Canada and the United States are bound by the world’s largest bilateral trade relationship—one now under unprecedented strain. In what follows, we focus on four strategically significant industries: critical minerals, energy, automotive, and defence, which sit at the intersection of that relationship. We explore how deepened strategic alignment can enhance North American security, competitiveness, and resilience—and how that could be achieved.

Auto Manufacturing

The Challenge: The Canada-U.S. auto trade is under pressure on several fronts

-

U.S. Section 232 tariffs introduced friction at precisely the moment the industry needed continental coordination.

-

The deep structural threat to the US$100-billion Canada-U.S. auto trade is China, which produced 33 million vehicles in 2025—more than a third of the global total. China’s rising dominance is underwritten by scale, superior technology, development speed, and vehicle affordability.

-

Four other mega forces compound that challenge:

-

Electrification is stalling in North America, even as Chinese-led propulsion electrification is accelerating everywhere else;

-

Vehicles are becoming software-defined platforms, with value increasingly concentrated in chips, sensors, and software rather than mechanical hardware;

-

Industry 4.0 is transforming manufacturing operations and reducing labour demand;

-

Market maturity, as slowing population dynamics and the rise of shared mobility platforms are changing ownership patterns among urban consumers.1

-

Collective Strengths

-

The U.S. brings the scale, capital, and market demand. American manufacturing expertise, R&D infrastructure, and domestic policy levers shape where investment flows across the North American system.

-

Canada brings complementary assets: award-winning assembly plants, global calibre parts-makers (e.g., Magna, Linamar), and a tech cluster with capabilities in sensors, AI, lightweight materials, and autonomy. BlackBerry QNX software, for instance, is already embedded in more than 250 million vehicles worldwide.2

-

Both countries have strengths in AI and autonomy, but trail China in battery chemistry, primary extraction and refinement of battery elements, and the manufacturing scale that drives efficiency.

-

Canada’s power grid is clean and more competitively priced than comparable auto jurisdictions like Michigan and Ohio. This is becoming more strategically significant as electrification, onboard computing, and autonomous systems raise the power load per vehicle.

-

Canada’s critical minerals are a hedge against dependence on China. The mining and refining of copper, cobalt, lithium, and graphite would strengthen integrated battery, EV, and smart car supply chains. From mine to finished vehicle, the entire value chain can be completed within North America—much of it within a day’s drive to assembly plants.

-

Batteries are expensive and dangerous to transport (owing to their chemical composition), which makes Canada’s rail, Great Lakes shipping, and cross-border trucking a competitive advantage.

The Obstacles

-

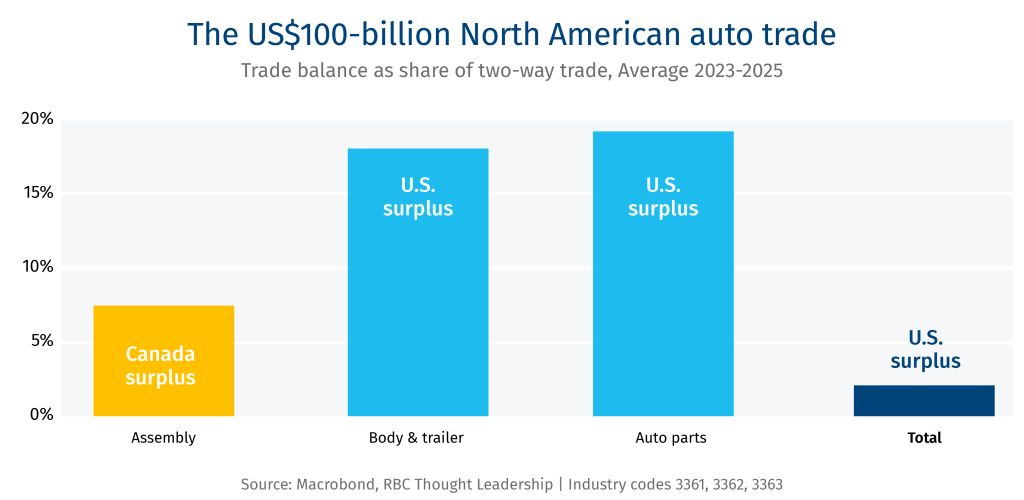

Tariff uncertainty is the most immediate obstacle to growth and innovation. For Canada, the threat is existential. More than 90% of Canadian vehicles are shipped to the U.S. Even with a relatively low effective tariff rate, plant margins would be compressed, changing the calculus for investment committees in Detroit and Tokyo.

-

For the U.S., retaliatory tariffs are damaging but not fatal. Canada’s consumer market is large and lucrative—on a per capita basis, Canadians buy more vehicles than any other country. save the U.S. Canada is not only the largest export market for U.S. vehicles—it’s larger than the next 10 countries combined.

