Donald Trump has set out to remake the global trading order, and with it America’s relationship with the global economy. Unsettling as that is, it’s neither new nor sudden. Trade reform has been a dominant part of American political thinking since the collapse of the Berlin Wall and, with it, the end of a Communist counterweight to global capitalism. While resistance can be traced back to the early days of NAFTA, the fragility of America’s trade confidence really rose to the fore during the Global Financial Crisis and in the years that followed as China grew emboldened with its claim for great power status.

Brick by brick, it’s now orchestrating the dismantling of another dominant structure of the 20th century—the supporting wall of a global economy, one that relies on American military protection, legal principles, and monetary policy. The emerging trade war of 2025 is as much about Pax Americana Oeconomia as anything else and is quickly threatening to create a wholesale break in that support, equal in consequence perhaps to that moment in 1989. It’s why some Trump advisers have called this moment one of “generational change” in trade.

The shape of the global economy, and its direction heading to the 2030s, is in play, and few countries have as much at stake as Canada—because few countries benefitted as much from that trading era that may now be in its twilight. Each country is each other’s largest customer, with over 75 percent of Canadian exports going to the U.S. and 17.3 percent of American goods exports destined for Canada. The two-way trade is more than commercial; the two neighbours have come to rely on each other for energy and food security, military security, and economic security, through aligned standards and principles for everything from car parts and aeronautics to telecom protocols and computing principles.

For Canada to navigate this new age of disruptive economics, in which those long-term understandings may now be at the perpetual whim of political capriciousness and mercantile mindsets, a more strategic approach will be needed. Yes, our future will be more beholden to tariffs and tirades—but beyond those moments, it will be shaped in more lasting ways by our understanding of America’s fundamental challenges, and whether we can help address them, to ensure the generational change helps us regenerate our economy. Among those challenges:

It’s security, stupid

The Trump economic agenda is about security more than prosperity. It’s why security and trade policies are more intertwined than we’ve seen in decades, even though the U.S., remarkably, has not fought a war over trade interests since becoming the world’s dominant economy. The tariff threats are not so much a shakedown, to gain advantage in bilateral and multilateral deals; they’re aligned with an American First view of the world. We can expect, in the coming years, to see the U.S. pull back to this hemisphere, in military and trade engagement. That is, unless and until U.S. economic interests come under threat. This new imperative will require Canada to play a greater role in policing global trade

The world is no longer flat

Successive U.S. Administrations have undermined the World Trade Organization enough to make it largely insignificant to major trade considerations. Trump is now out to remake the broader system, targetting the preferential tariff regime that the U.S. created, coming out of the Cold War, to stimulate growth in allied and developing economies. The U.S. effective tariff rate, at about 3 percent, is the lowest among major economies. The European Union’s effective rate on imports is 5 percent; China’s is 10 percent; Bangladesh’s is 155 percent, the world’s highest. The resulting re-orientation of global trade will complicate Canada’s ambitions to diversify exports.

King Dollar is dead? Long live King Dollar

Underlying America’s trade imbalances is its very awkward position as a backstop for the global economy. The U.S. dollar, as the reserve currency, continues to pull capital to the U.S., in turn making its exports less competitive. The dollar’s strength, in turn, makes its cost of borrowing cheaper than it should be—enabling a credit binge for governments and consumers, and permitting a series of administrations to run fiscal deficits that do little to make America competitive again. As the world’s leading economy became a consumption machine, it relied ever more on imports and the ever-growing need to find cheaper imports, so as not to fuel inflation. Canada will need to join others in helping to rebalance global currencies.

Many have suggested the need for a new version of the Plaza Accord—the 1988 agreement, following a stock market crash the previous year, that helped reset the dollar against other major currencies. That would be much harder today, given the dollar’s dominance over all other currencies, accounting for roughly 60 percent of the world’s $12 trillion in foreign exchange reserves. Moreover, since 1988, the U.S. debt, as a share of GDP, has tripled. The best hope may be a long-term transition that incents America’s leading trade partners, including Canada, to share some of the hidden costs of a reserve currency.

These are some of the strategic pressures the U.S. is facing, and integrating in its approach to trade. It needs others to help police global commerce, including shipping lanes. It needs others to increase its imports of American goods, including energy. And it needs others to help destress long-term pressures on the U.S. dollar and even pay part of the cost of running a reserve currency (through tighter fiscal or monetary policy).

With these major forces at play, we can expect the U.S. to continue to push for trade reforms, perhaps radically so.

