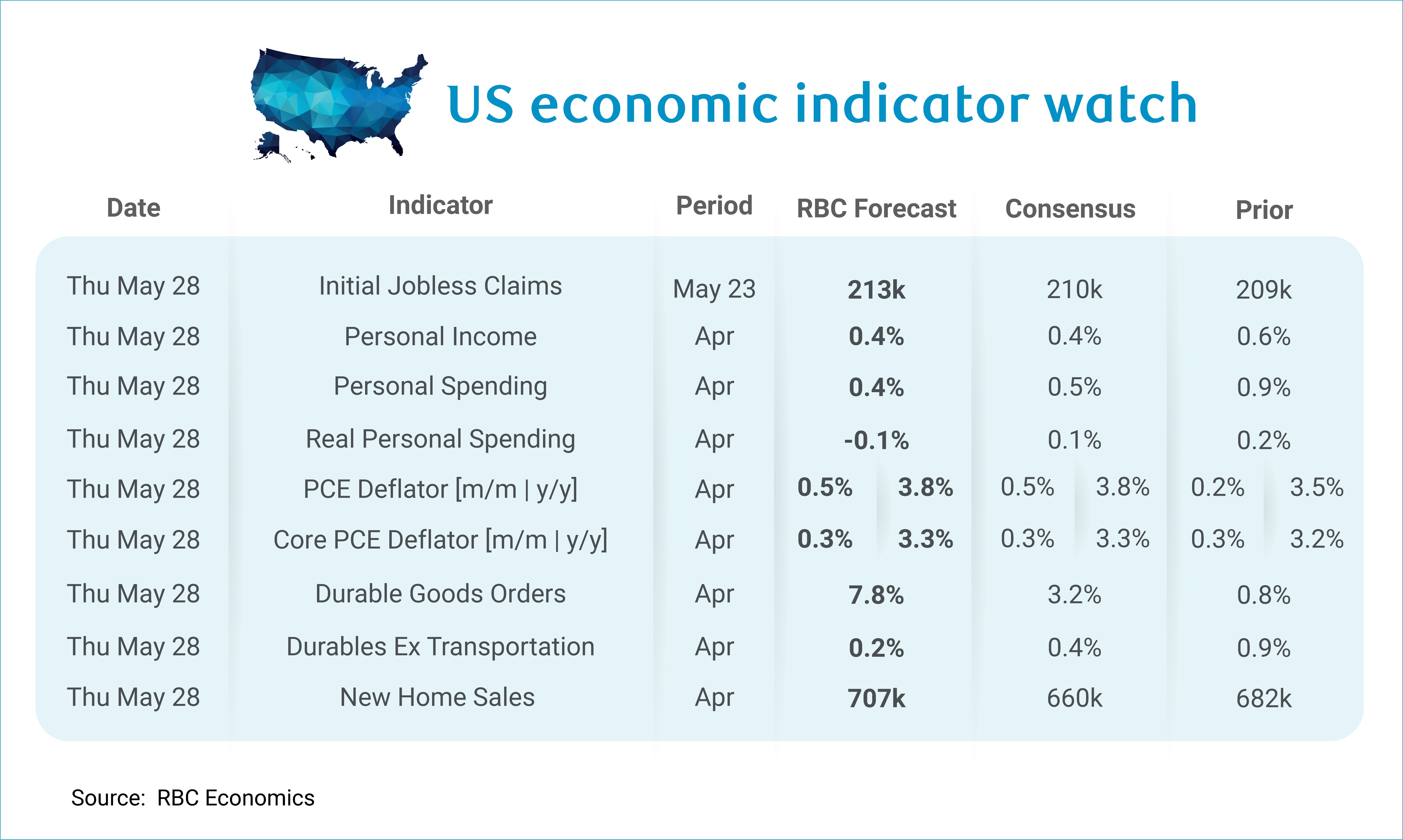

Next week, personal income and spending data will be front-and-center as elevated gas prices continue to weigh on consumers. We expect personal spending rose by +0.4% m/m in April. The retail sales data for April largely quelled fears of demand destruction amid higher gasoline prices. Nominal non-durables spending rose significantly, and durables pared back slightly due to weaker auto sales. And while we expect spending to continue to increase in most services sectors, a notable uptick in inflation means we anticipate real personal spending will show a modest pullback (-0.1% m/m).

For inflation, we do not expect the PCE data to be as jarring as the April CPI and PPI prints. The upside to core CPI was largely mechanical – a methodological quirk attributed to how the BLS handled missing housing data during the October government shutdown. Housing matters relatively less for PCE, and key PPI inputs to PCE (medical care services, portfolio management) are not expected to contribute significantly this month. We forecast that core PCE rose at a more modest pace in April vs core CPI (+0.3% m/m), which would bring the y/y pace of growth slightly higher to 3.2%. Still, the pressure from gas as well as food is pushing the headline pace higher – we expect to see headline PCE inflation advance 0.5% m/m, pushing the y/y pace to 3.8%.

