U.S. tariffs looming over Canada’s economy demand an urgent, forceful and strategic response. The next 30 days are critical: Canada must demonstrate to Washington that America’s path to energy and economic security depends on Canada. Especially, Canadian resources.

A focus on key commodities can underpin a broader Canadian industrial resurgence that boosts Canadian GDP, revitalizes technical innovation, attracts foreign and domestic investment in several key areas, enhances productivity and accelerate Indigenous investments in resources. That would make us indispensable to U.S. interests, and a key pillar of its economic and energy strategy.

Focusing on specific commodities can also drive a renaissance in Canada’s manufacturing and ancillary services, and can ensure robust Canadian sustainability policies, such as methane capture and conservation, advance emission reductions across the value chain. In other words, a resource-focused economic strategy need not be a strip-and-ship strategy.

There’s a broader imperative, too: geographic diversification. U.S. tariffs of 25% on all steel and aluminum imports from Canada and other countries highlight the urgency of finding new markets. Resource expansion would further derisk large-scale commodity projects and boost Canadian agriculture, materials and energy exports to Asia and Europe. Over time, this could widen the door to greater trade with many of the world’s largest and fastest-growing countries. Strategically owning parts of the value chain raises our global profile, boosts our leverage in trade negotiations with the U.S. and other partners, and makes us more resilient to shifting geopolitics.

Washington already recognizes Canada’s resource strength. The decision to impose less-punitive 10% tariffs on Canadian energy compared to 25% on other goods was a tacit U.S. acknowledgement of the strategic importance of resources to American interests. We need to seize on that geo-strategic edge and elevate commodities, and their end products, in future trade negotiations with Washington.

Here are three strategic sets of resources Canadian negotiators can focus on to deepen one of the world’s most valuable economic partnerships:

1. Abundant Canadian oil, gas and power can underpin America’s energy ambitions

Canada’s exports of oil, gas, and electricity strengthen U.S. energy reserves, reduce consumer costs, and support American objectives to expand international energy exports to global allies. Deep north-south integration of North American energy infrastructure means efforts to diversify away from Canada would be costly and time-consuming.

Although a net exporter of oil and natural gas, the U.S. is looking to help Europe and allied Asian countries reduce their reliance on less-friendly energy sources, while meeting its growing domestic demand. American reserves are plentiful but energy-intensive data centres to power artificial intelligence, and other technologies, are straining capacity. Stable Canadian energy production can add to U.S. supply through integrated pipelines and grids. That would give the U.S. a cushion to export oil and natural gas to global allies without raising prices at the pump for domestic consumers-a key Trump priority.

![]()