What it means for Canada

A headline tariff rate of 25 percent is unlikely, given the blowback that would cause to the U.S. economy and consumers. But its potential impact should not be lost on Canadians: according to RBC Economics, such a tariff hit would cause unemployment to rise above 8 pecent, cut GDP growth in half this year, and add 2.5 percent to consumer price increases. It would also cost U.S. consumers, on average, $1,200 USD a year.

Such modelling is a challenge in that tariffs are never applied in isolation. Also to consider is the likelihood of counter-tariffs, and worse, escalation, as well as the impact on the Canadian dollar. A further factor is the ability of firms to absorb the cost of tariffs, through efficiencies and margin compression. Many Canadian firms have hinted they can absorb a 10 percent tariff, by dividing the cost roughly in thirds—for consumers, intermediaries, and their own profits. In fact, Canadian profit margins have reached relatively high levels, in part because of the 70-cent dollar along with capacity challenges in the U.S., including labour shortages.

But that’s just one measure, by the standard of profit-and-loss statements. The unpredictable trade policies of the Trump administration also create an insidious tax on investment confidence. The Economic Policy Uncertainty Index for Canada has increased to its highest level ever—four times higher than its 20-year average, and well above where it was during the COVID pandemic. Merger and acquisition activity has also slowed, as have investment intentions in machinery and equipment. There is an additional negative effect emerging as firms stockpile inputs and exported outputs ahead of any anticipated tariffs and non-tariff barriers. We saw signs of this in January, as manufacturers hurried to get products across the border, even at a cost of greater inventory management.

That reaction—or pre-emptive action—could lead to an industrial slowdown in subsequent quarters. Add to that an expected decline in consumer confidence, as Canadians read of projected job losses, company closures, and needs for government support, which could lead to interest rate cuts.

In that mix, the Bank of Canada faces a dilemma as difficult as it saw during the pandemic when the supply side of the economy was shut down. Tariffs can simultaneously slow economic growth and increase prices. Deciding whether to adjust interest rates will depend on which effect—inflationary or deflationary—proves more dominant. And as was true in the pandemic, much of that will depend on innovation and the creativity of firms to manage the shock, which we tend to see only in hindsight.

Finally, and equally challenging for the Bank of Canada, there will likely be significant federal and provincial supports for affected businesses and workers, including subsidies and tax relief. This will be politically necessary and economically risky, as it could strain public finances, influence Canada’s credit rating, and prove pro-cyclical if it coincides with interest rate cuts.

How to navigate the uncertainty

While the exact impact of tariffs on the Canadian economy remains uncertain, we know from past experiences and economic fundamentals how such trade disruptions might further unfold.

