How Canada can crack the diverse India market

Prime Minister Mark Carney arrived in India with clear ambitions to move quickly toward a Canada–India trade agreement. The geopolitical logic is sound, rooted in diversification, Indo-Pacific cooperation, and increasingly aligned strategic interests.

But successive Canadian governments have tried—and largely failed—to unlock India’s massive market at scale. India liberalizes selectively, opening sectors where imports support domestic growth while maintaining tight protection where political sensitivity is highest. Early gains are therefore most likely where India requires external supply or technology—energy security, industrial inputs, and advanced technologies—meaning Canada’s strategy must prioritize sequenced commercial outcomes rather than broad economy-wide concessions.

Luckily, there’s already a blueprint: Canadian pension funds have laid incredible groundwork, having invested over $70 billion in India, which can open up commercial entry points.

We identify some sectors where Canada can make inroads in the Indian market.

Agriculture: Domestic sensitivities, big trade

-

Agriculture remains Canada’s largest export sector to India, yet also one of its most politically constrained. Current measures—a 30% duty on Canadian yellow peas and 10% tariffs on lentils—are designed to protect Indian farmers and manage food-price stability.

-

India frequently adjusts tariffs, licencing rules, and procurement conditions in ways that effectively cap import volumes, particularly for pulses where Canada is a leading supplier.

-

These policies function as domestic economic management tools and can shift quickly with harvest outcomes or inflation pressures, creating persistent uncertainty for Canadian exporters. Clearer import frameworks would help.