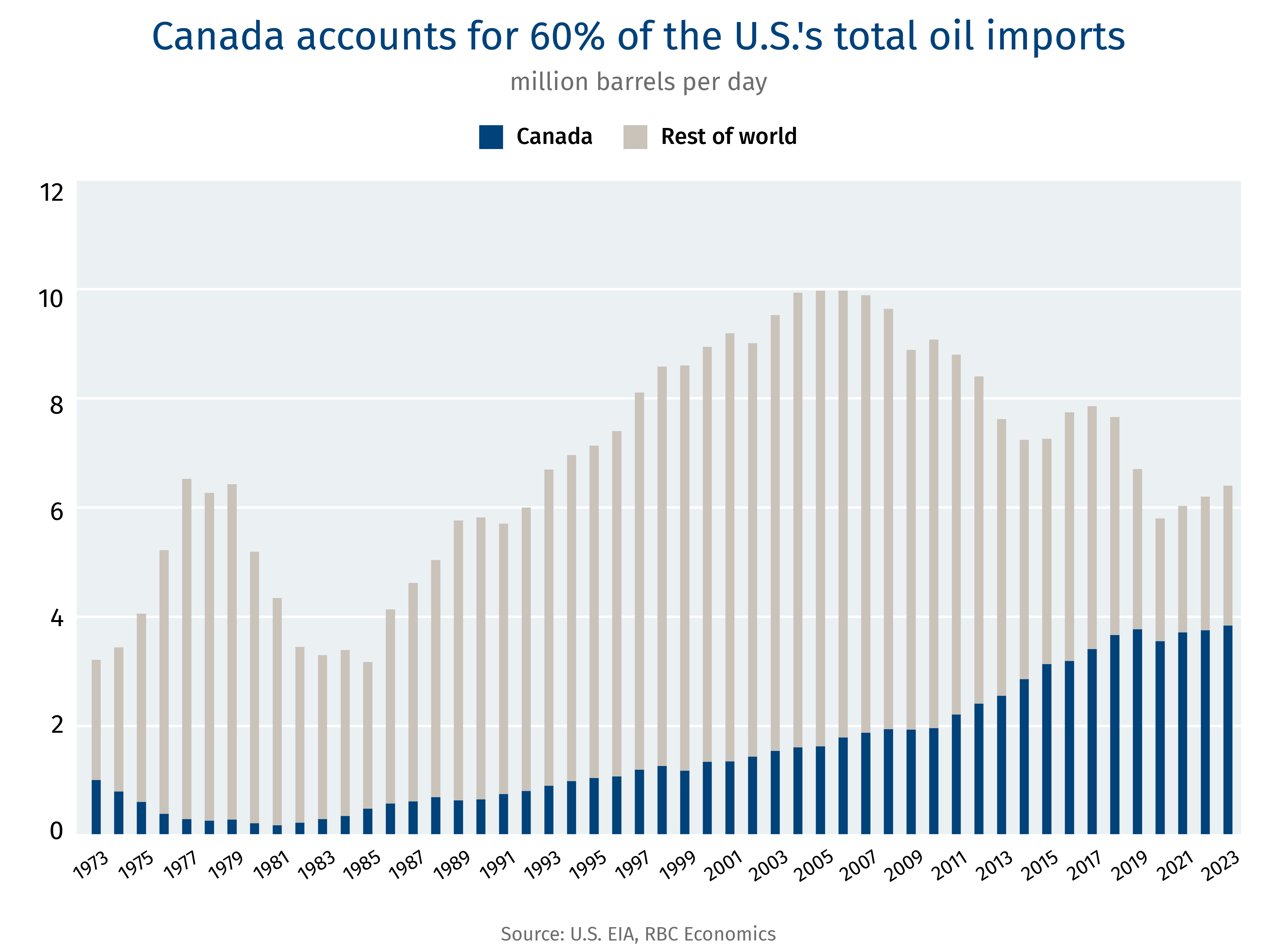

Oil: 60% of U.S. imports1

Canada’s advantage: Canadian oil can backstop U.S. efforts to become the de facto global swing oil supplier.

Canada’s share of U.S. crude oil imports has grown significantly over the past few decades, and now represent 24% of total U.S. oil consumption2. Cross-border pipelines deliver heavy crude directly to U.S. refineries that are specifically designed to process it. For these refineries, particularly those in the Midwest, moving away from Canadian heavy crude would leave them with high retooling costs or dependent on alternative sources such as Venezuela or the Middle East, exposing them to geopolitical risks. Recently, the Trans Mountain pipeline expansion has nearly tripled Canada’s oil shipping capacity to tidewater markets, carving out a role for Canada’s oil in supporting global allies, such as South Korea and Japan.

![]()

Electricity: 90% of U.S. imports3

Canada’s advantage: Low-cost and clean Canadian electricity can power several U.S. efforts including artificial intelligence, advanced manufacturing and advanced technology products.

Although the U.S. generates most of its own electricity, Canadian supplies keep the lights on and costs low across several U.S. states. New projects, such as Hydro-Quebec’s Hertel-New York powerline, aim to further increase electricity exports by providing 20% of New York City’s electricity needs, saving its residents an estimated $17 billion in electricity costs over the next three decades4.

With more than 30 cross-border transmission lines linking Canadian provinces with American states, Canada is essential for ensuring cross-border grid security and a potential source for incremental generation. For example, the rapid growth of AI technology–a U.S. strategic priority–is expected to drive a sharp increase in electricity consumption from U.S. data centres, which is estimated to account for up to 12% of U.S. total consumption by 2028, compared to 4.4% in 20235.

![]()

