CER Update: Ottawa’s Flexibility On Natural Gas Gives Provinces Major Win

Category: Energy

rbc_toc_for_mmm_action

The federal government’s latest Clean Electricity Regulations update shows it’s softening its position on sharply cutting emissions from natural gas-fired power plants by 2035.

Ottawa has demonstrated that it’s receptive to the provinces’ and utilities’ concerns about their ability to meet 2035 Net Zero targets.

We see this as a major win for Ontario, and it also gives Alberta and Saskatchewan more leeway in how they manage their transition to cleaner sources.

The proposed changes are not expected to compromise the 2035 Net Zero target set for the electricity sector if the regulations for offsets are included.

The devil will be in the detail, as the white paper does not provide any details on what the regulations could look like when finalized.

In terms of next steps, comments on potential changes to CER are due to be submitted by March 15, and final regulations are set to be released by the summer.

Ottawa’s draft Clean Electricity Regulations (CER) has sparked significant debate among provinces since its release in August 2023. Various stakeholders, including provinces, industry, and utilities, have raised concerns about the draft’s strict approach to phasing out natural gas from the grid. Most provinces worry that achieving the federal target of a Net Zero electricity grid by 2035 across the country will be challenging while ensuring system reliability and affordability. There were particularly large backlashes from Alberta and Saskatchewan, which are currently phasing out coal in favour of less emitting generation like natural gas.

The federal government responded last Friday with an update on the consultations and design options that are being considered for the final regulations. It comes several months after the consultation period for the draft regulations closed.

The feedback that the federal government received from the consultation raised concerns about the effectiveness of carbon capture and storage (CCS), potential operation of inefficient units, short end-of-prescribed life, challenges for existing cogeneration facilities, provisions for greenhouse gas offsets, and post-facto emergency exemptions review. These concerns could impact units under development and how existing units are operated.

In last week’s update, the federal government proposed major changes to its draft to reduce carbon emissions from Canada’s electricity sector by 2035. The new design options show more pragmatism in the federal government’s approach, indicating that it is softening its position on sharply cutting emissions from gas-fired power plants by 2035.

What’s in the update?

The updated design options for the regulations would provide electricity system operators more flexibility to continue operating their natural gas power plants past 2035. This includes setting annual emission limits rather than performance standards, allowing plants to operate longer without constraints, and permitting the purchase of offsets when emissions from natural gas generation exceed those limits.

The improvements to the regulations currently being considered are a significant win for provinces that will still need to rely on natural gas generation past 2035. This ensures that provincial electricity system operators can continue to provide reliable and affordable electricity while maintaining Canada’s ability to achieve its emissions reduction goal.

Flexibility for provinces

The federal government is considering several options to provide more flexibility to provinces, utilities, and other electricity regulators and providers, while still ensuring significant emissions reductions. One such consideration is changing the approach from a performance standard, which is a fixed emissions intensity standard, to a possible emissions limit. This limit would be tailored to each unit’s capacity, replacing the current “performance standard approach.”

This new approach could potentially incentivize efficiency improvements and provide flexibility. However, it could also eliminate the “peaker provision approach” that was included in the draft regulations, and was an area of concern for Ontario.

We see this as a major win for Ontario, and it also gives Alberta and Saskatchewan more leeway in how they manage their transition to cleaner sources.

Additionally, the regulations could permit a unit to exceed its emissions limit by a certain amount, provided it compensates for all excess emissions with greenhouse gas (GHG) offsets. In this scenario, the federal government will be faced with the task of ensuring a reliable supply of high-quality GHG offsets. Additionally, they need to establish effective market mechanisms to manage potential increased demand for offsets within Canada.

Other considerations include extending the “End of Prescribed Life” beyond the current proposed level of 20 years and allowing responsible parties, such as utilities and crown corporations, to pool the emissions limits of their multiple existing units in the same jurisdiction.

Regulatory treatment of cogeneration is also under review, potentially shifting to an emissions limit. The approach under consideration would also differentiate between “behind the fence” electricity emissions and the emissions associated with electricity provided to the grid.

The federal government plans to continue engaging with stakeholders, including provinces and utilities, before finalizing the CER later this year. Ottawa has stated that continued collaboration will be essential to ensuring the regulations can provide significant emissions reductions while supporting electricity system reliability and affordability. Comments on potential changes to CER are due to be submitted by stakeholders by March 15.

rbc_toc_for_mmm_action

Cleantech is in correction mode. Last year’s CleanTech Forum, in Palm Springs, was brimming with measured optimism, although there were whispers of some impending corporate failures wafting down the halls.

Clean technology fortunes between the commercially viable and the questionable had already begun to diverge in 2023, a trend that will only deepen.. At this year’s forum in San Diego, there was a full-throated acknowledgement of a much-needed cleantech shakeup in the offing.

This year will almost certainly see further retrenchment from the US$40 billion capital flows into clean technology companies and national and corporate climate commitments of 2023, according to BloombergNEF.

Companies with weaker economics or technical fundamentals are struggling, while venture and growth dollars for new industrial technologies are waning. Dozens of cleantech companies have seen their values drop and financial flows dry up as financing becomes more difficult to obtain. Further declines and eventual consolidation in the industry seems inevitable.

Still, that’s in Silicon Valley’s DNA: test, crash and burn until a unicorn rises. On repeat.

To be clear, there’s plenty of optimism, too: project financing and job creation for clean technology manufacturing facilities have never been stronger. Meanwhile, government measures, such as the U.S. Inflation Reduction Act, and climate-focused investors will sustain the best companies as they commercialize.

North America’s manufacturing renaissance is underway with technologies graduating from demonstration to deployment. Factories for electric vehicle batteries, electrolyzers, carbon dioxide pipelines, and low-carbon steel, cement, and ammonia plants are coming online across the continent.

Other bright spots are the opportunities in emerging economies, especially in Asia Pacific. Highly susceptible to climate change’s impacts as they raise their standards of living, India, South Korea, and China, for example, are bucking the Western downturn and are happy hunting grounds for clean technology investors and entrepreneurs.

By the end of the year, the role of politics, another key variable in forward climate trajectory, will also become clearer. Electoral unease has already manifested in the rollback of climate policies around electric vehicles and strengthened oil and gas licensing in the U.K., and calls for axing the carbon tax in Canada.

In the conference halls of San Diego Bay Mission Resort there were whispers of further headwinds with a potential return to a Donald Trump presidency. But with Red States securing most of the capital flows emanating from IRA incentives, climate policies may yet not be dumped by Trump. Of course, another Joe Biden term could cement climate policies in the American economy.

Vivan Sorab is Senior Manager, Clean Technology, at the RBC Climate Action Institute.

rbc_toc_for_mmm_action

The global energy system is in the throes of a generational shift.

Population and economic growth spell a demand for much more energy. Climate pressures spell an imperative for a different mix. And new technologies mean new opportunities for both.

Looking out a decade, to the mid-2030s, can that changing world of nearly 9 billion people power itself into a new age of sustainable growth? And where can Canada, a global leader in all forms of energy, create the most value in a Net Zero economy?

To map out the expected courses for both energy demand and supply in the 2030s, RBC Economics & Thought Leadership and RBC Capital Markets, including Global Research, developed global and national datasets, and new projections. The estimates are based on current assumptions of population growth, economic growth and distribution, technology adoption and government regulation.

The highlights of that research are laid out in this report, and its six major conclusions which are designed to help inform policy discussions at COP28, the UN Climate Conference in Dubai, and subsequent energy policy conversations.

We know energy is fundamental to every part of our economy, while our management of energy emissions is also fundamental to progress on climate change. Balancing those needs will require an informed public discussion, which this research is meant to contribute to.

