Also in this edition: Breaking down six under-the-radar trade themes and a deep dive on four strategically significant industries that could drive U.S.-Canada relationship going forward

Overheard

With the CUSMA deadline looming and rhetoric heating up (“We don’t need anything Canada has,” President Donald Trump told reporters earlier this week) more than 300 senior business and government leaders from both sides of the border gathered in Toronto for the RBC and Eurasia Group’s US-Canada Summit.

Here are some highlights:

-

Robert Lighthizer, the 18th United States Trade Representative, argued why 50 years of trade deficits left the U.S. no choice but to impose tariffs. And why, despite not being the worst offender, Canada was a target. In a democratic political system, a government doesn’t have years to address an issue, he said. It needs to act quickly. As for where things go with tariffs from here, Lighthizer didn’t mince words: “Nobody here has a grandchild in whose lifetime America is going to be free trade.”

-

Regardless, it’s up to Canada to put on its “sales hat” said Pete Hoekstra. Though the U.S. Ambassador to Canada said potash is about the only thing the U.S. needs from Canada, the U.S. is open to offers. Hoekstra pointed to autos and oil, and even offered some points to help make Canada’s case: the countries have similar pay scales, labour standards, and a thoroughly integrated ecosystem.

-

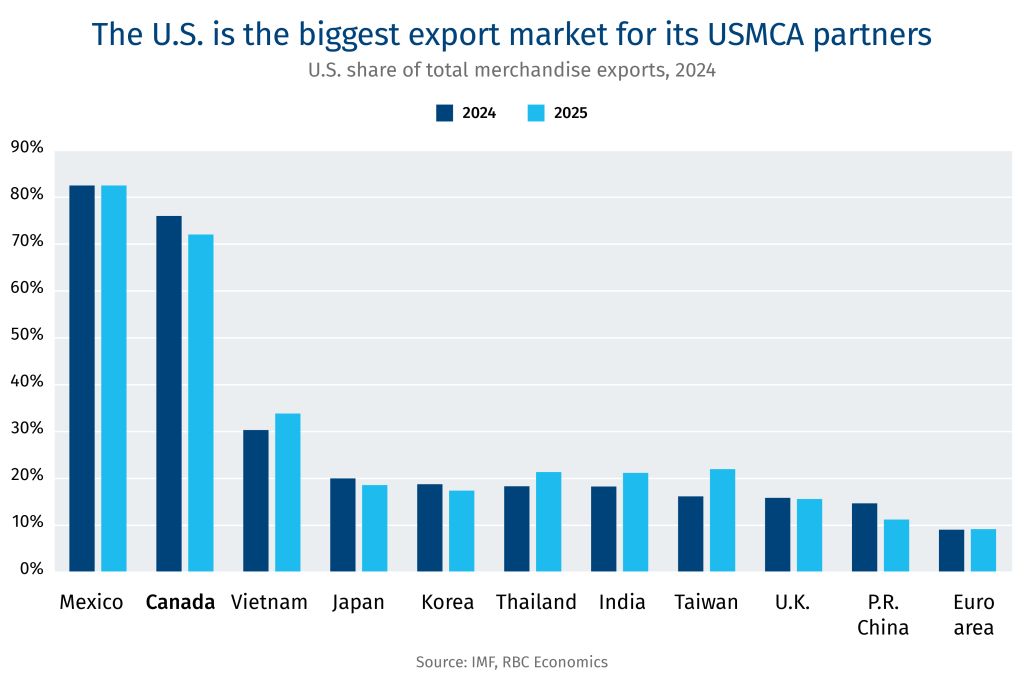

“America First doesn’t mean America Alone,” said Mark Wiseman, Canada’s Ambassador to the U.S., who added that Canadians are not always good at reminding Americans about the importance of Canada. Remind them of what exactly? For starters: Canada is the largest buyer of U.S. cars, outside the U.S. The No. 1 export market for 30 states. And in the top 3 for almost every state. And Canadians, on per capita basis, buy 40x more American goods than the EU, China and India.