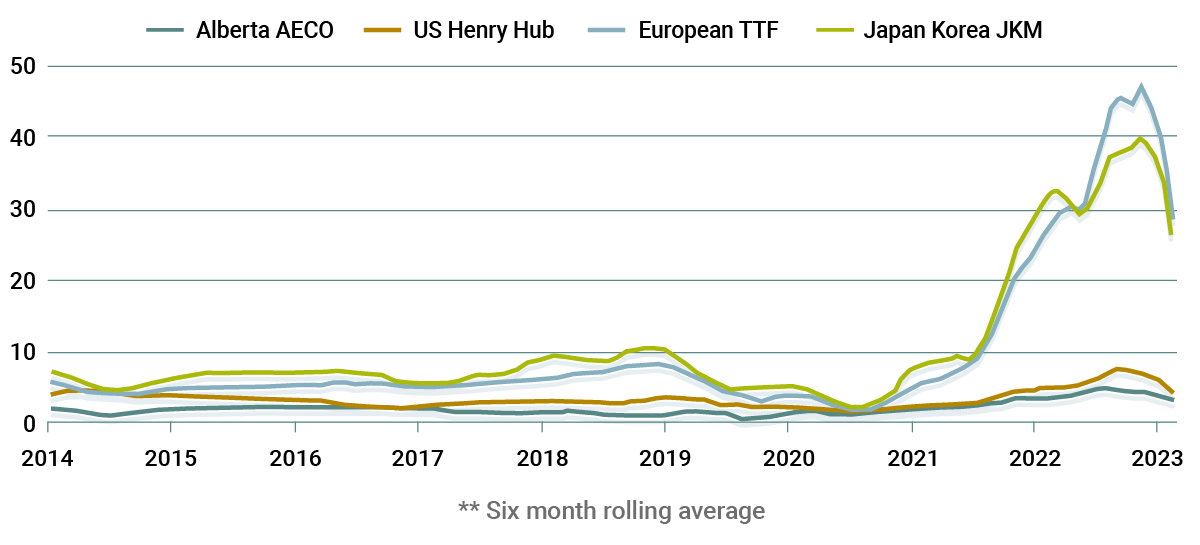

Natural Gas: 99% of U.S. imports

Canada’s advantage: Canadian natural gas can help America ensure ample domestic supplies and room for exports to allies in Europe and Asia.

Higher U.S. natural gas demand is expected to outpace supply growth in the next two years, according to the U.S. Energy Information Association. In addition, demand from data centres and reshoring of manufacturing could further strain natural gas power generation. Canadian natural gas is well positioned to meet supply gaps, and already accounts for 9% of total U.S. natural gas consumption with the capacity to expand further.

Canada is also poised to become a significant supplier of liquefied natural gas (LNG), and is uniquely positioned to export energy to strategic Asian allies. With six West Coast LNG projects proposed and under construction, including LNG Canada Phase I which is set to come online this year, Canada is estimated to have a total export capacity of 6.26 billion cubic feet per day (bcfd). This proposed capacity would put Canada among the top five global LNG exporters at current levels. In addition, West Coast terminals are strategically located just 10 shipping days from Asia, compared to 20 days for U.S. Gulf Coast exporters via the Panama Canal.

2. Canadian agriculture would strengthen American food security

Canada is a major part of the North American breadbasket, providing a stable and reliable supply of agricultural commodities that supplement the United States’ strengths in the sector. As a key provider of essential inputs like potash and seed oils, Canada supports U.S. food and biofuel production. With the U.S. facing potential labour shortages due to a crackdown on illegal immigration, Canada can help supplement this gap in the short term, while adding to continental food security in the long term.

![]()

