income as their primary source of income.8 Workers experiencing moderate to severe food insecurity often occupy low-wage or precarious jobs that are not keeping pace with the cost of living. Visible minorities, women and new immigrants in Canada earn less than the national average. As a result, food insecurity is disproportionality experienced by these groups. More than 46% of black households and 39% of the Indigenous population living off-reserve are food insecure.9 Single-mother households also have higher rates of food insecurity at 52%.10

The effects of food insecurity further marginalize vulnerable groups. Food insecurity is associated with higher rates of chronic diseases, including diabetes and cardiovascular disease. This means more visits to the doctor’s office and the hospital. Severely food insecure Canadians incur health costs that are more than double those who are food secure.11 Food insecurity also impacts the physical and mental development of children, as well as academic performance and behaviour.12 These impacts underline the health and socio-economic costs to families and the Canadian economy.

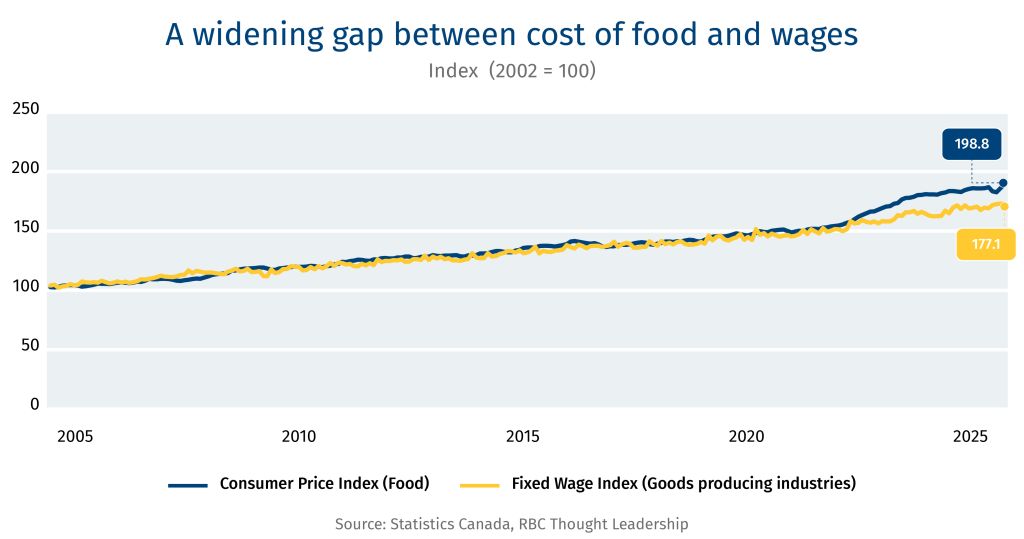

Over the past five years, the affordability crisis has been acutely experienced by households whose wages are not keeping pace with the rising price of goods and services. With pre-tariff inventory coming off grocery store shelves, tariffs are starting to intensify the unaffordability of products in Canada, especially food. Since January 2025, food prices have been a notable driving factor growing the Canadian Consumer Price Index. In April 2025, food prices increased by 3.8% from last year.

Supply chain disruptions impact food consistency and costs

Food companies and retailers reported loses in the first quarter—a direct result of the tariff wars.13 On top of mitigating losses, Canada-U.S. agri-food supply chains are now tasked with additional administrative demands in proving the Canada-United States-Mexico (CUSMA) trade agreement compliance as only two-thirds of Canada’s agri-food exports in 2024 were traded under CUSMA. These stacking complexities and added costs cannot only be absorbed by agri-food suppliers, wholesalers, and retailers, who often operate on thin margins. Eventually rising costs are passed onto the consumer. In the U.S., the impact of tariffs is estimated to increase food prices by 2.6% in the short run, disproportionately impacting fruit and vegetables, that are expected to rise 5.4%.14

Trade wars have sparked a diversification movement. And while trade diversification is a strategy to grow and strengthen Canada’s agri-food exports, it can also result in trade-offs such as short-term uncertainty in quality and cost for consumers while supply chains are being established. Stability and consistency in trade is a key factor in keeping transportation, logistics and operational costs down for traders, wholesalers and retailer, which helps ensure consumers have consistency in price, quality, and availability. Now, uncertainty from tariffs jeopardizes these benefits that North American consumers have become accustomed to through Canada and the U.S.’s interconnected supply chains.

The next step: Tying food solutions to Canada’s growth ambitions

Solutions to food insecurity in Canada are well documented but the issue remains on the sidelines when it comes to large-scale policy and funding commitments.

Potential solutions include:

Address the disparity between Canada’s rural and urban as it relates to access to resources, living wages, and economic development opportunities.

Rebuild Canada’s social safety net to better support low-income households and proactively respond when a household has lost income or has experienced a disruption that impacts its budget.

Improve the affordability of housing.

A food security target may be the catalyst needed to pull these solutions together to drive action across Canada and track progress. This is not a new idea. Food security experts in Canada have called for a 50% target by 2030.15 16 But now is the time to implement a bold vision for food security in Canada as the country sets out to build back a better economy. A key challenge is identifying where food security solutions can be aligned with existing landmark commitments to build momentum. A food secure plan for Canada must also consider how it proportionally improves rates in regions and among groups that are the worst impacted.

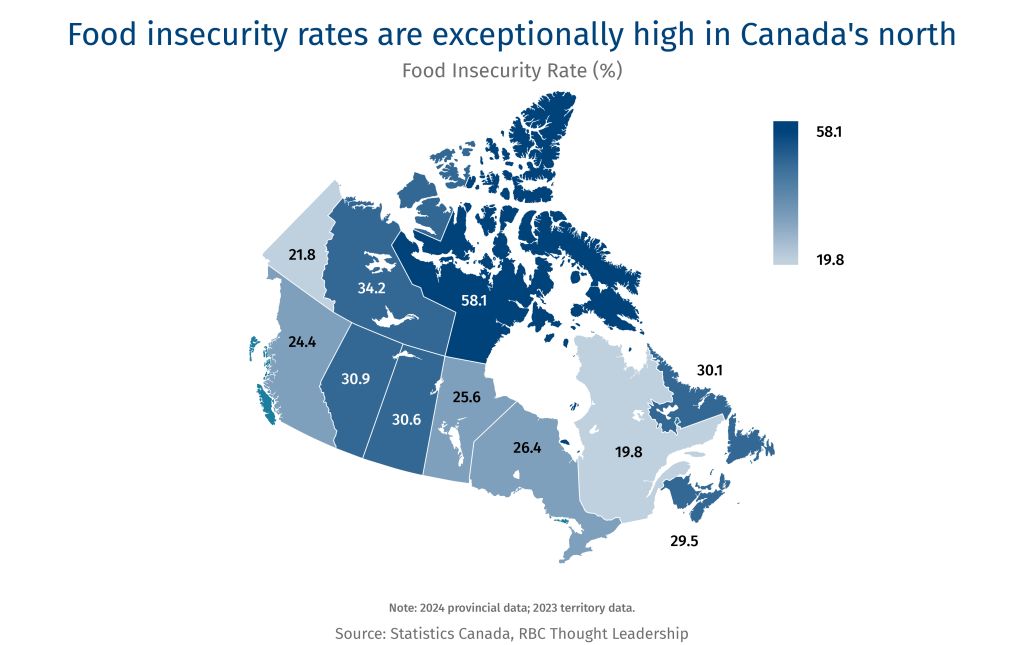

Expedite the development of rural and remote community and health services alongside efforts to expedite Canada’s major infrastructure projects. Canada’s ambitions to accelerate major infrastructure projects from the Port of Churchill to the Ring of Fire are primarily concentrated in northern rural and remote Canada. Canada’s rural and remote areas account for 25% of Canada’s GDP but are grossly underserviced when it comes to health care, housing, and other basic needs, including access to healthy food.17 Food insecurity is high across Canada but is highest in northern and remote areas. More than 58% of people in Nunavut experience food insecurity. Further, only 7% of doctors work in rural areas despite the fact Canada’s rural population accounts for 18% of the total population.18

Much of Canada’s plans to build its economic security and sovereignty hinges on having a productive workforce in rural and remote Canada. But getting people to stay in rural and remote areas or relocate for these projects is a tough sell if they can’t access resources needed for their families to lead a healthy life. Canada can help flip the trend of urban areas growing 15 times faster than rural by mitigating brain and resource drain through investments in community resources including access to healthcare, food and housing that match the ambitions of major infrastructure projects.19

Improving access to household financial supports and benefits through policy reform. It is especially timely to advance such reform efforts as the Liberal government has committed to review and reform the process of applying for the Disability Tax Credit (DTC). The DTC is the gateway to key federal programs, including the Canada Disability Benefit, the Canada Child Benefit for children with disabilities, and the dental benefit. This review process is an opportunity to engage Canada’s network of food banks servicing families that rely on DTC benefit to develop practical solutions that work for households, especially those experiencing housing and food insecurity.

On top of qualifying for benefits, Canada’s most vulnerable groups, including those with disabilities and houseless people, are often the hardest to reach populations for tax returns, and have filing rates below Canada’s national average of 92%.20 Unfiled taxes and unclaimed returns account for more than 8.9 million uncashed Canada Revenue Agency (CRA) cheques, totaling $1.4 billion.21 The value of household tax credits won’t solve a household’s financial challenges, but it’s a start.

Building upon CRA’s automatic tax filing pilot and approaches to streamline and simplify tax filing, there is an opportunity to explore support services that better position Canadians to navigate administrative processes to qualify and access credits. And to learn from community organizations including food banks who offer “wrap around services” such as food and financial literacy programming for Canada’s most vulnerable and marginalized populations.

Align food security objectives with Canada’s home building boom. Cutting housing costs can transform a household’s budget. The new federal Liberal government’s plan to build 500,000 homes a year would boost the economy and address a critical need: one of the priority functions of Canada’s forthcoming entity “Build Canada Homes” (BCH) is to build affordable housing at scale. This priority includes a $6 billion commitment for deeply affordable housing including supportive housing, Indigenous housing, and shelters. Complementary to building these homes rapidly and setting homelessness targets with provinces, government could also consider aligning with national food security targets and activities as a measure of their success in affordable housing and enabling people to achieve a healthy, more productive lifestyle that in turn contributes to growing Canada’s economy.

Food insecurity is a systemic problem, requiring systems-based solutions. As Canada embarks on its pro-growth era, it is opportune to consider how its unified approach can be applied to address the most chronic symptoms of a poor economy—food insecurity and poverty.

Experiences and approaches from around the world

Food insecurity affects every country, and over 295 million people worldwide face acute hunger.1 Countries are taking different approaches to measure, monitor, and mitigate the issue, which extends far beyond food programming and policy into income, housing and social equity domains. However, advanced economies like Canada are increasingly expanding food programming to counter the short-term impacts food insecurity is having on communities.

