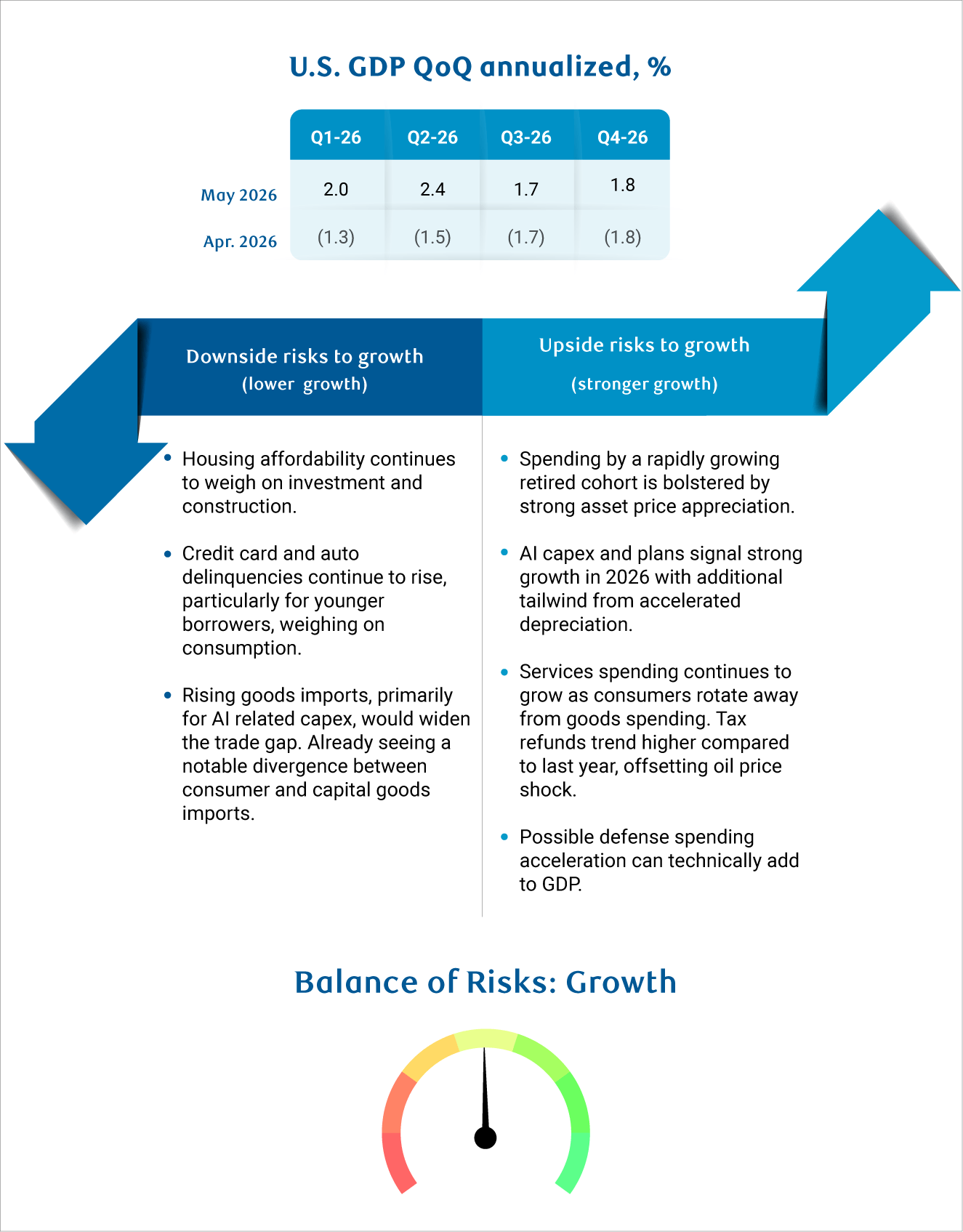

The U.S. economy got a bucket of good news in the past month. Growth in Q1 was better than expected—hitting 2%—and early tracking has us raising our GDP growth forecast for Q2 to a hearty 2.4%. That puts the annual pace of expansion at 2.2%, which may seem like decimal point minutia, but signals gathering momentum above the psychologically important “2% threshold.”

Inflation continues to be a problem, of course (we’ve long held the view that inflation would remain sticky with upside risks). But the labor market is stable— importantly—now even outside of health care. Indeed, as we wrote last month, it’s hard to bet against the U.S. economy.

We acknowledge, however, that this rosy outlook might seem disconnected from a flurry of difficult headlines surrounding the conflict in the Middle East, coupled with surging energy costs and discouraging consumer confidence data.