-

Relocating assembly within the U.S. would make vehicles more expensive for American consumers. Canadian aluminum is produced using clean, low-cost hydro and nuclear power and is a critical input for lightweighting vehicles. The Ford F-Series is North America’s top selling vehicle and contains some 850 pounds of aluminum. Canada supplies more than half of the total U.S. aluminum consumption. Reshoring production with tariffed aluminum could cost U.S. auto consumers US$1 to US$2 billion.3 Vehicle affordability has already deteriorated on both sides of the border. The average transaction price for a new vehicle now exceeds $50,000 in the U.S. and $60,000 in Canada, putting new vehicles out of reach for many consumers.4 The result is an aging vehicle fleet, as households stretch replacement cycles or exit the market entirely. Tariffs, onshoring mandates, and the cost premium associated with electrification threaten to compound the affordability challenge.

-

The EV retreat is stranding capital without solving the competitiveness problem. Detroit automakers US$53 billion in write-downs reflects a genuine misread of consumer behaviour and policy stability.5 Industry forecasters project North American vehicle production will remain below the 2016 record of 18 million light vehicles through the end of the decade.6 The pivot back to ICE and hybrid platforms buys time, but Chinese OEMs continue to build technological and scale advantages on the platforms—electrified, software-defined—that will dominate the coming decades.

The Path Forward

-

Trade Policy Reforms. Washington’s goal—repatriating manufacturing—reflects a legitimate industrial concern, but the production the U.S. seeks to recover did not migrate to Canada. Since 2000, both Canada (-1.7 million units) and the U.S. (-2.6M units) saw assembly volumes shrink as the continental assembly footprint migrated to Mexico (+2.2M units). Canada, the U.S., and Mexico could align and strengthen the Rules of Origin and reform Most Favoured National tariff policy, which would incent global OEMs to locate production within the bloc, while jointly levying tariffs on EVs, parts, steel and aluminum from outside the bloc—hedging Chinese dumping. Reforms to the Labour Value Content provisions such as raising the content share and the wage rate would help rebalance investment and production within the bloc, which has long been biased toward Mexico.7

-

Critical Minerals Auto Pact. Cooperation on an end-to-end supply chain would tie Canada’s world-class geology and mining expertise with American capital markets industrial demand. In exchange for duty-free access to the U.S. market, Ottawa and the provinces could formalize free trade for steel, aluminum, and copper, and off-take agreements, stockpiling arrangements, and price floors for cobalt, lithium, graphite, and rare earths—commercially de-risking private investment and converting Canada’s processing infrastructure into implicit U.S. supply chain security with no net new capital cost to either government. Extraction and refinement could utilize Canada’s vast capabilities in clean power.

-

Cooperation in Skills and Research. North American OEMs are pivoting toward extended-range electric vehicles (EREVs) and hybrids as the bridge between ICE and full electrification. Co-investment in testing facilities, SR&ED reform to cover autonomy, connectivity, and cybersecurity mandates, and immigration reform to attract engineering and AI talent would deepen the skills density needed to compete with China.

The Potential Outcome: Canada and the U.S. could be better prepared for an electrified, autonomous, and increasingly software-defined auto future by building on a bilateral partnership that ties Canadian aluminum, clean power, critical minerals, and advanced manufacturing capability to American capital markets, OEM headquarters, and consumer demand. Preserving market access for both parties could help keep vehicle prices competitive for consumers while excluding Chinese content from continental supply chains.

Critical Minerals

The Challenge: China’s Structural Dominance

-

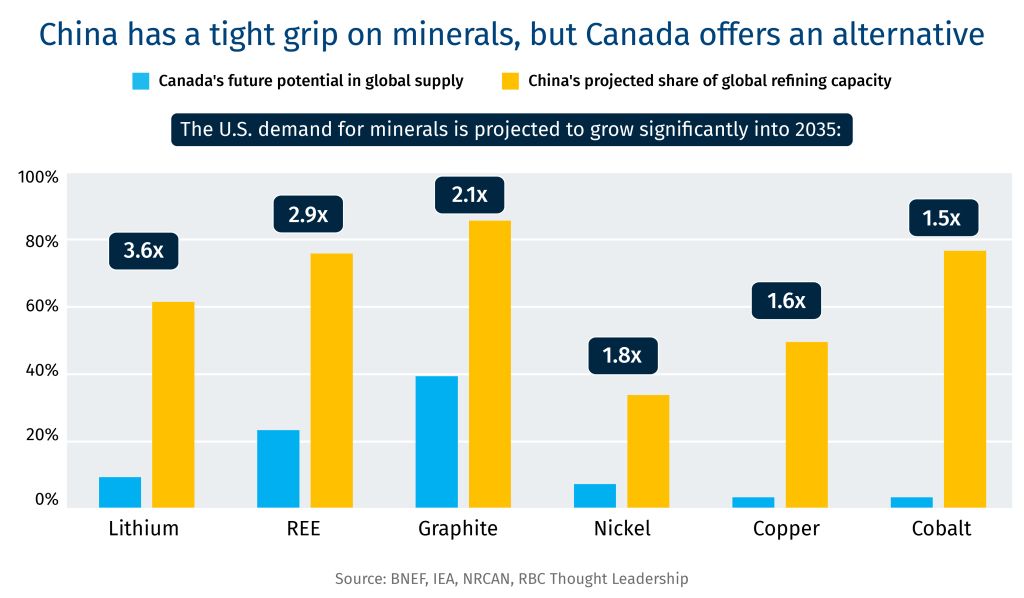

Chinese dominance in the refining and manufacture of critical minerals is the most direct threat to industrial sovereignty in North America. China dominates processing for 19 of the 20 most critical minerals, commanding, on average, 70% of market share. For tech and battery materials like gallium, graphite, and rare earths, its share exceeds 90%.8