More than 7 million people, or 11% of the population, in the U.K. are living in food insecure households.22 And one-third of children in the U.K. are living in poverty. To tackle this challenge, the government launched a Child Poverty Taskforce.23 The U.K. also has a few notable programs that directly relate to food access such as:

Free school meals program provides meals for children and young people during school with standards on the nutrition of food offered. Complementary to school meals, the UK launched Holiday Activities and Food (HAF) in 2022 to improve access to food and resources during school breaks.24

Healthy Start vouchers in England, Wales, and Northern Ireland support people on low incomes to access pre-natal vitamins, infant milk formula, and healthy food for young children. In Scotland an equivalent Best Start Foods program launched in August 2019.

Household Support Fund: Allocated £1.5 billion in 2022/23 to help with household essentials, including food, energy and housing bills.

The U.K. is also undergoing its largest home building campaign since World War II. The lack of affordable housing and its impact on household stability and spending is a key driver for this building boom. The campaign goes as far as outlining a plan for creating a dozen new towns of approximately 10,000 homes each.25

In New Zealand, 27% of households with children ran out of food often or sometimes in 2023, up from 14.4% in 2021.26 In response to rising rates of food insecurity, New Zealand led the development of a 10-year food security roadmap for the Asia Pacific Economic Cooperation (APEC) covering four key areas: digitalization, productivity, inclusivity and sustainability. APEC includes 21 member countries across the Pacific Rim, including Canada.

Food security research, policy and programming are delivered under multiple ministries in New Zealand, including health, education, and social development ministries, signalling the recognition of food insecurity’s impact on human health and wellbeing. Within New Zealand there has been a growing movement to improve access across its four main regions to resources for basic needs and to improve healthy living standards:

Launch of the Public Health Advisory Committee in 2022, which was asked in 2023 to review New Zealand’s food system and provide advice and recommendations, which are presented in the 2024 report, Rebalancing Our Food System.

New Zealand provides some government funding to maintain community food distribution infrastructure and support regional community food hubs under its Food Secure Communities program, which was established in 2020.

Ka Ora, Ka Ako (Healthy School Lunches Program) was launched in 2019 to provide free lunches to students attending schools in low-income areas. The program is active in over 1,000 schools and provides meals for nearly 240,000 students every day.

Food insecurity affected 47 million Americans in 2023. The U.S. has experienced a similar post-pandemic trend to Canada with the rate of food insecure households rising from 10% to 14% between 2021 and 2023.27 Among those in the OECD, only Costa Rica has higher levels of income inequality. And proposed legislation such as, One Big Beautiful Bill Act, risk worsening inequality in the U.S. by raising national debt and potentially triggering cuts to programs that are designed to reduce food insecurity and improve food access, including:

The Supplemental Nutrition Assistance Program (SNAP) provides a restricted subsidy to purchase food. SNAP serves an average of 42.2 million people per month (12.6% of the US population).28 Participating in SNAP for six months has been shown to decrease food insecurity by 5-10 percentage points and is even more effective for children and those with very low food security.29 30 SNAP has also shown to positively impact local communities’ economic activity and job creation.

The Special Supplemental Nutrition Program for Women, Infants and Children (WIC) provides a restricted food subsidy for pregnant and post-partum people, infants and children up to five years old who meet both income- and nutrition-based eligibility criteria.31 In 2023, the federal government spent US$6.6 billion on WIC program, reaching an average of 6.6 million people per month.32

Statistics Canada. Food insecurity by economic family type, 2025.

Food Banks Canada. HungerCount 2024, 2024.

Statistics Canada. Labour force characteristics by census metropolitan area, three-month moving average, seasonally adjusted, 2025.

Statistics Canada. Employment by industry, monthly, seasonally adjusted and unadjusted, and trend-cycle, last 5 months (x 1,000), 2025.

Statistics Canada. Household spending by household income quintile, Canada, regions and provinces, 2025.

French et al. Nutrition quality of food purchases varies by household income: the SHoPPER study, 2019.

Statistics Canada. Labour force characteristics by census metropolitan area, three-month moving average, seasonally adjusted, 2025.

Li T, Fafard St-Germain AA, Tarasuk V. Household food insecurity in Canada (2022), 2023.

Statistics Canada. Food insecurity by selected demographic characteristics, 2025.

Statistics Canada. Food insecurity by economic family type, 2025.

Statistics Canada, Canadian Community Health Survey (CCHS) 2005, 2007-2008, 2009-2010, Ontario administrative health databases. Adapted from: Tarasuk, Cheng, de Oliveira, Dachner, Gundersen & Kurdyak (2015)

Gallegos et al. Food Insecurity and Child Development: A State-of-the-Art Review, 2021.

Thriving natural ecosystems are critical to growing North America’s resource-based economy. “Build, baby, build” and “Drill, baby, drill” policies are driven by immediate concerns such as trade, economic sovereignty and security, and affordability. But plans for growth should consider building up our foundational asset–nature.

As part of the Salazar Center for North American Conservation’s symposium in Vancouver last week, the RBC Climate Action Institute co-hosted a roundtable with Nature United. The topic: How nature conservation and stewardship can be positioned as a strategic asset in pro-growth plans for nature-dependent sectors, including forestry, agriculture, and mining.

Here’s what we heard:

Focus on the economic benefits. There continues to be a movement away from models protecting landscapes with no public activity or access to those efforts that benefit local economies–creating jobs, spaces for recreation, and new streams of revenue (environmental credits) and businesses (ecotourism, responsible logging, forest management). This shift reflects that durability in conservation requires people. A good example of this is the Heiltsuk Tribal Council’s 2021 purchase of the Shearwater Marine Ltd., a 63-acre resort and marina in Bella Bella, B.C. The Heiltsuk regained an important part of their territory and unlocked new economic opportunities, including eco-cultural tourism.

Communicate with people where they’re at. The energy transition risks leaving behind rural communities dependent on fossil-fuel extraction for employment and economic activity. Revitalizing these communities via nature-based economies can be part of the solution, but generating buy-in depends on how the opportunities are communicated, requiring a focus on place-based values and priorities. In West Virginia, a hotspot for coal mining and a focus of the Trump administration’s efforts in building back the coal industry, there has been a new wave of growth via a nature-based economy focused on job creation and regenerate abandoned towns. Opportunities span responsible forestry and forest restoration, conservation rehabilitation within renewable energy projects on retired coal mine sites, and growing tourism along the Appalachian Mountain range.

A debate over assigning nature a monetary value. While opponents argue against commodifying nature, proponents say that valuing nature enables a broader scope of stakeholders to invest. This debate has shaped nature’s role in environmental offset markets and other mechanisms that drive investment in nature, from budgetary accounting to green bonds. For example, the town of Gibsons, B.C. developed an eco-asset strategy, integrating the value of nature in its planning processes. As a result, the town determined that green infrastructure was cost effective in managing stormwater, resulting in the reduction of associated development costs for residential and commercial projects.

3 things to watch:

Proposed U.S. tax cut package could authorize the sale of nearly 300-million acres of public lands. There is growing concern that these lands will be sold for mining, logging and drilling with limited restraint on the scale. This is an issue for Canada, as well, since neighbouring public lands provide intact natural landscapes for wildlife crossing borders on migration routes. It also plays a critical role in the U.S.’s ability to meet global biodiversity and climate commitments. Public Lands in Public Hands Act is a piece of legislation that aims to prohibit the Secretary of the Interior and the Secretary of Agriculture from selling land of more than 300 acres to a non-federal entity. The bill was initially sponsored by Ryan K. Zinke, Republican congressperson from Montana. While seeking further support, the bill is with the Congress’ Subcommittee on Forestry and Horticulture.

The role of the UN Agreement on Biodiversity Beyond National Jurisdiction on Arctic development. While the agreement has 114 country signatories, only 21 have ratified it so far. That’s well short of the 60 required for it to take effect and ensure the conservation and sustainable use of marine biological diversity in international waters. The Arctic is home to some of the world’s largest intact marine ecosystems–the protection of which is a timely consideration with Russia, China, the U.S. and Canada eyeing Arctic-based tourism, commercial fishing, trans-Arctic shipping, and deep-sea mining.

Can the Carney government build up Canada’s natural resources in a pro-growth environment? The Liberal government platform outlines a plan for expediting and scaling energy and critical mineral projects, parallel to commitments to expand Canada’s nature conservation efforts. The challenge for a Liberal minority government will be integrating Indigenous reconciliation, nature-positive efforts, and resource extraction pathways while addressing tensions such as the pace of projects and the value of nature in extraction-based sectors.

Lisa Ashton, Agriculture Policy Lead, RBC Climate Action Institute

Martha Rogers, Senior Economist, The Nature Conservancy/Nature United

Field Notes: How Canadian businesses are navigating trade tensions

Canada’s agriculture sector is among the first casualties of the trade wars with China and the United States. Monty Reich, CEO of SWT Ltd, a farmer-owned, independent grain and crop input company in Saskatchewan, discusses how farmers are navigating the trade tensions.

Uncertainty and volatility a near-daily irritant

The current environment is challenging, uncertain—and confusing. “Each day is a different journey,” Reich said.

Even before the 100% Chinese tariffs on canola oil and meal and yellow peas were imposed, the U.S. had started talking tariffs in December, with durum wheat on the list to be hit.

SWT had to absorb the financial blow of U.S. tariffs on durum wheat, choosing not to pass those costs onto its farmer-shareholders. “We sold product into future spring positions and took that hit on our own bottom line,” Reich noted.

U.S. tariffs have made durum wheat exports more costly. “We are the importer of record,” Reich noted, meaning SWT itself is directly responsible for paying the 25% tariff—a cost that prohibits any future sales.

Canola prices are plunging

For canola farmers, the impact has been brutal. Prices have plunged by 25-30% since the Chinese tariffs were imposed, dropping from around $16 per bushel to $12.

“Margins on the farm are pretty narrow as it is,” Reich said. Even small price shifts can turn a profitable season into a financial disaster. With this level of decline, farmers are watching their incomes evaporate.

Tariffs are hitting from all quarters

China’s restrictions on canola and yellow peas have cut off a crucial market, leaving farmers with few places to turn to. “China accounts for about 87% of the yellow pea market along with the U.S. and India,” meaning farmers now face a near-total lockout.

India’s on-again, off-again tariffs on pulses add another layer of uncertainty, leaving Canadian farmers with few viable alternatives.

Farmers are scrambling for alternatives

“Growers are penciling in right now, trying to figure out what’s going to provide them the best return,” Reich said.

Farmers could pivot to other crops, but in practice, it’s not that simple. “It’s not easy to just flip commodities,” he explained.

Farmers are “scrambling” to adjust before the next planting season.