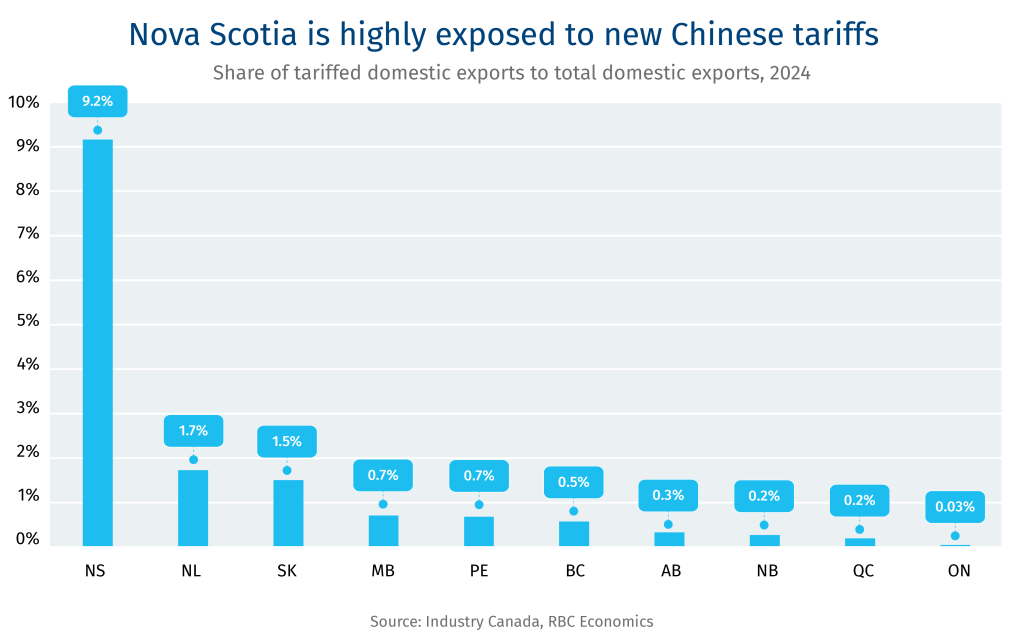

The first thing to recognize is that trade-sensitive industries will be most vulnerable. Tariffs function as taxes on the movement of goods, not on production. Therefore, industries that rely heavily on cross-border trade—such as automotive manufacturing—face the greatest risk. Decades of free trade have led to deeply integrated supply chains, where goods cross borders multiple times at different stages of production. This means that tariffs can apply multiple times within the same production cycle, compounding costs. The auto industry is most typically cited, but there are similar examples in most sectors: Maine lobsters, for instance, are sent to Canada for processing and then returned to the U.S. market. Overall, more than 60 percent of Canada’s manufacturing sector has trade flows with the U.S. that are at least twice the size of their domestic production.

In addition, even if Canada does not impose retaliatory tariffs, U.S. tariffs alone can indirectly harm Canadian businesses. Because of the tight integration between U.S., Canadian, and Mexican manufacturing sectors, tariffs on U.S. industrial imports will drive up costs for U.S. exporters. This, in turn, raises the price of goods that Canada imports from the U.S., creating an inflationary effect. The OECD estimates that a significant portion of U.S. imports are actually American-made goods that were exported for processing and later re-imported. The result is that North American manufacturing supply chains suffer more from tariffs than those in Asia or Europe.

A clear target for Trump is steel and aluminum, in part because of his stated belief that “if you don’t have steel, you don’t have a country.” The U.S. accounts for over 90 percent of Canadian steel and aluminum exports, meaning these tariffs directly impact nearly $24 billion worth of Canadian goods. However, the trade relationship is deeply intertwined—Canada is also the largest supplier of these metals to the U.S., making up about 20 percent of American steel imports and 50 percent of aluminum imports. In 2024, U.S. steel imports from Canada totaled $7.5 billion, while aluminum imports reached $9.4 billion.

While Canada maintains a trade surplus in these industries—$14 billion in 2024, with $11 billion from aluminum—their overall contribution to the national economy remains relatively small. Steel and aluminum represent just 0.5 percent of Canada’s GDP and jobs and about 3 percent of total exports. Quebec and Ontario are the most affected provinces, where these sectors account for 1 percent and 0.6 percent of GDP, respectively.

The U.S. market also has limited alternatives to replace these goods. The 2018-19 tariff experience demonstrated that U.S. producers struggle to replace Canadian steel and aluminum. Most alternative suppliers also face tariffs and production capacity cannot be expanded quickly. Many specialized products are difficult to substitute, forcing U.S. importers to absorb higher costs. Interestingly, despite the 2018 tariffs, U.S. imports of steel products increased, with Canada, Mexico, and Europe slightly growing their market share. In Canada, employment in steel and aluminum industries grew by 4 percent in 2018 and 6 percent in 2019. Meanwhile, U.S. steel and aluminum production capacity actually declined over the tariff period.

What Canada can do

In the near term, Canada may find itself in a tariff brawl, absorbing and delivering blows with our biggest trading partner. We need to think longer-term, too, simultaneously investing in our own trade diversification while exploring ways to help the U.S. address its secular economic challenges. In the long run, those will be our challenges, too.