-

Questions about the weaponization of supply chain dependence are no longer theoretical. China imposed export controls on gallium, germanium, rare earths, and battery chain technologies during the height of trade tensions with the U.S. In 2025, Ford shut down its Chicago assembly plant for one week following China’s rare earth export restrictions. The U.S. Geological Survey estimates that a 30% supply disruption of gallium could reduce U.S. output by US$600 billion—2% of U.S. GDP.9

Collective Strengths

-

The continental response—who mines, who refines, and who captures the downstream value—will shape North American industrial and defence competitiveness through 2040.

-

Canada and the U.S. are already each other’s largest minerals trading partner—approximately $150 billion in bilateral minerals trade annually.10 Canada is the top source for U.S. critical mineral imports, supplying 20%.11 But the current system is fractured: Canada mines, China refines, and the U.S. manufactures. Closing the gap is the defining industrial policy challenge of the coming decade.

-

Canada has world-class geology across cobalt, copper, gallium, germanium, graphite, lithium, nickel, tungsten and rare earths, with a seven-fold supply potential by 2040.12 Canada also has mature or developing refining infrastructure, including Anglo Teck’s Trail Operation (germanium), Neo Performance Materials’ Rare Earth Metals Facility (gallium), the Sudbury corridor (copper, nickel, cobalt), and the Bécancour mineral processing ecosystem, which connects Quebec’s mines with processing plants and downstream battery manufacturing.

-

Canada has clean, affordable power and abundant water. The U.S. has manufacturing scale, dominant capital markets, and the political will to strengthen supply chains.

The Obstacles

-

China has access to nearly unlimited, state-subsidized capital to finance mines and processing plants.

-

The talent and R&D gap with China has widened. China has 39 university degree programs to train engineers and technologists in critical minerals—Canada has none.13

-

For many critical minerals, North American demand is too thin to anchor the market. In 2024, the U.S. accounted for less than 2% of rare earth consumption—far below the threshold needed to make offtake agreements commercially viable.

-

Investment cycles in mining are long. In a world where capital is flowing into short-cycle AI, attracting investment into the refining of low-volume minerals is economically challenging.

-

High labour and environmental standards are strategic advantages in the long run, but they generate permitting timelines that extend well beyond those in China. Processing facilities face additional environmental impact assessments.

-

Supply chains will form around demand, not supply, but most demand will come from renewables and EVs, not defence. Battery chemistry is evolving rapidly, and with it, mineral intensity. Until recently, cobalt was considered essential. Lithium iron phosphate chemistry has since displaced it as the dominant cell technology. Sodium-ion and solid-state could similarly disrupt lithium demand.

-

Canada cannot pursue a strategy across all 34 critical minerals simultaneously. Capital, talent, permitting bandwidth, and infrastructure are finite. A more credible strategy would concentrate investment in minerals where Canada has refining infrastructure already in place and where Canada’s clean power advantage is most decisive. The strategy could also be geared toward minerals with demand that is technology-path-independent and is supported by multiple end uses beyond EV batteries.

-

While states have a role to play in creating and supporting markets, regulatory capture by a few anchor firms is a threat to the public good.

The Path Forward

-

Canada’s supply infrastructure and U.S. demand architecture are symbiotic. A formal Critical Minerals Partnership would tie Canadian geology, clean power, and mining expertise with American capital markets and North American manufacturing demand in a pairing that no other allied combination could match.

-

Long-term demand for critical minerals is expected to be strong. The IEA projects demand growth to 2040 for copper (30%), cobalt (50%), graphite (130%), lithium (350%), nickel (70%), and magnet rare earth elements (65%), driven by renewable energy, EV adoption, grid battery storage, and electricity network expansion. Defence layers on top of these, reinforcing the strategic case to build these supply chains now. Demand aggregation across the U.S., Canada, the European Union, the U.K., Australia, India, Japan and Korea could expand the market beyond 2.5 billion people.14

-

Project Vault works better with Canada. Canada’s federal strategy targets the same six minerals—lithium, graphite, nickel, cobalt, copper, and rare earths—mirroring Project Vault’s key focus areas. Ontario’s $500 million Critical Minerals Processing Fund is building the midstream refining capacity that U.S. OEMs need as a Vault counterparty. Explicit Canadian rules-of-origin eligibility under Vault—so that minerals refined at these facilities qualify as U.S. domestic supply—would convert existing Canadian processing facilities into implicit U.S. industrial capability with no net new capital cost to either government.