Deferred investments, shrinking profitability

Some canola crush plant investments were already deferred a couple of years ago due to ongoing challenges with the Chinese marketplace and the cost of construction.

Production facilities being built today are going to continue, and existing facilities will continue operating, but margins are getting tighter.

Farmers are weighing whether to cut back production, reduce costs, or even scale down their operations altogether.

Fear of stranded shipments

China’s anti-dumping tariffs on canola seeds can come soon, adding to the threat.

That risk makes exporting to China a high risk. If canola seed shipments hit the waters, the Chinese “can slap on a tariff tomorrow.” That uncertainty alone is enough to spook exporters and depress prices.

This feels different from the dispute with China in 2019 that was more restricted to a few companies over “dockage concerns,” and quality issues.

Backdoor trade routes

In the past, when China restricted direct imports, Canadian canola still made its way there—through other markets.

“There will be other South Pacific Asian countries that’ll take the product and flip it over to China.” But those countries will try to secure the goods at a discount.

In addition, building trade relationships with new markets takes time. It’s not simply about switching markets from one to another (e.g., from China to the Philippines).

Other crops are also facing challenges

Pulse crop (e.g., lentils) are also facing challenges, particularly due to tariffs from India. This adds pressure to the profitability of these crops, with farmers having to navigate changing trade policies, especially when tariffs are applied or removed unpredictably.

Who will replace Canadian canola?

In the short term, other countries such as Australia can substitute Canadian canola, but Canada’s product is generally seen as highly reliable and high-quality.

As supply and demand dynamics shift, other countries may adjust their crop rotations to meet market needs.

Billions of dollars have been invested in Western Canada in canola capacity and crush capacity. There’s a lot of investment at stake in canola to “just let it go away,” Reich said.

The need for stronger government engagement

While farmers often prefer minimal government intervention, strong trade agreements are essential in resolving issues like tariffs or trade restrictions.

Canada’s government should ensure robust trade relations with key partners (China, the U.S., India) to reduce barriers, Reich recommended.

Saskatchewan, for instance, has set up nine offices abroad to facilitate smoother trade relations and reduce friction.

Canadian agriculture needs to have strong representation globally, not just through trade agreements, but through actual presence and ongoing diplomatic engagement.

Government investments are needed to improve infrastructure to boost interprovincial markets and move products west-to-east.

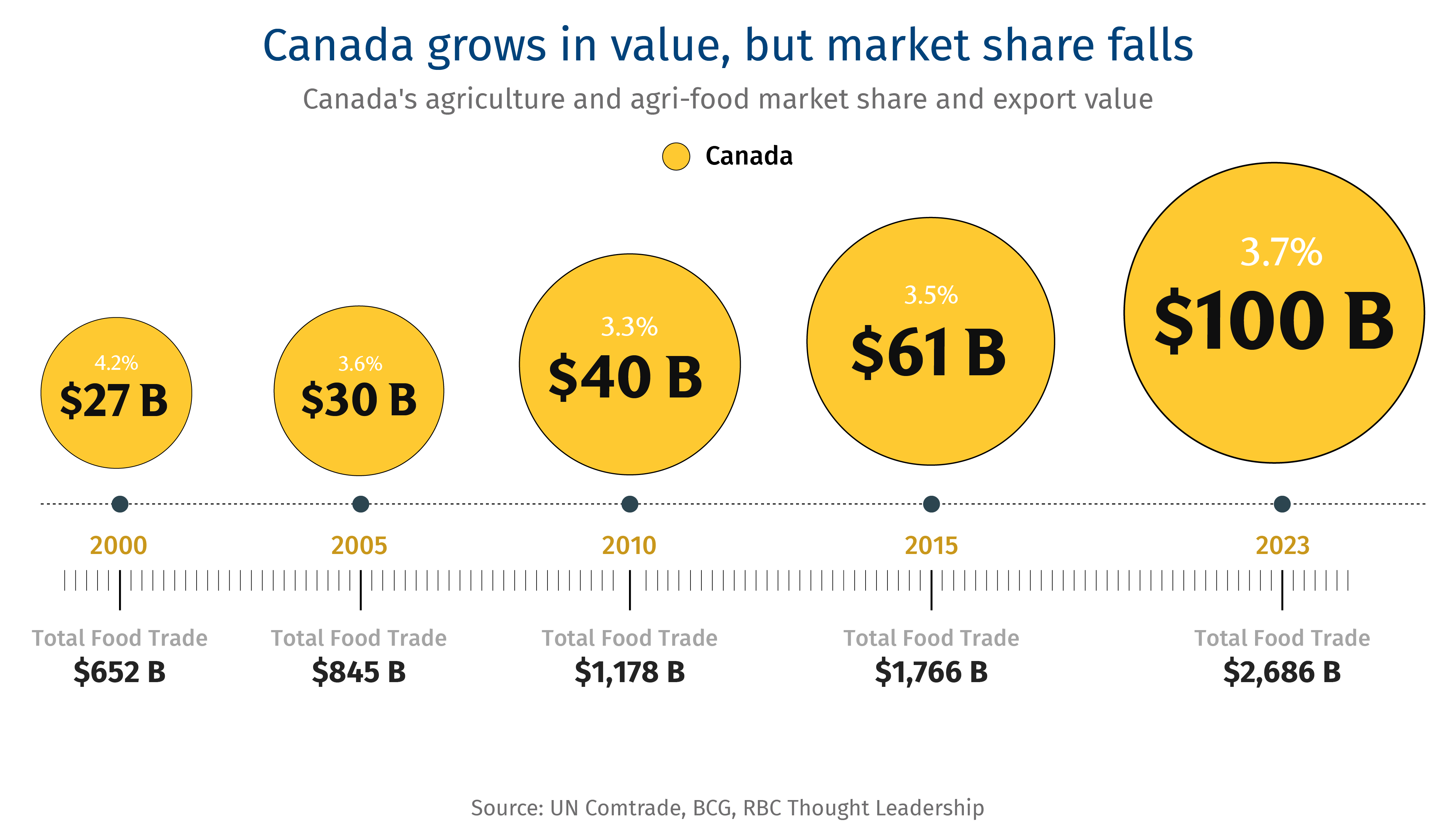

U.S. trade tensions have cast a spotlight on Canadian food trade: American tariff threats pose a special challenge to Canadian agriculture and agri-food exports, as they now account for 20% of U.S. agri-food imports.

Exports to the U.S. are growing: Over 60% of Canada’s agriculture and agri-food exports go to the U.S.—and the value of those exports has quadrupled since 2000.

But Canada’s falling behind competitors globally: Canada’s position in global agriculture and agri-food trade has slipped to 7th from 5th place, and could drop to 9th by 2035 if corrective measures aren’t taken.

Rivals are gaining ground in the world’s top growth markets: Emerging competitors like Brazil have gained ground in Africa and the Middle-East, while traditional rivals like Australia are gaining market share in Southeast Asia.

Canada can increase our global share by 30%: With the right investments, Canada can increase global share from 3.7% to 4.8% to regain 5th place in exports, according to new modelling by RBC and the Boston Consulting Group’s Centre for Canada’s Future. That could add $44 billiona to agriculture and agri-food’s export value by 2035.

A clear plan is critical: To regain market share, Canada needs to focus on innovation, investment, export-oriented infrastructure, digital infrastructure, and overseas agri-food promotion.

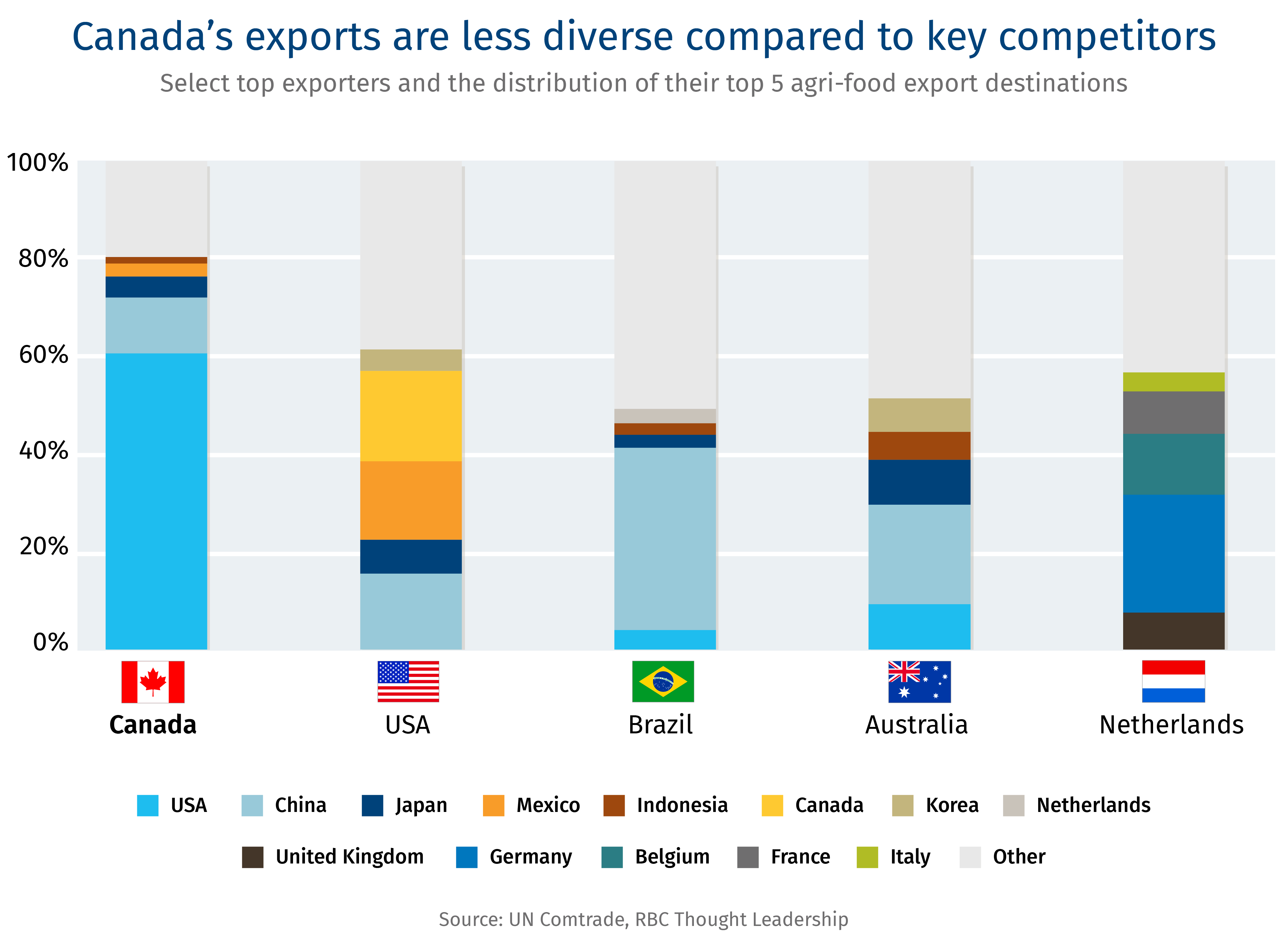

Canada has become overly reliant on the US for agri-food exports

Steel, autos, lumber and oil: The growing trade conflict between the United States and Canada has focused on the backbone of our blue-collar economy. But check any border crossing, and you’re just as likely to see food and agriculture products—be they lobsters trucked from Nova Scotia to Maine, or muffins from Toronto to Chicago, or cattle from Alberta to Montana.