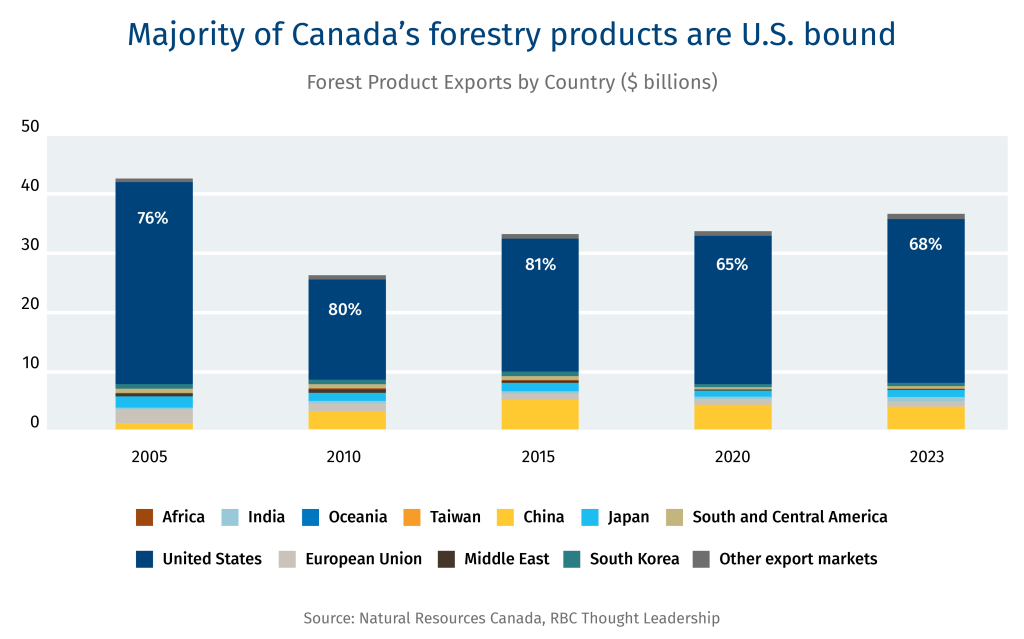

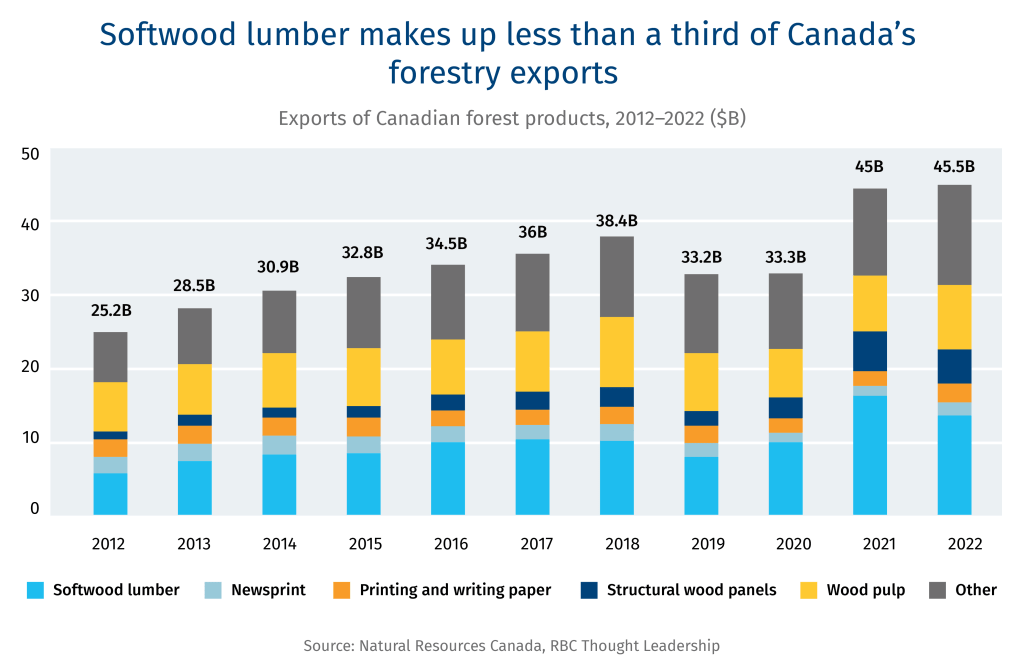

We can start with our natural resources, not only because Trump has cited them as targets. Canada must continue to highlight its critical role in U.S. energy and economic security, emphasizing its resource wealth with the goal of avoiding American trade threats.

In addition, a focus within Canada on developing key commodities can drive industrial growth, boost GDP, attract investment, and advance Indigenous participation, making Canada further indispensable to U.S. interests. Geographic diversification of Canadian resource exports is also essential, as expanding trade beyond the U.S. mitigates risk. Washington already acknowledges Canada’s resource importance, offering a negotiating advantage. By prioritizing energy, agriculture, and critical minerals, Canada can strengthen its position as a key partner in global trade and U.S. economic stability.

Consider just how important these commodities are to the American economy.

Canada’s oil, natural gas, and electricity exports play a crucial role in stabilizing U.S. energy reserves. Integrated pipelines and cross-border electricity grids facilitate a seamless supply of energy, while expansions such as the Trans Mountain pipeline allow Canada to increase its capacity to serve both the U.S. and international markets.