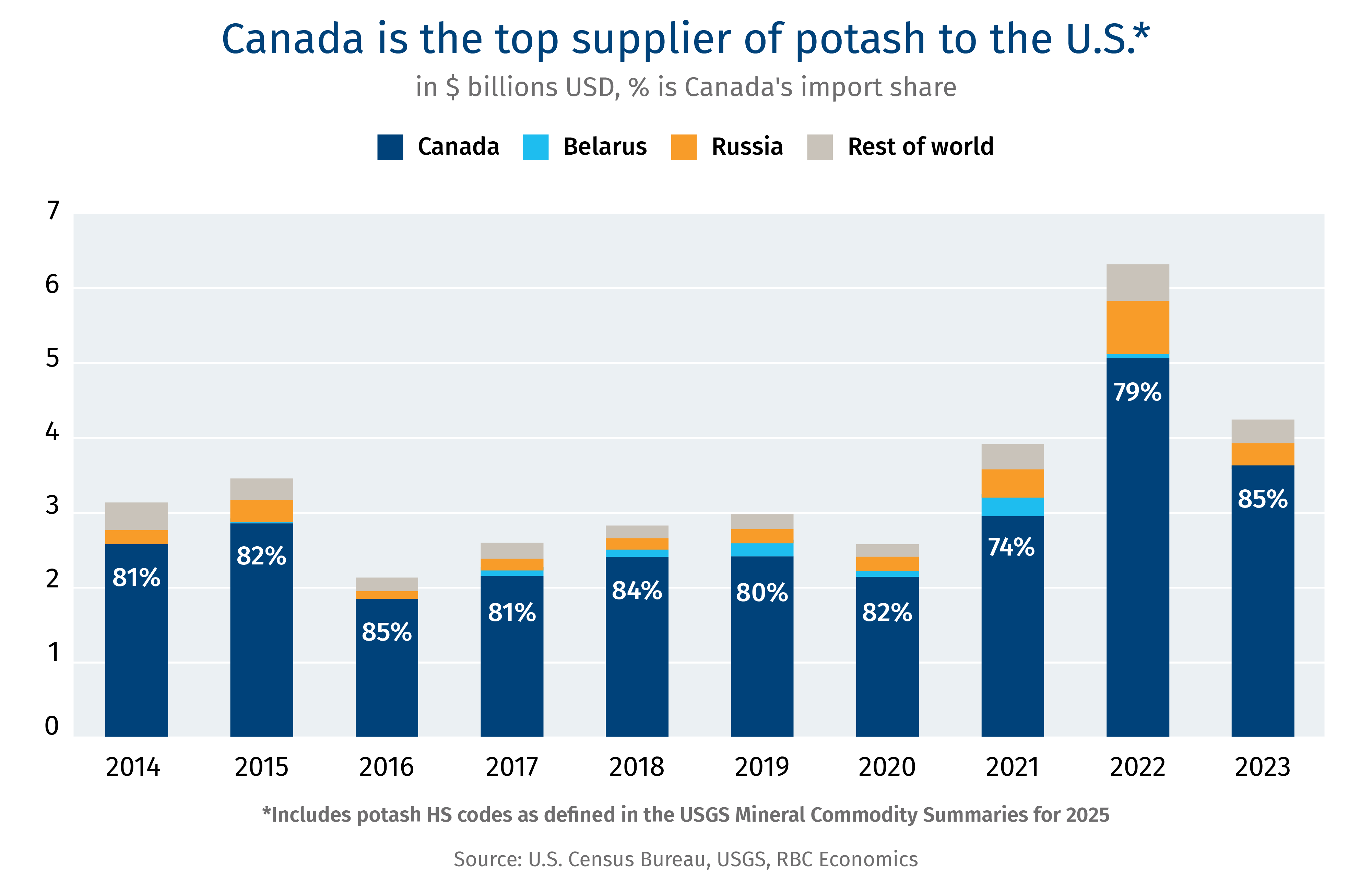

Potash: 85% of U.S. imports

Canada’s advantage: Canadian potash, a critical fertilizer component, can boost American crop yields amid extreme weather patterns, reinforcing continental food security and supply chain stability.

With growing food demand, there’s significant potential to strengthen this partnership. The Jansen potash mine, slated to begin operations in 2026, is projected to boost Canadian potash production by 4.2 million tonnes per year (mtpa), with potential expansion up to 8.5 mtpa by 2029—boosting Canadian capacity by more than a third. The new project would raise Canada’s global market share to nearly 40% by 2026. The increased production will not only bolster American food security but also help displace potash exports from non-aligned nations such as Russia and Belarus.

![]()

Canola oil: 98% of U.S. imports6

Canada’s advantage: Canola, a product developed in Canada, can play a key role in U.S. food security and meeting biofuel demand.

Canada provides a stable and diverse supply of agricultural products to the U.S., second only to Mexico. The U.S. is heavily reliant on Canadian canola oil, which account for 98% of its total imports, and is a key input in U.S. food production and renewable fuels.

Canada is also the top U.S. import source for cereal products, underpinning the deeply integrated cross-border supply chain in these sectors.

![]()

Meat: 34% of U.S. imports

Canada’s advantage: Canadian meat, including bovines and swine, are an important part of the meat feedstock into the U.S.

Animal proteins will continue to play a significant role in American diets, with per capita consumption in the U.S. projected to increase from 68.7 kilograms in 2023 to 74.6 kilograms by 20288. Canadian meat producers are essential in meeting this rising demand, as the U.S. already imports 33% of its beef and 66% of its pork from Canada7. The strong integration between Canadian and American meat markets is driven by high safety standards, a similar market structure, and alignment on product quality. As a result, Canadian meat not only supports U.S. domestic consumption but also contributes to American meat exports to global markets.