-

Allied demand aggregation works better if the U.S.-Canada bilateral partnership is the foundation. The Forum on Resource Geostrategic Engagement (FORGE) could be recast along NATO-like lines, wherein allies commit to procuring refined minerals from other allies as part of their NATO spending targets.15

-

China’s price manipulation is the shared threat that makes bilateral price stabilization essential. Use of a contract-for-difference (CFD), price floors, and volume guarantees could be applied bilaterally to Canadian processors, which would insulate North America’s supply chains against Chinese price manipulation.

-

Sustained investments in R&D, processing chemistry, and engineering talent are needed. Joint investment, shared technical training programs, and co-location of processing and end-use manufacturing could help build the skills density that neither country could develop on its own.16

The Potential Outcome: A North American supply chain could lead to reduced dependence on Chinese refining, tying Canadian geology and mining with American financing and manufacturing demand, deepening supply chain resilience and strategic capabilities simultaneously.

Oil and Gas

The Challenge: Security, Affordability, and Optionality

-

In 2024, Canada exported $170 billion worth of hydrocarbons to the U.S.—crude oil, natural gas, natural gas liquids, and refined products—accounting for 22% of Canadian exports. Canada supplies more than 60% of U.S. crude oil imports and virtually all natural gas imports. Two-way energy trade sits at $215 billion, underpinned by over 100 transboundary pipelines and transmission lines.17

-

Three imperatives define the relationship:

-

Energy security and sovereignty: Canada’s export dependence on a single buyer exposes both countries to disruption risk—political, logistical, or geopolitical. For oil, future demand growth is in Asia. For natural gas, demand growth is both Asian and North American.

-

Consumer affordability: Energy price volatility, whether caused by conflict in the Persian Gulf, tariff friction, or infrastructure constraints, passes through to households and industry on both sides of the border.

-

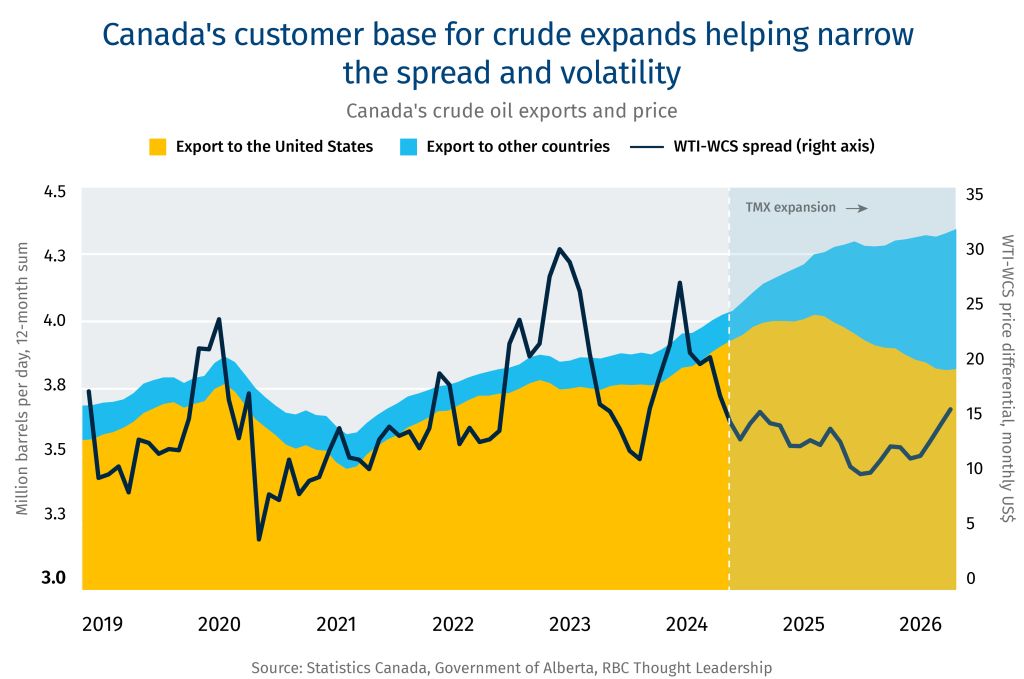

Value Maximization: The WCS-WTI price differential—historically US$10-25 per barrel—represents a structural transfer of value from Canadian producers to American refiners, driven by Alberta’s landlocked geography and insufficient export optionality.18

-

-

The crisis in the Persian Gulf has tightened heavy crude markets, elevated prices, and sharply illustrated the vulnerability of relying on politically unstable supply. The U.S. and Asian allies are assessing alternatives. Canada is the obvious answer.