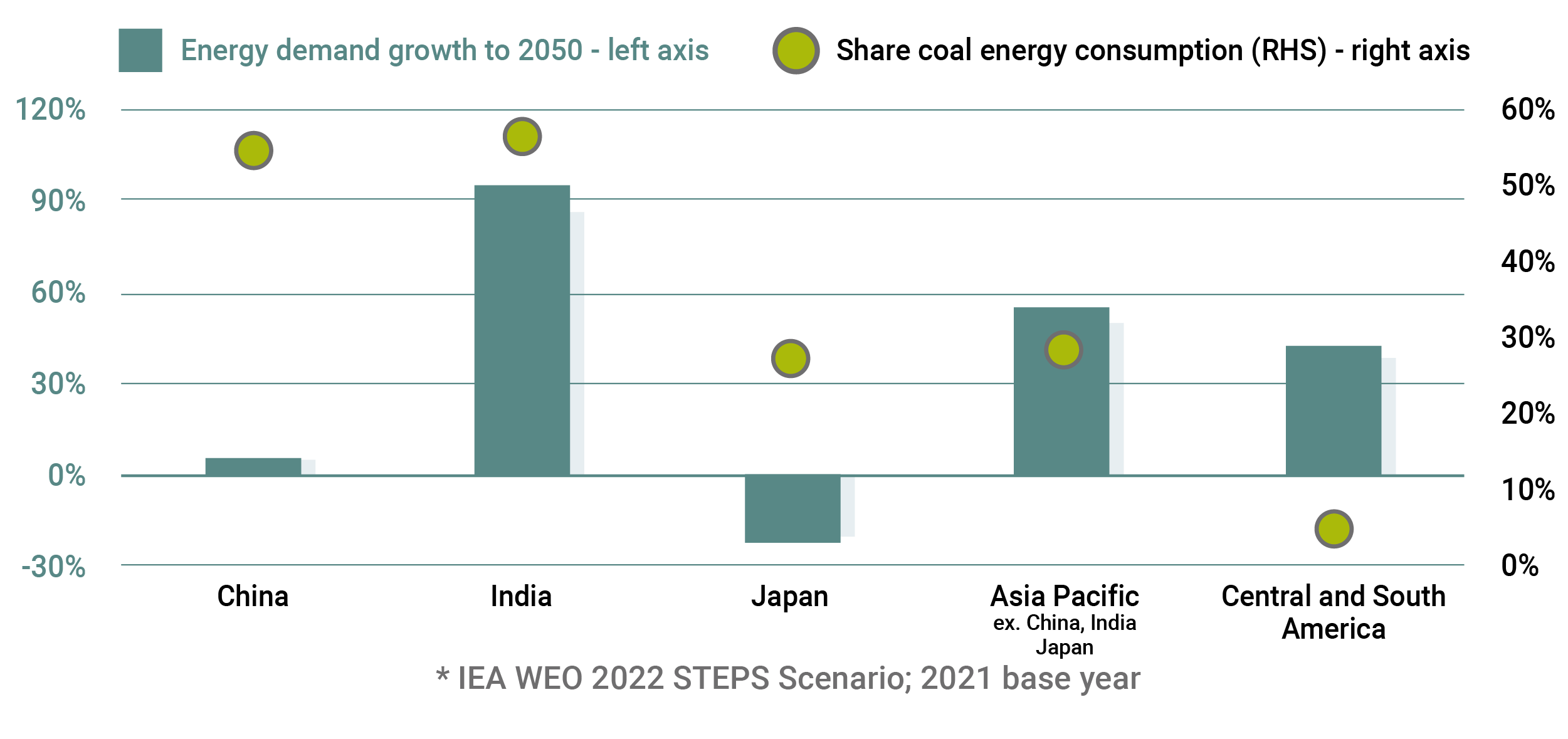

1. The world will need to supply another United States worth of demand

Global population growth may be slowing, but the world still needs to generate more exajoules in the next few decades to power emerging economies’ growing needs. Global population is set to rise by 1.7 billion to 9.7 billion by 2050, adding the equivalent of another China and United States in one generation. More imminently, world population will rise by around 834 million by 2035, which is the equivalent of another Europe. That will require another 93 Quad BTU of energy, or close to what the United States consumes now.

When it comes to energy-intensity growth, the world appears to be on a two-track trajectory. In advanced economies, efficiency gains are lowering per capita consumption, which has contracted 13% over the past 20 years in Europe and North America, or about 0.7% per year. Population growth is also easing, but not declining outright in most advanced economies. Still, efficiency gains on a per-capita basis aren’t yet large enough for total energy demand to decline outright, even among advanced economies, especially in Canada.

Emerging markets are on a faster track and still in the early stages of adopting passenger vehicles, home appliances and advanced manufacturing. In India, the world’s most populous country, energy consumption rates are still relatively low. A slowing population growth rate will help contain emissions growth but not sufficiently enough to offset a growing demand for intensive energy sources, including coal. Indeed, India’s population growth remains concentrated in the north where coal-dependency remains significant for industrial and urban demands.

Global energy demand growth by region

Per-year percentage contribution to world energy consumption growth

Source: U.S. Department of Energy, RBC Economics

Elsewhere, the pace of growth is uneven across the developing world. Per-capita energy consumption rates in China, the world’s largest market, are approaching advanced economy levels and will begin to level out. The pace of energy demand growth is set to slow after rising by 2% per-year over the past decade. And decades of low birth rates from the one-child policy mean China’s population is outright declining, which (all else equal) lowers total energy demand. By our count, growth in total energy consumption will be half the pace of the last decade in China – with risks of further decline if its economy weakens.

The populous countries of Africa, rest of Asia and Latin America are facing their own unique challenges to build their economies while managing energy demand and climate pressures. Capital will be critical. Developing countries account for only one-fifth of investment in clean energy, despite making up two-thirds of the world’s population. Middle income countries, such as Brazil, Mexico and South Africa, are home to 75% of the global population and 62% of the world’s poor. Their rising disposable income, and aspirations to buy motorbikes, homes and electronics, will require all forms of energy.

Eventually, the massive gap between energy consumption rates in emerging markets will close as their economies mature — but we are not there yet.

Energy consumption per-capita

MMBtu/person, 2021

Source: U.S. Department of Energy, RBC Economics

2. Renewables will account for 20% of global energy needs

While total energy demand will continue to increase, a rising share will come from production of zero emissions and renewable power. Renewable power is set to grow at five times the rate of conventional energy by 2035, which would push the share of total energy consumption globally from renewables to about 20% from 12% in 2022 and 8% a decade earlier in 20121.

The cost competitiveness of renewables versus conventional energy has improved greatly, and government supports are encouraging a faster transition than otherwise would occur. Thanks to the Inflation Reduction Act, U.S. renewable energy growth is set to more than double by 2035, rising at a 7% per-year rate, or double the growth rate for renewables over the past decade.

In virtually all regions, renewable power is set to rise as a share of total energy consumption. One key reason: between 2010 and 2020, the cost of solar and wind power fell 56% and 85%, respectively. Much of that growth could displace coal and other high-emissions sources. Coal consumption outright declined by about 0.5% per year globally over the last decade, and is expected to decline annually at twice that pace through 2035. That would still leave coal accounting for about 20% of total global energy consumption in 2035, down from 27% currently and over 30% a decade ago.

Still, renewables are not without their challenges. Countries that have rolled out ambitious clean grid plans worry about the reliability of grids that depend primarily on wind and solar. A surge in installations is leading to cost inflation, at least in the medium term, while scaling up battery storage remains a challenge, although rapid advances are being made.

Global co-operation is also crucial to ensure a smoother roll-out of renewables and a level playing field across countries. The patchwork of global regulations, such as a carbon border adjustment tax, and different carbon pricing mechanisms, need further refinement, robust common standards, and general acceptance across jurisdictions to speed up the transition.

Political calculations could also change the trajectory of renewable adoption in many counties. There are signs of political resolve weakening on climate policies as the electorate around the world struggles with high cost of living, especially inflated energy bills. As many as 3.2 billion people in 40 countries (including the U.S.) with a combined GDP of US$44.2 trillion, will head to the polls in 2024. Climate policies are set to come under scrutiny and the prevailing public mood could well shift momentum in either direction.

Meanwhile, worries around China’s control over metals and minerals and technologies vital for the energy transition have led many countries to develop parallel, and costlier, supply chains. But new mines will take at least a decade to build and renewable supply chains could easily become more complicated and costlier in a trade-restricted world. While these frictions are unlikely to slow the pivot to renewables, they could delay it.

Global energy consumption by source

Source: U.S. Department of Energy, RBC Economics

3. Peak oil demand is coming—but not yet

Discussions around “peak oil” can miss the bigger picture: An industry can remain dominant for decades even if it never surpasses some past high point. We assume global oil demand will continue to slow as a share of total energy consumption, but volumes consumed will not outright peak before 2035.

Total petroleum consumption is already declining in major advanced economies (including the United States) but will continue to grow in emerging markets as population and energy use per person rises. There is substantial uncertainty around those estimates, with near-term risks both on the downside (slower global growth, notably in China) and on the upside (rapid technology adoption, also notably in China). Still, the direction of travel is clear: Over 60% of total global oil consumption is from the transportation sector, where the EV transition is well underway. China alone accounted for almost two-thirds of total global petroleum consumption growth over the last decade, and is now shifting rapidly to EVs. Full electric and plug-in hybrid vehicles have increased to 40% of total retail vehicle sales in China – more than 10 times the roughly 3% share in 2019.

