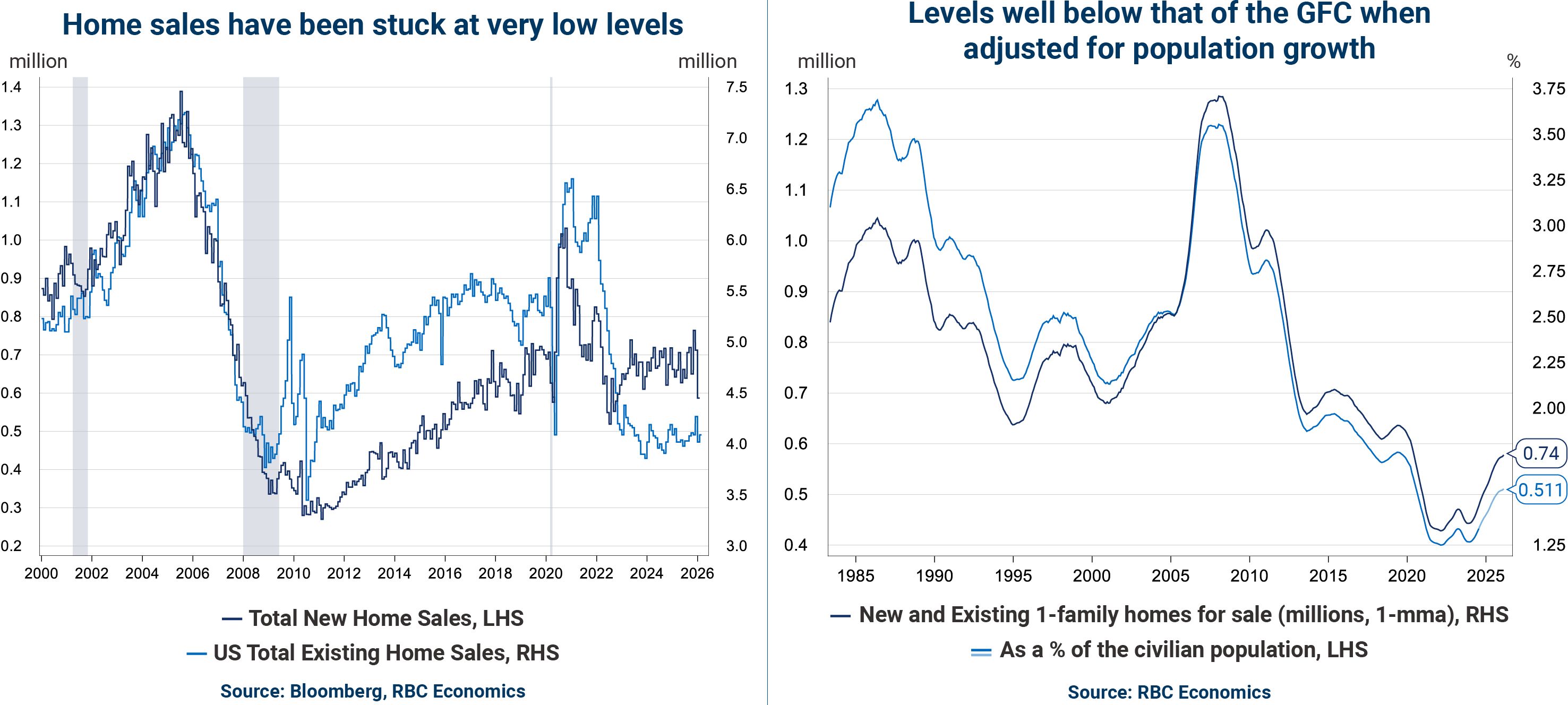

As we enter the spring season—typically viewed as the busy time for the housing market—US home sales remain in a deep freeze.

Home sales are lower than the worst seen during the Global Financial Crisis, especially after adjusted for population growth.