Collective Strengths

-

Canada is the world’s fourth-largest oil producer, pumping 5.8 million barrels per day. The oilsands are a distinctive asset: long-lived, capital-intensive, and—unlike U.S. shale—resilient to short-cycle price volatility. U.S. crude production is plateauing: the EIA’s long-run reference case projects peak production in 2030, followed by decline in the 2030s. As the shale boom recedes, Canadian imports become more strategically important.19

-

North American heavy crude demand is structural. U.S. Midwest and Gulf Coast refineries are configured to process heavy, sour Canadian bitumen—the same configuration increasingly common in India and China. U.S. refineries with heavy conversion capacity will require a replacement source. Venezuelan production remains constrained by security, risk, and infrastructure. Canada is the only proximate heavy supplier at scale.20

-

The Trans Mountain Expansion (TMX) has begun to transform Canada’s strategic position. Since it came online in 2024, TMX has tripled capacity to 890,000 bpd to tidewater. The WCS-WTI discount narrowed and stabilized from nearly US$30 per barrel in 2022 to approximately US$10 by 2025. Each additional barrel shipped to Asia rather than into the continental market compresses the differential, improving producer netbacks.21

-

On natural gas, Canada’s Montney formation in northeastern British Columbia is one of the largest natural gas resource plays in the world, and LNG Canada’s Kitimat facility, which shipped its first cargo on in June 2025, has opened Canada’s first large-scale Pacific LNG export route.

The Obstacles

-

Oil prices: low and volatile prices challenge greenfield expansion and pipeline infrastructure; high prices trigger demand destruction and accelerate the energy transition. Sustained greenfield expansion will require policy stability and expanded export infrastructure.

-

Greenfield investment in the oilsands is limited. Growth from existing facilities is achievable but requires a policy environment that fosters growth and does not disadvantage Canada relative to other jurisdictions. A resolution of the Gulf crisis—returning Saudi, Iraqi, and potentially Iranian heavy sour supply to the market—would loosen the premium that currently benefits Canadian barrels in Asia. Venezuelan production, if rehabilitated under a U.S. policy shift, would compete more directly with Canadian heavy than U.S. shale.22

-

On gas, substitution is a constraint that does not apply to oil. Asian buyers can switch from LNG to coal, nuclear, or renewables. LNG Canada’s competitive position in Asia depends on carbon policy coherence, shipping costs relative to Qatari and Australian exporters, and whether Canadian gas can price below coal.

-

The Pathways Alliance—Canada’s five largest oilsands producers—has committed $16.5 billion for carbon capture and sequestration through 2030. The tension between energy security and climate policy has led to policy volatility on emission management, which compounds the technical and financial challenges associated with CCS projects.

The Path Forward

-

Optionality benefits both countries. The strategic logic for oil and gas runs in opposite directions, and both countries’ energy policy could reflect that asymmetry. For Canadian oil, diversification into Asia is the value-maximizing move: every additional barrel shipped via TMX to Asian buyers narrows the WCS-WTI discount and increases netbacks for Canadian producers. Pushing more heavy oil into the continental U.S. market has the opposite effect. For natural gas, the calculus is reversed: AI-driven electricity demand has elevated Henry Hub pricing, making the U.S. a premium gas market. LNG Canada’s Pacific route remains strategically important for Canada’s long-run diversification. The U.S., likewise, could continue to seek optionality for its refineries, securing Canadian supply while finding new import sources.

-

A formal Energy Security Partnership. One with harmonized pipeline permitting and regulatory timelines, joint strategic reserve coordination, bilateral CCS and methane abatement collaboration, and a common framework for infrastructure investment that treats Canadian production as implicit U.S. supply security without requiring government capital from either side. This could be expanded to include the G7 and NATO allies.

-

Oil is a market that works. The continental oil and gas system—hundreds of pipelines, integrated refining, established commercial flows—functions efficiently when policy does not distort it. Tariffs on Canadian energy raise prices for U.S. consumers, widen the WCS discount, and reduce producer revenue without repatriating any production. The U.S. refining system—particularly the heavy conversion capacity—was built for Canadian oil. Disrupting that relationship would require billions in retooling at U.S. refineries or sourcing heavier barrels from less stable suppliers.

-

Gas is complementary, not competing. Henry Hub natural gas prices have spiked with AI-driven electricity consumption in the U.S., making gas sales to the U.S. market economically attractive for Canadian producers. The Montney gas basin and U.S. demand growth reinforce each other. Investment in Montney production infrastructure by U.S. and Canadian investors alike expands the continental gas supply that both countries need for power generation, industrial use, and LNG export.

The Potential Outcome: A bilateral energy partnership could link Canada’s world-class oil and gas resources, pipeline infrastructure, and Pacific tidewater access with U.S. refining capacity, capital markets, and continental demand to deliver affordable, secure energy to consumers while expanding strategic optionality in global markets for both.