3. Canadian critical minerals and uranium can power advanced technologies in North America

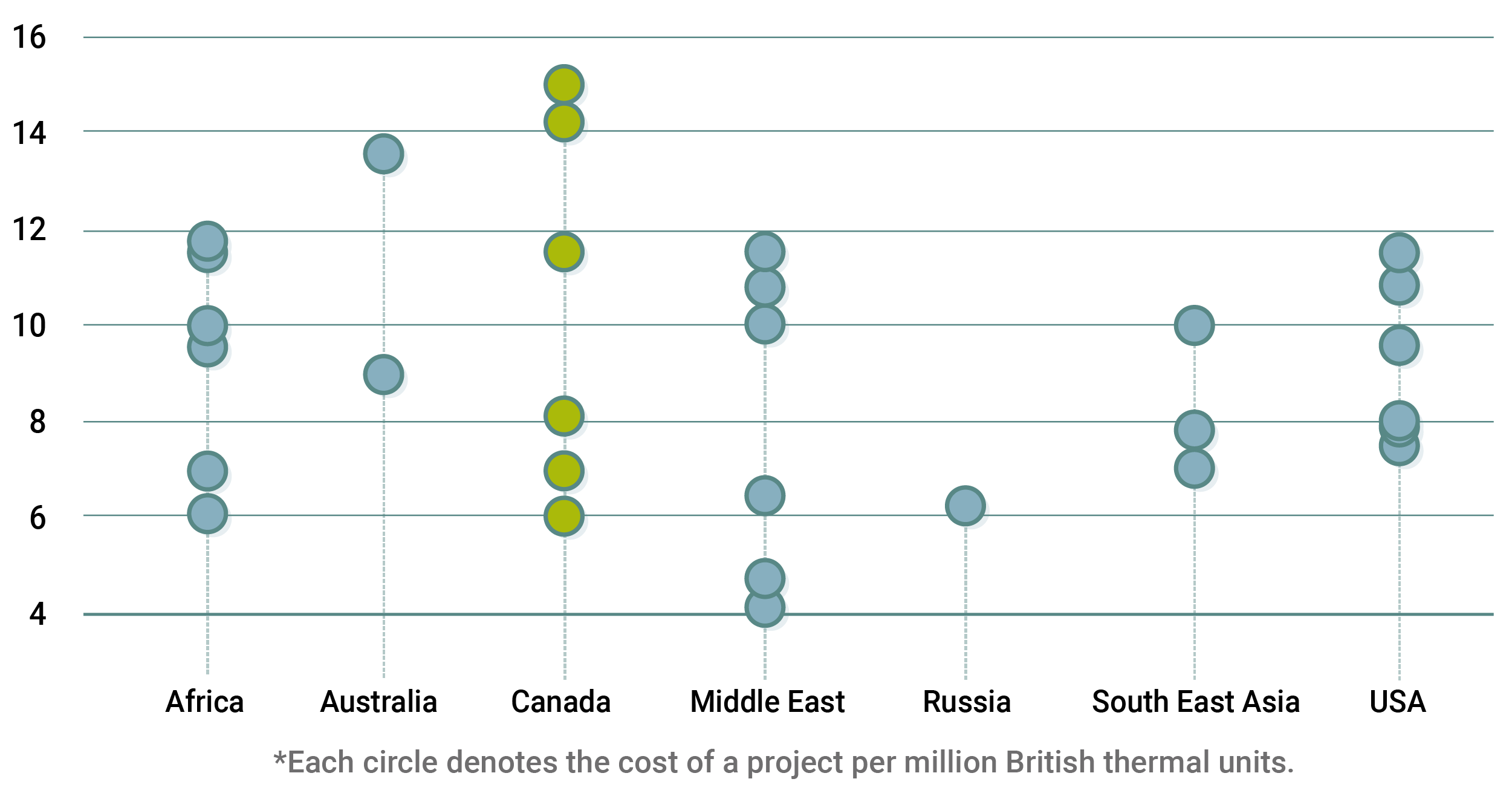

The U.S. has reserves of many of the critical minerals needed in semiconductors and other sensitive technologies. Its uranium reserves are also able to help build out a new wave of nuclear power projects. It’s aiming to mine and enrich as much as possible within its borders to displace supplies from China and Russia but faces constraints, especially in adding enrichment capability. Canada has capacity in key complementary areas, like uranium conversion, that can help the U.S. build out an efficient North American value chain.

![]()

Critical minerals: 19% of U.S. imports, in total minerals and metals9

Canada’s advantage: With the right investments and innovation, Canada can advance production of several critical minerals.

The new U.S. administration is looking to accelerate several critical mineral projects and considering opportunities to advance activity within the Quadrilateral Security Dialogue, comprising the U.S., India, Japan, and Australia. Although outside this alliance, Canada is a player in the critical minerals space. It is a top 10 global producer and already a major supplier to the U.S. for aluminum, iron, steel, copper, nickel and more.

