Also in this edition: Should farmland be used to produce food or fuel? And four potential routes for Canada’s embattled auto industry.

A summit about managed competition

The summit between President Donald Trump and President Xi Jinping in Beijing produced no breakthrough agreements, but that may have been beside the point. After a year in which tariffs between the two countries exceeded 100% and trade flows sharply contracted, the immediate objective on both sides appears to have been stabilization versus resolution.

The atmospherics mattered. Trump described the talks as producing “fantastic trade deals,” while Beijing emphasized “common understandings” and continuity. But beneath the optics, the summit revealed where the real negotiations and constraints now sit.

A few themes stood out:

The trade relationship is structurally smaller than it was

-

U.S. imports of Chinese goods and the bilateral trade deficit are now at roughly 20-year lows. Washington’s efforts to reduce exposure to China through tariffs, supply chain diversification, and industrial policy have had a measurable effect. The relationship is no longer defined by integration.

-

There was no material progress on tariffs or the Section 301 trade investigations targeting China over state-subsidized production overcapacity in sectors like steel, and electric vehicles.

China’s priority is predictability

-

The Chinese spent the years between Trump’s first and second terms doing their homework, preparing counteractive policies for more U.S. trade confrontation. Export controls on rare earths and critical minerals, industrial policy tools, and tighter supply chain leverage have proven key weapons in China’s arsenal.

-

But the summit reinforced that Beijing’s near-term priority is a more predictable operating environment with Washington—one that reduces the risk of escalation and preserves access to key export markets, technology inputs, and capital flows.

No major progress on chips and export controls

-

Global semiconductor stocks slid with no major chip deals announced and continued stagnation over the sale of Nvidia’s H200 chips to China.

-

This remains the clearest dividing line in the trading relationship. Washington still sees leading-edge chips and export controls as a way to mitigate China’s access to advanced semiconductors that could be used for military applications or AI innovations. Beijing, in turn, hasn’t formally approved shipments of the chips and has looked inward, urging Chinese firms to switch to domestic hardware.

Agricultural purchases are a U.S. political priority

-

The clearest deliverables, as is often the case in trade negotiations with China, may ultimately come in agriculture. U.S. Trade Representative Jamieson Greer said Washington expects China to commit to “double-digit billions” in annual purchases of U.S. agricultural products over the next three years, including soybeans, poultry, and pork.

-

The White House needs to be seen as supporting U.S. farmers, especially as the impacts of the Iran war on fertilizer prices and other agricultural inputs rise ahead of the mid-terms and as planting season gets underway.

Both sides appear to want guardrails

-

Discussions around a possible “board of trade,” investment mechanisms, and even preliminary AI guardrails show neither Washington nor Beijing currently wants uncontrolled escalation.

-

The strategic rivalry continues, but both sides appear increasingly focused on managing it rather than intensifying it in the near term.

—Thomas Ashcroft, Global Issues Policy Lead

Food or fuel?

Skyrocketing oil and gas prices and supply constraints are pushing countries to boost biofuel production and use. The shift aims to curtail reliance on Middle East oil and gas supplies. But the surge in policy-driven biofuel demand coincides with the rising food affordability crisis reviving a recurring debate: should farmland be used to produce food or fuel?

The biofuel boom:

-

The U.S.’s Environmental Protection Agency set record Renewable Volume Obligations (RVOs) for 2026–2027 with notable increases for biomass-based diesel, produced primarily from soybean and canola oil in North America. In addition, the U.S. House passed legislation this week to allow nationwide year‑round sales of gasoline containing 15% ethanol (labelled as E15), which is largely produced from corn in the U.S.

-

The European Commission proposed the AccelerateEU strategy in April, which includes measures to boost EU sustainable biofuel production and use. This proposal is a rapid response to the bloc spending an additional €24 billion on fossil fuel imports within the first 50 days of the Iran conflict.

-

Indonesia revived its plans to introduce a higher biofuel blend in 2026 following rising fossil fuel import costs. The blending rate mandate for biodiesel made from palm oil is planned to move to 50% from 40% this year.

-

Brazil is actively accelerating its biofuel blending mandates to enhance energy sovereignty. President Luiz Inácio Lula da Silva announced in April that the ethanol blend mandate will be raised to 32% (E32) in gasoline this spring. For biodiesel, testing is underway to understand the viability for moving the blending rate from 15% to 20%.

-

India reached its E20 ethanol blending goal in April. Disruptions to the country’s oil and gas prices and supply are prompting discussions on ramping up to E85 or E100 as production capacity expands.

