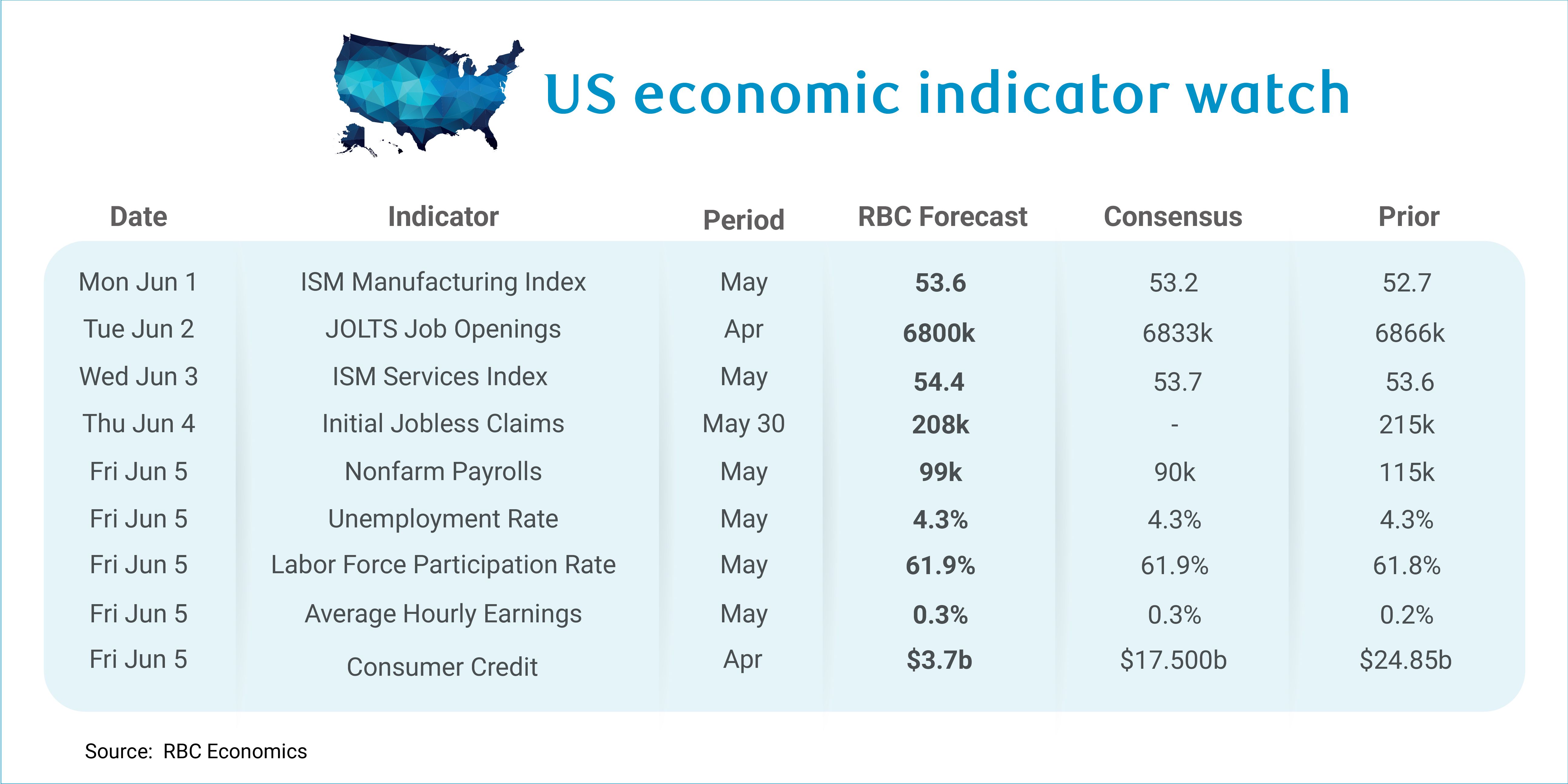

Next week, the May employment report will be front-and-center. We expect 99K jobs were added to payrolls with the unemployment rate holding steady at 4.3%. So far in 2026, the labor market appears to be on solid footing. Still, on aggregate, new job creation has been quite limited with monthly payroll gains averaging 55K over the past six months. But the interpretation of payroll gains is changing.