While it’s clear the U.S. is not currently in a recession, how long can it hold on to the current environment before dreaded recession risk rears its head? A long time. We did the math and found it would take more than one million job losses before the US faced a true technical recession. That makes odds of one in 2026 low, even as we remain mindful of growing risks around our base case.

Reconciling all this conflicting data and headlines means recognizing that two things can be true: Headline data can be solid and improving, while pockets of the economy are struggling.

Lest we be accused of sitting on both sides of the fence, acknowledging headline strength with underlying weakness isn’t about trying to have it both ways. Instead, it’s a pushback against conflating headline strength with either overall health or sector-specific recessions as ominous signs of things to come.

For global markets, headline data matters—and that’s why we watch it closely. But for businesses with targeted clients or operating in specific sectors, divergence from headline growth can be extreme. Put differently, this two-speed economy means the Wall Street versus Main Street divide grows.

Enter the energy shock

Overall, the jump in energy prices is a net neutral effect on the US economy over time since it weighs on consumption but boosts investment—at least in theory.

Yet, one understated feature of the energy shock is the longer it persists, the further it weakens segments of the economy already under duress while having more minimal impact on existing pillars of strength. It effectively widens distance between the two tracks of the economy.

So, while we maintain our cautiously optimistic take of the U.S. economy for 2026, we also emphasize three sectors that are likely to remain persistently weak beneath the “2% economy.” This will be even more true the longer the energy shock continues.

Three struggling sectors despite a resilient aggregate economy

1. Low- and middle-income consumers are bearing the brunt of inflation.

We’ve already witnessed a notable divergence between hard economic data and soft data (i.e., consumer surveys). Weak consumer confidence has been signaling a divide for some time: Job prospects are not as plentiful as before, wage growth is slowing more quickly for lower paying jobs, and tariff-induced inflation disproportionately impacts middle to low income earners.

Real personal income transfers turned slightly negative in March for the first time since 2022. While we have long appreciated that transfer payments are helping prop up the economy and take up a growing share of personal income, consumers who rely on wage and salary income are falling behind. In fact, nearly all other sources of income are outpacing wage growth including dividend, interest and rent—all sources that tend to flow to upper-income households.

Layering on the energy shock doesn’t feel good for most consumers. Gas represents a sizable share of household budgets that has nearly doubled since 2025. That means most households need to find ways to adjust—either through lower savings, higher credit card utilization, or demand destruction. For now, we see the personal saving rate move lower, but that’s not a permanent solution.

2. Trade-related sectors still struggle with tariff uncertainty, and now face added pressure on input costs.

It’s been a bumpy ride for trade in the US—one that saw a massive surge of imports ahead of Liberation day, a pull forward of spending by consumers, and an unusual drawdown of inventories typical during recessions. Yes, IEEPA was overturned, but that is only adding to the uncertainty. Some companies will get tariff refunds, but it’s unlikely to help consumers. And, the administration is likely to continue pursuing tariffs through other avenues, meaning the outlook for trade will remain in flux for the rest of 2026. This suggests hiring, investment, and broader activity in trade-reliant sectors will be negatively impacted until trade policy negotiations conclude.

3. Non-AI business investment continued to slow in Q1 despite the accelerated depreciation benefits offered by the One Big Beautiful Bill Act.

A big part of this story is financing costs—borrowing costs are influenced by long-term rates, which remain elevated. That’s in addition to already high input costs.

Indeed, consumers are not the only ones feeling the pinch of higher inflation. The Producer Price Index is re-accelerating, and shows costs for critical inputs like steel, copper, and concrete as well as transportation and warehousing costs are elevated.

AI-related investment did get a boost from the CHIPS Act, and the tailwinds will continue as investments in AI-related equipment and software are poised to accelerate. But, the appetite for investment outside of AI is falling amid trade uncertainty, weakening in consumer sentiment, and high borrowing costs.

Growth outlook

Even in the face of the ongoing conflict in the Middle East, our outlook is cautiously optimistic as we expect higher tax returns in Q2 (the greatest tailwind) will offset higher gasoline prices for consumers (the largest headwind).

In May, we upgraded our growth outlook for Q2 to reflect recent upside surprises from the consumer coupled with ongoing strength in productivity, AI investment and sizeable government spending. However, with a higher baseline, we now view risks to our outlook as broadly balanced (versus tilted upside), and continue to monitor the feedthrough from the commodities shock into the economy.