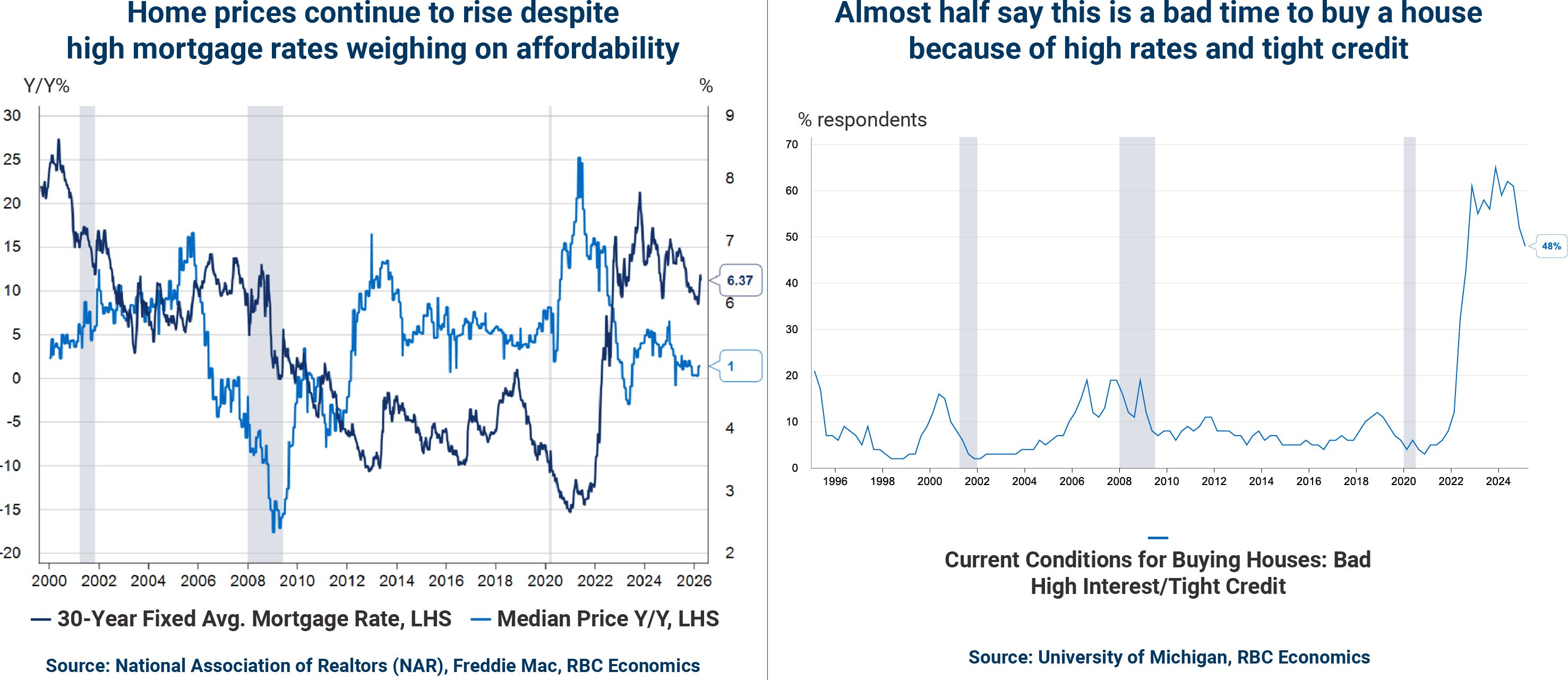

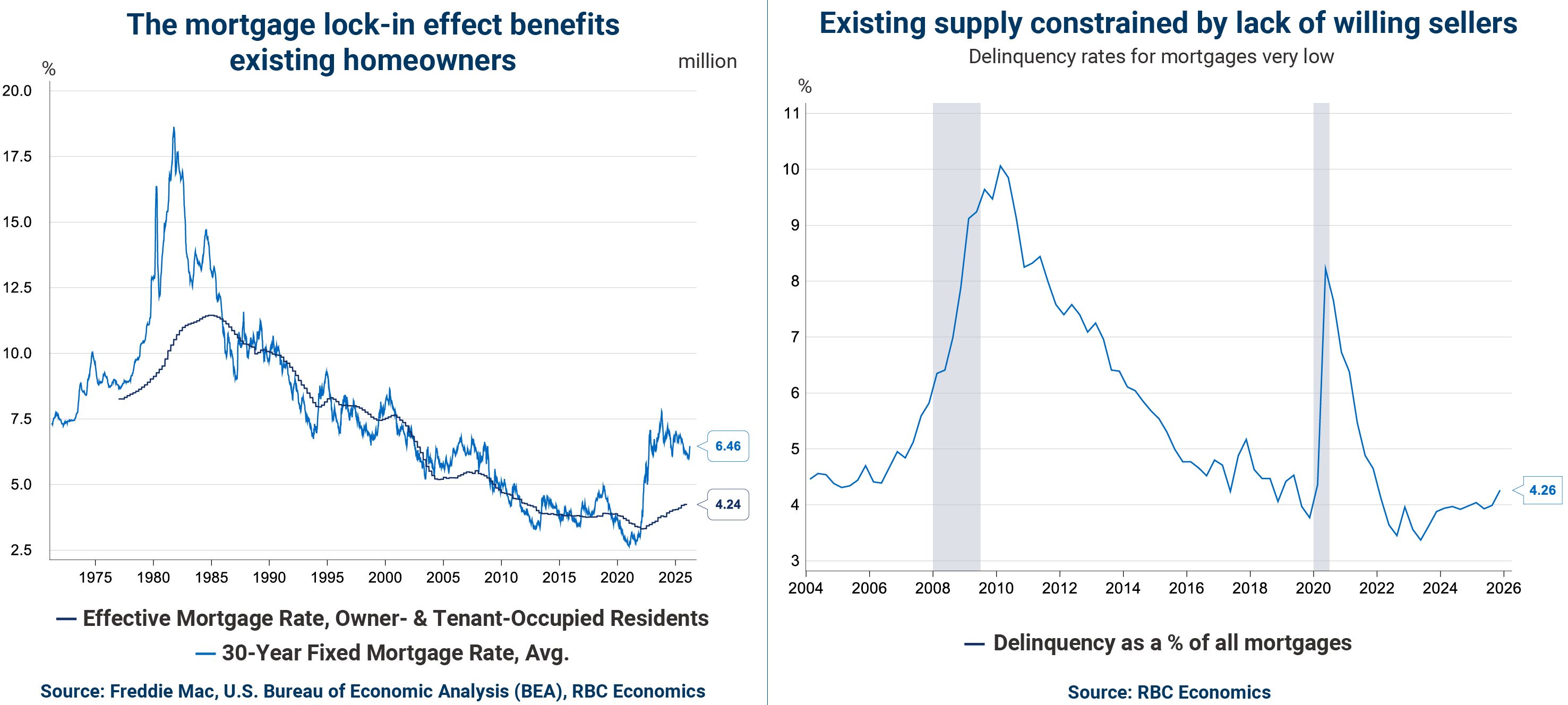

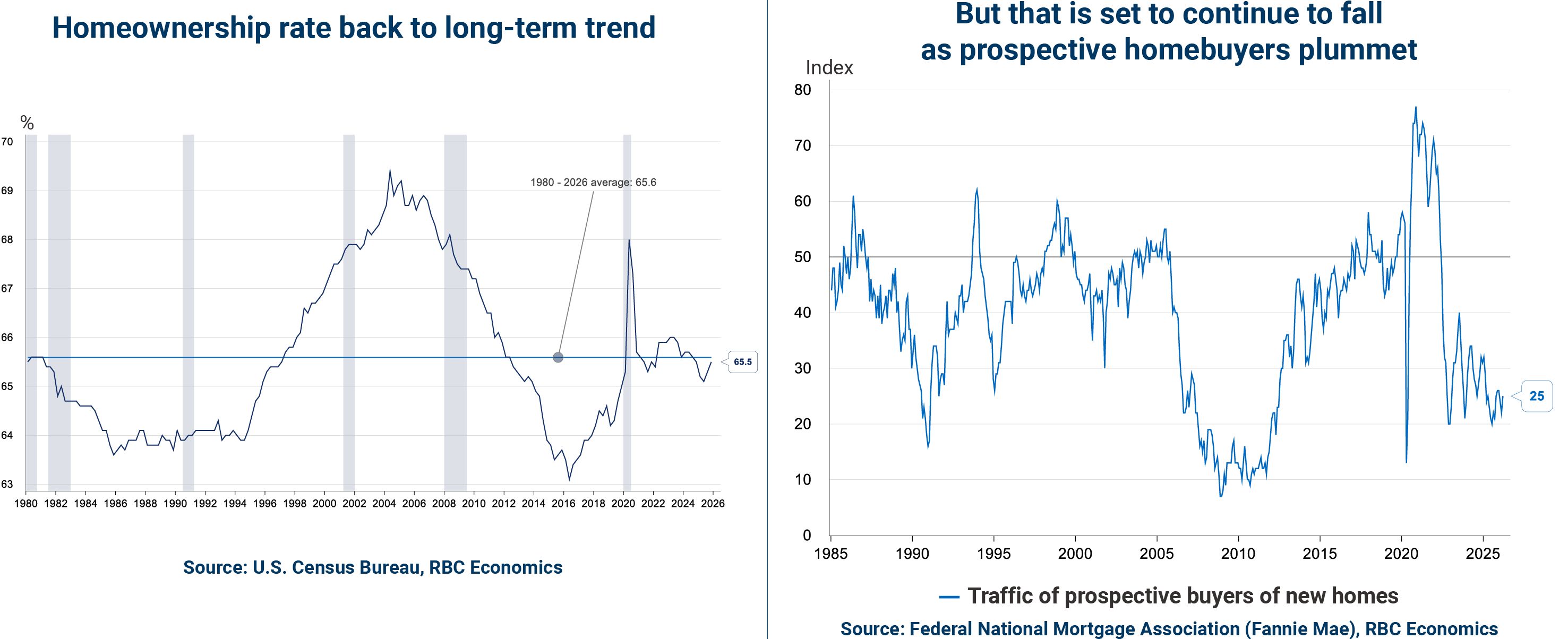

The primary issue is affordability, driven by (relatively) high mortgage rates and a lack of supply. The supply story is two-fold. For existing