Expected petroleum consumption growth by region

Per-year percent change, 2022 to 2035 (expected)

Source: UN, U.S. Department of Energy, RBC Economics

In Europe, electric vehicles already account for 44% of total car sales in 2022. The U.K. plans to fully end the sale of fully internal combustion engines by 2035. Canada plans to increase zero-emission vehicle sales to 60% of the new car market by 2030 and 100% by 2035. Those plans can change, and governments have a long history of delaying green energy objectives.

The turnover of vehicle fleets is another key factor. Internal combustion vehicles are staying on the road for longer than ever as reliability and durability improves (the average age of a vehicle in the U.S. is 12 years), suggesting a longer shelf life for existing stock even as EVs make up a greater share of sales. Still, per-capita petroleum consumption rates have already been declining for decades across advanced economies thanks to fuel efficiency increases, and that trend will likely accelerate as the market share of EV sales grows.

Per-capita petroleum consumption

Index = 100 in 2011

Source: UN, U.S. Department of Energy, RBC Economics

4. Natural gas faces a more uneven transition

The phasing down of coal power is expected to boost demand for natural gas as a transition fuel on an eventual pathway to renewables and battery storage—at least in advanced economies.

The pace of that transition will vary significantly by region, and with levels of government support. In the U.S., heat pump subsidies in the Inflation Reduction Act will help accelerate the transition to renewable fuels for home and commercial heating. Elsewhere, coal remains a core energy source, which gas could displace over time. China, the world’s largest emitter of greenhouse gases, is continuing to invest in nuclear power, but also permitted the equivalent of two large scale new coal power plants per week in 2022, despite pledges to reach Net Zero by 2060. In India, there is an estimated 65.3 GW of proposed, on-grid coal capacity under active development, equal to a third of its current coal generation capacity.

Globally, natural gas demand growth is expected to be driven primarily by increased demand in emerging markets — enough to ensure total demand for natural gas is not likely to peak until after 2035. But the pace of growth will average about half the 1.8% annual rate of growth over the last decade, and the share of natural gas in the total global energy mix will edge lower with renewable power sources growing more quickly.

In Canada, natural gas demand will be underpinned by strong demand from industrial sources – including high demand from the oil & gas sector. The expected launch of LNG Canada by mid-decade will signal Canada’s first major gas export foray beyond the United States, as major markets look for secure energy supplies. In Europe, since Russia’s invasion of Ukraine, plans for 26 new regasification terminals have been announced or launched, totalling 104.5 MTPA—a fifth of the current global LNG capacity, according to the International Gas Union. In Asia, Japan, China and South Korea remain among the world’s top three LNG importers. Their new long-term deals with multiple LNG exporters underscore their desire to secure and diversify energy supplies.

Petroleum remains an important source of energy – still accounting for around 30% of total energy consumption by 2035. That would remain true even in the International Energy Agency’s more optimistic scenario in which global oil consumption peaks before the end of this decade. And the nature of Canadian oil production – heavily weighted to long-lived projects with very large initial sunk capital costs, and a relatively small share of global production – means that domestic oil production is relatively insensitive to near-term market dynamics2.

Canadian oil & gas capex spending still low

% of GDP

Source: Statistics Canada, RBC Economics

Still, the sector remains constrained by insufficient pipeline capacity to get Canadian production to market. The government-owned Trans Mountain Pipeline expansion will boost takeaway capacity significantly once it enters service likely in 2024. The 590,000-barrel-per-day expansion will fetch tidewater prices and reduce the discounts on Canadian benchmarks.

Additionally, oil sands production is well-capitalized and may not need significant further investments. As a result, total oil and gas investment has declined to 1.5% the size of annual Canadian GDP – less than half the share (3.7%) before the oil price collapse of 2015.

Even without new projects, the domestic industry can increase production over the next decade if global demand grows. We expect Canadian oil production to rise by 16.5% by 2030, primarily by increasing capacity of existing production rather than new investments.

The Federal government’s proposed framework for an oil & gas emissions cap could change that outlook. There is still no certainty of what that the final regulations will look like. The framework envisions a (soft) cap at 35%-38% below 2019 emissions from oil & gas production to be phased in from 2026 to 2030 and with options to produce above caps for a price. But details are still to come and will be influenced by feedback from industry, legislative pressures, and potential court challenges.

Decarbonization strategies may present the most significant capital need for oil and gas producers heading into the 2030s. The oil sector has already lowered emissions per barrel by roughly 20% since 2010, although increased production led to an absolute growth in emissions over that period. Plans and proposals for decarbonization projects, including carbon capture and sequestration, will require tens of billions of dollars of new capital, including from the federal and provincial governments. The sector believes such investments could secure its export markets for years, perhaps decades, to come.

6. Canada’s strong population growth will require a broad energy mix

Canada has one of the highest per-capita energy consumption rates in the world thanks to cold winters, hot summers, and a widely dispersed population. In addition, high levels of immigration are now the key driver of population growth, and added energy demand.

Will Canadians shift to climate-friendly technologies fast enough to offset the addition of five million newcomers over the next decade? The transition to EVs is one signal it might—the share of hybrid and full-electric vehicles in total autos sales has more than doubled over the last decade, to 16% from 7% a decade ago. And the volume of gasoline sales is running ~3% below 2019 levels despite a 6% population increase over that period.

Canadian gasoline sales growing slower than population

Index = 100 in 2019

Source: Statistics Canada, RBC Economics

The pandemic reset consumer behaviour with possibly long-term consequences. Work-from-home policies have also dented public transit traffic and fuel consumption. Plus, a new generation of Canadians, and younger immigrants, living in more urban settings, may further cut fuel consumption over time.

More people will likely mean more buildings to heat, too. Over the longer-run, alternative heat sources like heat pumps can help displace traditional natural gas and fuel oil as primary home heating sources. But cold winters mean energy demand for home heating will continue to grow and keep a floor under natural gas consumption—for now.

Canadian population growth bucking a slowing global trend

Average percent change per year

Source: UN population projections (Statistics Canada for Canada), RBC Economics

Canada’s share of renewable power is still relatively high (25%) compared to other countries, mainly due to the availability of abundant hydro power. But the impressive figure masks a weakness: Canada is one of the few advanced economies that failed to increase that share significantly over the past decade. That could change in the decade ahead with renewable power growth expected to accelerate, as envisioned in the proposed federal Clean Electricity Regulations. The rules aim to create low- or zero-emission electricity grids across Canada by 2035 and are part of the federal government’s overarching goal for the economy to get to Net Zero by 2050. The eventual shape and success of those regulations, which are opposed by several provinces, will be significant to the trend-line of natural gas consumption.

Canada is also expected to rely on growth in nuclear energy, led by Ontario, to boost the share of total energy consumption from the zero-emission source. As the industry regains acceptance as a reliable and safe zero-emissions energy source, we assume a 9% increase in nuclear energy consumption in Canada by 2035.

Canada energy consumption by source

Source: U.S. Department of Energy, RBC Economics

More broadly, the right policy levers and industrial innovation can transform Canada into an all-round global energy player, and taps its sun, wind and timber, in addition to its strategic fossil fuels. Canadian resources and ingenuity can be a force in the world and help us deliver our Net Zero target, as we stated in our $2 Trillion Transition report.

Lead author: Nathan Janzen, Assistant Chief Economist, RBC Economics

Myha Truong-Regan, Head of Climate Research, RBC Climate Action Institute

Yadullah Hussain, Managing Editor, RBC Climate Action Institute

Caprice Biasoni, Graphic Design Specialist

There is room for faster growth in renewable power if governments are more aggressive at accelerating the transition. IEA projections also have renewable power rising to ~20% of global energy consumption by 2035 based on ‘stated policies’, but the share rises to closer to a third in the more aspirational ‘announced pledges’ scenario.

Oil production in Canada continued to grow through the global oil price collapse of 2015

rbc_toc_for_mmm_action

Canada is facing a major electrification challenge at a time of rising demand—and intense competition for decarbonization dollars.

We have a head start with a low-emissions grid but building on that advantage would require significant new investments to develop a larger and reliable electricity infrastructure that attracts clean industries.