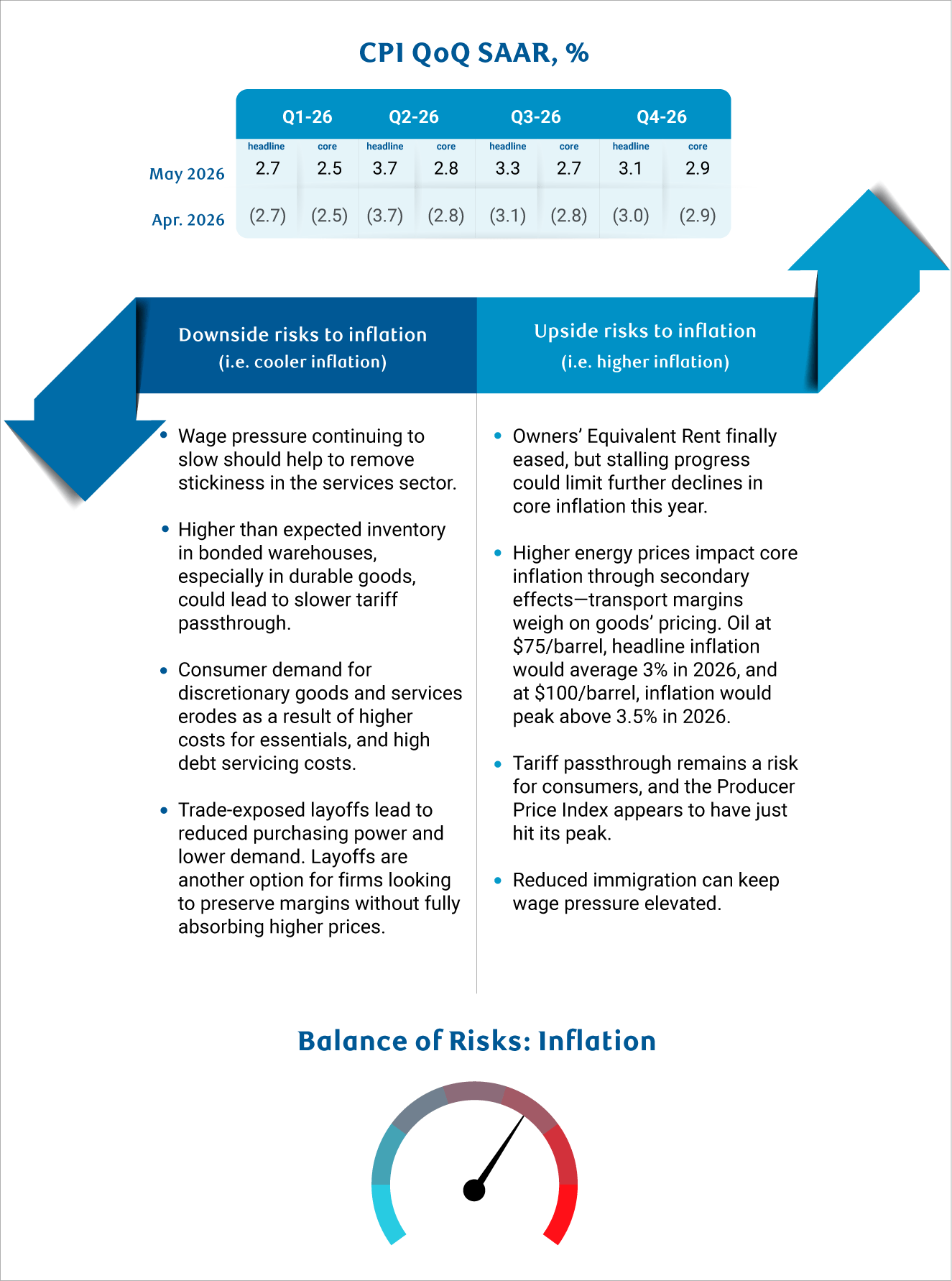

Inflation outlook

Inflation is moving in the wrong direction. Price growth remains fundamentally sticky around 3% with upside risks even after stripping out the impact from the ongoing energy shock.

The commodities shock continues to add to inflationary pressures, but challenges extend beyond oil and fertilizer. For one, now that pre-tariff inventories have been used up, tariffs are showing up more prominently in producer and consumer prices.

Meanwhile, services’ prices are also sticky, supported by a structurally tight labor market. This inflation profile will keep the US Federal Reserve on the sidelines for the rest of 2026 and 2027.

