It’s more than a year into the historic U.S.-Canada trade shock, and the two economies suddenly find themselves at another nexus—the future of CUSMA, and a next chapter where precedents don’t necessarily hold.

In some ways, it’s a moment of relief. What initially seemed like a monumental disruptive trade shock became a watered-down version of threats, and a growing list of exemptions for traded goods for many trading partners. Canada’s list has been the largest, thanks mostly to CUSMA, which makes about 90% of exports to the U.S. tariff-free. As a result, the trade schism between the two countries has been quite narrow, albeit deep.

But there’s also hesitation. The U.S.-Canada ties seem to be bruised, not broken, but the outcome of the trade negotiations remains far from certain, and adjustments to this new relationship are still in play. Trade-related jobs have still bled on both sides of the border, and Americans are beginning to see the rise in tariff-related inflation.

The trade war has turned out to be a slow leak—a disruption and transformation in slow motion. Slow leaks buy time to maneuver, but they can also produce some complacency. And they have a way of revealing cracks in the foundation that had been papered over before. This trade shock has uncovered under-the-radar stories about global trade, and the U.S.-Canada trade relationship. Here are six worth highlighting:

-

Global trade growth doubled without the U.S.

A big Liberation Day concern was that mass tariffs would spark a global recession, given the U.S.’s importance in the world economy. Instead, global trade, excluding the U.S., doubled, growing 4.4% year-over-year.

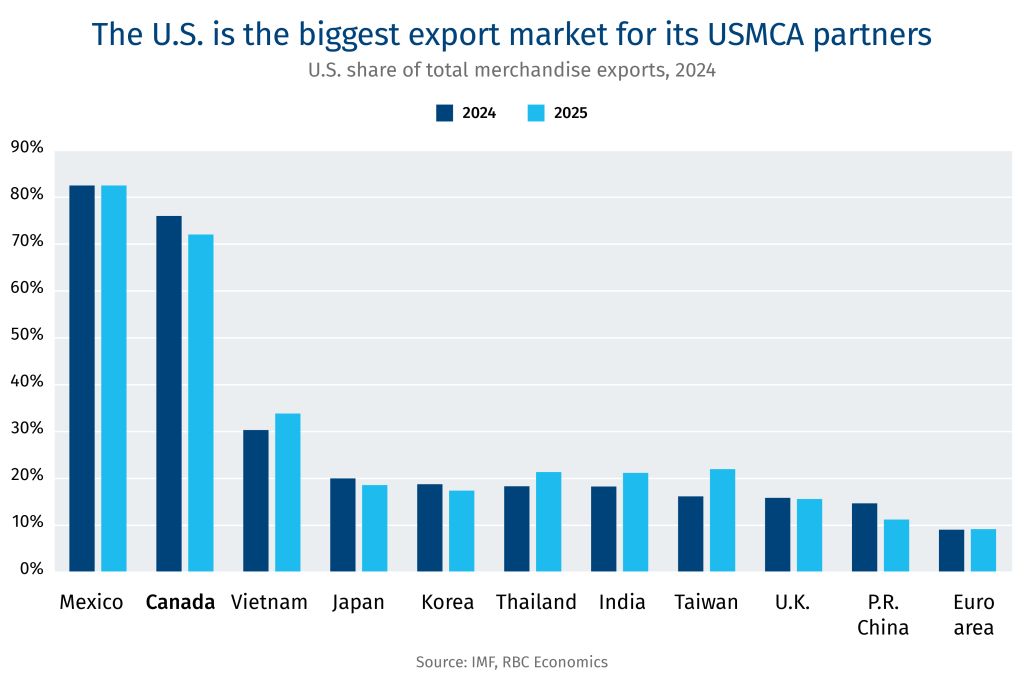

A North American centric view of the world would, perhaps, have missed that outside of Mexico and Canada, American trade partners are far less exposed to the U.S. consumer market. Prior to 2025 tariffs, exports to the U.S. ranged from 30% in Vietnam to 15% in China, and 9% for the Euro area.

Indeed, rather than break the global economy, the rest of the world is adapting to re-orient around the U.S. market. In a world focused on trade leverage, the jump in trade amongst global partners would suggest the U.S., perhaps, has less than initially appears.