More than $100 billion worth of agriculture and agri-food products cross the border every year, with the U.S. importing nearly 60% of this trade. And thanks to a surge in agri-food processing investment over the last 20 years, that trade gap is growing. The value of Canadian exports to the U.S. has quadrupled since 2000, and Canada is now the source of 20% of U.S. agriculture and agri-food imports.2

This quiet transformation has helped the Canadian agri-food sector become the country’s largest source of manufacturing revenue. No longer just a bulk commodity producer, we are now a dominant foreign supplier to America’s grocery aisles and dining tables, as Canadian farmers and processors have become more advanced in developing new products and marketing them to Americans.

Take canola, for instance, used for cooking and biofuels and meal for animal feed. Thanks to large crushing facilities, roughly 96% of Canada’s canola oil and 65% of canola meal export volumes went to the U.S. in 2024.4 And then there’s potash, which is key to American fertilizers. Canada supplies 85% of U.S. needs, which could go higher if it pulls back from Russia and Belarus, its only other major suppliers.5

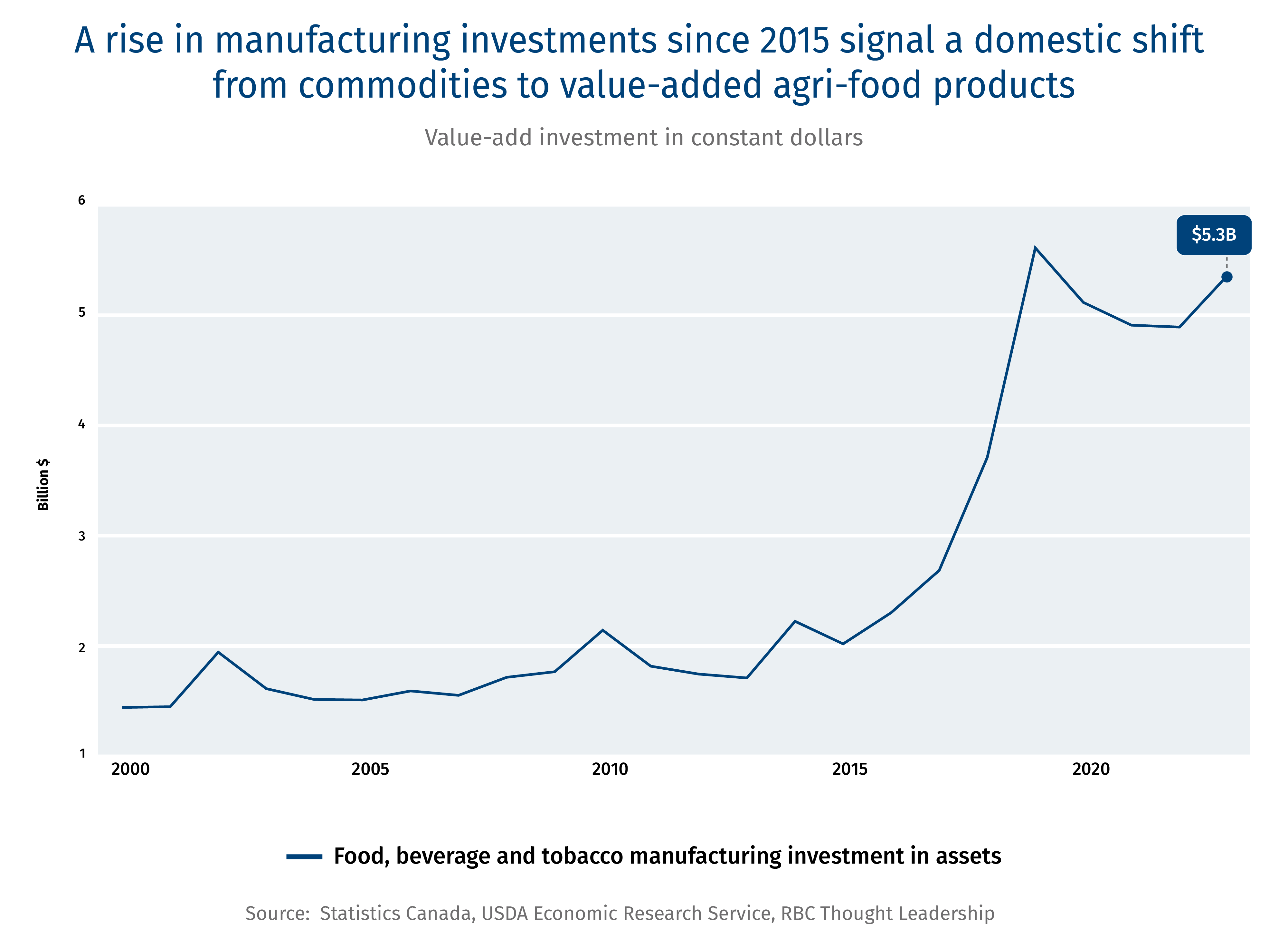

Both countries have benefitted. The U.S. has had priority access to Canada’s production and processing that has a comparative advantage for products including prepared cereals and vegetable oils. Canada’s large production base in the Prairies, as well as the scale and proximity of manufacturing and processing hubs in Ontario and Quebec, have been key to the large inflows of investment capital in recent years. In addition, consistent, high volumes and a lower dollar have propped up Canada’s ability to be a preferred importer. Historical growth in the efficiency of Canadian farms and food processors has further strengthened Canada’s position as a reliable and efficient place to source agriculture and agri-food products from. The result: Canadian food manufacturing has increased its value-add ratio—its production minus its consumption—by 71% between 2014 and 2023.7

These advantages are now in question with the threat of large-scale tariffs. If they’re applied to agriculture and agri-food products, they will make Canada a less desirable trade partner to the U.S., as our position as a low-cost exporter of agriculture and agri-food products relative to others, including China and the Netherlands, will suffer. Agri-food manufacturing may also struggle to maintain investment levels, as one of its biggest selling features has been its preferential access to the world’s largest market.

Such challenges will force Canadian producers to make a choice: accept the cost of tariffs to access the U.S. market, or search for more demand abroad.

Meanwhile, our global competitiveness has slipped

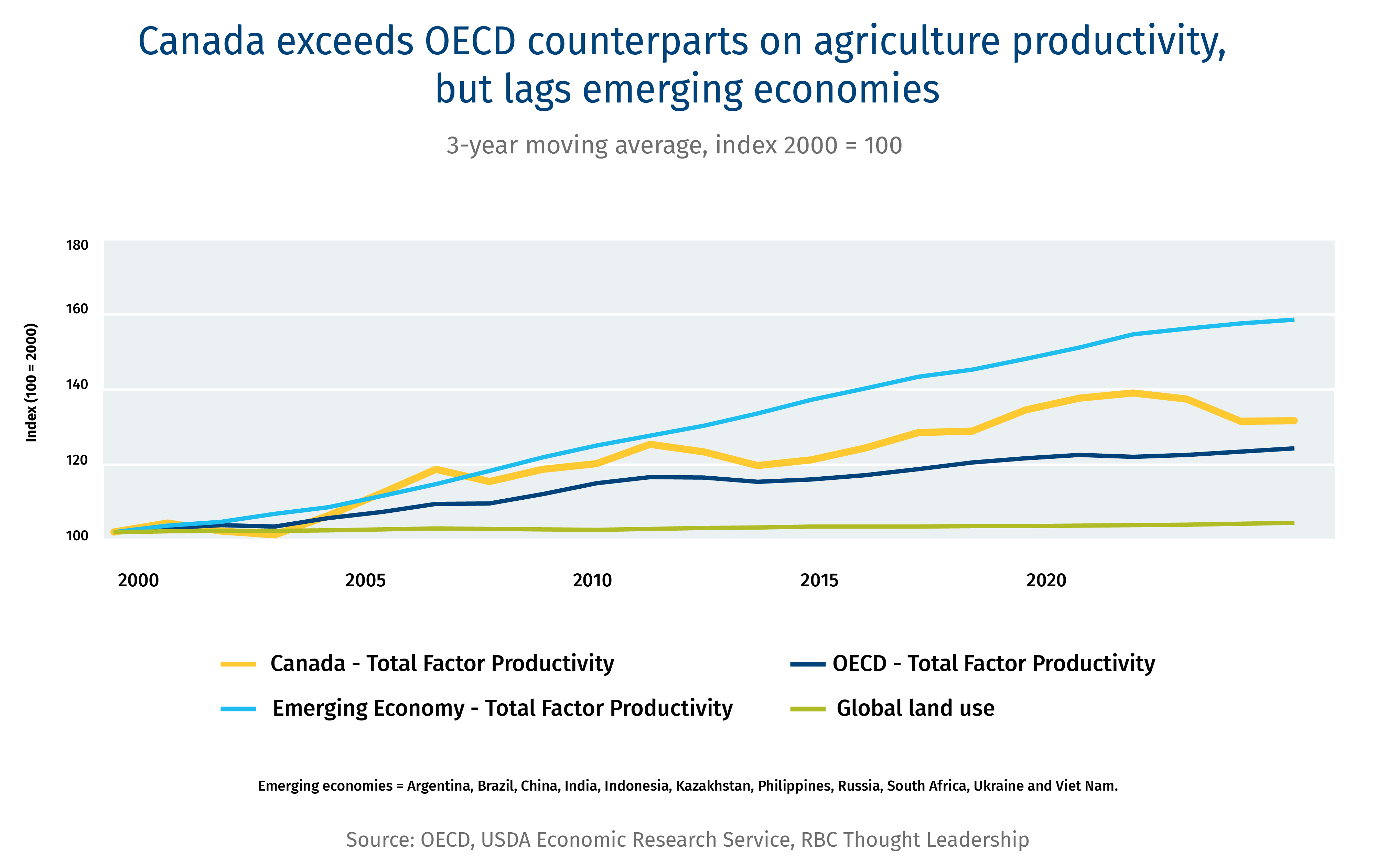

For generations, Canada has been a global leader in agriculture—wheat shipments to China during that country’s post-revolutionary struggles, pork to Japan as its economy took off, lentils to India as it looked to feed its rapidly growing cities, and maple syrup to Europe as it opened its markets. Canadian potash, fertilizer and seeds have also been critical to the ability of the world’s farmers to grow more for their own markets. Thanks to decades of export growth—ahead of most of Canada’s economic sectors—our agriculture and agri-food sector entered the 21st century as a productivity leader. But with so much focus on the U.S. market, many Canadians didn’t realize that the rest of the world was catching up, and in some categories, overtaking us.