As the new Net Zero race heats up, the U.S.’s Inflation Reduction Act (IRA) has emerged as a key catalyst, with its slew of incentives running into billions of dollars. While offering Canada fresh opportunities to capitalize on energy transition, IRA also challenges Ottawa, the provinces and industry to raise their game. If Canada gets it right, a substantially bigger and sustainable grid would serve as a springboard for the new energy economy.

In a bid to meet the challenge, the federal government unveiled its much-anticipated Clean Electricity Regulations (CER) last week, sketching out a roadmap for a Net Zero grid by 2035—with a few detours.

Ottawa’s original, stringent stance on a non-emitting grid has given way to a more flexible approach, accounting for each province’s unique challenges and the sheer scale of managing the energy transition without hurting affordability and reliability. It’s an acknowledgement that the country needs all the energy sources at its disposal to build out a reliable energy infrastructure, with guardrails to ensure new dollars heavily favour low-emission sources.

The proposal also offered more clarity on the role of abated natural gas in the power grid—a contentious issue between Ottawa and the provinces. Despite some latitude, the proposed CER still requires electricity generation in Canada to achieve a low-carbon grid 15 years sooner than legislated targets for the whole economy.

The regulations are going to be play a critical role in boosting the country’s green credentials. A diverse mix featuring gas-fired power with carbon capture, nuclear, hydro and renewables will be needed to meet growing electricity demand. It would also help attract investments to build an electric vehicle supply chain, sustainable mining and other new energy sectors.

The onus is now on provinces to adopt the new regulations. The federal government is seeking feedback until November 2023 with plans to publish finalized regulations by 2024.

Some provincial grids will find it harder to hit Net Zero targets by 2035

GHG emissions in electricity sector by jurisdiction

Jurisdiction

Electricity Total

Greenhouse Gases (Megatonnes)

Electricity Sector Emissions as a % of Total Emissions

Share of clean/renewable electricity (%)

British Columbia

0.4

1

97.5

Alberta

32.7

13

15.1

Saskatchewan

13.9

21

14.1

Manitoba

0

0

99.8

Ontario

3.7

2

92.3

Quebec

0.3

0

99.7

New Brunswick

3.5

28

73.4

Nova Scotia

6.3

43

26.6

Prince Edward Island

0

0

99.3

Newfoundland and Labrador

1

10

97.8

Yukon

0.1

9

72.8

Northwest Territories

0.1

4

68.7

Nunavut

0.2

25

0.2

Canada

62.1

9

82.6

Source: Environment & Climate Change Canada, Canada Energy Regulator, RBC Climate Action Institute

A Role For Natural Gas

The CER consultations launched last year had sparked tensions between Ottawa and fossil-fuel reliant provinces such as Alberta—which recently announced a six-month moratorium on renewable energy projects. Other gas-powered provinces such as Saskatchewan, Ontario and Nova Scotia had also expressed concerns.

Provincial utilities worry that as more power comes from wind and solar power, it will be harder to reliably match supply and demand of electricity, risking blackouts. Ontario’s Independent Electricity System Operator (IESO) noted that 40% of severe weather events that could cause renewables outages exceeded the length of time it can store power in batteries. Rising demand and higher costs of alternatives such as energy storage or nuclear power makes the case for gas a lot stronger.

The proposed rules offer some flexibility to help alleviate those concerns and ensure natural gas has a role to play, albeit diminishing, in provincial grids:

The draft regulations require that grid-connected electricity generating units online as of 2035 with a capacity of 25 megawatts (MW) or more meet an annual average emission threshold under 30 tonnes of CO2 per gigawatt-hour (GWh) of electricity produced. An unabated gas-fired generator produces 400-500 tonnes per GWh.

For reliability, unabated peaking gas turbines can fire for up to 5% of the year without meeting an emissions performance standard. Ottawa considered allowing peakers to run more but found it decreased costs by only 2% while increasing emissions.

Natural gas turbines already in service before 2025 have 20 years of uncapped emissions before being subject to the rule (this likely will not apply to any gas units not already planned, which won’t be commissioned before 2025).

Natural gas-fired generators that install carbon capture can apply for exceptions to the emissions threshold (increasing allowed emissions to 40 tonnes/GWh on an annual average basis) for up to 7 years after commissioning the unit, to allow for capture system downtime.

“Behind-the-fence” (i.e., own-use) power generation is exempt, as are emissions associated with the heat element of combined heat-and-power systems (e.g., those used in the oil sands). They are still covered under the large emitters carbon price.

That gives gas-reliant Alberta and Saskatchewan some breathing room before they need to reduce their dependence on fossil fuels. Still, incentives are firmly nudging the provinces to transition natural gas out of the grid over time.

Provinces Take Charge

We think these are material concessions in response to provincial and industry feedback, without sacrificing the core intent of the regulations. We expect the regulations will have a significant impact on the role of unabated natural gas in the grid.

The 5% threshold for peaking is restrictive (many peakers operate above this capacity factor) but existing transition gas (e.g., Alberta’s recently grow in gas to get off coal) will be allowed to operate for at least 20 years, enough time for operators to be paid out for their investments.

Future gas baseload plants will likely be significantly challenged in areas without access to carbon storage. If the regulations come into force as proposed, gas baseload power is unlikely to offer a solution for eastern Canada without significant work to develop a carbon, capture and storage (CCS) strategy and studies of storage opportunities. Indeed, the federal government’s model sees little role of emitting generation under the regulations even with the peaker provisions, with natural gas providing somewhere between 0.5% and 1% of Canada’s electricity after 2035.

The sum of the regulations and investment tax credits from Budget 2023 would help move the needle.

Teasing a forthcoming clean electricity strategy, Ottawa suggested federal funds would be restricted to provinces that “take concrete action to achieve Net Zero.”

Indeed, provinces will likely need to publicly commit to the 2035 Net Zero Electricity goals and start cutting emissions beyond electricity. Supporting the required permitting for transmission lines, power storage projects, and carbon capture equipment will also be critical for provinces to move at an accelerated pace.

Contributors:

Lead author: Colin Guldimann, Senior Economist

RBC Climate Action InstituteMyha Truong-Regan, Head of Climate Research

Yadullah Hussain, Managing Editor

Shiplu Talukder, Digital Publishing Specialist

Caprice Biasoni, Graphic Design Specialist

rbc_toc_for_mmm_action

Ontario’s clean grid strategy, released this week, has the “all-of-the-above” vibe to it

The province is doubling down on its nuclear power prowess, keeping natural gas in play and eyeing more hydro even as it plugs in more solar and wind into the grid.

There’s a lot to like in the provincial government’s plan to meet rising long-term electricity needs. The plan to invest more in nuclear will add certainty that Ontario’s electricity grid would facilitate Net Zero goals by 2050. But its reliance on natural gas in the near term could threaten short-term climate targets.

Ontario’s “Plan For A Clean Energy Future” signals the government’s recognition that the province’s economic growth depends on more clean electricity: a greener grid would help the province attract billions of dollars in transition energy investments such as electric vehicle supply chains, decarbonizing industries, energy storage, and critical minerals. But the plan falls somewhat short in putting much of the focus on the 2040s. The province’s decision to maintain natural gas-fired power in the energy mix could set up a potential political dust-up with the federal government, which is poised to finalize its Clean Electricity Regulations.

Our key take-aways from Ontario’s clean energy plan:

Demand Surge

By 2050, Ontario’s electricity capacity—how much power the province can produce at one time—is expected to more than double to 88,000 megawatts. The province will also have to replace power generation capacity of 20,000 megawatts over the next three decades. Coupled with rising population over the next few decades, Ontario will be challenged to power the grid without raising its emissions.

The province is also attracting unprecedented investments in electric vehicle battery manufacturing, clean steelmaking and other sectors, partly as a function of subsidies, which would strain capacity. Five major investments in the new energy economy alone will increase industrial demand by 21% once online.

Nuclear Renaissance

Ontario is going big on new nuclear reactors to meet that demand. Plans to make Bruce Power Generating Station the world’s biggest nuclear site with a 4,800-megawatt expansion, announced last week, were augmented to add three innovative small modular reactors to one announced at the Darlington nuclear site in 2021.

Stand-by Source It’s what the province calls its “insurance policy.” Natural gas will continue to play a role as the Darlington and Bruce sites undergo refurbishment over the next decade (at its peak four nuclear units representing 9% of Ontario’s capacity will be offline). To that end, the province is in search of 1,500 MW of new gas generation capacity (growth of about 15%, if met). But that could upset the province’s plans to cut emissions: a recent Independent Electricity System Operator (IESO) estimate foresees nearly tripling electricity sector emissions by 2030 as gas plants stand-in for nuclear power generation in the short-term.