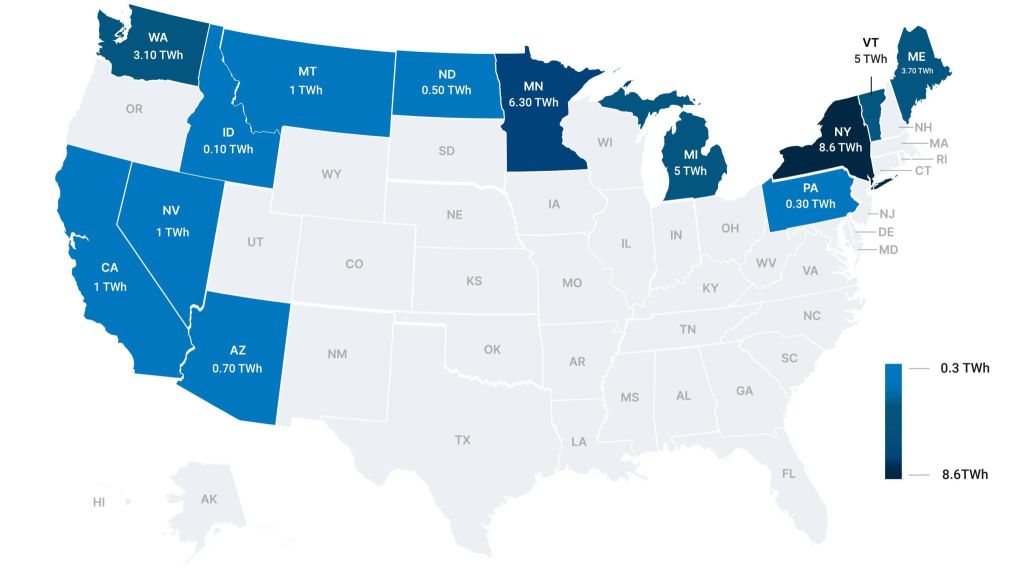

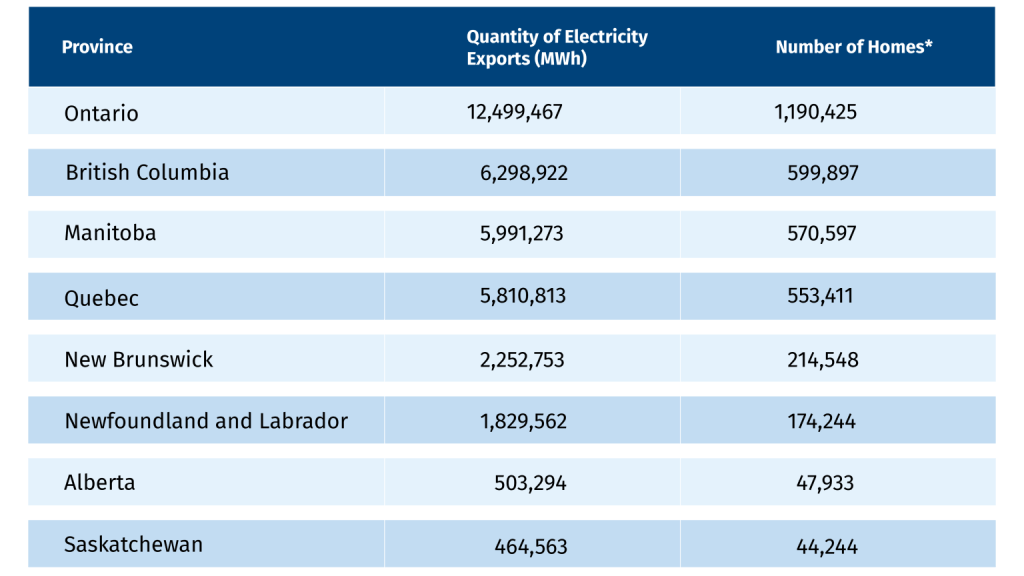

Canada supplies 60 percent of U.S. oil imports, particularly heavy crude oil that is vital for U.S. refineries. Without Canadian crude, U.S. refineries would face expensive retooling or become reliant on riskier suppliers like Venezuela and the Middle East. Similarly, Canada provides 90 percent of U.S. electricity imports, offering a low-cost and clean energy alternative that supports high-tech industries such as artificial intelligence and advanced manufacturing. Additionally, Canada supplies 99 percent of U.S. natural gas imports, which are essential to meet growing U.S. energy demands, particularly as domestic production struggles to keep pace.

Canada is also a vital contributor to U.S. food security, providing key agricultural commodities that support American food production and biofuel industries. With the U.S. facing potential labour shortages due to immigration policies, Canada’s role in supplementing the North American food supply will become even more critical.