Here’s where we stand today on the global leaderboard: over the first quarter of this century, we’ve slipped from 5th to 7th place, bumped by China and Brazil.8 And under a business-as-usual scenario, we could drop to 9th place over the next decade. A global model developed by the Boston Consulting Group’s Centre for Canada’s Future and RBC shows Canada’s market share since 2000 has declined, relatively, by 12%. Our exports are still growing—they’ve quadrupled during that time. It’s just that we’re not keeping pace with the rest of the world, which saw agriculture and agri-food exports grow five-fold over the same period.c d

This relative decline could be an early-warning signal that our agriculture and agri-food exports are not only overly dependent on the U.S., they’re likely to face even greater competition abroad in the decades ahead. Other countries such as Brazil and Chile have taken big bites of markets including meat and fish, where Canada has been competitive in the past.

Ecuador is another case worth studying. It has a highly concentrated inland aquaculture industry, outside the city of Guayaquil, where advancements in shrimp genetics have led to production volume increases of 18-fold since 2000.9 Today, shrimp accounts for roughly 24% of Ecuador’s total exports and 25% of the global crustacean export market, including shrimp and lobster.10 Similar trends can be seen in blueberries from Peru, pasta from Türkiye and soybeans from Paraguay. Such focused, aggressive growth from our competitors has contributed to Canada losing market share in two-thirds of the sectors that make up agriculture and agri-food trade—including meat (-2%), live animals (-5%) and beverages and spirits (-2%). The result for Canada, according to our model: $23 billion in forgone export value in 2023 as a result of market share loss from 2000, which is worth more than the steel and iron Canada exported to the U.S. in 2024.

An important battleground to watch is Southeast and South Asia. India and Southeast Asia‘s global agriculture and food consumption is expected to grow to over 31% of global consumption within the next decade.11 Much of the region has also been a long-time reliable market for Canadian producers, be it soybeans to Vietnam or wheat to Indonesia or peas to India. But the region is increasingly turning to other suppliers. A free trade agreement between Australia, New Zealand and the Association of Southeast Asian Nations (ASEAN) eliminated tariffs on 99% of New Zealand exports to Indonesia, Malaysia, the Philippines, and Vietnam. Through this agreement, Australia has steadily built up its exports to ASEAN, now accounting for 23% of its agriculture and agri-food export value.12 13 Brazil is another competitor to watch. Its enhanced trade promotion has not only made it a bigger supplier to ASEAN; it’s accelerating its presence in Africa and the Middle East—the world’s fastest growing regions—where its export values jumped by 24.4% and 20.4%, respectively, from 2023 to 2024.14

That re-ordering of global food trade occurred largely during a period of liberalized global trade—but that era may now be fading. If tariff and non-tariff barriers become normalized, and trade becomes more politicized, Canada’s ability to compete internationally may be challenged anew, including by growing exporters like Kazakhstan that are seeking to gain market share, especially in Asia and the Middle East.

Last year set a record US$45 trillion in global merchandise trade value, yet year-over-year growth in volumese have been on a downward trend since 2000.15 Average annual growth in trade volume was 2% between 2016 and 2025, slower than 3.45% in the previous decade.16 A key factor driving the slowdown is a deviation from a rules-based system, making way for protectionist-like policies.

For example, harmful trade interventions for cereals have increased by 2.5 times relative to liberalizing interventions since 2009, driven by financial grants, state loans, and import tariffs.17 Agriculture and agri-food often bear the brunt of such policies, given the political importance of food prices and also the political power in many countries of food producers. Average tariffs by a World Trade Organization member charged on an agriculture product is 14.8%, compared to 8% for non-agriculture products.18 A slowing appetite for trade, fewer new trade agreement opportunities, and disruptions to Canada’s North America-first export strategy are among the biggest challenges we may need to consider in the years ahead.

How to diversify: Play to our strengths, grow with new allies, invest in old markets

The opportunity is clear. Our model estimates that Canada’s share of the global export pie could grow by 30% by 2035f, adding $44 billion to total exports, if we pursue three main trade objectives: grow where Canada has market access, expand in the world’s best growth markets, and maintain existing relationships through strengthened “food diplomacy.“

The first challenge is straightforward, which is taking advantage of what we have. Canada has 15 free trade agreements providing access to over two-thirds of the global economy. Through these agreements, there is room to make better use of Canada’s market access in Europe, Asia, and Latin America. For example, the Canada-European Union Comprehensive Economic and Trade Agreement (CETA) is gradually phasing out most tariffs on seafood. Before CETA, EU tariffs for fish and seafood averaged 11%, with highs of 25%. These will be fully phased out within the next five years.19

Taking on new growth markets, with more ambition, is our next challenge. That can start in the Asian markets mentioned in the previous section. Consumers in Southeast and South Asia are expected to have more to spend on higher value products over the next decade, thanks in part to expectations for economic growth that will be among the best in the world, with GDP per capita forecast to rise 3.9%, annually, between 2024 and 2033, up from 2.6% in the previous decade.20 India is one of the clearest opportunities — a market of 1.5 billion people whose economy and standard of living are growing rapidly. This market will increasingly be an opportunity for Canada’s agri-food processing industries, especially plant-based proteins driven by Canada’s production of legumes – peas, lentils, and soybeans.

Canada’s oilseed and agriculture waste processing can also help meet expected growth in biofuel demand in Southeast Asia, where blending rates of biofuels with fossil fuels in markets such as Indonesia are expected to stay above 30%. That would raise biodiesel demand by 56% over the next decade in that country.21 Sub-Saharan Africa, the Middle East, North Africa, and Latin America are also expected to see large GDP expansions. For these regions, we can expect to see total and per capita consumption not only rise, but shift towards more nutrient-dense foods, including animal protein, vegetables, and legumes. One way to help: Canada can contribute to linking global marine transportation to local supply chains by helping to build up food corridors and port infrastructure in Türkiye, United Arab Emirates, and Saudia Arabia as key points of entry to growth markets.

Thirdly, Canada can strengthen and grow current partnerships. These markets include the U.S., Japan, China, and Mexico—the first three of which are projected to have food trade deficits over the next decade that surplus producers like Canada will compete for. Our advantage is established business networks and consumer confidence in our products. In particular, the U.S. is expected to expand its imports of fresh produce, fish, and vegetable oil over the next decade.22 Driving production and processing in these domains will help position Canada as a strategic as well as a reliable partner, if we can make some of the investments we’ll outline in the following sections.

Countries to watch

Brazil – The Investor

Now the second largest exporter of agriculture and agri-food products, Brazil is taking exceptionally large bites out of global oilseed and meat exports, with an approximate 20% and 11% rise in value shares, respectively.23

Row cropping in Brazil nearly doubled between 2000 and 2014, primarily from pasture conversion (80%), but forested land as well (20%).24 Brazil is also improving yields per inputs such as land, fertilizer use, and labour, with agriculture total factor productivity growing by 53% between 2000 and 2022. For comparison, Canada’s productivity grew by 27%. An industrial policy regime took a pro-business support model during the early and mid-2000s that attracted investment from multinational agri-businesses and life science companies, and helped finance growth in domestic storage, transportation infrastructure, and processing capacity.26

Brazil has taken an aggressive approach to marketing and promotion in growth markets and in expanding its market share in China. On the other hand, the European Union, Brazil’s second largest market, is set to enforce a zero-deforestation regulation by the end of 2025, prohibiting select imports, including soy, beef, and coffee products associated with deforestation post-2020.27 The regulation and other similar environmental policies tied to trade could present compliance challenges for Brazil even as domestic deforestation rates fall.

For the next decade, Brazil’s industrial policy playbook, Nova Industry Brazil, will drive innovation and sustainability with agri-food supply chains as a top priority for growth.

Australia – The Trader

Australia has used its 18 free-trade agreements with 30 countries to diversify, expand and adapt its agri-food export flows. The value of Australia’s agri-food exports to India increased +106% between 2022 and 2023 after the Australia-India Economic Cooperation and Trade Agreement (ECTA) entered into force in December 2022. In 2023, Australia took advantage of lower tariffs for meat in the Korea-Australia Free Trade Agreement, raising sheep and goat sales by ~50% in value relative to 2022.28

It’s diversifying its production to align with growth in export markets such as canola, and support that with trade promotion. Its new cross-sector agribusiness expansion initiative is a $85-million-dollar fund aimed at expanding and diversifying agri-food exports.29

An active participant in the Codex Alimentarius Commission, which is a collection of internationally adopted food standards. Alignment on food standards between trading partners is essential to avoid non-tariff barriers.

Spain – The Scaler

The country positioned itself as the go-to market for fruit, vegetables, and pork in the European Union, by focusing on production scale, quality, and regionalized production.

Propelled itself as a leader in agri-food reaching its EU and international customers via its 46 ports.30

Spain scaled production to meet export volume demands through growing productivity and a shift towards farm commercialization. This is evident through its centralized greenhouse production, optimized for regional market access and trade. However, this production cluster is primarily reliant on road transportation, creating vulnerabilities in logistics.

Spain will remain one of Canada’s top competitors in expanding in the European market, if it were to optimize its use of CETA.

Kazakhstan – The Grower

While not yet cracking the top 50 list of exporters, Kazakhstan’s agriculture and agri-food export value has grown by nine-fold since 2000.31

Over the next decade, if Kazakhstan’s agriculture land use trends mirror other agriculture powerhouses such as Brazil, Canada, and the U.S., we can expect to see its pastureland, which accounts for roughly three-quarters of all agricultural land to, in part, be transformed into cropland, strengthening their place in global cereal and oilseed markets.32

Under the Ministry of Agriculture 2021-2030 agricultural development plans, Kazakhstan plans to boost productivity in meat and dairy production, increasing carcass weights and milk outputs per animal, with sights on increasing their exports.33

Its agriculture sector has significant potential for growth, but is underdeveloped and underfinanced. With meaningful investments scaled through state-owned financial institutions such as KazAgroFinance, Kazakhstan will be one to watch for cereals, oilseeds, beef and sheep.34

Brésil

Brésil : l’investisseur

Devenu le deuxième plus grand exportateur de produits agricoles et agroalimentaires, le Brésil prend une part exceptionnellement importante dans les exportations mondiales d’oléagineux et de viande, avec des augmentations respectives d’environ 20 % et 11 % en valeur.