-

The year of Canada’s trade divergence

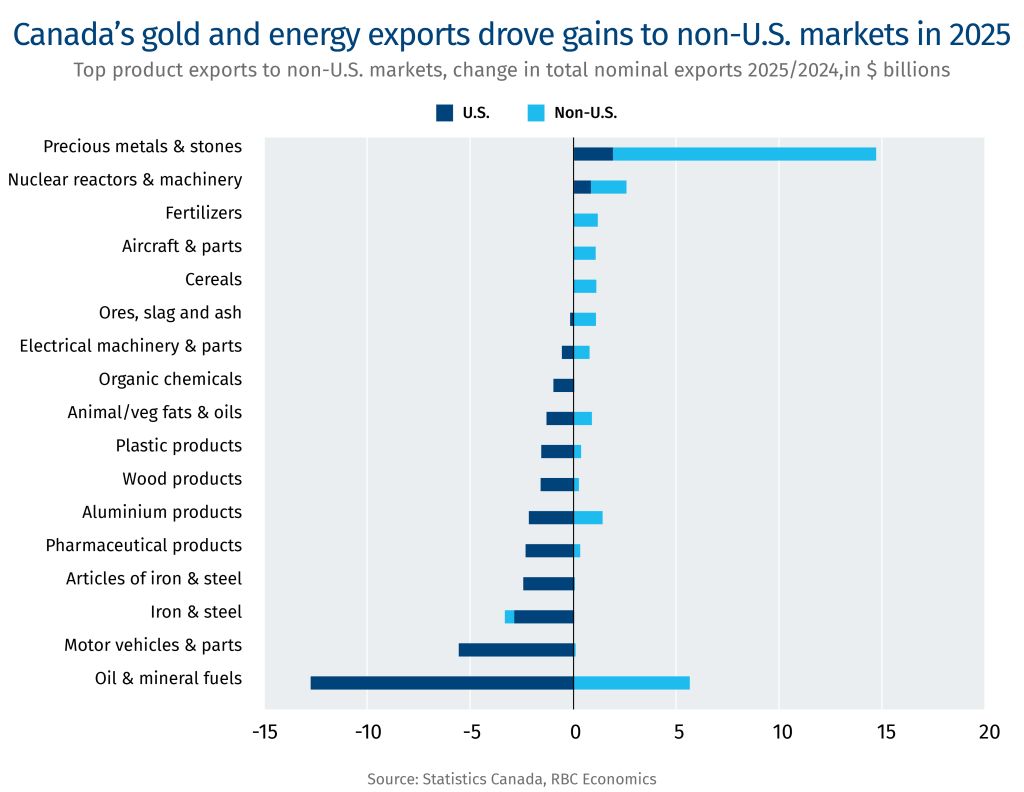

Canada also re-oriented trade away from the U.S. in 2025—the U.S. share of total Canadian exports went from 76% in the fourth quarter of 2024 to 68% in the same period in 2025. While exports to the U.S. fell 6% year-over-year, or by about $35 billion, this was offset by a hefty $29 billion increase in exports to the rest of the world.

Diversification didn’t come from finding new buyers for tariffed products. The increase, instead, came thanks to a surge in gold prices, which rose more than 60% in 2025. The result: gold exports to the U.K. alone spiked by $17 billion, or 76%, last year, making gold Canada’s second-largest export after crude oil. This significantly cushioned declines in other goods.

Gold also provided a big lift to the Canadian stock market, boosting Canadians’ financial wealth. The gold rally accounted for an estimated third of the TSX’s 28% gain and was the biggest driver behind the index outperforming the S&P 500 last year.

-

The U.S.-Canada trade war has been more narrowly impactful

Coupled with the energy shock, the trade shock is creating more distinct regionalization across Canada with some provinces and local economies disproportionately bearing the brunt of the breakdown. Though, none have been entirely immune.