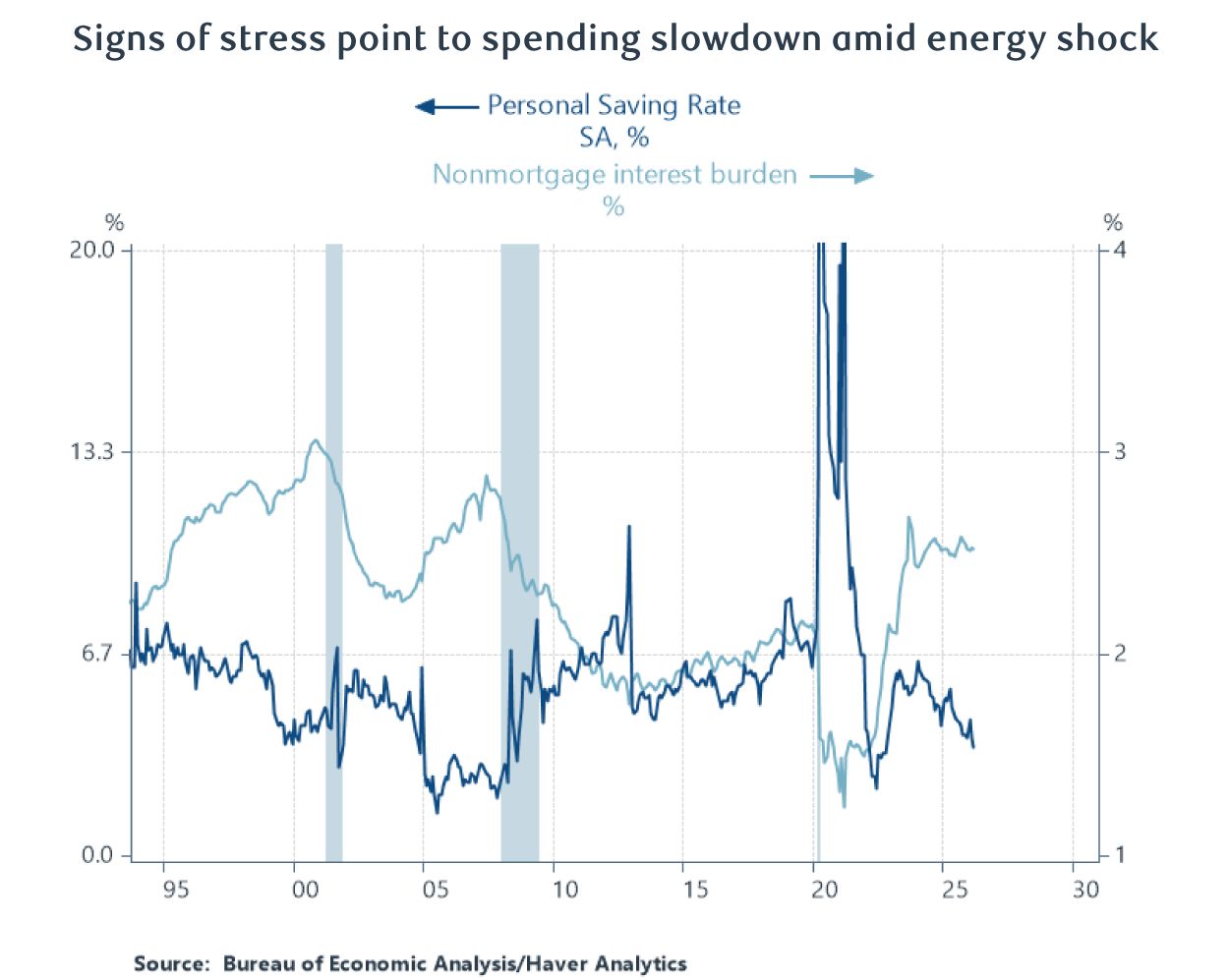

We will get personal income data as well, where we expect a proportionate rise to spending (+0.4%). The boost to income should be helped by higher weekly hours and stronger average hourly earnings seen in the April employment report, and continued strength in government transfers. The personal savings rate will be more important, which has fallen -1.5 percentage points over the past year and now sits at 3.6%. If we see a further decline, that would suggest consumers are continuing to save less to maintain spending against a backdrop of higher gas prices. And that leaves little room for unexpected expenses – something that would likely contribute to a rise in credit utilization. While the non-mortgage interest expense burden has eased since the Fed started cutting interest rates, it remains elevated as a share of disposable personal income. And a rise in that measure would be a worrying sign of stress for consumers, especially as the saving rate falls.

Aside from the personal income and spending release, here’s what else we’re watching next week:

-

Durable goods orders likely popped in April (+7.8% m/m) driven primarily by strong Boeing orders. Excluding transportation, durable goods orders likely slowed (0.2% m/m) as we expect higher fuel and transport costs weigh on activity.

-

We expect new home sales likely ticked up only slightly to 707k in April, after we saw an increase in mortgage application volumes. But with mortgage rates moving higher, we don’t expect to see any material improvement in the housing market this year.

-

We will also get the Advanced Goods Trade balance for April, and following the overturn of IEEPA, we expect to see imports pick up in the Q2.

About the Authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. Carrie is responsible for projecting key US indicators including GDP, employment, consumer spending and inflation for the US. She also contributes to commentary surrounding the US economic backdrop which she delivers to clients through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.