Les cultures en rangs ont presque doublé entre 2000 et 2014 au Brésil, principalement en raison de la conversion des pâturages (80 %), mais aussi des terres forestières (20 %). Le Brésil améliore également les rendements par rapport aux intrants tels que la terre, les engrais et la main-d’œuvre, et la productivité des facteurs agricoles globaux a augmenté de 53 % entre 2000 et 2022. À titre de comparaison, la productivité du Canada a augmenté de 27 %. Le régime de politique industrielle a adopté un modèle de soutien aux entreprises au début et au milieu des années 2000, ce qui a attiré les investissements des multinationales de l’agroalimentaire et des sciences de la vie et contribué à financer la croissance du stockage national, des infrastructures de transport et de la capacité de transformation.

Le Brésil a adopté une approche agressive en matière de marketing et de promotion sur les marchés en croissance, et il augmente progressivement sa part de marché en Chine. D’un autre côté, l’Union européenne, deuxième marché du Brésil, compte appliquer fin 2025 un règlement contre la déforestation interdisant des importations spécifiques, notamment de soja, de bœuf et de produits à base de café associés à la déforestation après 2020. Cette réglementation, conjuguée à d’autres politiques environnementales régissant le commerce international, pourrait poser des problèmes de conformité au Brésil malgré le repli des taux de déforestation dans le pays.

Au cours de la prochaine décennie, la politique industrielle brésilienne « Nova Industry Brazil » encouragera à l’innovation et à la durabilité, les chaînes logistiques agroalimentaires étant définies comme une priorité absolue pour la croissance.

Australie

Australie : le négociateur

L’Australie a mis à profit ses 18 accords de libre-échange avec 30 pays pour diversifier, développer et adapter ses flux d’exportation agroalimentaires. La valeur des exportations agroalimentaires de l’Australie vers l’Inde s’est envolée de 106 % entre 2022 et 2023 après l’entrée en vigueur de l’Accord de coopération économique et commerciale Inde-Australie (ECTA) en décembre 2022. En 2023, l’Australie a tiré parti de la baisse des tarifs douaniers sur la viande dans le cadre de l’Accord de libre-échange entre la République de Corée et l’Australie, augmentant les ventes de moutons et de chèvres d’environ 50 % en valeur par rapport à 2022.

L’Australie diversifie sa production afin de s’adapter à la croissance de marchés d’exportation tels que le canola, et soutient cette politique à l’aide de promotion commerciale. Sa nouvelle initiative d’expansion agroalimentaire intersectorielle est la création d’un fonds de 85 millions de dollars destiné à accroître et diversifier les exportations agroalimentaires.

Participant actif à la commission du Codex Alimentarius, qui est un ensemble de normes alimentaires adoptées à l’échelle internationale. L’harmonisation des normes alimentaires entre les partenaires commerciaux est essentielle pour éviter les barrières non tarifaires.

Espagne

Espagne : l’expansion

Le pays s’est positionné comme le marché de référence pour les fruits, les légumes et le porc dans l’Union européenne, en se concentrant sur l’échelle de production, la qualité et la production régionalisée.

L’Espagne s’est hissée au rang de chef de file de l’agroalimentaire en se connectant à ses clients européens et internationaux depuis 46 ports.

L’Espagne a augmenté sa production afin de répondre à la demande de volumes d’exportation, grâce à une amélioration de la productivité et à une transition vers la commercialisation agricole. Cela se traduit par une production sous serre centralisée, optimisée aux fins d’accès au marché régional et de commerce international. Toutefois, ce centre de production dépend principalement du transport routier, ce qui crée des vulnérabilités logistiques.

L’Espagne restera l’un des principaux concurrents du Canada pour ce qui est de l’expansion sur le marché européen si le pays décide d’optimiser son utilisation de l’AECG.

Kazakhstan

Kazakhstan : la croissance

Bien qu’il ne figure pas encore parmi les 50 premiers exportateurs, le Kazakhstan a multiplié par neuf la valeur de ses exportations agricoles et agroalimentaires depuis 2000.

Au cours de la prochaine décennie, si les tendances d’utilisation des terres agricoles du Kazakhstan reflètent celles d’autres puissances agricoles telles que le Brésil, le Canada et les États-Unis, on peut s’attendre à ce que ses pâturages, qui représentent environ les trois quarts de toutes les terres agricoles, soient transformés en marchés de cultures.

Dans le cadre des plans de développement agricole 2021-2030 du ministère de l’Agriculture, le Kazakhstan prévoit stimuler la productivité de sa production de viande et de produits laitiers en augmentant le poids des carcasses et la production de lait par animal en vue d’accroître ses exportations.

Le secteur agricole du Kazakhstan présente un potentiel de croissance important, mais il est sous-développé et sous-financé. À la suite des investissements significatifs réalisés par les institutions financières d’État telles que KazAgroFinance, le Kazakhstan deviendra un pays à surveiller pour les céréales, les oléagineux, le bœuf et le mouton.

Leveraging global strengths to ensure food security at home

Canada’s agriculture and agri-food sector is not just an exporter; it’s a source of high quality, affordable, and nutritious food for a growing domestic population. We produce more than we need, positioning ourselves as a net exporter of agriculture and agri-food products by $32 billion in 2023.35 However, the production mix of an export-oriented sector may not round out a healthy diet for all Canadians.36 A balanced approach is needed.

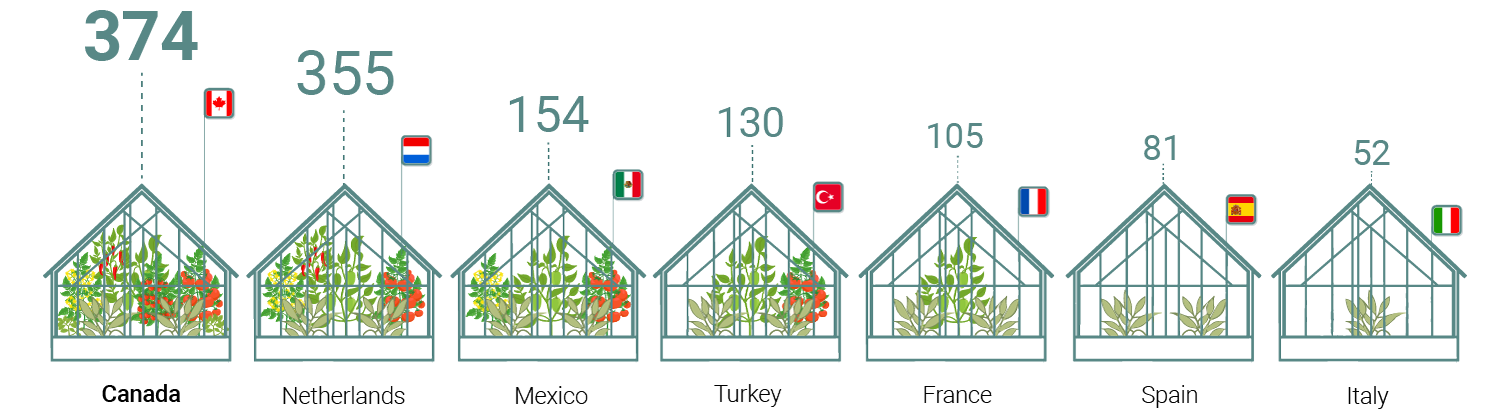

Canada has formed trade relationships with countries that specialize in producing foods such as fruit at a more competitive and productive rate. As a result, Canada runs a production deficit in fruits and vegetables, as well as sugar and confectionary products. Technology can help, in this case through the rise of modern, controlled environment agriculture. Pockets of production in Ontario, Quebec, Alberta and British Columbia have led to greenhouse fruit and vegetable production volumes increasing by roughly five times since 2000.37 This growing industry can play a critical role in closing the production gap, where vegetable production would need to double and fruit production would need to grow by five times to feed domestic demand.38

Canada will need to enable this growth through sufficient utilities, especially water, energy, and waste management. Expanding and decarbonizing Canada’s electricity grids will be essential, and could require provinces to invest nearly $160 billion to double their electricity supply with clean energy. Such investments create ripple effects in decarbonizing Canada’s food system by reducing the carbon intensity of energy used in storage, processing facilities and transportation.

Other areas for growth to meet domestic demand and regain global market share can be found in meat processing as well as fish and seafood production and processing. Meat production nearly doubles Canada’s average consumption rate, while fish and seafood production are just above consumption averages.40,41

These industries have been challenged by high operation costs, volatile commodity prices, labour shortages, and a challenging policy environment for aquaculture. Yet, there is a growing domestic and international demand for sustainable, Canadian-made proteins, which means the efficiencies created through global operations in Canada can help improve the cost and availability for domestic consumers.

Betting on Canada to feed the future may prove to be a safe environmental bet, too. While no country is immune from the negative impact of climate change on crops and animals, yield growth scenarios that account for increasing effects of climate change suggest Canada is projected to increase its role as a global breadbasket of staple crops such as wheat, soybeans, and corn.42 Canada is also well endowed with natural resources, and home to efficient production systems that responsibly use them. Canada’s agriculture water use for agriculture remains low at 11% of total freshwater withdrawal, compared to 67% in Australia and 40% in the United States. 43

Canada’s land use for agriculture also pales in comparison to the United States and Australia, which represents over half of their total land masses, while Canada’s agricultural land covers 6% of the country, underlying the limitations that other agriculture powerhouses face in meeting competing land demands for housing, energy, and food.44,45,46

Five keys to unlocking Canada’s export potential

1. Innovation

We’re a production leader and an innovation commercialization laggard. However, Canada is now also facing a productivity slowdown in agriculture production. Creating room for innovation in efficiency is the next reboot in productivity. Adoption is one area for improvement. Take automated steering for tractors and variable rate technology for fertilizers and seeds, as examples. Adoption rates for both remain low at 27% and 16%, respectively.46 We also need greater connectivity among researchers, start-ups, funders, and companies, preferably within agri-food innovation hubs like the ones grown in the U.S. Mid-West and Netherlands. That will require us to address the widening gap between private and public resourcing, which threatens Canada’s ability to develop partnerships in IP and commercialization. Government spending on agri-food research and development has declined by 9% on average, annually over the past decade. .47

2. Capital

Canada is in the top 10 countries for investments in agri-food technology and innovation.48 We could be in the top five, if annual investments in Canadian-based startups doubled. That could be tougher in a tariff world, which is inherently risky to foreign capital, but the returns on overseas exports could be enough to offset those North American challenges. Further expanding Canada’s agri-food processing sectors will also require upfront investments. Protein Industries Canada estimates we could own 10% of the global market share of plant-based foods by 2035, which would add $25 billion to annual sales. To achieve this ambition, Canada will need 10 to 15 new plant-based food processing facilities and $6 to $9 billion of capital investment for ingredient manufacturing alone.49 Scaling capital in Canada will also require us to beef up the business case, with more competitive approaches to tax and regulation. We can also do more to tell our story and reposition ourselves as a value-add producer, competing on price, quality, and volume. Developing company, region, and industry case studies (see box) that explicitly showcase what in Canada is ripe for growth, can contribute to attracting a new wave of investors.