Canada has been working toward U.S. efforts to reduce reliance on China, from establishing a Canada-U.S. Joint Act Plan on Critical Minerals to $3.8 billion in public investments to ramping up exports to the U.S. of gallium and germanium, both impacted by Chinese export controls. Canada’s existing extraction and processing infrastructure could further fill U.S. gaps in key areas, such as aluminum, nickel and zinc.

![]()

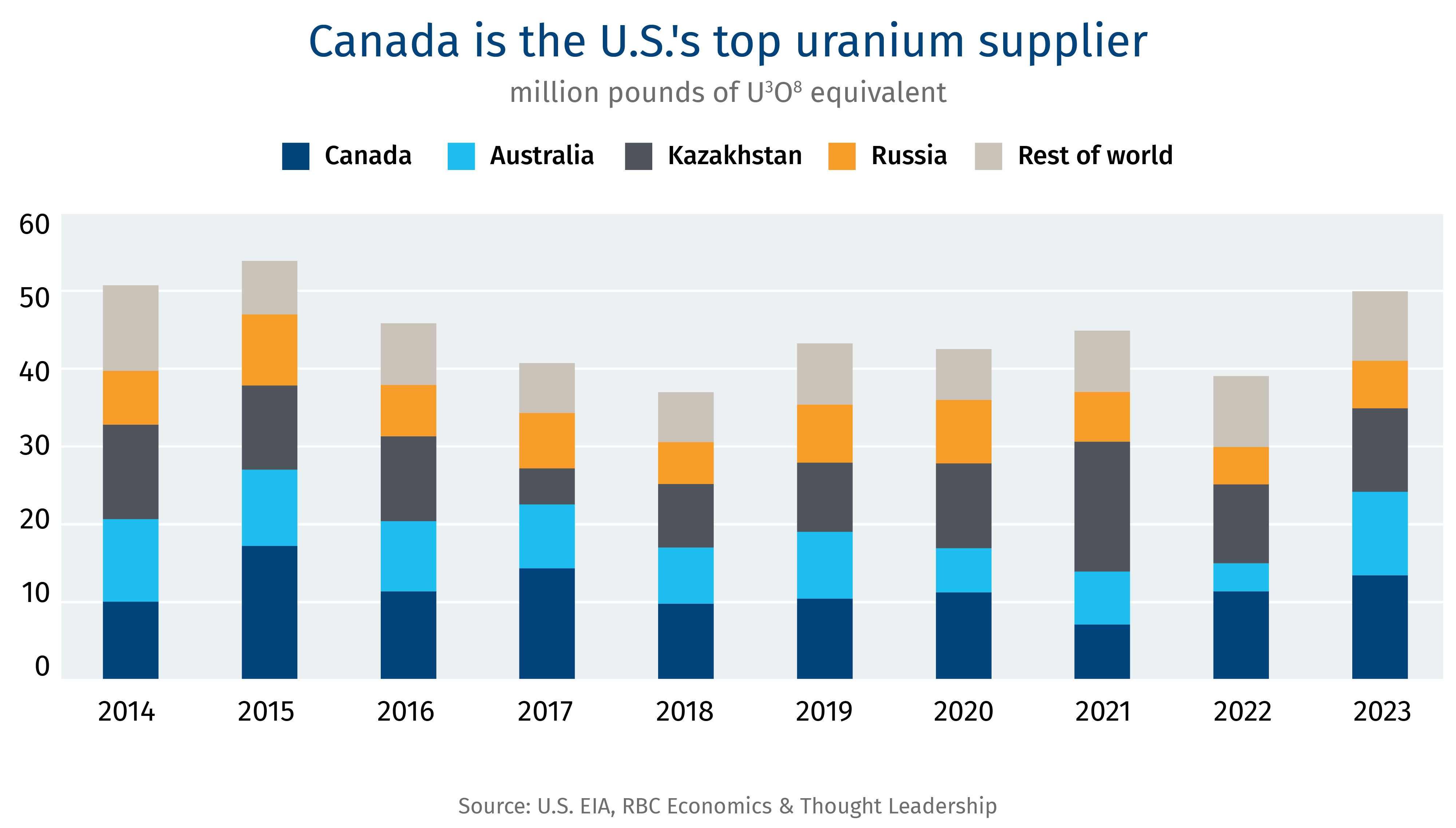

Uranium and nuclear expertise: 27% of U.S. imports, in uranium

Canada’s advantage: America’s path to nuclear renaissance goes through Canada—the world’s second largest producer of uranium after Kazakhstan.