Defence

The Challenge: Heightened threat environment, fraying alliances

-

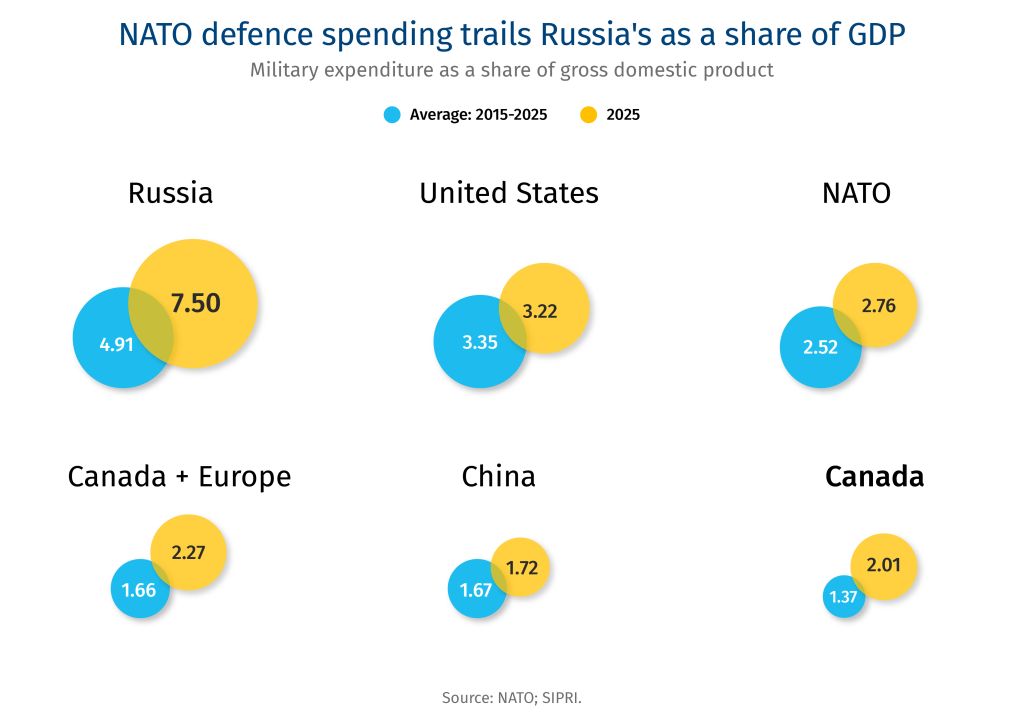

World military expenditure reached US$2.9 trillion in 2025—the ninth consecutive annual increase. The U.S., China and Russia accounted for roughly half of that—unchanged from 2000. However, the relative share changed dramatically: in 2000, Russia and China combined to spend a tenth of U.S. expenditure; today, they spend more than half that of the U.S.23

-

Russia’s invasion of Ukraine broke the security calculus for Europe. NATO responded with a historic commitment: at the 2025 Hague Summit, all 32 allies met the 2% GDP target for the first time since the 2014 Wales pledge. And NATO Allies agreed to a new benchmark of 5% of GDP by 2035.24

-

Russian and Chinese exercises and probes around the Arctic illustrate the rising threat level for North America.25 The Canada–U.S. defence partnership faces four frictions:

-

Defence Expenditure: Canada increased its military spending by nearly 70% from 2022 to 2025—hitting the 2% NATO target for the first time since the 1980s.26 Despite pledging to reach 5% of GDP by 2035, Canada has yet to produce a roadmap Washington finds convincing, prompting the U.S. to suspend the Permanent Joint Board on Defence.27

-

F-35 Procurement: Canada’s review of the program comes amid deepening trade tensions. The U.S. frames the delay not merely as a procurement decision but as a test of whether Canada intends to remain operationally relevant in an era of fifth-generation air and missile defence. The trade tensions also call into question whether Canada will continue to buy the most sophisticated U.S. hardware.

-

The Golden Dome: Designed to provide continental defence, the Congressional Budget Office has pegged the cost at US$1.2 trillion over 20 years.28 Canada’s role remains undetermined.

-

Collective Strengths

-

In addition to unmatched platform scale, capital depth, and technological sophistication, the U.S. possesses a dynamic defence innovation economy, R&D density, and an advanced defence industrial base.

-

Canada brings world-class capabilities in domains critical to modern defence, including avionics, aircraft maintenance repair and overhaul, marine sensors, electronic warfare, UAV’s, and training and simulation—all of which are designated as priority sovereign capabilities in Ottawa’s Defence Industrial Strategy (DIS).29 In space, Canada has a six-decade legacy spanning Earth observation, satellite communications, and positioning-navigation-and-timing systems. Canada contributes heavily to the early-warning capabilities via the northern radar networks and operates a portion of the North Warning System (NWS), and maintains Forward Operating Locations in the Arctic.30 Nearly half of Canadian defence output is exported, with 70% to U.S. and Five Eyes partners, underscoring deep interconnection into global markets.31

The Obstacles

-

Over 90% of Canadian defence firms are SMEs. The absence of large defence primes depresses capital formation, posing challenges to the ambition to scale up Canada’s industrial base. Canada’s venture capital pool—roughly $12 billion—is less than 5% of the U.S. equivalent. Collateral assets in defence (specialized facilities, restricted IP) are often illiquid, with persistent mismatch between up-front investment requirements and revenue timing.32

-

Protectionist procurement policies: Both Canada and the U.S. are pushing to buy domestically, increasing trade frictions. For Canada, directing contracts to domestic firms where industrial capacity does not yet exist at scale could increase costs and extend timelines. Outside of space, ocean, and some aircraft, the target of 70% Canadian content in defence acquisitions by 2035 (up from ~40% today) requires building industrial infrastructure that cannot be created quickly.