3. Digital access

Canada needs to fix our 5G gaps. The use of precision agriculture tools highlights the importance of strong wireless connections in rural Canada. These tools rely on app or web-based platforms to improve use of feed, seed, fertilizer, and pesticide, so we can produce more with less. That requires high-speed internet and strong 5G cell reception, which rural Canada is lagging in. Deetken Insights estimates that if all Canadian farmers had access to 5G, it could add between $2.7 billion and $3.5 billion to Canada’s GDP by 2030, through input efficiencies and enhanced automation on farm.50 Canada’s Connectivity Strategy, a national vision for IT infrastructure, has propelled projects across Canada to expand access. Yet, two key agriculture producing provinces, Saskatchewan and Manitoba, have only 50% and 30% rural coverage, respectively, when it comes to 5G.51 Redeploying Canada’s rural connectivity funds to focus on rural and remote 5G access could be the initiative needed to unlock the digital economy for Canadian farmers.

4. Export infrastructure

Turnaround times at Canada’s ports are slower than many large competitors, averaging 2.7 days in 2022 while the United States, Brazil, and Australia, had average turnaround times of 2.1, 1 and 2 days, respectively.52 The Port of Vancouver, Canada’s largest port, has had longstanding infrastructure bottlenecks from the Second Narrows Bridge to the Thornton tunnel, which mechanisms such as the National Trade Corridors Fund or Canada Infrastructure Bank could help transform—if they have transformational funding. Currently, Canada’s roughly $20-billion a year investment on transportation infrastructure lags agriculture competitors such as Australia and the United Kingdom. Keeping up with these economies would require additional investments of between $13-20 billion.53 While ports are our main connection to global markets beyond the U.S., Canada’s rail system is a major domestic connector, and it is challenged with limited routes and rising labour disputes, that too require a rethink for growth. There are smaller opportunities, too, such as container logistics and inland terminals, as simple problems like container storage can clog our ports and rails.

5. Global marketing

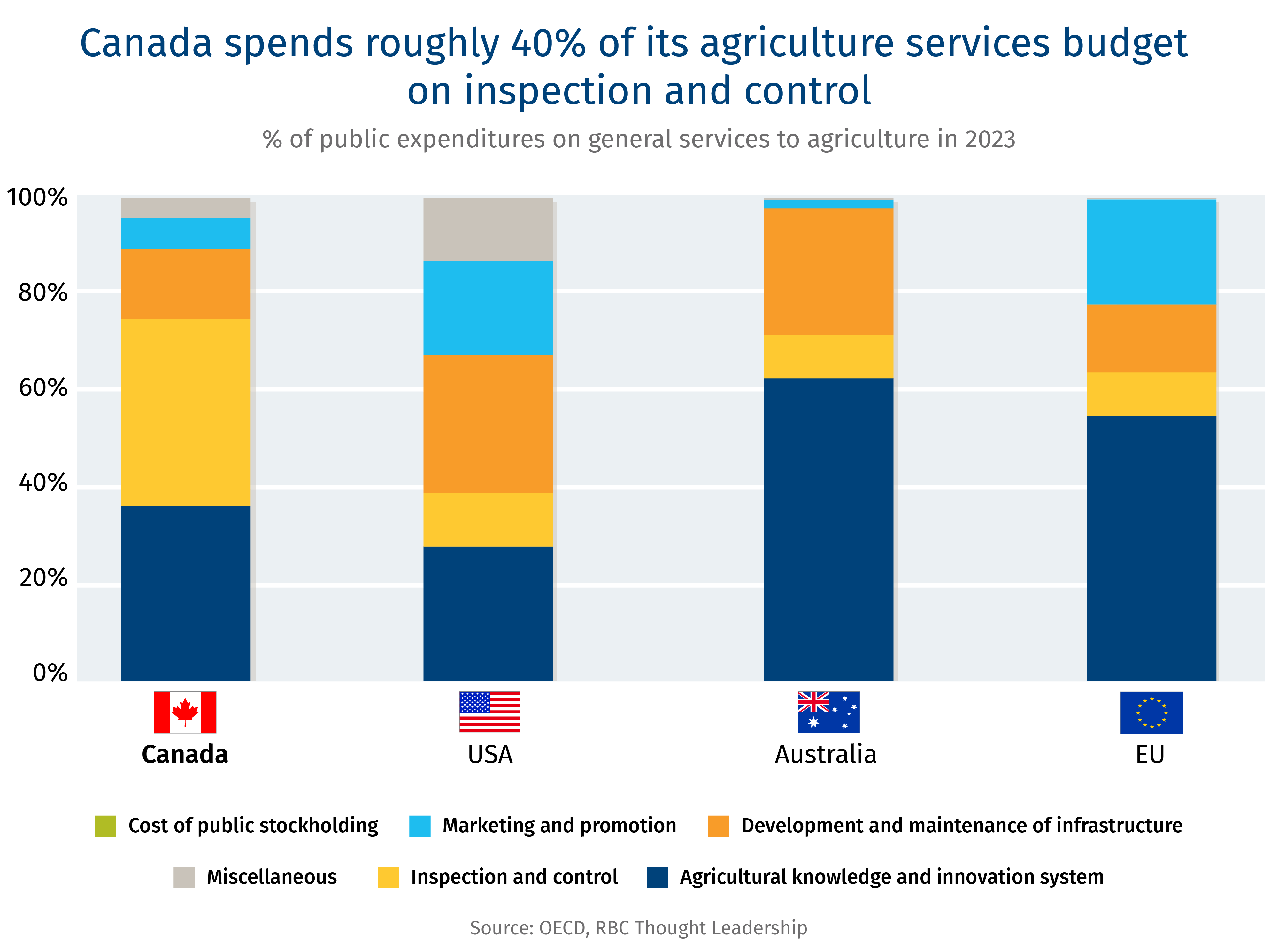

Canada is suffering from a dilution effect in its market development and access approach—with limited resources to boot. The U.S. spends close to 20% of its agriculture support services budget on marketing and promotion, or triple Canada’s share of 6%.54 In a similar vein, gaining market share requires robust inspection and control services that ensure food safety and agriculture production’s protection against new diseases and pests. Canada has a strong reputation, but also must come to grips with a dilemma: even though we allocate 40% of that agriculture support services budget to inspection and control, we still face market access issues and duplicative inspections.55 One approach would be to pick the top five products for export potential and develop priority market assessments, such as Europe for seafood. Pooling public-private resources, the federal government could work with industry associations, companies, and provinces in region-specific, agile taskforces to promote exports and inform regulatory bodies on what’s needed to support growth. A complementary option: position regulatory bodies such as the Canadian Food Inspection Agency to proactively develop standards recognition and harmonization in the identified growth markets.

Canada in 2035

In just 10 years, the world will need to feed close to nine billion people, and many of them will have more income, and appetite, for higher quality foods like the kind Canada is known for. To meet this demand, the world will need to produce 14% more food, feed, and biofuels than we’re delivering today, and do it in a more disruptive trade environment.56

To feed this future, agriculture must also compete with climate change, urban sprawl and rising land use needs from energy production. Moving from short-term reactionary tactics to strategic growth, Canada can use the U.S. tariff threats as a wake-up call to leverage agriculture and agri-food as a driving force for trade diversification while building Canadian self-sufficiency.

Under a high growth scenario, we estimate Canada could return to our position as the world’s 5th largest exporter, regaining our international clout from the early 2000s. In such a scenario, Canada in 2035 would need to expand value added agri-food exports by 50% and grow agriculture commodity exports by 10%.h

If we achieve this growth, we can imagine a Canada in which:

The Atlantic aquaculture industry doubles in production and processing, feeding our European neighbours and the ones just next door;

Alberta, home to 80% of the country’s beef output, advances the resilience of its feedlots and supply chains, contributing to Canada becoming the second largest source of meat in Japan, just behind the U.S., from fourth place today.57,58

Our greenhouse sector, with aspirations of doubling its acres over the next decade, moves Canadians closer to their fresh produce at an affordable price.

Finally, all these products are delivered to consumers via transportation systems with fewer bottlenecks from rail to port and fewer constraints, from on-farm internet to non-tariff trade barriers.

Agriculture is often left off the plate in Canada’s economic strategy discussions. This needs to change if we are to build resilience at home and regain our presence abroad. By acting on these ideas, and others, with precision and speed, the next decade can see a boom in productivity, an unprecedented scale of manufacturing, and a new path for growth through diversified markets. For every part of the country, the opportunity is ripe for growth.

How to be a global champion

AGT Food and Ingredients—The value of processing clusters

Pulses and plant-based product supplier exports to more than 100 countries.

Primary markets: Türkiye, Algeria, Iraq and the U.S.

Growth markets: India, South Africa, Saudi Arabia, and United Arab Emirates.

Export strategy:

Its ability to handle and process high volumes of pulses grown in close proximity to processing facilities in western Canada has boosted its export ambitions.

AGT has an integrated supply chain from farm gate to global distribution, and has expanded its ownership into export-oriented packaged foods and value-added processing infrastructure and bulk and containerized freight handling and transportation.

International business has also been driven by expanding offices and processing capacity in Türkiye, Kazakhstan, United Kingdom, Australia, Europe, U.S., South Africa, and India.

Growth strategy:

Acquisitions and new capacity to expand processing within production clusters have enabled AGT to become a global exporter of value-added pulse and durum wheat food products. It has also positioned AGT to go from a buyer and exporter of commodities to retail products with over 21 facilities across Western Canada.

AGT is investing and engaged in research and development to create novel products and processing systems.

Maple Leaf Food—The value of efficiency

Protein company with products sold in roughly 20 countries.

Primary markets: U.S., China, and Japan.

Growth markets: Philippines, Singapore, and Vietnam.

Export strategy:

Advanced market and supply chain integration with the U.S extends its geographical reach.

Market access and development between Canada and U.S. has also been strengthened through mutual standard recognition on animal welfare, biosecurity, and quality.

The quality of Canadian pork has been well established and enjoys a strong reputation in existing Asian markets.

Setting up offices have helped support market development in Asia. It has enabled MLF to work closely with trade commissioners in Asia for market access and development, and resolving local market issues.

Growth approach:

Recognized portfolio of brands and strong leadership, especially within North American and Asian markets.

Vertically integrated supply chains with a prioritization of reinvesting in the business to expand capacity and improve operational and supply chain efficiencies.

Over the years, MLF has used acquisitions to achieve greater scale but also to acquire major competing or complementary brands.