-

Dominic LeBlanc, Minister for Canada-U.S. Trade, noted that the Canadian government has put some proposals forward to the Trump administration—but is also building a Canadian economy that is strong and resilient. Canada is not an “idle spectator.”

-

Wiseman, along with Michael Sabia, the Clerk of the Privy Council and Secretary to the Cabinet, were clear that the government’s diversification efforts do not equate to decoupling from its largest trade partner. It’s ‘and’ not ‘or’. A stronger Canada, they both noted, is a stronger partner for the U.S.

-

Hoekstra didn’t disagree, noting that if Canada is a rich country, maybe a few of those dollars could flow south—maybe to Michigan (“in the summer”), Florida and Arizona. He also joked about Kentucky bourbon, which has been removed by several provinces amid the trade war: “If you need some, I’ll see that you get some.”

A new nexus

After decades of economic co-operation comes a trade shock from the U.S. side. In a report in the runup to the U.S.-Canada Summit, Frances Donald, Senior Vice President and Chief Economist at RBC Economics, notes that the bruised U.S.-Canada ties have uncovered several under-the-radar trade themes. Here are a few worth highlighting:

-

Global trade growth rate doubled without the U.S. Rather than break the global economy, the rest of the world is re-orienting around the U.S. market.

-

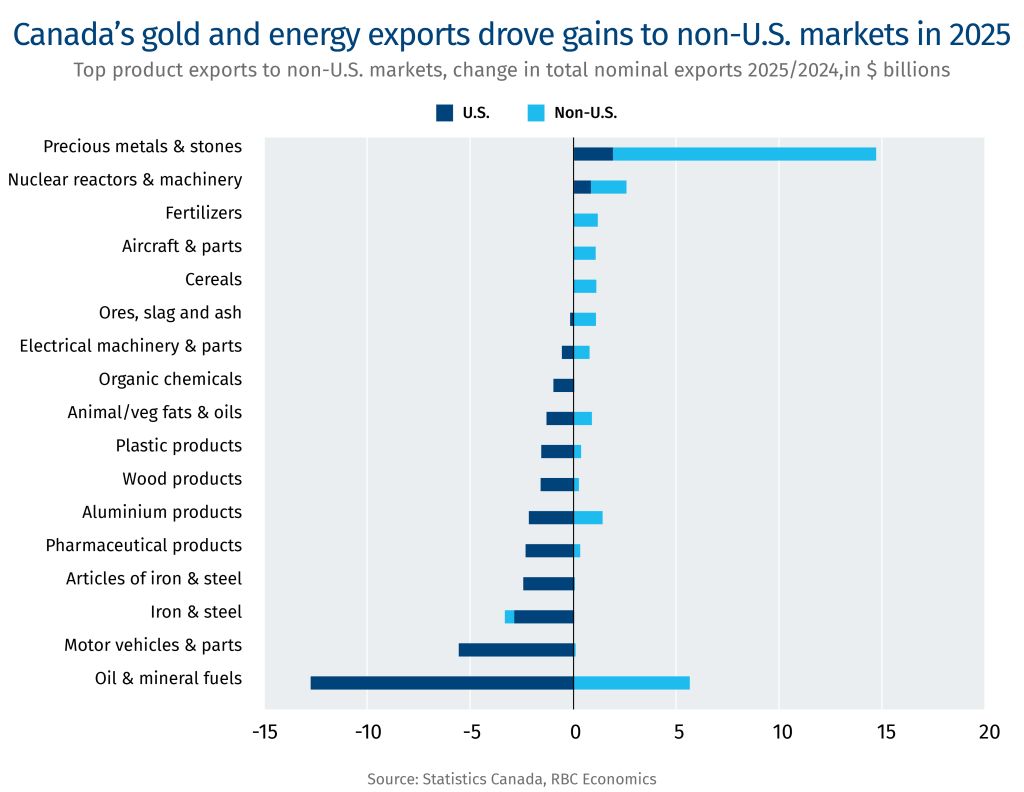

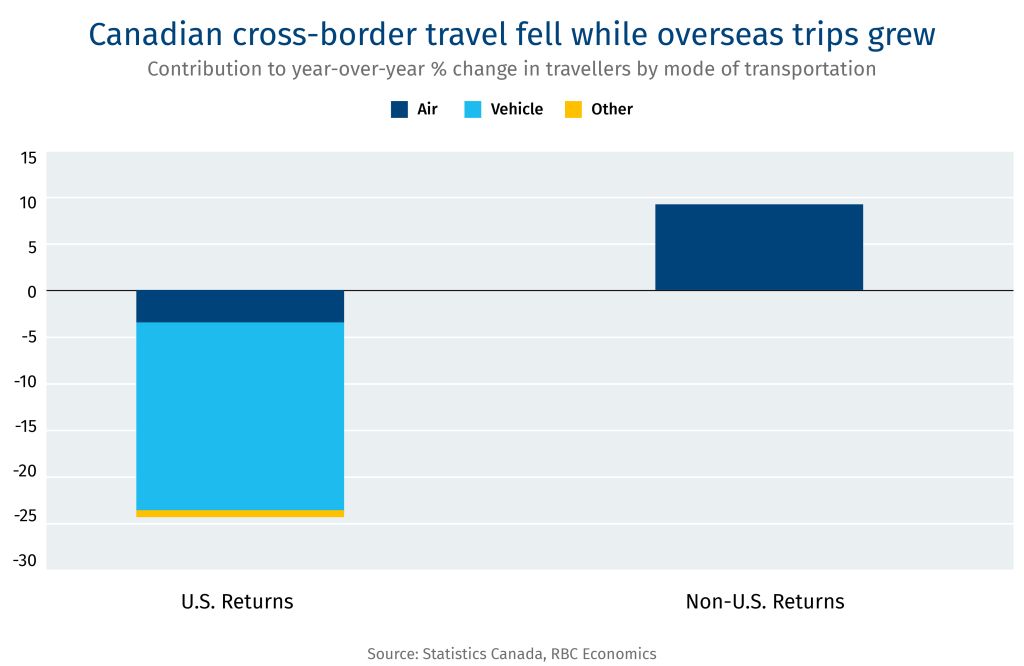

The year of Canada’s trade divergence. Higher gold prices helped Canada boost exports to other markets, even as shipments to the U.S. fell 6% in 2025.

-

Canadians have taken economic protection into their own hands. Cutting U.S. travel, boycotting American-made liquor, and seeking out domestic products showed Canadian resolve.

-

Canada added more jobs than the U.S. in 2025. While 68% of Canadian exports are headed for the U.S., only 12% of jobs are dependent on U.S. demand.

Read Frances Donald’s full briefing here.

Aligning the stars

It’s the world’s largest bilateral trade relationship—but it’s now under strain. Jordan Brennan, RBC Thought Leadership’s Managing Director, identified four strategically significant industries, which could drive U.S.-Canada relationship going forward.