Facilitating Renewablese The province is procuring electricity storage, which is critical if it’s to deploy more cost-effective wind and solar power. It’s current procurement of 2,500 MW of clean energy storage is the largest battery procurement in Canada’s history. The Oneida Energy Storage Facility and Marmora Hydroelectric Pumped Storage Project are also positive developments.

But as the province’s grid integrates more renewables, a buildout of transmission lines will be critical to plug in power from remote sites. The province has not yet outlined a strategy to address that looming transmission challenge.

What’s Missing

The province has the long-term plan mostly right in our view: nuclear and hydro firming up a lot of new renewables, with some questions around peaking power from gas with carbon capture or hydrogen. Efforts to expand hydropower capacity and exploring promising low-carbon technologies such as renewable natural gas and renewable diesel will also ensure the province remains a clean-tech hub.

But a lack of near-term focus on key infrastructure is concerning. Transmission will be critical to integrate renewables, investments to facilitate electrification of households by local distribution companies will be needed to ensure the grid can handle EVs and heat pumps, and smarter technology can help facilitate more limited natural gas peaking in the near and medium term.

The plan takes some good first steps in facilitating a more flexible electricity system, by allowing consumers to access their utility data via Green Button, an energy efficiency tracking program, and considering more use of distributed energy (like rooftop solar) or energy conservation.

Ontario’s long-term nuclear investment will secure a visible path to 2050 climate goals. But the province will need to move quickly and make costs more visible to consumers if it’s to avoid major investments in emitting infrastructure over the next few years.

rbc_toc_for_mmm_action

Ontario faces a $450-billion investment bill by 2050 to meet surging demand and emerge as a green-grid hub that’s attractive to industries looking to cut or eliminate their emissions.

Rising electricity demand could strain the province’s grid as early as 2026 and even trigger chronic shortages by 2030.To meet pressing short-term needs, Ontario is eyeing more gas-fired power generation, which, unabated, could clash with the federal government’s forthcoming Clean Electricity Regulations.

The province can avoid making expensive decisions on its future energy mix by pursuing robust policy measures and incentives to save power.

Timely action to conserve energy could save enough electricity to power 3 million homes by early 2040s—a little more than half of the province’s residential electricity demand.

Readily available technologies such as smart thermostats, electric panels and AI-enabled HVAC systems that can substantially improve grid efficiency and sustainability would give Ontario the room to manage demand peaks without building new gas plants.

The measures could save Ontario ratepayers at least $500 million annually in avoided generation costs over that time.

Smart homes can unlock grid efficiencies

Tech-savvy homes could save Ontario ratepayers $500 million annually

1

Smart thermostats

2

Solar panels

3

Smart HVAC

4

Distributed battery storage for EVs

5

LED light bulbs for conservation

6

Insulation and air sealing

7

Smart electrical panel

8

Wi-Fi enabled plugs

9

Energy-efficient appliances

10

Heat Pump Water Heater

Ontario is bracing for a wave of electricity demand

The province’s rapidly growing population, electrifying industry, and aging nuclear reactors will shift the province’s electricity grid from decades of comfortable surplus to critical shortages in just a few years. By 2026, the province’s grid could strain to meet demand during peak hours; by 2030 soaring demand could outpace generation capacity.

Clearly, building more power generation is going to be unavoidable in the coming years. The Independent Electricity System Operator (IESO), which runs the province’s power market, plans to import power (primarily from Quebec), expand renewables, store power in batteries, and dabble with new nuclear reactors to meet demand. But IESO is also seeking bids for new gas-fired power plants that are vital to manage near-term capacity pressures.

The strategy could clash with Ottawa’s expected Clean Electricity Regulations (CER) that will prohibit unabated gas-fired power plants to ensure a Net Zero electricity grid by 2035.

Electricity generates 7.7% of Canada’s greenhouse gas emissions—the 6th largest source of emissions in the nation.

The country boasts one of the cleanest grids in the world, but that label is threatened as provinces such as Ontario, Alberta and Saskatchewan remain heavily dependent on natural gas and see it as a critical and reliable source to meet future demand.

The expected CER builds on federal coal regulations that stipulate phasing out unabated coal-fired electricity units by 2030, and aims to avoid grid emissions as other sectors electrify. Rising demand for electric vehicles and heat pumps, electrified steelmaking, and battery manufacturing, among other segments, will cause the grid to expand rapidly over the next few decades. Left to their own devices, some provinces have planned to add natural gas power, partially offsetting emissions cuts from these sectors.

The federal government believes recently announced electricity tax credits should offset the cost of taking gas out of the power mix or fitting it with carbon capture, but several provinces say building enough non-emitting power to meet Ottawa’s timeline is going to be difficult. Alberta and Saskatchewan who are rapidly phasing out coal as a power source, are reluctant to shut the door on natural gas without ensuring the reliability of other sources.

The CER’s rollout in its current form and timeline could set up a federal-provincial fight.

Ontario, the country’s largest economic engine and most populous province, faces the most immediate challenge.

But investing $450 billion in generation, transmission, and distribution by 2050 without knowing the scale of demand is risky.

To ensure an accelerated but orderly transition, Ontario will have to do both: boost supply, but also find other ways to manage demand in the interim.

RBC’s $2-Trillion Transition report estimates annual investment of $5.4 billion in renewable and batteries are needed to save around 11 million tonnes in electricity emissions, but natural gas will have to play a stabilizing role in ensuring an orderly energy transition.

As Ontario’s reliable generators such as nuclear plants get refurbished and coal power shuts down, more natural gas generation is the province’s preferred route. But that strategy is at odds with federal Net Zero targets: A recent IESO estimate foresees nearly tripling of emissions by the end of the decade, as gas plants meet increasing demand and declining nuclear production.

Stepping off the gas

What can the province do to bide its time and avoid making an early call on costly natural gas generation?

One way is to use policy levers to delay demand. Energy conservation can buy the province time to build large-scale, cleaner power sources such as hydro and nuclear instead of gas, saving money long-term, as we wrote in Price of Power last year.

Deferring hefty financial commitments will keep electricity affordable and gives Ontario time to redefine itself as a low-carbon manufacturing hub that attracts companies involved in electric car supply chains, green metal production, and clean-tech.

The good news: technology exists that Ontario can use to navigate the looming demand rush and delay committing to natural gas-powered generation. Changing consumer attitudes and behaviours to promote flexible demand and energy efficiency will also be key to unlocking significant savings and alleviating grid pressures.

By 2040, Ontario could meet nearly 20% of its electricity demand growth via economically viable conservation

Electricity conservation is often overlooked, since it has done little to cut emissions in Ontario’s already-green grid, but it could emerge as a vital policy lever to avoid new gas plants. By 2040, Ontario could meet nearly 20% of its expected demand growth—or 28 terawatt-hour (TWh)—via economically viable conservation. Doing so could save Ontario ratepayers at least $500 million annually by 2040.

It’s worked before. Over the past two decades, albeit against slowing demand growth, IESO’s conservation programs have outpaced demand. By funding retrofits and LED lighting, among other actions, electricity conservation doubled between 2014 and 2021, from 11 TWh to nearly 22 TWh. Demand grew just 7 TWh in comparison.

To maximize potential, Ontario will need to leverage technology to shift peaks to avoid building more capacity now.

Smart tech to the grid’s rescue

Ontario can build on its reputation as a leader in grid innovation to support smart energy use. It’s one of the only jurisdictions globally that has a smart meter installed in nearly every home. That’s allowed the province’s widespread time-of-use pricing policy to manage peak demand.

Flexible demand can also respond better to variable zero-emitting sources, like wind and solar. Given the right financial incentives that inspire attitude change, consumers may be prompted to install home solar panels, smart thermostats and smart electrical panels that can improve grid efficiency.

Currently, Ontario’s centralized grid system is underutilizing these technologies. Here are a few ways the province can leverage new technologies.

Make it pay: EV owners save money when they charge their cars overnight. But what if they could use it themselves when they turn on their induction stove or sell the leftover power in their car back to the grid? Our research suggests EV owners could earn as much as $100 per month. Those payments could offset distribution upgrade costs for households, although infrastructure upgrades will be needed to facilitate the new vehicle-to-grid technology. Set right, they can save the province money, too, since storing power in EVs may be cheaper than single-use utility-scale batteries. Giving consumers the right price signals can facilitate more responsive demand.