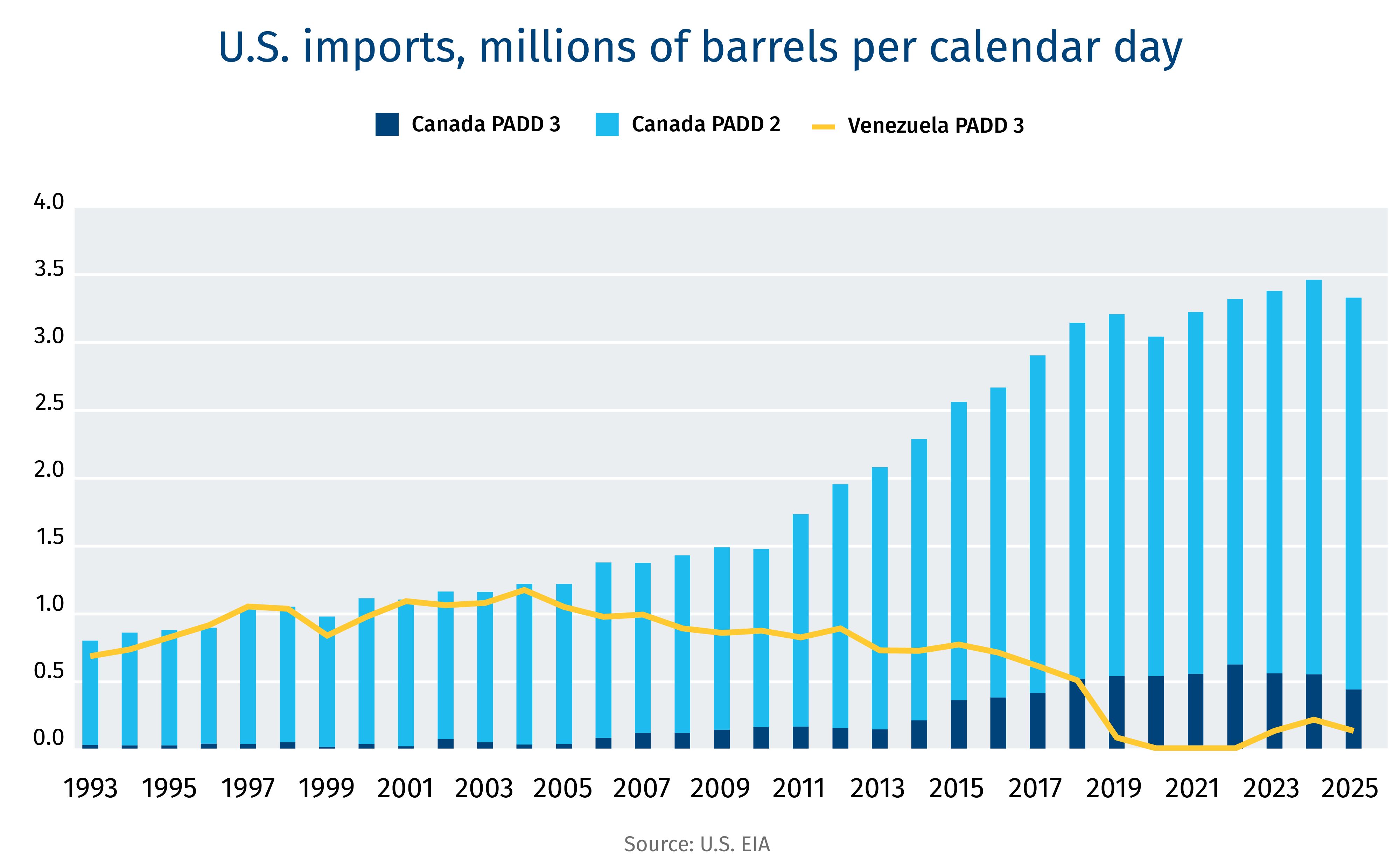

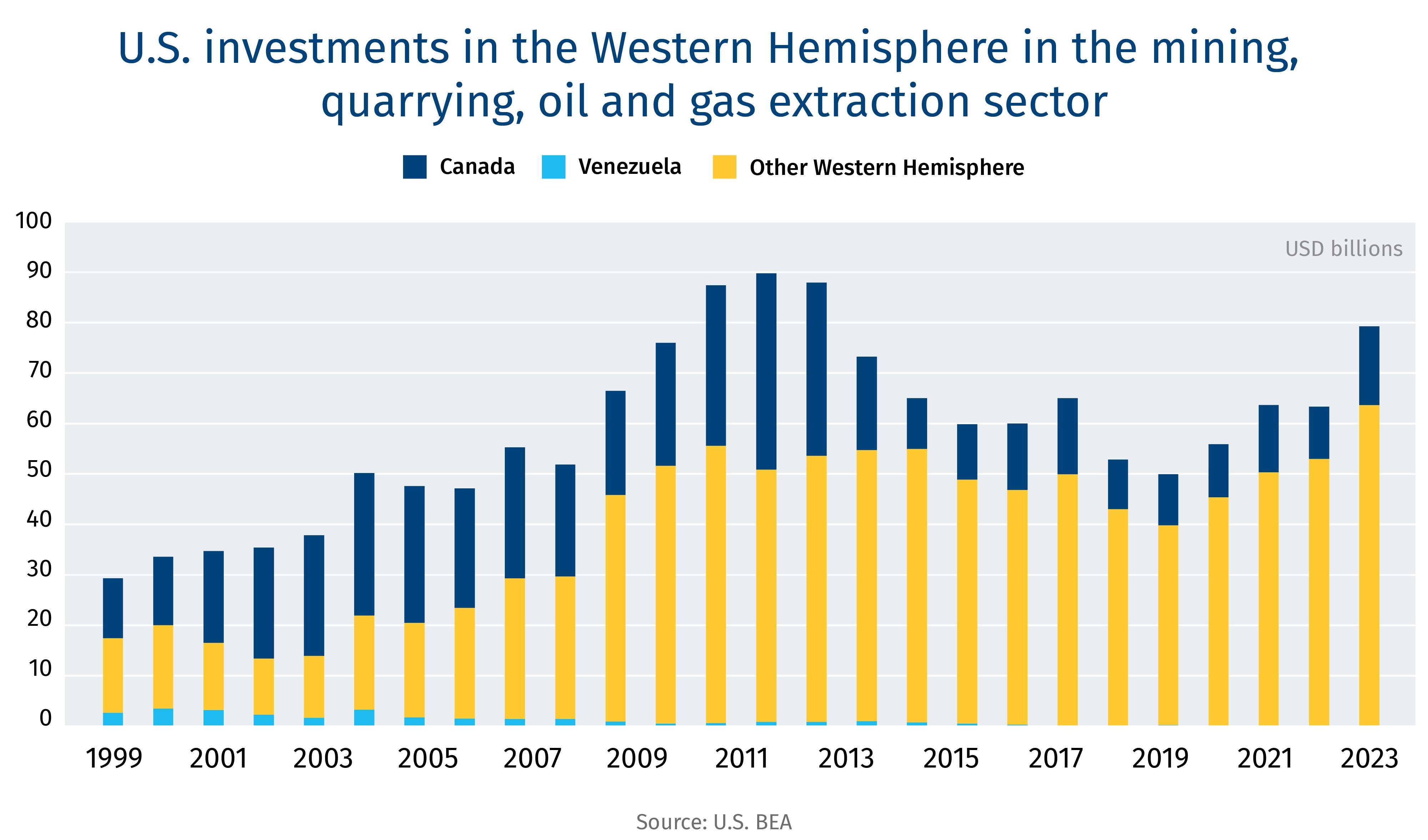

Energy: Displacing Russian oil and gas

-

India’s energy demand is expanding across oil, gas, and electricity generation faster than any advanced economy, creating structural alignment with Canada’s resource base.