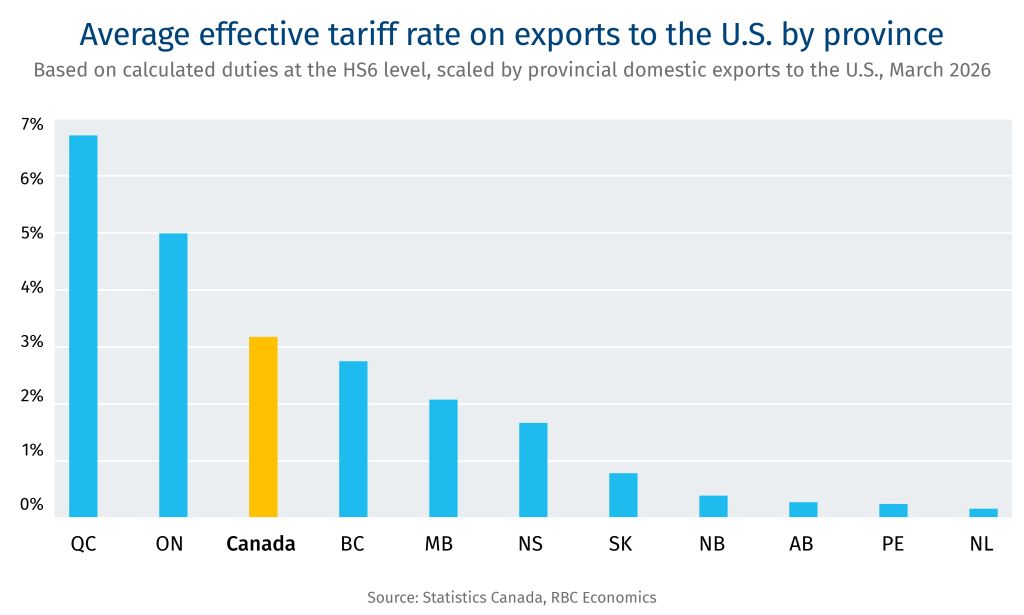

Thanks to CUSMA, a narrower subset of industries, and therefore geographies, experienced the bulk of the trade shock. While the trade war became a national fixation, it hit manufacturing-heavy provinces of Quebec and Ontario the hardest. Steel, motor vehicles and parts saw the largest export losses, creating particularly acute challenges for regions like southwestern Ontario. Cities like Windsor, Ont., saw unemployment rates rise as high as 11.1%, while the national average peaked at 7.1%.

Outside of Ontario and parts of Quebec, the rest of Canada—particularly energy and agricultural-producing provinces—felt minimal direct impacts from the trade war. They benefitted from having very little trade being exposed to U.S. tariffs, and greater overall trade diversification. B.C., for instance, didn’t find itself at the heart of the conversation in 2025, but is likely to feel some pain in 2026 from the knock-on effects of lumber duties, which jumped in October 2025.

Coupled with the energy shock, the trade shock is creating broader economic divergence across the country, with several implications worth exploring for policymakers at all levels of government.

-

The U.S. trade deficit was redistributed

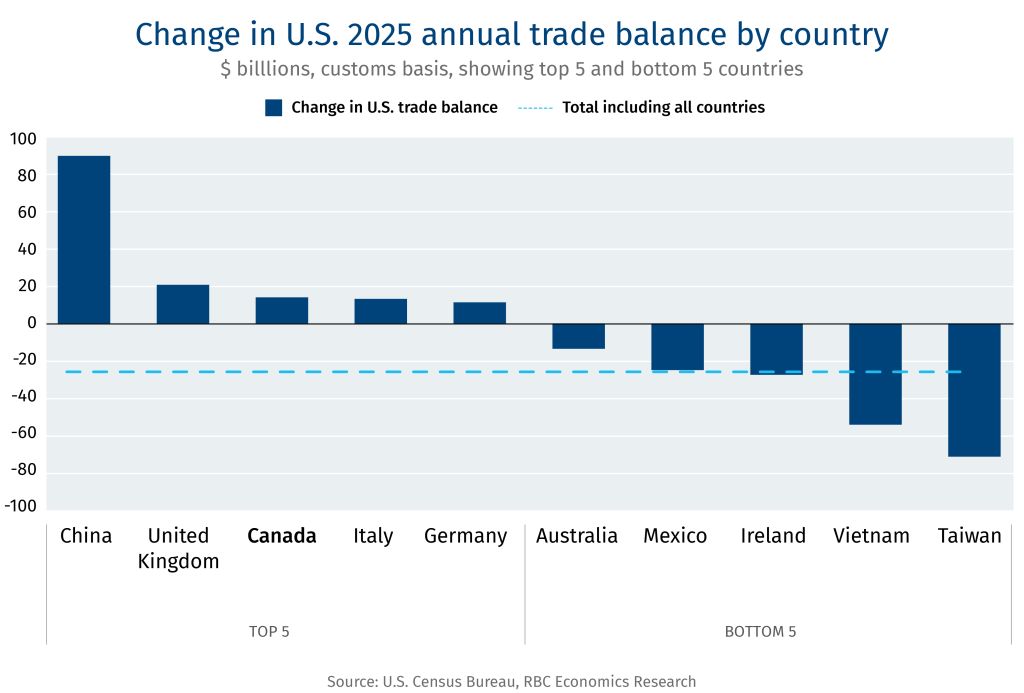

Tariffs were justified by the U.S. administration, in part, as a method to reduce the U.S. trade deficit. One year on, however, the deficit has moved in the wrong direction. Overall, the goods and services deficit widened by US$47 billion in 2025 compared to 2024. The goods trade deficit alone hit a record US$1.26 trillion in 2025.

Beneath the surface lies a clear trade policy shift: While the total deficit grew, its mix changed meaningfully. Tariffs successfully reduced imports from primary targets (especially China), while ramping up from other Asian countries, including Vietnam, Taiwan, India, Thailand, and Malaysia.

Some other targets, including Mexico, saw exports to the U.S. rise. The U.S. deficit with Mexico grew significantly by US$25 billion despite being subject to 25-35% tariffs at various points in 2025, but with significant exemptions. Some trade goals are a poor match for deeply integrated manufacturing supply chains.