Make it smart: Home monitoring systems attached to electrical or smart panels can combine with Wi-Fi-enabled plugs and smart thermostats to remotely control appliances, lights, heating and cooling to avoid electricity peaks. In Montreal, start-up Brainbox’s artificial intelligence software cut electricity use 10% in a major office tower by weeding out inefficiencies in the system.

Make it responsive: With smarter systems in place, electrical panels can alert consumers that the dryer they just turned on is more economical to run in an hour. Or when the system predicts new peaks, smart water heaters could pre-heat and store hot water for later in the day. This could be key to managing a grid that’s increasingly reliant on variable renewable power.

Make it accessible: Ontario’s current demand response programs focus on paying industry and large buildings to cut demand during peaks. Finding ways to encourage widespread, distributed adoption of these technologies can help consumers benefit (and get paid) for the services they can provide to the grid, easing the cost of electrification.

Make it cost-effective: Traditional energy efficiency can also ease the strain on Ontario’s grid. Think analog solutions like LED light bulbs, energy-efficient appliances, efficient pool pumps for homeowners. Retrofit programs will also need to be scaled up, with support from IESO.

Actions for a green & efficient grid

Ontario is in an enviable position to get electricity consumers to change behaviour. Adjustments to time-of-use pricing are already set to shift demand away from peaks. But with overnight set as the cheapest rate, consumers may not be willing to alter behaviour beyond EV charging.

A well-established track record of successful efficiency programs does not mean consumers will invest in retrofits without education or financial incentives. The key will be to help consumers understand the cost of their actions and price them sufficiently to change behaviour. We’ll need to support household investments in technologies to get there faster and assist lower income households through transition.

The action points below should ideally be pursued together to maximize benefits for consumers, industry and the province.

Ideas to move forward

Ontario’s Ministry of Energy should direct IESO to ramp up and expand cost-effective energy efficiency programming.

Energy efficiency programs should finance low-income households’ adoption of smart technologies such as panels, thermostats, and water heaters to ensure they can benefit from new rate structure.

Economic incentives in existing time-of-use pricing structure are not large enough to nudge consumers to shift their energy consumption to off-peak and mid-peak hours. After supporting tech adoption and real-time pricing feedback, the Ontario Energy Board should introduce higher on-peak rates and set time-of-use pricing as a default, with financial support for low-income households.

Utilities should take a more consumer-minded approach to pricing that clearly communicates to ratepayers the pricing consequences of their electricity use patterns.

As a policy default, allow homeowners and building operators with onsite renewable power generation capacity to sell surplus power back to the electricity grid during peak demand.

Future electricity subsidies from all levels of government should not be focused on subsidizing more generation, regardless of cleanliness. Rather they should support adoption of new technologies to make the grid smarter and accelerate behaviour changes.

Lead author: Colin Guldimann, Senior Economist, RBC Climate Action Institute

RBC Climate Action InstituteMyha Truong-Regan, Head of Climate Research

Yadullah Hussain, Managing Editor

Darren Chow, Senior Manager, Digital Media

Shiplu Talukder, Digital Publishing Specialist

rbc_toc_for_mmm_action

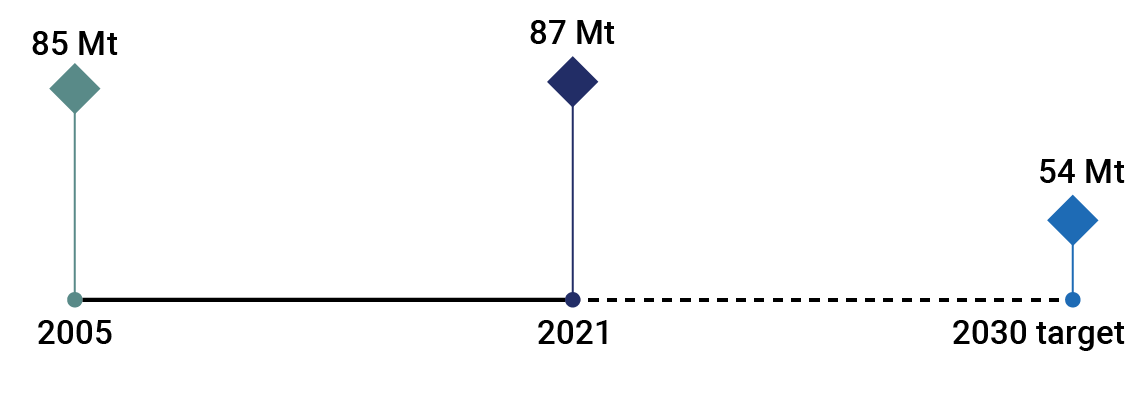

Scaling down Canada’s emissions rapidly to 440 Mt by 2030 will require cuts equal to around four times the drop seen during the pandemic.

Canada’s latest National Inventory Report highlights the progress made on curbing greenhouse gas emissions but also the distance that needs to be covered to reach climate targets.

Canadian GHG emissions stood at 670 million tonnes (Mt) in 2021, a 54-Mt contraction from pre-pandemic levels, but 1.8% above the 2020 lows. Scaling down Canada’s emissions rapidly to 440 Mt by 2030 will require cuts equal to around four times the drop seen during the pandemic. While emissions were 8.5% lower from the 2005 benchmark, achieving the federal government’s target of 40% lower emissions by 2030, as set out in the Emissions Reduction Plan (ERP), would require greater effort.

Encouragingly, existing policies have moved the needle: the coal phase-out triggered the largest cuts in the country, while methane reduction policies appear to have a lasting impact, pointing to policy efficacy. Spearheaded by the ERP, further cuts could be driven by recently announced climate policies such as investment tax credits for cleaner fuels, the proposed Clean Electricity Regulations and Oil and Gas Emissions Cap. Carbon pricing remains the cornerstone of the government’s emissions drive, and its continued rollout will be critical to hitting 2030 targets.

Here’s a look at how some of Canada’s most carbon-intensive sectors are managing their emissions:

Oil & Gas

Oil & gas is charged with cutting emissions by 73 Mt—the single largest cut in terms of volume among sectors to meet Canada’s 2030 targets.

A relatively cheaper fix for methane leaks combined with stringent government policies will help in cutting another 23 Mt.

Carbon capture, utilization and storage (CCUS) capacity is projected to reach 30 Mt CO2e per year by 2030, consistent with ERP expectations. If realized, the technology will deliver half the cuts needed to reach the target.

New oil and gas related projects valued at $200 billion would require additional heavy investments in abatement technologies such as CCUS to manage emissions.

Industry would need to quickly develop and deploy more abatement technologies and identify electrification opportunities across the value chain.

Path to 2030: The proposed oil and gas emissions cap policy is designed to slow and limit emissions, while investment tax credits could potentially bolster additional CCUS capacity.

Transportation

Canadian car fleet, accounting for half of transport emissions, grew 30% in past 15 years to reach 24 million. That’s pushed emissions higher despite improved fuel efficiency and exhaust systems.

Zero-emission vehicle (ZEV) registration is growing, but at a 1% market share (in 2021), the stock has yet to make a dent in emissions.

At current pace, Canada is expected to achieve 40% ZEV sales of the total market by 2030—short of its stated 60% target. ZEVs would make up 17% of the total Canadian car fleet.

Pandemic lockdowns saw a 27 MT drop in emissions in 2020, but traffic levels returning to pre-pandemic levels would likely see sector emissions rebound.

Path to 2030: Auto makers will need to accelerate EV development and offer consumers more choices to comply with ZEV sales target of 60% of total car sales by 2030 and 100% by 2035. Boosting the stock of emissions-free cars could tip the emissions scale later in 2030s.

Electricity

A major coal phase-out drove emissions lower in Ontario and Alberta over the past decade. Ontario’s emissions fell rapidly as it expanded its clean energy infrastructure, but maintaining a low-emissions grid is a challenge as its economy and population grows. Meanwhile, Alberta’s electricity emissions declined largely due to a switch from coal to natural gas. Expanding its promising renewables infrastructure will be key in bringing emissions down further.

Nationally, continuing coal phase-out will provide just under half of the required 38 Mt reduction (assuming coal-to-natural-gas transition).

Additional challenges lie in meeting rapidly increasing electricity demand, grid upgrades, and dependence on stable sources.

Meeting new demand entirely with natural gas could potentially push the progress back by 30 Mt.

Path to 2030: The proposed Clean Electricity Regulations could facilitate the deployment of cleaner energy sources to curb emissions from rising demand, and lay the foundation of a low-emissions infrastructure to replace retiring plants.

Buildings

Population growth and expanding floor space is driving building emissions faster than energy efficiency can offset. Housing demand is also unlikely to relent any time soon.