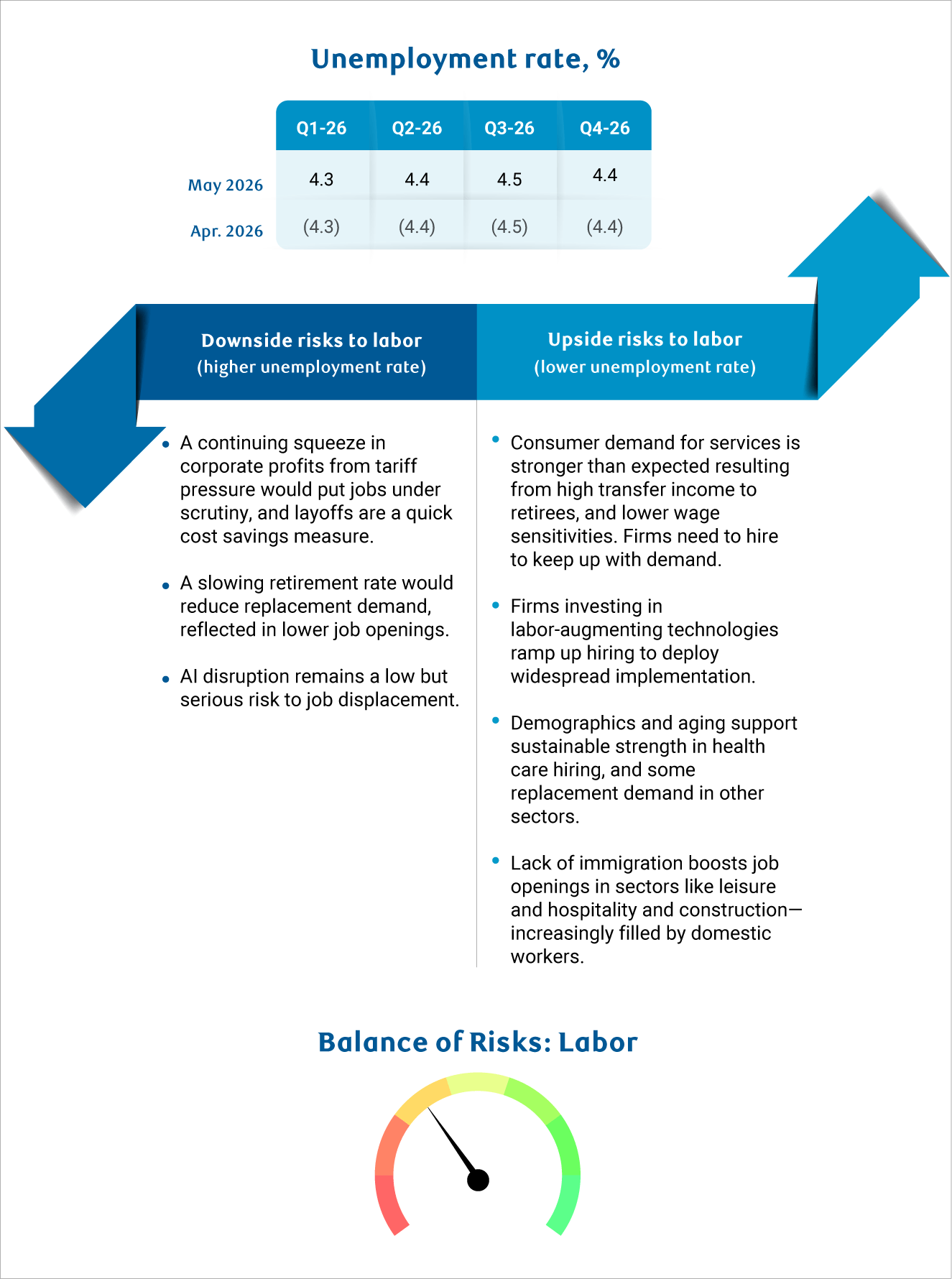

Labor market outlook

The US labor market is stable. Job creation has slowed meaningfully in the past six months, but downward momentum, at least, for now has paused temporarily.

The bulk of job creation, however, remains in health care—a structural trend—while trade-exposed sectors remain soft. At the same time, falling labor supply amid rising retirements means the economy can generate far fewer jobs to keep the unemployment rate stable—perhaps as few as zero a month.

Structurally reduced labor supply should mean there’s a floor under how weak wages can decelerate. But, the recent energy shock has real wages tipping into negative territory, particularly for low-income households.

Indeed, the new measure of the American consumer is no longer whether they have jobs, but if they earn enough from them. We’re still optimistic that the labor market is stable, but the impact of tariff pressures, and rising energy costs suggest risks to our base case forecast remain to the downside.

Download the report

About the Authors:

Frances Donald is the Chief Economist at RBC and oversees a team of leading professionals, who deliver economic analyses and insights to inform RBC clients around the globe. Frances is a key expert on economic issues and is highly sought after by clients, government leaders, policy makers, and media in the US and Canada.

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. Carrie is responsible for projecting key US indicators including GDP, employment, consumer spending and inflation for the US. She also contributes to commentary surrounding the US economic backdrop which she delivers to clients through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.