-

Arctic sovereignty is another tension. Russia and China pose threats to the Arctic, and despite American pressure to invest in Arctic defence, the region remains exposed (current investments in Arctic defence notwithstanding).

-

The U.S.’s defence industrial base is production-constrained, not merely capital-constrained. The conflict in Ukraine and Iran have exposed munitions stockpile gaps while ‘Buy American’ provisions and export controls have restricted supply chain integration with allies.33

The Path Forward

-

Develop distinct but interoperable industrial bases. Canada has set itself on a clear, distinct path to diversify its defence industry from the U.S. and develop its own sovereign manufacturing capacity. This will create divergent capabilities and more Canadian autonomy. However, it will be important for key capabilities, particularly those important to joint commands, to maintain technological and operational interoperability for the long-term functioning of North America’s defence framework.

-

Deepen in areas of mutual operational necessity. NORAD modernization is foundational. Canada’s ~$40 billion, 20-year investment—over-the-horizon radar (including the $6.5 billion Arctic system being co-developed with Australia), space-based surveillance, command and control, and northern infrastructure—signals deep commitment to the partnership. Canada could negotiate its participation in a future Golden Dome: Canadian sensors, Arctic radar infrastructure, and airspace access are genuine contributions that warrant cost-sharing terms, Canadian IP rights over jointly developed systems, and a defined Canadian role in intercept decision-making.34

-

Explore cooperation on space and drone technology. Recent conflicts demonstrate that uncrewed systems are redefining warfare. At the same time, space is a strategic domain that’s increasingly contested. Ukraine has become the “Silicon Valley” of defence innovation and recent NATO exercises have shown the effectiveness of these capabilities against outdated militaries. This phase of rearmament will not take the same form as previous ones. Canada must update its military equipment and infrastructure writ large, and the U.S. is facing depleted stockpiles and asymmetric threats. Therefore, both must re-prioritize what defence technology they need to develop and procure, creating opportunities for collaboration to avoid duplication in areas of shared security interests.

-

Deepen partnership on critical minerals. Canada’s geology, if twinned with refining capacity, could hedge reliance on adversarial powers. Formalizing supply agreements for NATO’s defence-critical minerals—with off-take arrangements, price stabilization mechanisms, and Rules of Origin eligibility that treat Canadian-refined inputs as U.S. domestic supply—would strengthen both countries’ industrial resilience.

-

Diversify on platforms and partnerships. Canada’s $530 million European Space Agency investment, its participation in the European Union’s SAFE initiative, and its emerging bilateral arrangement with Australia reflects Ottawa’s efforts to diversify its defence industrial base. European partners will expect access to Canadian procurement as the price of access to European markets.

The Potential Outcome: The Canada–U.S. defence relationship has historically rested on an implicit bargain: Canada provides geographic depth, on the ground, under the ocean, on the ocean, in the air and in space; the U.S. provides an umbrella of security and protection, reinforced by unmatched platform scale, capital depth, technological sophistication, and R&D expenditure. Ensuring that bargain holds requires Canada to close the gap between financial commitment and operational credibility—delivering on NORAD modernization, resolving the F-35 decision , and building a genuinely capable domestic industrial base. For the U.S., a more reliable long-term partner will be secured by respecting Canadian sovereignty.

Acknowledgments

The authors would like to thank the external experts consulted for this report, some of whom are listed below.

Peter Dawe, BDC

Steve Carlisle, General Motors (Retired)

Robert Johnston, University of Calgary

Frank McKenna, TD Securities and former Canadian Ambassador to the United States

Michael Robinet, S&P Global Mobility

[1] Brennan, J. 2026. Steering Through Uncertainty: Four Future Paths for Canada’s Auto Industry. Toronto: RBC Thought Leadership.

[2] Brennan (2026), Steering Through Uncertainty.

[3] Canada exports ~US$11 billion in aluminum to the U.S., with more than one-third demanded by the transportation sector. At tariff rate at 50%, the impact on auto assembly alone could exceed $1 billion. When auto parts are layered in, the tariff cost moves higher. For economic analysis of tariffed Canadian aluminium, see Aluminum Association. 2025. Powering Up American Aluminum: A Roadmap for Next Generation Supply Chain Resilience. Arlington, VA: The Aluminum Association; Business Data Lab. 2025. How to Undermine U.S. Manufacturing: Debunking Aluminum Tariff Myths. Ottawa: Business Data Lab.; and Livingston, Brian. 2025. Canada’s Aluminum Production and US Tariffs. Intelligence Memos. Toronto: C.D. Howe Institute. September 2.

[4] Brennan (2006). Steering Through Uncertainty.

[5] Markman, J. 2026. ‘How Legacy Automakers Torched $53 Billion on EVs They’ll Never Sell’, Forbes, February 9.

[6] Robinet, M. 2026. New Automotive Geo-economics. S&P Global Mobility. Presented at PMA, May 2026.