In half the provinces, the sector is emitting at above 2005 levels. Many regions remain highly reliant on fossil fuels as a heating source and require heavy investments to switch to cleaner fuels.

The sector requires a massive 33 Mt reduction to meet 2030 targets, a 39% decline from current levels.

Path to 2030: Retrofit grant and loan programs have struggled with low pick-up rates. Retrofitting 30% of existing real estate—, an immense challenge and expensive endeavour,—would take us only halfway to our target. Complex set of measures, including but not limited to stronger incentives and stringent regulations, could lead the way past 2030.

Conclusion

Emissions in half the provinces are trending either at above or close to the 2005 stating point, as each region grapples with its own set of unique challenges. Despite higher emissions in carbon-intensive provinces, they will likely see relatively faster cuts in the near term as current policies continue to deliver results, mainly due to methane reduction. Ontario and Quebec made headway in cutting emissions over the past two decades but will enter a slower reduction phase as they tackle the more challenging transport and buildings sectors.

A few key measures drove emission cuts over the past two decades, but further reductions will require greater provincial and federal focus—and co-operation. Emissions rising in tandem with an economic recovery could also prove to be a headwind. However, the emerging trend of economic growth decoupling from emissions and Canada’s willingness to implement tough climate policies are grounds for some optimism.

Farhad Panahovis an economist at RBC. He holds a BSc in Economics from the University of British Columbia, and Master of Applied Science in Data, Economics, and Development Policy from the Massachusetts Institute of Technology.

rbc_toc_for_mmm_action

Natural gas currently presents one of Canada’s biggest climate choices

Expansion of the abundant resource could unlock a fresh wave of economic activity and help cut global emissions. But we risk missing our Net Zero targets without major investments in abatement technologies.

As major energy importers Japan and Germany eye Canadian natural gas, federal and provincial policymakers are wrestling with a conundrum: Turn them away and risk more global energy volatility or tap British Columbia and Alberta gas and leave Canada’s economy more exposed to shifts in the global gas outlook.

The Japan-led G7 Summit in May will struggle with this twin challenge of managing energy and climate security. The group of the world’s richest countries are still debating natural gas’s role in ensuring market stability. A strategic energy alliance that protects the group’s long-term economic prosperity and climate ambitions would bring some clarity to the path forward.

Here are three roles Canada can play:

The Gulf Coast Gas Exporter: Ramp up natural gas exports to the U.S. Gulf Coast liquefied natural gas producers, which is developing a number of gas-exporting projects. The strategy may raise Canada’s upstream gas sector emissions by up to 7%.

The Strategic Exporter: Carve a niche in global LNG markets as a strategic supplier of stable, low-emissions gas. A handful of projects could potentially reduce global emissions by a net 105 MtCO2e—roughly equivalent to Qatar’s total GHG emissions, but would also raise Canadian gas sector emissions by a third assuming current technologies. However, most of the upstream gas emissions and nearly a third of LNG terminal emissions could be abated with electrification and other technologies. The strategy would attract a projected $133 billion in capital investment into the Canadian economy over 40 years.

The West Coast Hub: Build out LNG capacity to its full potential, taking a more assertive role in global natural gas markets. The strategy could reduce net global emissions by as much as 211 MtCO2e but raise the Canadian sector’s emissions by 66%. The strategy would attract more than $200 billion in investments.

Each path carries economic and climate risks that Canadian policymakers and industry must weigh. And fast. Global LNG markets are restructuring, opening fresh opportunities for West Coast projects. But that window won’t be open for long.

Canada’s Choices for Supporting Global Energy Security

Asia Key To Long-Term Demand As LNG Investors Eye New Investments

Getting to Net Zero requires the world to cut fossil fuel consumption, including natural gas. But we’re not there yet. Even as wind and solar farms spring up around the world, LNG—natural gas cooled to -162°C to 1/600th of its original volume to ship over long distances cheaply—is gaining fresh momentum. A key reason: cleaner-burning natural gas often means lower emissions than oil or coal.

Europe has demonstrated LNG’s value with its frantic dash to replace piped Russian gas, importing the equivalent of 10% of LNG trade in 2021, mostly from the U.S.

Though the EU remains intent on transitioning to a clean energy economy, for now it’s rushing to build new regasification terminals. Meanwhile, natural gas is part of the EU taxonomy for sustainable activities—albeit under strict conditions including no unabated natural gas in power generation beyond 2035. If carbon capture technology for gas abatement evolves constructively, gas could be a player in European energy for longer.

While gas will remain in the mix in Europe and other advanced economies for some time, it’s clear that future demand will decline as these economies build cleaner energy infrastructure.

Natural Gas is a cleaner-burning fossil fuel

Asia, on the other hand, will have a harder time turning away from natural gas. As one of the world’s biggest LNG importers, Japan is alarmed by its dependence on Russian and Middle Eastern countries as well as new export limits proposed by major LNG supplier Australia. It’s encouraging the development of nuclear energy, hydrogen and natural gas as part of this year’s G7 agenda.

LNG will also remain an essential fuel in China, India and other populous countries of South Asia and Southeast Asia as these countries seek to meet growing energy demand while reducing a strong reliance on coal to meet climate commitments. China, India and Southeast Asia will see gas demand grow by around 44% by 2050 in the International Energy Agency’s base case scenario. LNG would take the bulk of the growth with declining local pipeline-based production.

But it’s hardly a full-blown bull case for gas. Stunned by last year’s five-fold jump in LNG prices, many Asian countries raised their coal consumption, while others pivoted to renewables, especially as the economics of switching directly from coal to clean energy in Asia improved dramatically. Non-emitting energy rollout may take a while to gain traction in Asia, but it’s still a cloud hanging over the long-term gas outlook.

Emerging markets driving gas demand

Global LNG markets remain tight. But gas exporters are responding to high price signals with a raft of proposed projects from LNG heavyweights, including the U.S. and Qatar.Globally, more than 100 megatonnes per annum (MTPA) of new LNG supply could be approved before 2024, adding 17% to the global LNG market. Another 1,035 MTPA are in pre-final investment decision stage, but the International Gas Union believes “a fair portion” are unlikely to proceed given investor focus on capital discipline and a reluctance to invest in long-term projects in an uncertain global energy market. There are also question marks hovering over Russia’s new planned LNG capacity, given the spate of Western sanctions and departure of oil and gas majors from the country.With a strong market outlook in the medium term but possibly much weaker in the long-term, would 25 to 40-year Canadian LNG liquefaction capacity investments be profitable?

Canada’s Proposition

LNG Canada Phase I, a large B.C. export facility backed by Royal Dutch Shell, Malaysia’s Petronas BHD, PetroChina Co., Japan’s Mitsubishi Corp. and Korea Gas Corp. will mark Canada’s first meaningful entry in global LNG markets by mid-decade. The project’s capacity of 14 MTPA will place Canada among the top 10 largest LNG exporters in one fell swoop. Woodfibre LNG and Cedar LNG, with a combined capacity of up to 6 MTPA, are advancing toward development.

Global majors are certainly taking another look at new West Coast projects, drawn by the demand for diversified gas suppliers and some compelling advantages:

Canada is the world’s 4th largest natural gas producer, and home to a huge concentration of conventional and unconventional natural gas reserves.

The Montney shale basin straddling Alberta and B.C.—about the size of New Brunswick and Nova Scotia combined—can potentially produce 449 trillion cubic feet of natural gas, nearly six times Canada’s conventional gas reserves. And Montney reserves are relatively cheap: a 2018 study found 200 years supply in the basin below $2.50 per million British thermal units breakeven.[1]

B.C. projects are about 10 shipping days from Asia, compared to 20 for U.S. Gulf Coast exporters via the tolled Panama Canal, reducing both costs and emissions. The only major active U.S. West Coast LNG project is the federally-approved US$39-billion Alaska project.

Canada’s world-leading methane regulations, naturally low formation CO2 in the Montney, and promise of clean electricity supply is prized by global producers eager to reduce their greenhouse gas emissions. Two proposed Canadian LNG projects are majority-backed by Indigenous groups, suggesting strong local support.

Distance To Asia

Nautical miles

Source: Oxford Energy Institute

Still, several challenges cloud the cost and profitability picture. Canada’s capital costs for greenfield projects are relatively high and it’s unclear whether foreign consumers are willing to pay added costs for diversified energy supplies. While Canada has existing attributes that can drive a lower emissions profile for its LNG, new oil and gas climate policies requiring rapid industry-led decarbonization could add significantly to costs.

