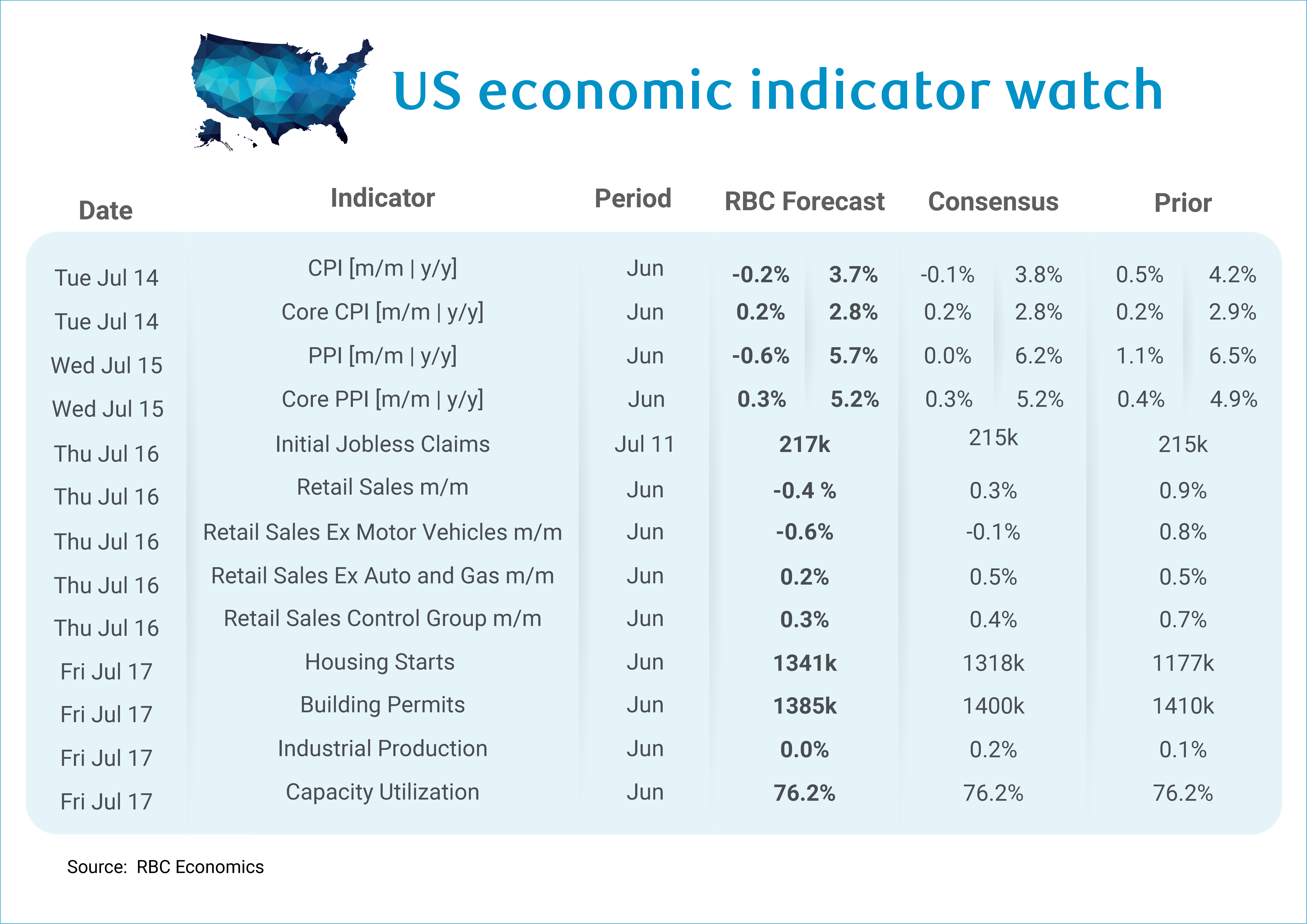

Next week brings several major data releases, with CPI as the focal point. We expect headline CPI fell -0.2% m/m in June, driven by lower gasoline prices following the US-Iran MOU signed in mid-June, bringing the y/y rate to 3.7%. Core CPI likely rose +0.2% m/m, pushing the annual pace to 2.8%.

We look for core goods prices to remain flat on a month-over-month basis, as tariff pressures reverse following the overturn of IEEPA. Still, with sector specific tariffs in place (i.e., section 232), goods including motor vehicle parts and used vehicle prices may show an acceleration, reflected in the recent uptick in the Manheim Used Vehicle Value Index. Within core services, shelter remains a source of pressure — OER and rent have both trended higher since last summer and we don’t expect either will provide relief for the remainder of the year. Additionally, elevated hotel pricing tied to the World Cup has pushed shelter higher. We do expect a reversal in August after the World Cup concludes, but it will hardly be enough to offset the broader rent and housing trends.

We expect June retail sales to show a similar decline in headline reading due to lower gas prices. We expect the fall in gas prices was large enough to pull the headline print negative (-0.4% m/m). Stripping out the impact of gasoline and auto sales, spending likely rose +0.2% m/m. Consumers appear to be losing momentum as the tailwind from tax refunds fades and real wage declines weigh on purchasing power. The retracement in revolving consumer credit in May — the largest improvement in outstanding balances since late 2024 — suggests households prioritized debt repayment over incremental spending, even with relief at the pump. But a strong month of auto sales data suggests the momentum remains for upper income households – we look for auto sales to rise 1.0% m/m, as upper income households continue to account for a growing share of consumer spending.

Aside from CPI and retail sales data, here’s what else we’re watching next week:

-

We forecast headline PPI declined -0.6% m/m in June with lower oil prices providing some relief to businesses. Growth in core PPI is expected to moderate, although our forecast of +0.3% m/m would represent the 10th consecutive monthly rise, as rising input costs reflect higher energy, tariff pressures, and strong AI demand.This is consistent with our view that inflation will remain sticky for the remainder of 2026.

-

Initial jobless claims are expected to show layoffs remain subdued at 217k. The labor force shrank by 720k workers in June, consistent with our view that with labor supply constraints, layoffs will remain muted.

-

Housing starts are expected to come in slightly higher in June (+1341k) after building permits ticked higher in prior months.

-

Building permits for the month of June are expected to point to weaker issuance (+1385k) as higher mortgage rates have limited mortgage applications.

-

We expect to see Industrial Production was flat for the month of June (+0.0% m/m). The ISM manufacturing index pointed to an expansion of activity, but manufacturing hours worked declined in June. On net, we expect the IP metric will remain unchanged, keeping the capacity utilization rate steady at 76.2%.

About the authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. She is responsible for generating RBC’s US economic forecasts across GDP, employment, and inflation, and providing macro commentary through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.