home sales, the significant gap between the average 30-year fixed mortgage rate (currently above 6%), and the incredibly low post-pandemic rates that many homeowners locked in has kept inventory suppressed. After all, how many homeowners would want to leave a sub-3% mortgage?

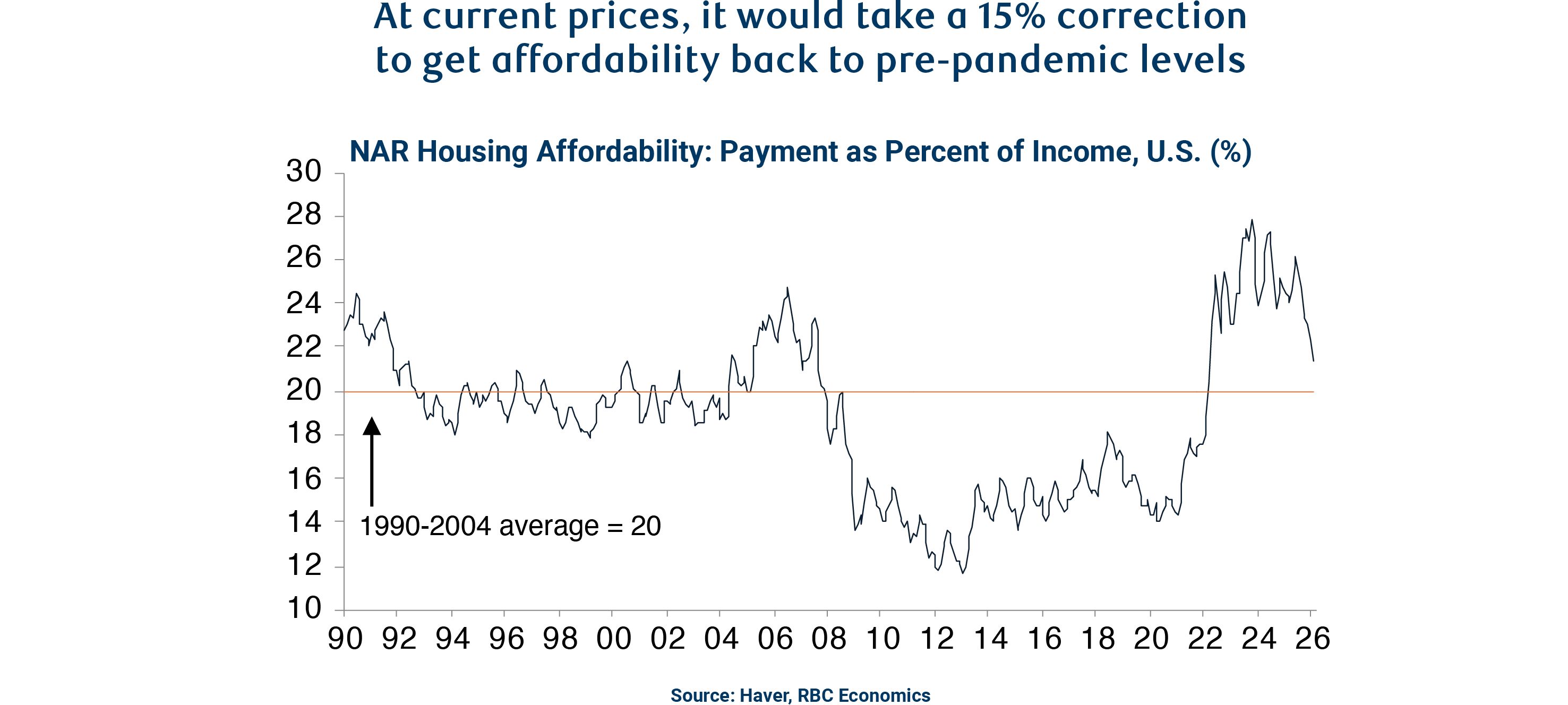

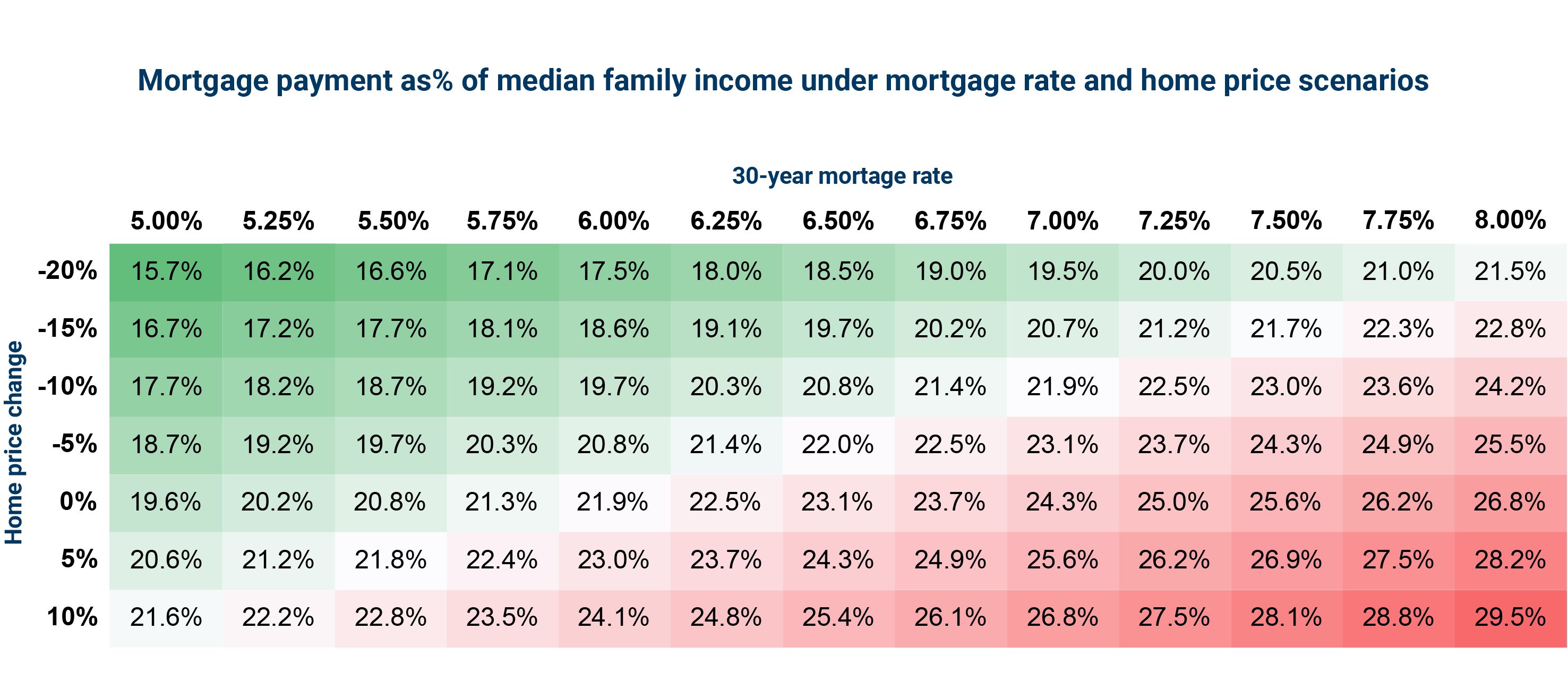

At the same time, higher rates and inflation have weighed on homebuilders, limiting the supply of new homes on the market. Lack of supply has contributed to home prices rising over the past several years, despite the typical inverse relationship with mortgage rates (i.e., home prices tend to drop as rates climb). In fact, we estimate it would take a near -15% price correction to return to affordability levels before the pandemic.