-

Vietnam expedited its national mandate for 10% ethanol blends in gasoline to begin in April due to energy shocks in price and supply. Ethanol is produced mostly from cassava, sugarcane, and increasingly corn in the Southeast Asian nation.

-

…and Canada? In response to the previous shock to Canada’s biofuel supply chains from U.S. trade tensions, the federal government announced a $370 million Biofuel Production Incentive and committed to amending the Clean Fuel Regulation to prioritize domestic low-carbon fuel production. These measures, while not in response to Iran war, are intended to increase the resilience of the domestic biofuel sector.

Bottomline: The global biofuel market is poised to enter another expansion cycle as countries raise blending mandates to meet energy security and transition to lower greenhouse gas emitting energy sources. However, early signs of rising corn, sugarcane, and vegetable prices may further pressure food prices this year.

—Lisa Ashton, Agriculture Policy Lead

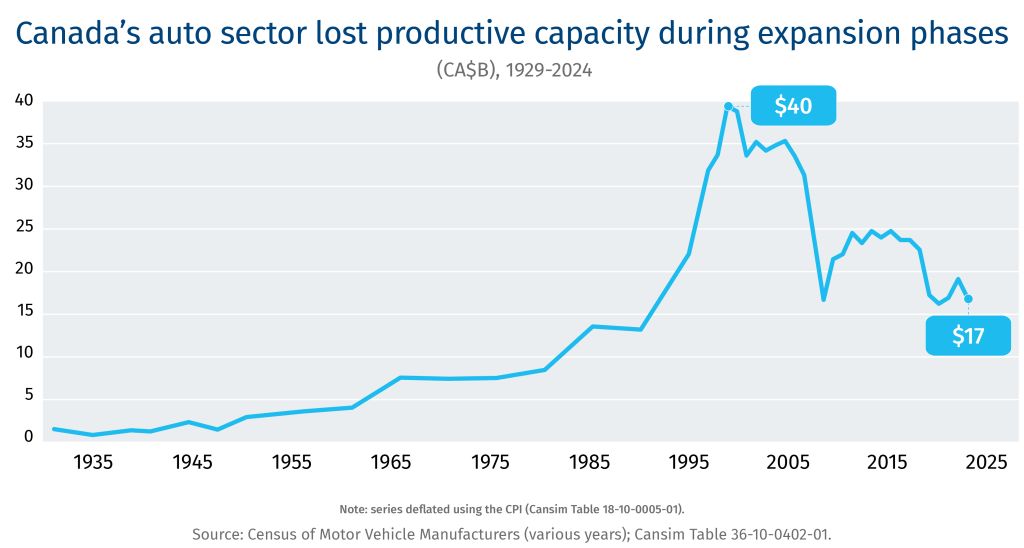

Road Test

About 200 auto sector executives packed into a hotel ballroom this week for the Toronto Region Board of Trade’s Ontario Auto Forum. Magna CEO Swamy Kotagiri laid out three distinct options for dealing with the industry’s headwinds: protect jobs, chase affordability, or build resilience through anchoring the industry in capabilities that can’t easily be replicated. The latter, he said, should be the priority.

RBC Thought Leadership’s Managing Director Jordan Brennan also took to the stage, presenting findings from his latest report Steering Through Uncertainty, which charts four distinct paths for the embattled auto industry.

Read the full report, including the five strategic considerations that cut across all four scenarios, here.

The week that was

USTR pushes for “Fortress North America” steel protections under USMCA

-

Deputy U.S. Trade Representative Jeffrey Goettman said an updated USMCA should include “unified tariff borders” for sectors like steel, aluminum, and autos to prevent products made with non-North American inputs from entering through Canada or Mexico. U.S. steel executives backed tighter “melt-and-pour” origin rules.

EU sanctions on Chinese chip supplier raise fears of automotive disruption

-

Industry executives warned EU sanctions of Chinese chipmaker Yangzhou Yangjie Electronic Technology, for allegedly supplying military technology to Russia, could trigger renewed chip shortages across the auto sector. Some firms are already seeking exemptions as manufacturers remain vulnerable following last year’s rare earth and semiconductor disruptions.

EDC expands focus on diversification, defence, and strategic sectors

-

Export Development Canada announced it facilitated $135 billion in trade-related activity in 2025, supported nearly 24,000 businesses, launched new programs, while expanding its European and Indo-Pacific presence.

Bank of Canada research highlights declining maritime connectivity

-

Canadian ports became less central to global shipping networks between 2016 and 2023, with declining direct connectivity and lower shipping capacity relative to major Asian hubs. The risk, writes the BoC, is “greater exposure to supply chain disruptions that could increase the cost of doing business.”