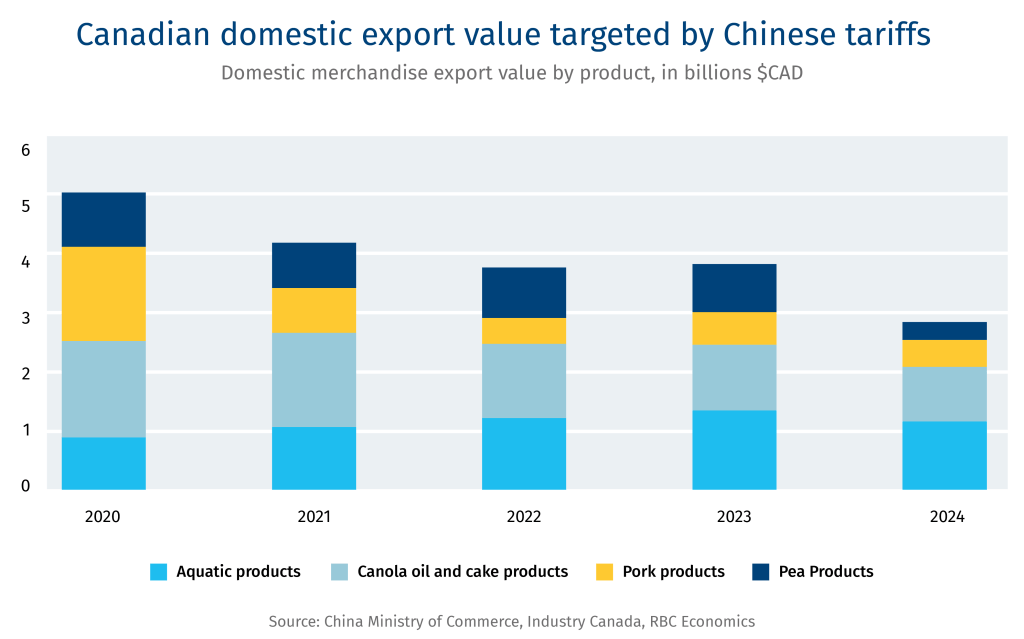

Canada supplies 98 percent of U.S. canola oil imports, a crucial ingredient in both food processing and biofuel production. Additionally, the U.S. imports 34 percent of its meat from Canada, particularly beef and pork, which are deeply integrated into North American supply chains. Furthermore, Canada provides 85 percent of U.S. potash imports, a critical component in fertilizer that supports crop yields, especially in the face of climate-related agricultural challenges.