The energy source is increasingly important to meet growing electricity demand to power AI data centres and other energy-intensive strategic advanced technologies. As the largest uranium supplier to the U.S., Canada can be an important part of the continental nuclear fuel cycle with world-leading technology and talent, small modular reactors (SMRs), and an 89,000-strong nuclear workforce honed through work on CANDU projects.

What Canada can deliver in advancing U.S. interests

In the short-term, there’s an urgent need for Canada to realign our economic interests with the U.S. For its part, the U.S. can go it alone, but it’s going to be a harder, costlier and longer route to self-sufficiency. A shifting economic and geopolitical environment behooves both to collaborate in the three core areas of mutual benefit.

This strategy heavily depends on the U.S. getting on board. We have a short window to convince Washington about the need to collaborate in the resource and energy space, which has been weaponized by several non-allied actors.

Canada also needs to get its own house in order.

A resource-focused economic and trade strategy would require billions of dollars in new infrastructure, including rail lines, seaports and processing facilities. However, domestic and foreign capital will only come to the table If there’s a stable regulatory environment and reliable pricing in what can be highly volatile markets.

These are not new challenges for Canada. Regulatory and policy uncertainty have hobbled economic development for decades. So, too, has lack of reliable demand from our major trading partners, including the U.S.

Resource production and processing calls for longer-term thinking, which will require the federal and provincial governments to work together to create entities, and strengthen existing ones, to attract and retain capital, and protect against extreme price volatility. We will also need to ensure our education systems are geared towards attracting the right talent and skills to ensure the economy is poised for long-term growth. And while positioning Canadian resources anew in the U.S. market, we will need to improve our trading relationships with many other countries and regions.

All this will require a different mindset among Canadians, to ensure our natural resources are not seen as a trading card with the U.S., but rather a strategic platform for growth, and prosperity, for decades to come.

It can be Canada’s greatest resource play.

Contributors:

Salim Zanzana, Economist, RBC Economics

Varun Srivatsan, Director of Policy, RBC Thought Leadership

Cynthia Leach, Assistant Chief Economist, RBC Economics

Yadullah Hussain, Managing Editor

Caprice Biasoni, Graphic Design Specialist

Shiplu Talukder, Digital Publishing Specialist

For more, go to rbc.com/tradehub.

Download the PDF

- All U.S. import shares from 2023 unless otherwise indicated.

- Natural Resources Canada “Energy Factbook 2024-2025”

- Average last 5 years as 2023 figure distorted due to droughts affecting Canadian generation and export capacity.

- 2024 Fall Economic Statement

- U.S. Department of Energy “Evaluating the Increase in Electricity Demand from Data Centers”

- Includes imports of products under HS code 1514 in 2023

- Agriculture and Agri-Food Canada “Sector Trend Analysis – Meat Trends in the United States”

- Includes products under HS codes 0201 and 0202 for beef and 0203 for pork in 2023