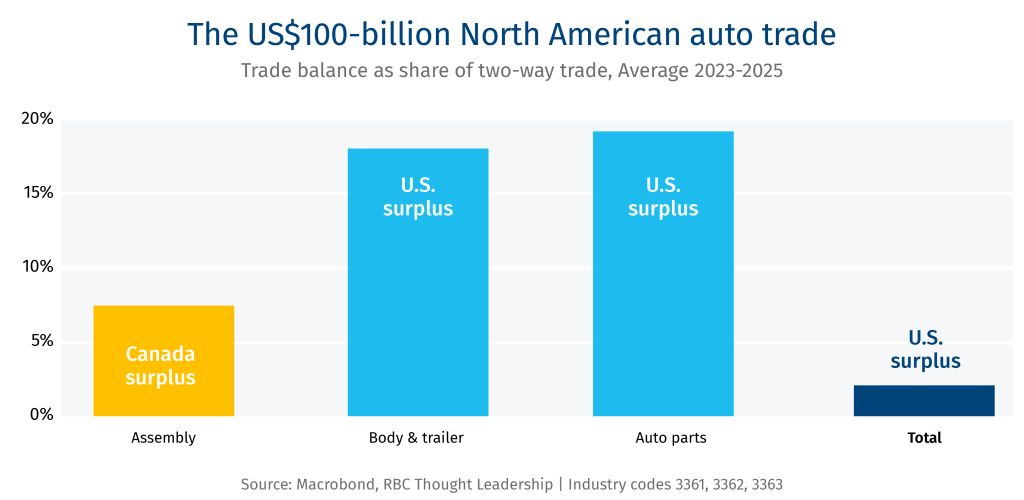

Auto Manufacturing: Build on the already-integrated nature of the industry by harnessing Canadian clean power, aluminum, and critical minerals with American capital markets, OEM headquarters, and consumer demand.