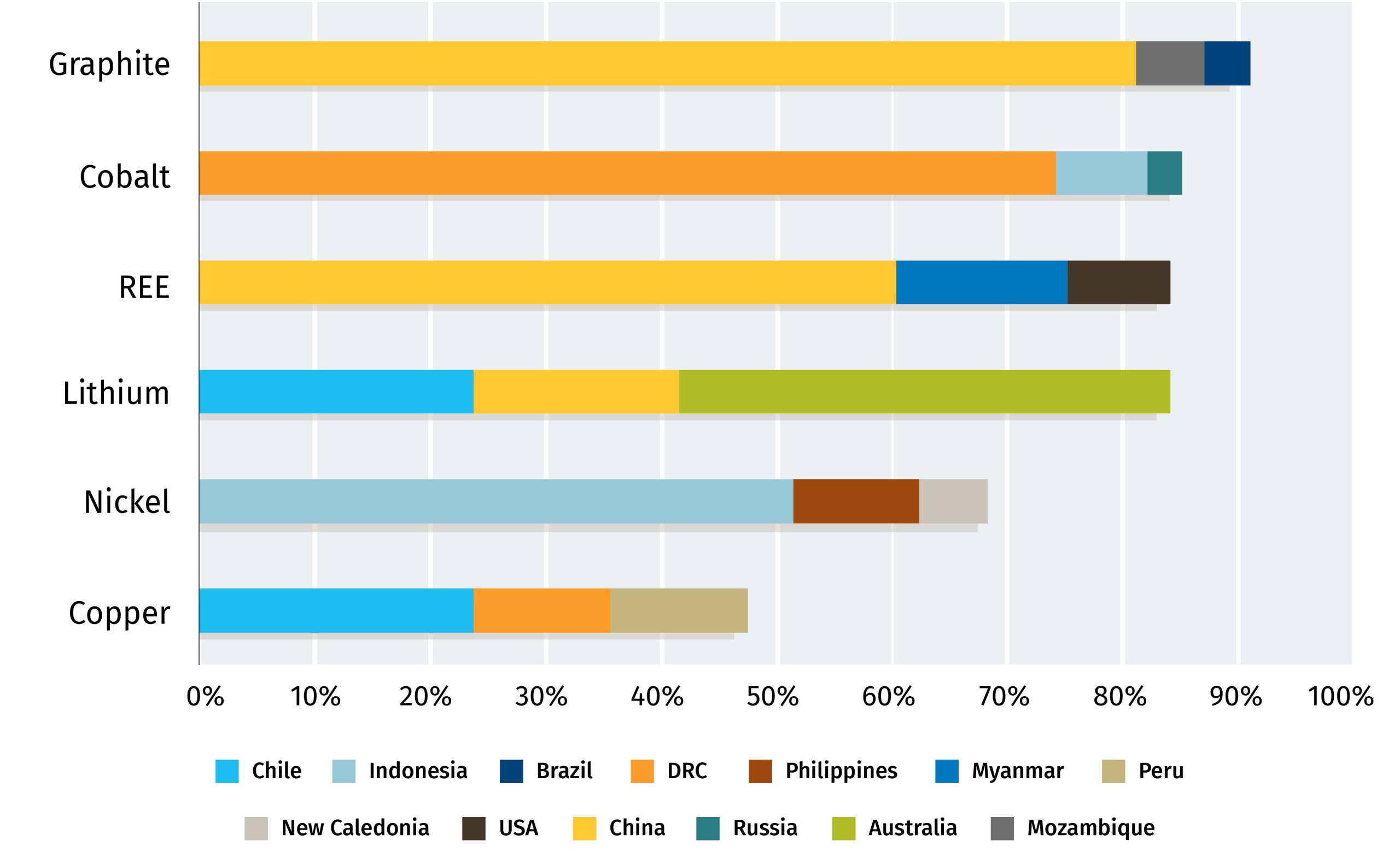

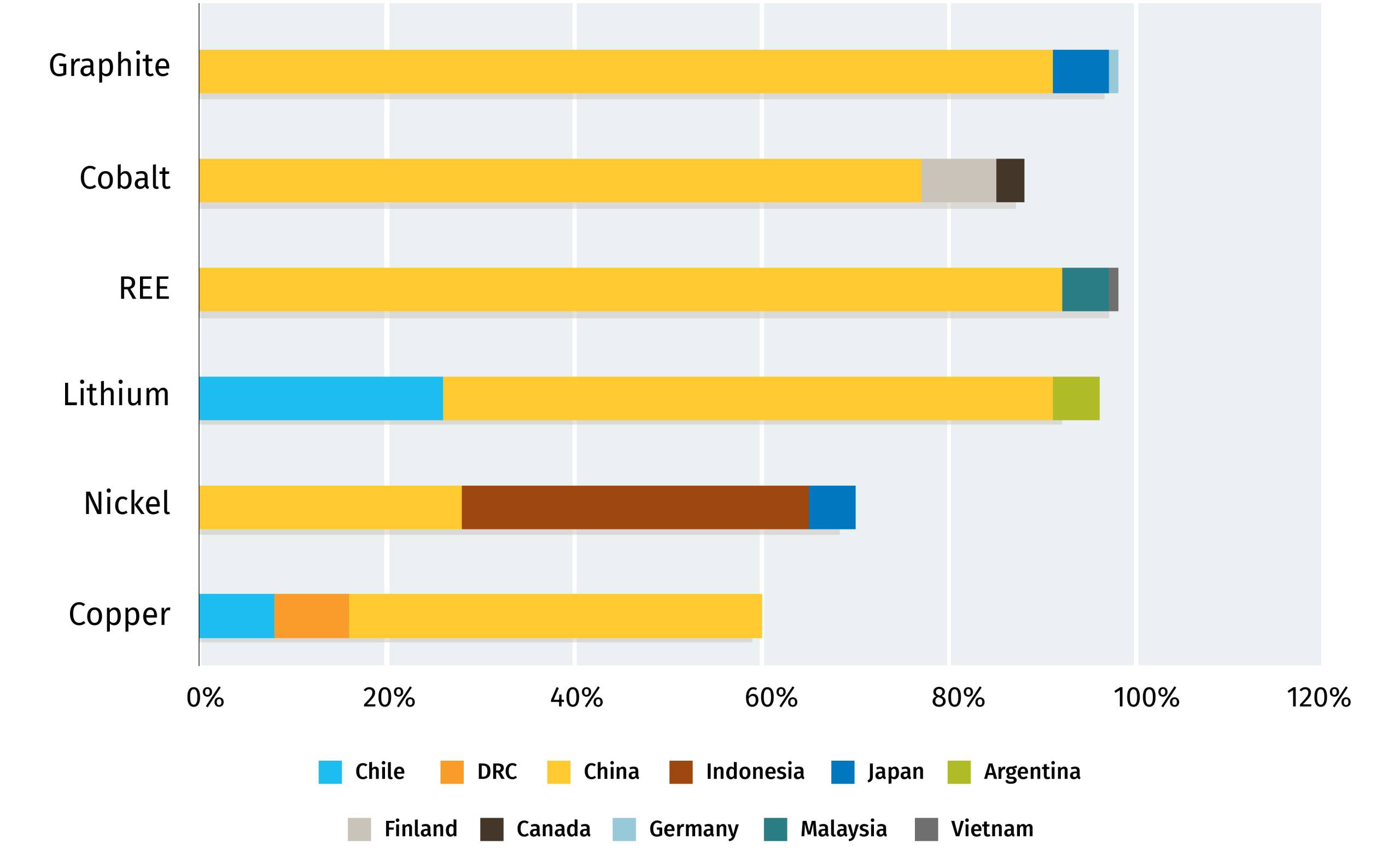

Finally, as the U.S. seeks to reduce its reliance on China and Russia for critical minerals, Canada has the opportunity to strengthen its role as a key supplier for industries like clean energy, semiconductors, and defence. Canada currently provides 19 percent of U.S. critical mineral imports, including essential resources like nickel, aluminum, and zinc. With the right investments and policy support, Canada could further expand its capacity in these sectors.

Additionally, Canada is a crucial partner in the U.S. nuclear energy sector, supplying 27 percent of U.S. uranium imports. As America looks to expand its nuclear energy capabilities, Canada’s advanced uranium mining, conversion, and small modular reactor (SMR) technologies can help fill gaps in the North American nuclear fuel cycle.

To maximize its resource advantages, Canada must invest in infrastructure, create a stable regulatory environment, and attract capital for long-term development. Expanding global trade partnerships—particularly in Asia and Europe—can reduce Canada’s overreliance on the U.S. while ensuring resilience in the face of shifting geopolitical dynamics.

But long term, Canada can’t always run large trade surpluses in these sectors, as such imbalances have the derivative effect of destabilizing the world’s largest economy. We can seek other markets for these resources and also look to buy more resource-related products from the U.S.—be it enriched uranium or packaged foods. That is, if the U.S. is interested in a negotiated approach to trade balances.

On that front, an accelerated renegotiation of the USMCA trade agreement seems both inevitable and in Canada’s interest. A quick resolution to the lingering uncertainties and frustrations in the original agreement might reduce the uncertainty that’s come with the Trump tariff threats. A renegotiation—ideally, free from the threat of tariffs—could help address trade concerns in the new, digital economy, including Canada’s adherence to a digital sales tax. Perennial concerns over