Highly focused on production efficiencies through automation and developing centres of excellence where processing plants specialize on particular product lines, taking advantage of scale.

McCain—The value of networks

Products are sold in over 160 countries.

Export strengths and approach:

Developed local sales offices in Tokyo and Osaka, and distribution centers throughout Japan to ensure on-time delivery

Close relations between international office and processing facilities to ensure reliable and consistent supply that responds to international customer needs.

In the event of a product shortage due to a force majeure event, such as transportation delays or crop-related issues, they are able to propose an alternative product in a timely manner, since they have production bases in various countries.

Growth approach:

Developed strong, long term relationships with farmers through direct contracts, allowing McCain to be nimble in responding to production and supply chain disruptions and build business resilience.

Invested in regional-specific agriculture resilience to help key supply sheds mitigate and adapt to climate change and other disruptions.

Expanded processing facilities and logistics to existing and emerging agriculture production hotspots. This approach is demonstrated through their recent investment in processing facilities in southern Alberta.

John Stackhouse, Senior Vice-President, Office of the CEO, RBC

Myha Truong-Regan, Head of Research, RBC Climate Action Institute

Yadullah Hussain, Managing Editor, RBC Climate Action Institute

Farhad Panahov, Economist, RBC Climate Action Institute

Caprice Biasoni, Graphic Design Specialist

Shiplu Talukder, Digital Publishing Specialist

Boston Consulting Group

Terence Smith, BCG Centre for Canada’s Future

Keith Halliday, Partner and Associate Director, BCG Global Advantage Practice Area

Arrell Food Institute at the University of Guelph

Evan Fraser, Professor and Director

Amy Standish Assistant Deputy Minister, Policy and Programs, Government of Saskatchewan Brian Innes, Executive Director, Soy Canada Brodie Berrigan, Senior Director of Government Relations and Farm Policy, Canadian Federation of Agriculture Charlie Angelakos, Vice President, Global External Affairs and Sustainability, McCain Foods Limited Craig Klemmer, Manager of Thought Leadership, Farm Credit Canada Cyr Couturier, Marine Biologist & Aquaculture Scientist, Marine Institute of Memorial University Dana Dickerson, Director of Market Development and Sustainability, Grain Farmers of Ontario Darlene McBain, Director of Industry Relations, Farm Credit Canada Dave Carey, Vice-President, Government & Industry Relations, Canadian Canola Growers Association David McInnes Principal, DMci Strategies Deb Stark, Former Deputy Minister, Ontario Ministry of Agriculture, Food and Rural Affairs Erin Gowriluk, President, Canadian Grains Council Greg Northey, Vice President, Corporate Affairs, Pulse Canada Guillaume Lhermie, Professor and Director, The Simpson Centre for Food and Agricultural Policy Ian Ross, President and CEO, Grand Valley Fortifiers Janelle Whitley, Senior Director, Market Access & Trade Policy, Pulse Canada Janice Tranberg, President and CEO, Alberta Cattle Feeders Association Jean-Marc Ruest, Senior Vice-President, Corporate Affairs and General Counsel, Richardson International Limited Jeff Vassart, President, Cargill Limited Canada John Cranfield, Dean and Professor, Ontario Agricultural College at the University of Guelph Kendra Donnelly, Chief Financial Officer, Korova Feeders Kim McConnell, Industry Advocate Kristjan Hebert, President, Hebert Group Kinga Nolan, Policy and Regulatory Affairs, Grain Growers of Canada Kyle Jeworski, President and CEO, Viterra Kyle Scott, Managing Partner, Emmertech Leif Carlson, Director of Market Intelligence and Trade Policy, Cereals Canada Lenore Newman, Professor and Director, Food and Agriculture Institute Simon Fraser University Lorne Hepworth, Board Member, Agricultural Research and Innovation Ontario Michael Harvey, Executive Director, Canadian Agri-Food Trade Alliance Margaret Hudson, President and CEO, Burnbrae Farms Limited Margaret Hughes, Vice President, Sales and Marketing, Avena Foods Mark Walker, Vice President, Markets and Trade, Cereals Canada Martin Scanlon, Dean and Professor, Faculty of Agricultural & Food Sciences, University of Manitoba Matt Korpan, Executive Director of Research and Development, Center for Horticultural Innovation Peter Dhillon, Chairman, Ocean Spray Randall Huffman, Chief Food Safety and Sustainability Officer, Maple Leaf Foods Ray Price, President, Sunterra Richard Lee, Executive Director, Ontario Greenhouse Vegetable Growers Rickey Yada, Dean and Professor, Faculty of Agricultural, Life & Environmental Sciences, University of Alberta Ryder Lee, General Manager, Canadian Cattle Association Sylvanus Afesorgbor, Associate professor, University of Guelph Ted Bilyea, Distinguished Fellow, Canadian Agri-Food Policy Institute Tim Kennedy, Executive Director, Canadian Aquaculture Industry Alliance Tom Rosser, Assistant Deputy Minister, Agriculture and Agri-Food Canada Trevor Tombe, Professor, University of Calgary William Gould, Director of Business Operations, The Progressive Group of Companies Yves Ruel, Associate Executive Director, Chicken Farmers of Canada

UN Comtrade. Trade.

UN Comtrade.

Statistics Canada. Annual Survey of Manufacturing Industries, 2023.

Statistics Canada. Canadian International Merchandise Trade Database.

UN Comtrade.

UN Trade and Development. Revealed Comparative Advantage.

Statistics Canada. Annual Survey of Manufacturing Industries, 2023.

UN Comtrade.

World Bank Group. Aquaculture production (metric tons) – Ecuador.

World Bank Group. Aquaculture production (metric tons) – Ecuador.

OECD and FAO. OECD-FAO Agricultural Outlook 2024-2033, 2024.

Australian Government. Snapshot of agricultural export diversification to ASEAN, 2024.

New Zealand Foreign Affairs and Trade. The ASEAN-Australia-New Zealand Free Trade Area.

Government of Brazil. Historic milestone for Brazilian agribusiness shows leadership in global food security, 2024.

United Nations. Global trade to hit record $33 trillion in 2024, but uncertainties over tariffs loom, 2024.

World Trade Organization Stats. Merchandise export volume change.

Global Trade Alert. Cereals.

Afesorgbor, SK. Trump’s Tariff Threat Could Shake Trade Relations and Upend Agri-Food Trade, 2024.

Government of Canada. Opportunities and Benefits of CETA for Canada’s Fish and Seafood Exporters, 2022.

OECD and FAO.

OECD and FAO.

USDA Economic Research Service. USDA Agricultural Projections to 2034, 2025.

UN Comtrade.

Zalles, V., et al. Near doubling of Brazil’s intensive row crop area since 2000, 2018.

USDA Economic Research Service. International Agriculture Productivity Data.

USDA Economic Research Service. Brazil’s Momentum as a Global Agricultural Supplier Faces Headwinds, 2022.

UN Comtrade.

Australian Government. Agriculture, fisheries, and forestry exports in 2022–23, 2024.

Australian Government – ABARES. Snapshot of Australian Agriculture 2024, 2024.

Invest in Spain. Spain for agri-food industry.

UN Comtrade.

United States International Trade Association. Kazakhstan – Country Commercial Guide, 2022.

Statistics Canada. Table 32-10-0456-01. Production and value of greenhouses fruits and vegetables.

FAO STAT.

RBC Climate Action Institute. Climate Action 2025, 2025. 40FAO STAT.

OECD and FAO.

FAO AQUASTATS. Agricultural water withdrawal as % of total water withdrawal.

AAFC. Overview of Canada’s agriculture and agri-food sector, 2024.

Australian Government – ABARES. Snapshot of Australian Agriculture 2024, 2024.

USDA Economic Research Service. Land Use, Land Value & Tenure – Major Land Uses, 2025.

Statistics Canada. Canada’s farms integrate renewable energy production and technologies toward a future of sustainable and efficient agriculture, 2023.

OECD. Agricultural Policy Monitoring and Evaluation, 2024.

AgFunder. Global AgriFoodTech Investment Report 2024, 2024.

Protein Industries Canada. The Road to $25 Billion, 2022.

Deetken Insights. The socio-economic impacts of 5G, 2022.

Canadian Radio-television and Telecommunications Commission. Current trends – Mobile wireless.

World Bank. Connecting to Compete, 2023.

CANCEA. Canadian Construction Association: Transportation Infrastructure, 2022.

OECD. Agricultural Policy Monitoring and Evaluation, 2024.

OECD. Agricultural Policy Monitoring and Evaluation, 2024.

OECD and FAO.

AAFC. Distribution of slaughtering activity and number of federally inspected plants.

AAFC. Sector Trend Analysis – Meat trends in Japan, 2023.

Estimates are conservative and based on 2023 nominal value.

Trade data is converted from USD to CAD using Bank of Canada’s average annual rates.

Total trade of all goods. This category is inclusive of agriculture and agri-food.

Model estimates a high growth scenario of Canada’s market share growing from 3.7% in 2023 to 4.8% in 2035.

Based on a 3-year moving average.

Scenarios are developed for HS codes 1-24, from 2024 to 2035. Growth in global trade is based on the latest OECD-FAO Agricultural Outlook (projected export tonnage growth at 2023 prices) individually for Cereals, Oil Seeds, Fats, Sugars, Meat and Fish. Global exports in all other categories are assumed to grow at 1% per-year based on OECD-FAO’s projected growth for agricultural commodities overall.

How indoor agriculture can serve as a local food source in northern—and urban—settings

Vertical farming is a form of controlled environment agriculture (CEA), that gives growers more control over the environment they tend their crops in, which can be advantageous in challenging growing conditions.

Indoor vertical farming was set to take off in a big way, but lacklustre investment returns and scaling challenges has limited production.

“There was a big bubble around this industry that has more or less burst over the past four years,” said Dr. Alesandros Glaros, Food and Agriculture Institute, University of the Fraser Valley. “The companies that have weathered the storm are patient and have invested substantially in research and development. They have tried and true technologies, are integrated into strong local and regional supply chains, and are highly collaborative. Now, we can find their vertically grown, competitively priced leafy greens in remote regions as well as major grocery stores.”

There are examples of innovations in the space. British Columbia-based QuantoTech Solutions, a vertically integrated ag-tech company, has developed a growing system that features 8 by 12 feet sheds with shelving units to allow for vertical farming, producing 4.8 between 7.2 tonnes of food per year, including leafy greens, strawberries, and cherry tomatoes. Each unit requires approximately 37.2 to 52 gigajoules of energy per year, which is less than the energy needed to power the average Canadian home1. The mobile units were originally developed for northern and challenging growing conditions, but are also suitable for urban settings.

QuantoTech Solutions’ system features 8 by 12 feet sheds with shelving units to allow for vertical farming.

A food source for northern and remote communities