[7] See Helper, S. and T. Tucker. 2026. ‘Challenges and Opportunities for the North American Auto Industry in the 2026 USMCA Renegotiation’, March 4. Washington: Brookings Institution; U.S. International Trade Commission. 2025. USMCA Automotive Rules of Origin: Economic Impact and Operation, 2025 Report. Publication no. 5642. Washington: USITC.

[8] IEA. 2025. Global Critical Minerals Outlook. Paris: International Energy Agency.

[9] Baskaran includes this claim in her testimony to the House Natural Resources Subcommittee—a claim we have not been able to independently verify. See: Baskaran, G. 2026. ‘Unleashing America’s Mineral Potential: The Critical Minerals Commodity Supply Chain’, Testimony before the House of Natural Resources Subcommittee on Oversight and Investigations. Washington: Centre for Strategic & International Studies.

[10] Natural Resources Canada. 2025. Canada-U.S. Minerals Data Dashboard.

[11] Baskaran, G. 2025. ‘Canadian Tariffs Will Undermine U.S. Minerals Security’, Center for Strategic & International Studies, January 29.

[12] Merwat, S. 2026. Mine & Refine: Bridging Canada’s Critical Minerals Capital Gap. Toronto: RBC Thought Leadership.

[13] Merwat, S. 2025. The New Great Game: How the face for critical minerals is shaping tech supremacy. Toronto: RBC Thought Leadership.

[14] See Baskaran (2026).

[15] See Baskaran (2026) for a suite of policy recommendations which integrate extraction, processing, refining, and manufacturing with demand anchors.

[16] Merwat, S. 2026. Critical Minerals Processing: The West’s refining challenge and the technologies closing the gap. Toronto: RBC Thought Leadership.

[17] Canada Energy Regulator. 2025. Market Snapshot: Overview of 2024 Canada-US Energy Trade. Available online at: https://www.cer-rec.gc.ca/en/data-analysis/energy-markets/market-snapshots/2025/market-snapshot-overview-of-2024-canada-us-energy-trade.html.

[18] Part of the differential reflects quality and transportation cost, but another part is derived from insufficient export diversification. See Alberta Energy Regulator. 2025. Alberta Energy Outlook ST98. Calgary: Government of Alberta.

[19] Energy Information Administration. 2026. Annual Energy Outlook. Washington: U.S. Department of Energy.

[20] Merwat, S. 2026. Six charts that analyze Canadian-U.S. oil ties amid new geopolitical developments in oil markets. Toronto: RBC Thought Leadership.

[21] Johnston, R. 2026. ‘Asia’s Oil Demand Outlook and Geopolitics’, Presented to PwC Canada/School of Public Policy Asia Oil Outlook, May 7.

[22] See the Oil Sands Alliance’s explainer on the Pathways Project: https://oilsandsalliance.ca/pathways-project/.

[23] Author’s calculations based on data from SIPRI Military Expenditures Database (constant 2024 $USD).

[24] NATO. 2025. Defence Expenditures and NATO’s 5% Commitment. Brussels: North Atlantic Treaty Organization. Available at: https://www.nato.int/en/what-we-do/introduction-to-nato/defence-expenditures-and-natos-5-commitment.

[25] Bingen, K.A. 2026. ‘Orbits of Influence: Emerging Threats to U.S. Space Security and Foreign Policy Implications’. Statement before the House Foreign Affairs Subcommittee on Europe. Washington: Center for Strategic and International Studies, April 29.

[26] NATO data indicates that Canadian defence spending rose from US$26 billion in 2022 to US$44 billion in 2025—an increase of 69% (using current prices and exchange rates). SIRPI data indicates that Canada spent 2.06% of GDP on defence in 1987.

[27] Some interpret the suspension of the PJBD as a response to Canada’s decision to review the F-35 program (and not as a response to Canada’s planned military expenditures, despite advertisements to the contrary).

[28] May 2026 report from the Congressional Budget Office: https://www.cbo.gov/system/files/2026-05/62379-golden-dome.pdf.

[29] Department of National Defence. 2026. Canada’s Defence Industrial Strategy: Security, Sovereignty and Prosperity. Ottawa: Government of Canada.

[30] See NORAD Backgrounder: https://www.canada.ca/en/department-national-defence/news/2022/06/north-american-aerospace-defense-command-norad.html

[31] See Canada’s (2026) Defence Industrial Strategy.

[32] Ashcroft, T. 2026. Frontline Investments: How to Advance Defence Finance in Canada. Toronto: RBC Thought Leadership.

[33] See reporting from the Associated Press, ‘US Will Need Years to Replenish Stockpiles of Advanced Weapons Used in Iran War, New Analysis Finds’, May 27. Available online at: https://www.usnews.com/news/business/articles/2026-05-27/us-will-need-years-to-replenish-stockpiles-of-advanced-weapons-used-in-iran-war-new-analysis-finds

[34] Department of National Defence. 2025. Fact Sheet: Funding for Continental Defence and NORAD Modernization. Ottawa: Government of Canada. Available at: https://www.canada.ca/en/department-national-defence/services/operations/allies-partners/norad/facesheet-funding-norad-modernization.html.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates. This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/our-impact/sustainability-reporting/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.