-

Yet current trade highlights the gap between potential and reality: Canada’s largest energy export to India today is coal, not oil or natural gas—demonstrating that infrastructure and commercial pathways are limiting the relationship.

-

India’s effort to diversify suppliers, notably Russia, under pressure from the U.S., creates an opening for Canada to reposition itself as a longer-term supplier of crude, LNG, and nuclear fuel.

-

Long-term oil and LNG purchase orders—not diplomatic announcements—will determine whether alignment translates into sustained export growth.

Nuclear: Powered by cooperation

-

India’s planned reactor expansion, targetting roughly 100 GW of capacity by 2047, requires secure fuel supply, while Canada remains one of a limited number of politically reliable uranium exporters.

-

Uranium trade operates on long planning horizons and structured supply arrangements, making it less exposed to short-term commodity volatility than most resource trade.

-

Cooperation typically extends beyond fuel into engineering services, safety systems, workforce training, and regulatory collaboration that deepen industrial ties over time.

-

A uranium agreement would signal that the bilateral reset has moved beyond diplomacy into sustained economic cooperation.

Talent and culture: Soft people power

-

Talent mobility and diaspora ties remain foundational infrastructure for the commercial relationship, underpinning investment and business linkages across sectors.

-

Pressures surrounding international students and domestic post-secondary capacity mean mobility policies must balance economic opportunity with political sustainability at home.

-

Film and media collaboration represents a practical early opportunity, as Bollywood production increasingly seeks global filming locations that “Hollywood North” can provide.

Industries: Beyond commodities

-

India’s growth constraints increasingly lie in systems—grids, logistics, emissions management, and industrial efficiency—not simply access to raw materials.

-

Canadian firms are competitive in these enabling technologies, allowing Canada to participate as a solutions partner alongside a resource exporter.

-

Pairing energy exports with clean technology and digital optimization broadens the relationship beyond commodity cycles and supports incremental, repeatable commercial integration.

Trade with India will advance not through political momentum alone, but by aligning commercial incentives with India’s domestic priorities. Canada’s success will ultimately be measured not by what paper is signed but what follows: goods shipped, projects financed, and supply relationships durable enough to expand over time.

–Thomas Ashcroft, Global Issues Policy Lead

Back to the Future: Lessons from a Post-WWII Tin Agreement

This week, the Office of the U.S. Trade Representative issued a request for comments on how a plurilateral critical minerals agreement should be designed. Buried within the submission is a reference to the 1956 International Tin Agreement. That reference is worth a short history lesson.

Why It Matters

The International Tin Agreement was one of the most ambitious experiments in commodity market governance ever attempted—a producer-consumer framework designed to bring price stability to a material the Western world depended on but couldn’t control. It lasted nearly 30 years but ultimately failed. The reasons it failed are precisely the questions the USTR notice is now asking allied governments to answer for critical minerals.

Lessons learned

-

The buyers’ club needs to be big enough to matter. The tin deal failed partly because non-members were significant suppliers. Plurilateral clubs need critical mass—hard to do given China dominates both refined supply and end-use demand.

-

Speed matters. Tin took six revisions over decades to lay the ground, and still collapsed. The window for today’s Western critical mineral supply chain realignment is shorter with China likely even more incentivized to further disrupt markets.

-

Rules of origin is the real enforcement mechanism. Price floors mean little without teeth, and the buyers’ club needs compliance. Given U.S. desires to reshore production, this reads as a competitive advantage for Canada relative to other U.S. trade partners.

Bigger picture

The critical minerals file is unusual as it’s the only area where Washington is leveraging partnerships rather than tariffs. Convening allies, building frameworks, and even asking trade partners to help design the rules is helping Washington foster greater confidence and investment certainty for industry and financiers.

The architecture is emerging, and if successful, a guaranteed price for metals tied to rules of origin that extend through to refined input should be enough to make Western refining economies work. At present, the capital to build that infrastructure is not. This is where more work needs to be done.