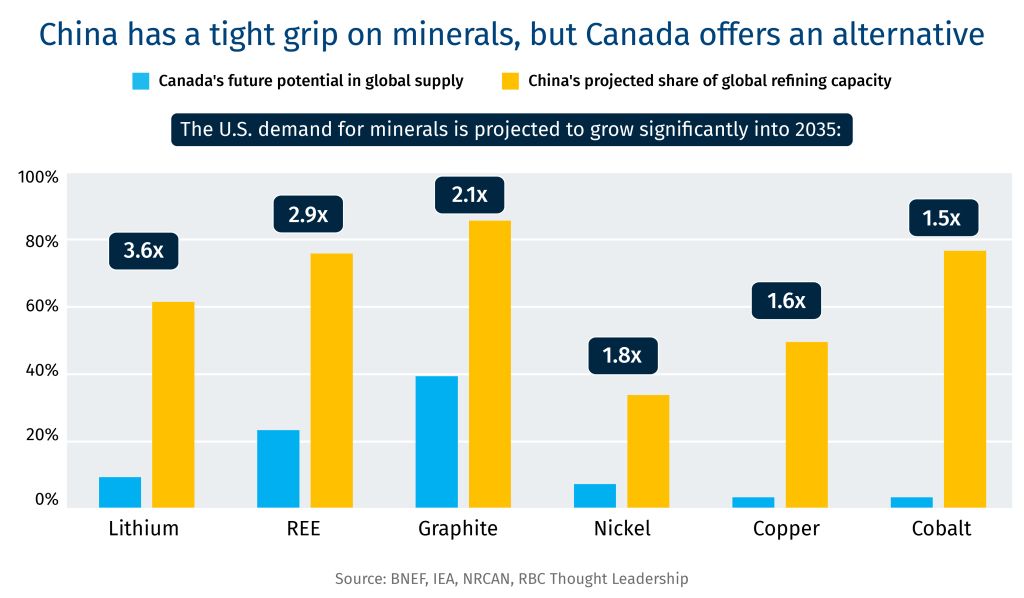

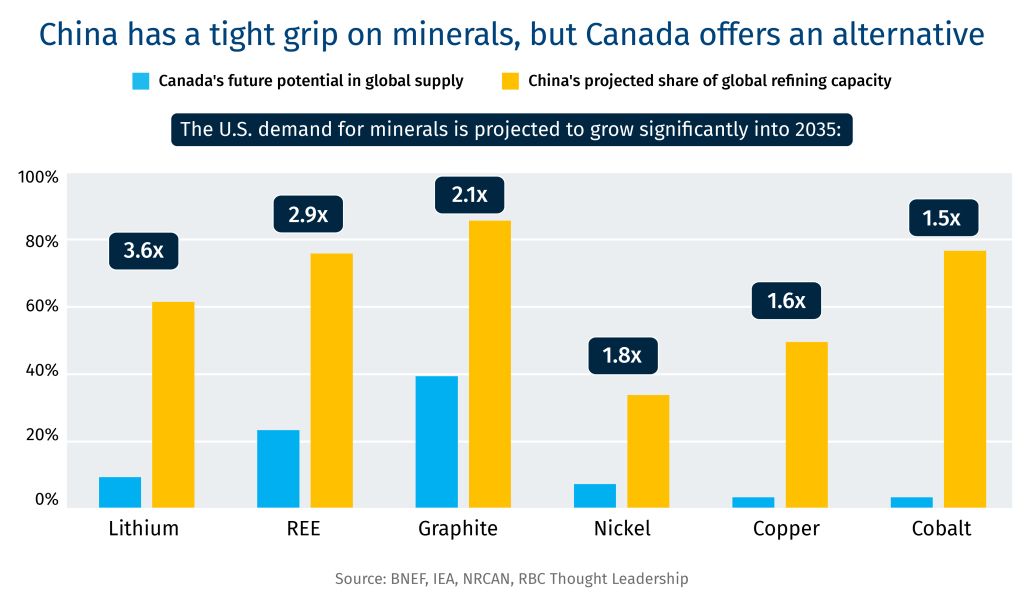

Critical Minerals: Tie Canadian geology and mining with American financing and manufacturing demand, to deepen supply chain resilience and dependence on China-controlled minerals.

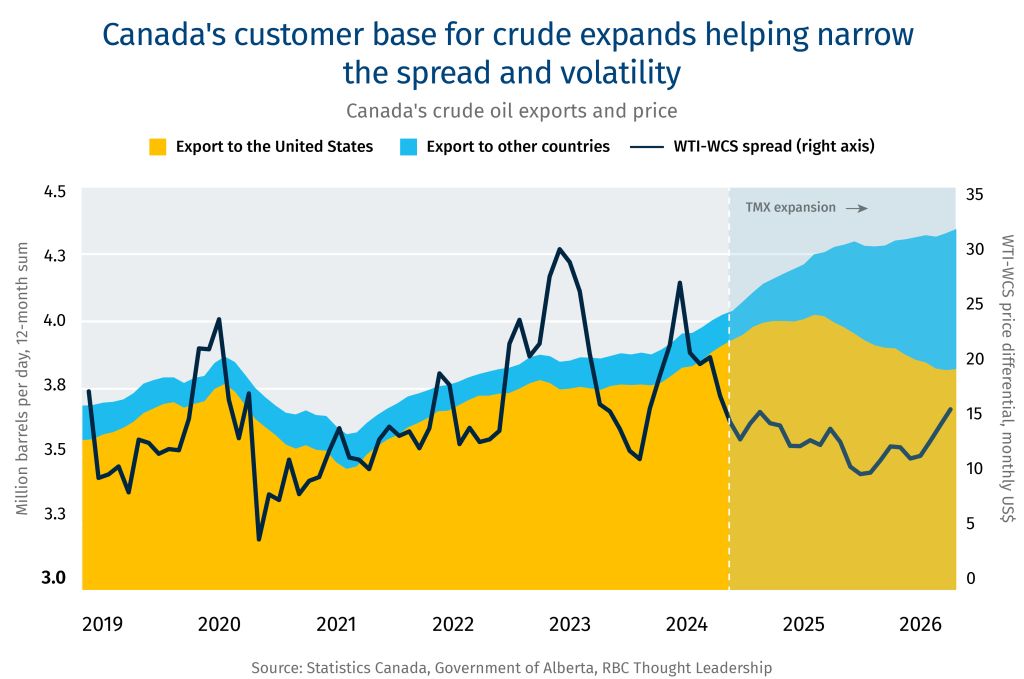

Oil and Gas: Match Canada’s significant oil and gas resources, pipeline infrastructure, and tidewater access with U.S. refining capacity and capital markets to deliver affordable energy domestically—and to the world.

Defence: Combine American capital depth, technological sophistication, and R&D expenditure, with Canada’s geographic depth and world-class capabilities in sensors, avionics, satellite technology, and training and simulation to surveil and defend the continent.

Read Jordan Brennan’s full briefing here.