Canada’s lumber and dairy sectors might also be resolved, helping create a new agreement that could reinforce North America’s value to global investors. The agreement can do more—to Canada’s benefit—to enshrine human rights and environmental standards in North American trade. But the three countries should remind each other of the mutual benefits of the agreement, even as it is now. In less than five years since it was implemented, North American trade has soared 47 percent, supporting nine million jobs.

More broadly, with the restoration of good faith between governments, Canada can help create a new strategic framework for North America, including the supply of critical minerals, defence of the Arctic, and shared approaches to another economic frontier, outer space.

As Canada navigates the economic uncertainty posed by U.S. tariff policies, this sort of strategic and proactive approach is essential. The deeply integrated Canada-U.S. trade relationship is built on mutual dependence, with Canada providing critical resources, energy, and industrial goods that bolster American economic and national security interests. While tariffs present immediate challenges, they also reinforce the need for Canada to leverage its economic strengths in trade negotiations, diversify its global partnerships, and invest in long-term industrial resilience.

By emphasizing its indispensable role in energy, agriculture, and critical minerals, Canada can position itself not only as a key U.S. trade partner but also as a leader in global markets. Expanding infrastructure, fostering innovation, and securing stable investment environments will be crucial for sustaining growth. While protectionist policies may shape near-term trade dynamics, Canada’s ability to adapt and strengthen its competitive advantages will determine its long-term economic success in an evolving global landscape.

RBC Thought Leadership has launched a multi-month campaign with The Hub The focus of this month’s series is tariffs, trade, and opportunities for Canada in this new economic order. Be sure to check out the kick-off DeepDive.