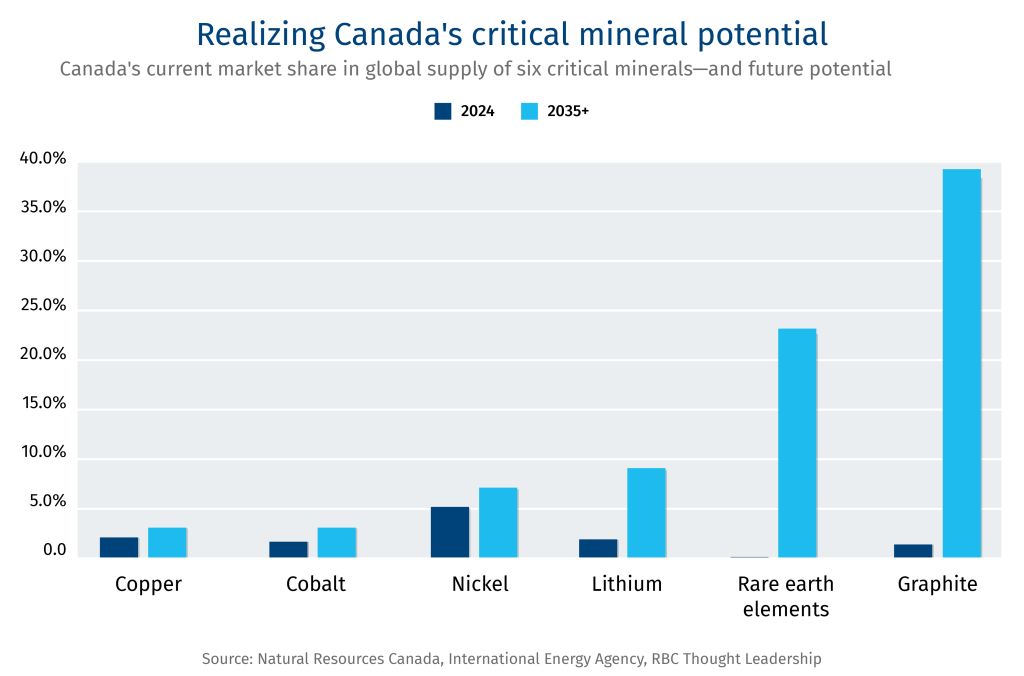

Landing on the eve of the annual Prospectors & Developers Association of Canada conference in Toronto, which attracts more than 27,000 attendees, is RBC Thought Leadership’s newest report, Mine & Refine, which examines that capital gap—the structures, financing mechanisms, and sovereign investment needed to make Canada a credible supplier of refined critical minerals into the new supply chain order.

–Shaz Merwat, Energy Policy Lead

The week that was

China’s finance ministry confirmed that tariffs on some Canadian agricultural goods will be suspended.

-

The announcement follows the deal Carney cut in Beijing earlier this month.

-

While the 100% tariffs on canola meal and peas, and the 25% levy on lobsters and crabs will not be imposed, the announcement made no mention of canola seed tariffs, which were supposed to come down to 15% as of March 1.

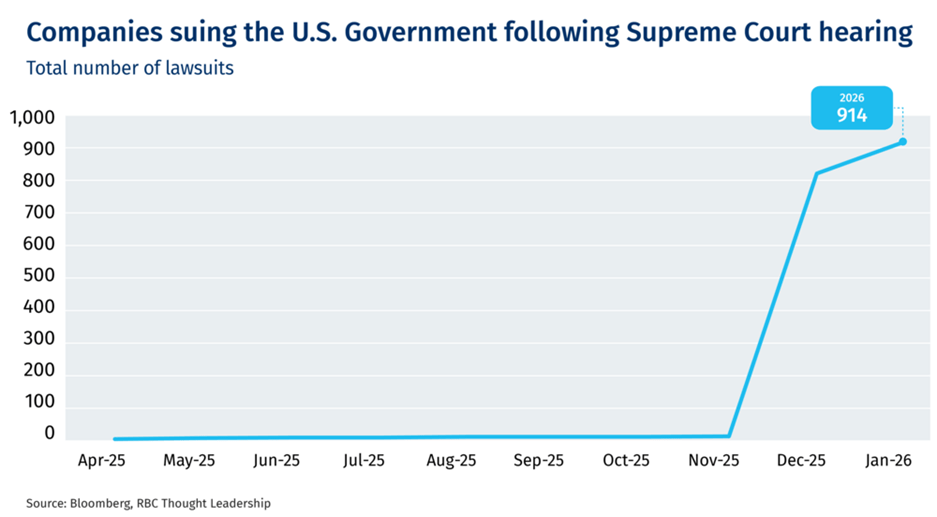

Over 900 companies have sued the U.S. government after Supreme Court tariff ruling

-

FedEx was the first major American company to come asking for refunds after last Friday’s ruling putting ~$170bn of tariff revenue in play.

-

The onslaught of lawsuits that have been filed with the U.S. Court of International Trade will keep lawyers busy for some time and introduce another major layer of uncertainty and difficulty for U.S. President Donald Trump’s tariff regime.

Germany pushes China for a trade reset

-

Chancellor Friedrich Merz urged Beijing to curb subsidies, address industrial overcapacity, and ease restrictions on European firms as EU concerns over unfair competition and widening trade imbalances grow.

-

Xi Jinping positioned China as a defender of multilateral trade and encouraged closer EU alignment, even as Europe seeks to reduce strategic dependencies in critical supply chains.

–Thomas Ashcroft, Global Issues Policy Lead