- United States International Trade Commission

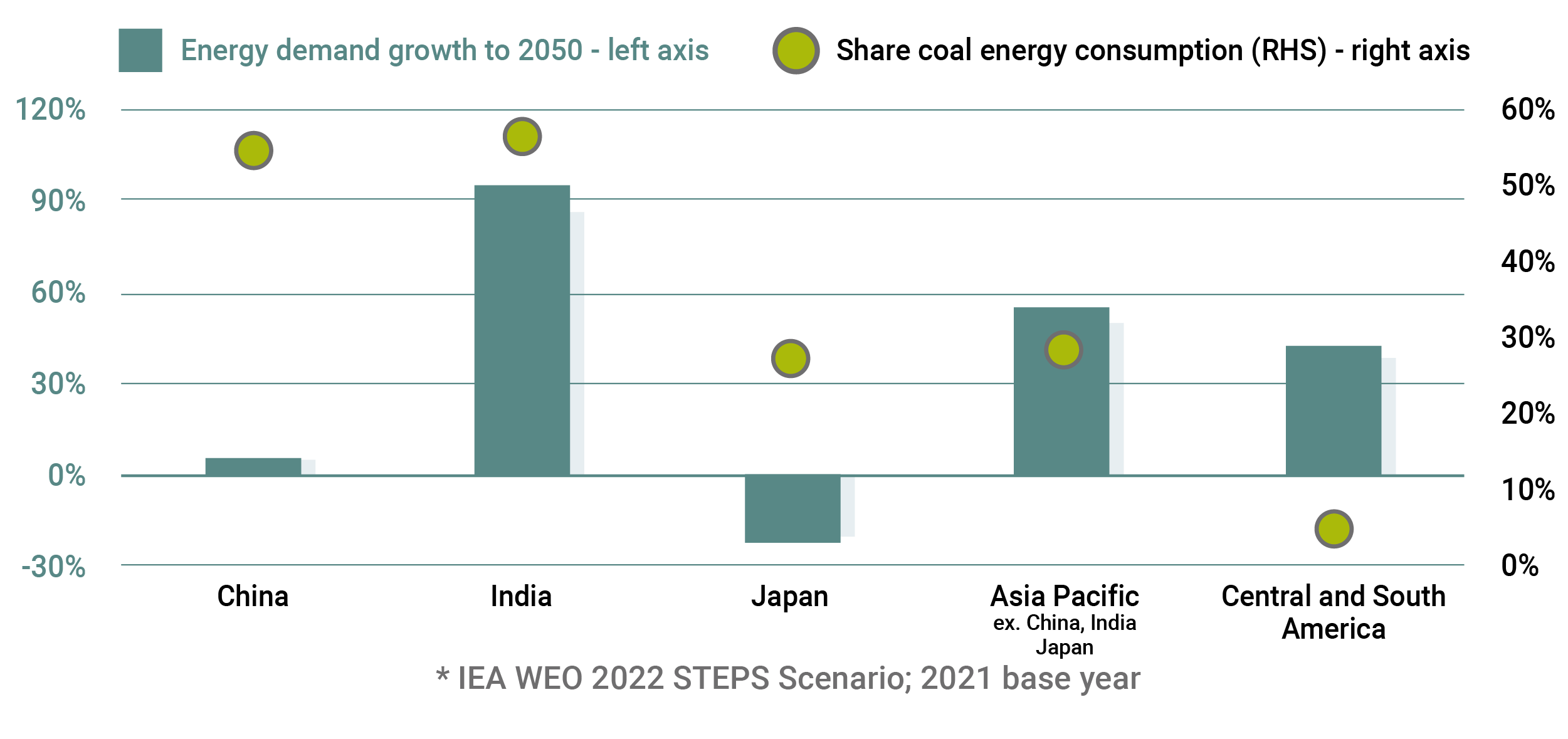

Asia, on the other hand, will have a harder time turning away from natural gas. As one of the world’s biggest LNG importers, Japan is alarmed by its dependence on Russian and Middle Eastern countries as well as new export limits proposed by major LNG supplier Australia. It’s encouraging the development of nuclear energy, hydrogen and natural gas as part of this year’s G7 agenda.

LNG will also remain an essential fuel in China, India and other populous countries of South Asia and Southeast Asia as these countries seek to meet growing energy demand while reducing a strong reliance on coal to meet climate commitments. China, India and Southeast Asia will see gas demand grow by around 44% by 2050 in the International Energy Agency’s base case scenario. LNG would take the bulk of the growth with declining local pipeline-based production.

But it’s hardly a full-blown bull case for gas. Stunned by last year’s five-fold jump in LNG prices, many Asian countries raised their coal consumption, while others pivoted to renewables, especially as the economics of switching directly from coal to clean energy in Asia improved dramatically. Non-emitting energy rollout may take a while to gain traction in Asia, but it’s still a cloud hanging over the long-term gas outlook.

Asia, on the other hand, will have a harder time turning away from natural gas. As one of the world’s biggest LNG importers, Japan is alarmed by its dependence on Russian and Middle Eastern countries as well as new export limits proposed by major LNG supplier Australia. It’s encouraging the development of nuclear energy, hydrogen and natural gas as part of this year’s G7 agenda.

LNG will also remain an essential fuel in China, India and other populous countries of South Asia and Southeast Asia as these countries seek to meet growing energy demand while reducing a strong reliance on coal to meet climate commitments. China, India and Southeast Asia will see gas demand grow by around 44% by 2050 in the International Energy Agency’s base case scenario. LNG would take the bulk of the growth with declining local pipeline-based production.

But it’s hardly a full-blown bull case for gas. Stunned by last year’s five-fold jump in LNG prices, many Asian countries raised their coal consumption, while others pivoted to renewables, especially as the economics of switching directly from coal to clean energy in Asia improved dramatically. Non-emitting energy rollout may take a while to gain traction in Asia, but it’s still a cloud hanging over the long-term gas outlook.