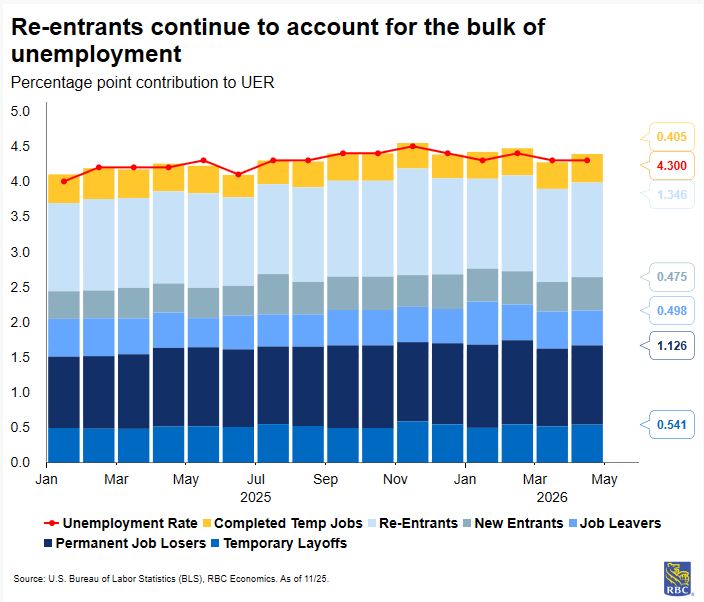

Our estimate of breakeven employment remains exceptionally low, as retirements create openings that when backfilled, don’t show up as a payroll gains. Coupled with the precipitous fall in immigration, the labor market needs far fewer new jobs for the unemployment rate to hold steady. In this lens, we expect the Fed will rely more on the unemployment rate than the payroll report to gauge labor market health.

A key risk remains coincident oil and tariff shocks: if firms cannot pass on higher input costs, margin compression could translate to headcount reductions. By our calculation, the US economy would need to shed 1 million jobs by year-end for the unemployment rate to rise sufficiently to trigger the Sahm rule. This would require all sectors to respond to higher costs with layoffs rather than price increases – and for now that is not playing out. PPI has re-accelerated dramatically in 2026, confirming that passthrough is happening. Limited layoffs, as evidenced by stable jobless claims data, have helped keep the unemployment rate from rising. Still, the unemployment rate is rising for some groups – most notably recent graduates who are facing competition from AI.

Aside from the jobs report, here’s what else we’re watching next week:

-

We anticipate the JOLTS data will show a slight decline in job openings for April (to 6800K). Indeed Hiring Lab’s job postings index fell 1.2ppts in April, suggesting the headline number will be little changed.

-

We get both ISM Services and Manufacturing indexes for May, and both are expected to come in higher than last month. But the headline strength will likely be overshadowed by the price indices which are likely to show continued input pressures rising as energy costs remain elevated.

-

For ISM Services, we expect headline will report 54.4. The Fed regional services survey showed Kansas City and Richmond in expansion, Texas contracting to a lesser extent, and only Philly Fed deteriorating.

-

Initial jobless claims are expected to come in at 208k for the week ending May 30th. Initial claims have largely been rangebound since mid-February (from 200k to 220k) as firms avoid layoffs.

-

Consumer credit likely increased by $3.7B in April as households continue to rely on credit to buffer higher gasoline spending. That said, consumers have largely leaned on savings so far—the personal savings rate has fallen from 4.5% to 2.6% between January and April – suggesting credit hasn’t yet become the primary release valve.

About the Authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. Carrie is responsible for projecting key US indicators including GDP, employment, consumer spending and inflation for the US. She also contributes to commentary surrounding the US economic backdrop which she delivers to clients through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.