How Canadian LNG projects stack up against rivals

CAD/Mbtu

Here are three ways Canada can support global energy and environmental security.

Scenario 1: The Gulf Coast Gas Exporter

The U.S.’s expeditious LNG buildout serves as an opening for Western Canadian natural gas producers. Canada’s low-cost, plentiful gas resources and investment grade companies are attractive to many U.S. LNG projects competing for stable gas supplies.

Canadian companies have secured supply agreements of 0.3 billion cubic feet per day (bcf/d) with U.S. LNG exporters. Growing these agreements to 1 bcf/d would give Canadian companies exposure to global pricing with limited capital risk.

Given the abundance of Western Canadian natural gas, higher U.S.-bound gas exports may not raise production. But if it did, Canadian emissions would increase by 2% relative to current oil and gas sector emissions. That’s directionally opposite to Canada’s stated goal to cut emissions from the sector by 42% by 2030.

Being a Gulf Coast exporter is not a growth strategy. U.S. LNG could be well supplied with domestic gas reserves over the long-term, new cross-border and interstate pipelines to the Gulf Coast will be difficult to build, and pricing premiums could be captured by other players.

Without sufficient pipeline capacity to the U.S. or Eastern Canada, or LNG to international markets, the value of Canadian gas resources will continue to be diminished. The result of flooded local markets: Canadian natural gas benchmarks priced at a discount to U.S. and international benchmarks.

Canadian gas priced at a discount to major benchmarks

USD/Mbtu

Scenario 2: The Strategic Exporter

Canada could take a more deliberate role in stabilizing global energy markets, with new LNG capacity of 40 MTPA, or about 7% of current global supply2. Exporting gas could ramp up trade and investment ties with strategic Trans-Pacific economies.

Proposed LNG facilities or those entering the environmental assessment process must demonstrate a credible Net Zero plan by 2030, according to new B.C. rules. Canada’s low emissions and relatively high environmental, social and governance standards would differentiate its gas for markets willing to pay premium prices.

Global emissions could fall. Canadian West Coast LNG shipped to China can produce less than half the lifecycle emissions per unit of electricity generated compared to the Chinese average, if it displaces coal fired generation. 3

The Paris Accord’s Article 6 international centralized emissions trading system—which would verify LNG’s displacement of coal and give Canada credit for global emissions reductions—is years away.

Major decarbonization of Canadian gas and LNG is technologically feasible and able to abate up to 90% of upstream gas emissions, while full electrification of LNG terminals can cut emissions by 63% compared to electrification for only non-compression systems (as in LNG Canada Phase I). This could add at least $0.7 per Mbtu to producer costs, raising Canadian supply cost.

Electricity demand for low-emissions LNG terminals and gas supplies would require major new generation and transmission infrastructure. Estimates of terminal electricity demand vary, but could translate into about 10% of BC’s current total electricity generation for every 20 MTPA of LNG—enough to power up to 2 million electric vehicles.4While BC will require new LNG projects entering the environmental assessment process to be Net Zero by 2030, BC Hydro has not yet set out clear provincial electrification plans, leaving a narrow window for new LNG investments.

Governments could collect substantial royalty and tax revenues from new LNG projects, but with the uncertain long term gas outlook, governments may be asked to pitch in with fiscal incentives to attract new projects, effectively subsidizing allied consumers to ensure energy security.

Exporting gas to Trans-Pacific economies would strengthen Canada’s Indo-Pacific investment and trade strategy.

Various – leak detection & repair, blowdown capture, replace pumps, etc.

68%

$1,900

CO2 Venting

17%

Carbon capture

70%

$158,000

Flaring

4%

Collection & compression of gas into pipelines

90%

$5,700

Total upstream gas sector emissions = 50 MtCO2e

Source: 2022 National Inventory Report, B.C. Ministry of the Environment, IEA methane tracker, RBC’s $2 Trillion Transition, industry consultation

Scenario 3: The West Coast Hub

By building up to 13% of current global LNG capacity and increasing natural gas production by 60%, Canada could become a global LNG player. But Canada’s high greenfield development and major decarbonization costs would make building clean, competitive LNG supply at scale a tall order.

Gas sector emissions would rise 60%, assuming current technologies. Canada would likely need to provide leeway in domestic sectoral emission targets, given steep decarbonizing costs and difficulty finding sufficient international buyers willing to engage in bilateral emissions trading.

To keep supply costs competitive and reduce sectoral emissions, new projects could require major fiscal incentives or taxpayer investment in electricity infrastructure. Governments could participate more in the financial upside of new projects, earmarking royalty and tax revenues in this high-risk, high-reward strategy for aggressive domestic decarbonization of non-gas sectors.

A massive buildout of natural gas could hurt Canada’s reputation as a climate champion. Without consent of Indigenous groups on whose lands most of Montney straddles, upstream gas supplies may have difficulty expanding sufficiently.

A larger natural gas sector provides a partial hedge against Canada’s oil sector. However, Canada’s economy would be exposed to transition risk if pessimistic natural gas forecasts play out, as more economic activity is exposed to fossil fuels. Stranded gas assets would cease to generate public economic benefits despite historical emissions allowances or taxpayer supports.

Nisga’a Nation, Rockies LNG (Advantage, Birchcliff, Bonavista, NuVista, Paramount Resources & Peyto) and US based Western LNG

Pearse Island, NW coast of BC

(Nisga’a Nation land)

Environmental Assessment Decision in progress

12

Woodfibre LNG

Pacific Energy Corp. (Singapore)/Enbridge (30%)

Squamish, BC

Approved

2.1

Tilbury Phase 2 Expansion

Fortis BC

Tilbury Island, BC

Environmental Assessment Decision in progress

2.5

Under construction; all other projects pre-FID (final investment decision)

Source: Project websites, RBC Economics

Ideas to Move Forward

LNG is one of the toughest economic and climate choices for Canada – tremendous upside and downside risks abound on both sides.

The country has historically avoided definitive moves on LNG, which led to a rash of abandoned projects a decade ago. The stakes are only higher now, so Canada cannot dither and be locked into a future decided by chance.

Canada needs to set clear guardrails for its domestic LNG industry, finding the right roles for industry, government, electricity ratepayers, and foreign consumers to best manage its preferred balance of climate and economic risks. Regardless of the outcome Canada aims for, there are key elements missing in the policy framework and industry playbook that will compromise Canada’s ability to move forward at all.

This is where we could start.

Canada should drive high standards in bilateral emissions trading agreements under the Paris Accord’s Article 6, with the federal government leading the development of robust frameworks through the G7. Canada’s forthcoming sustainable finance taxonomy could include flexibility for long-lived LNG transition assets where tied to verified global emissions reductions.

The federal government should deliver on promises to fast-track major project approvals and streamline regulatory assessment processes, including working with provinces on assuring a single process per project.

Industry should seek to expand gas takeaway capacity with existing infrastructure, including investment-grade Canadian operators securing more long-term supply agreements with U.S. LNG developers, investments by midstream companies to optimize pipeline capacity, and gas majors working with pipeline companies to resolve their frequent contract disputes.

Sponsors of new LNG projects should improve their cost profile by leveraging pipeline or scale efficiencies, leaning on more modular technologies, and proactively managing skilled labour and supply chain constraints.

Federal and provincial governments should set clearer decarbonization targets for the gas and LNG industry. Their support for sectoral decarbonization should be made clear and scale with Canada’s view of how the sector supports global energy security. The industry needs to deliver on emissions reductions.

BC Hydro should quickly establish a clear electrification strategy and timetable that helps guide private sector investments in electrification of the sector. Review of the pricing framework for industrial users should appropriately distribute the costs of grid expansion.

Federal and provincial governments should roll out broad-based supports for Indigenous communities to purchase equity in major projects, including LNG infrastructure, addressing a historic gap in access to capital that has eroded project support and slowed development.

Industry and government actively communicate Canada’s framework for LNG development internationally, so global investors understand Canada’s relative advantages and openness to investment.

Cynthia Leach, Assistant Chief Economist, Thought Leadership, Royal Bank of CanadaYadullah Hussain, Managing Editor, RBC Climate Action Institute, Royal Bank of Canada

LNG capacity in mtpa is converted to gas production in bcf/day by assuming a capacity utilization of 80%, multiplying by the LNG-to-gas (bcf) conversion factor of 48.0279, and then dividing by 365. This value is then grossed up to account for fuel use of the LNG terminal, assuming the specifications of LNG Canada Phase I .