Ultimately, the geography shifted substantially, but the aggregate scale of trade did not.

-

Canadians have taken economic protection, and damage, into their own hands

Retaliatory measures were put in place by governments, but Canadians took the trade war personally, particularly with travel. And, it had an impact on Canada, and a key sector in the U.S.

Limited retaliatory measures from the Canadian government minimized the impact of the trade war on consumer prices at home, but consumer behaviour, especially in travel, still changed.

The federal government’s initial tariff retaliation only covered about a third of U.S. imports before being repealed by September, except those on steel, aluminum, and autos. This kept consumer prices down and gave the Bank of Canada flexibility to further lower interest rates. Meanwhile, provincial governments have exercised product boycotts, notably around American-made liquor, while federal and provincial governments now have “Buy Canada” procurement policies.

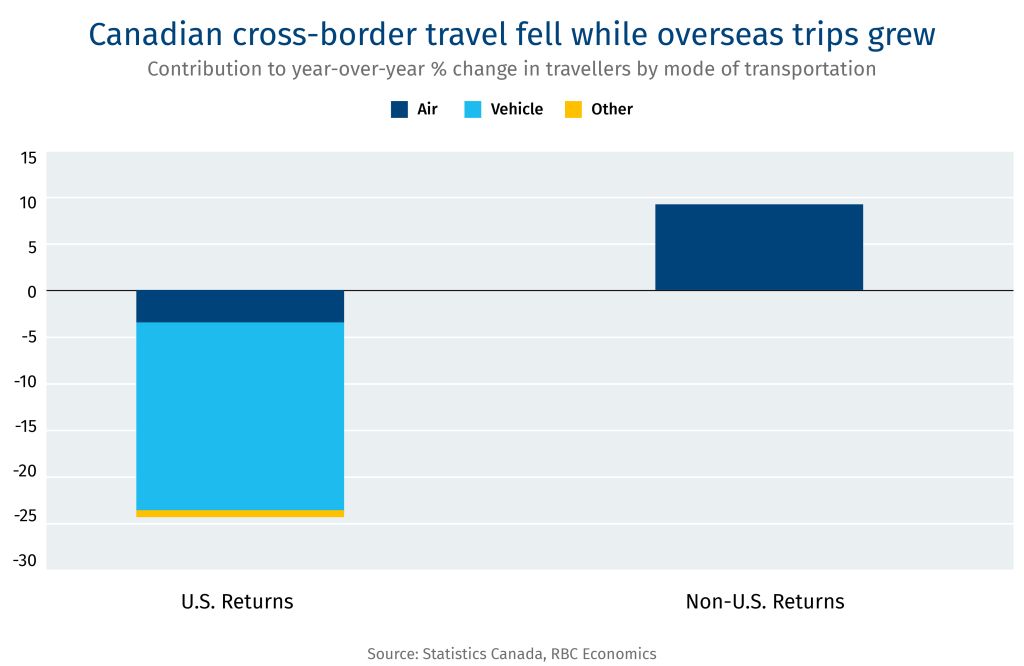

Still, the country responded in less official, more targeted ways. Travel is the most notable example. Canadian returns from the U.S. shrank 25% year-over-year in 2025.

Instead, travel to the rest of the world was up 9.2% compared to 2024. And Canadians spent more at home with a 2.7% bump in domestic tourism, raising spending to 11% above its pre-pandemic average. This has been a positive driver for increased domestic consumption.

-

Canada added more jobs than the U.S. in 2025 as both sides suffered from the shock

Jobs data tells a surprising story. Canada’s Labour Force Survey showed 211,000 jobs were added in 2025, up 1%. Meanwhile, the American Nonfarm Payroll survey showed a 116,000 increase, a 0.07% bump to the employed number.

What’s even more interesting is what happened beneath the surface. In the U.S., about 275,000 jobs were lost last year in trade-exposed sectors, including manufacturing, wholesale, retail, transportation and warehousing, and temporary help services. Out of all trade-exposed sectors, transportation and warehousing were hit the hardest with the magnitude of job losses reminiscent of COVID era cuts. Nearly 430,000 jobs were added on net in all other sectors combined.

In Canada, jobs dependent on U.S. demand fell by 2%. The silver lining, at least for Canada, is that while the country’s exports (~68%) are heavily dependent on the U.S., only ~12% of jobs are dependent on U.S. demand, helping to stem the bleeding from the trade shock.

The bottom line: Workers in both economies have suffered and would benefit from improving trade relations over deterioration.

Frances Donald is Senior Vice President & Chief Economist, RBC Economics

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates. This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/our-impact/sustainability-reporting/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.