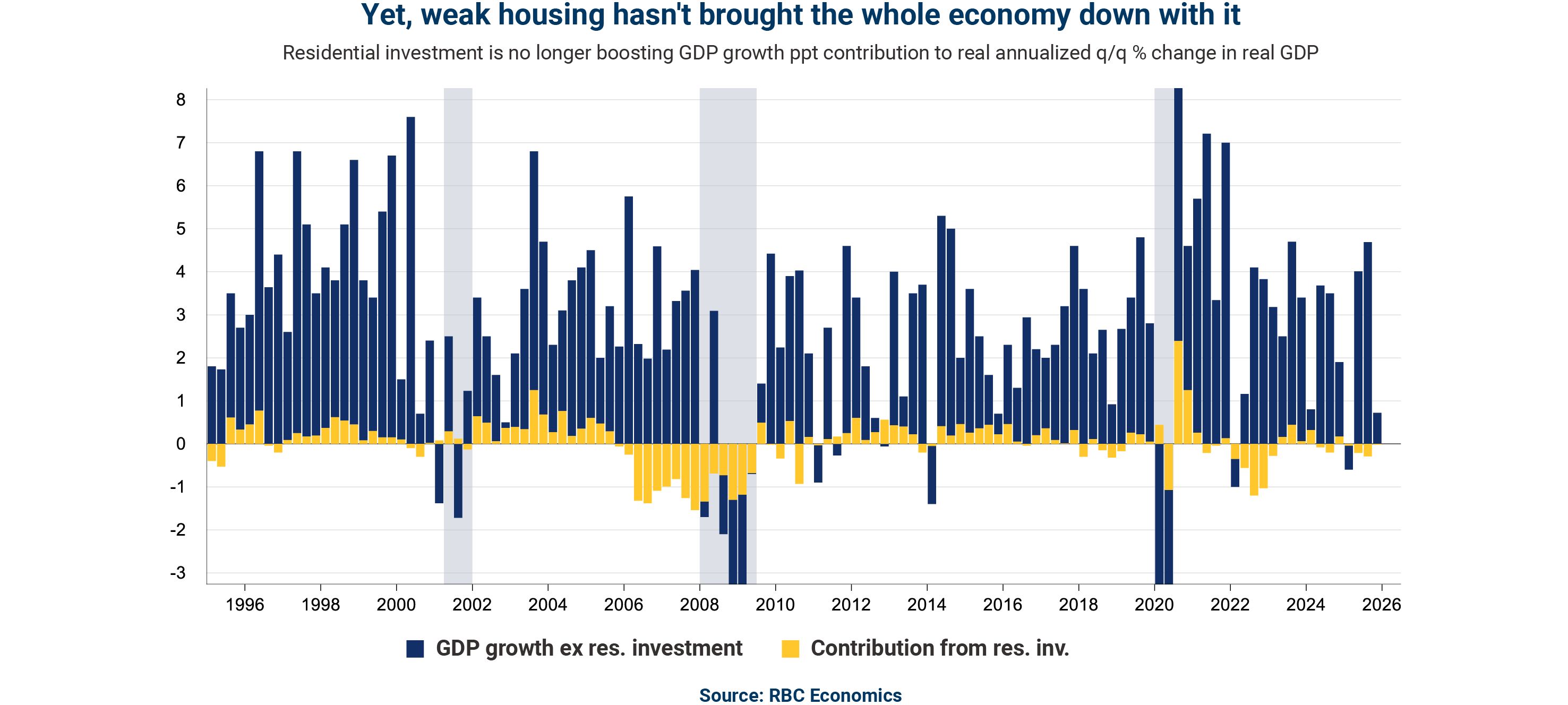

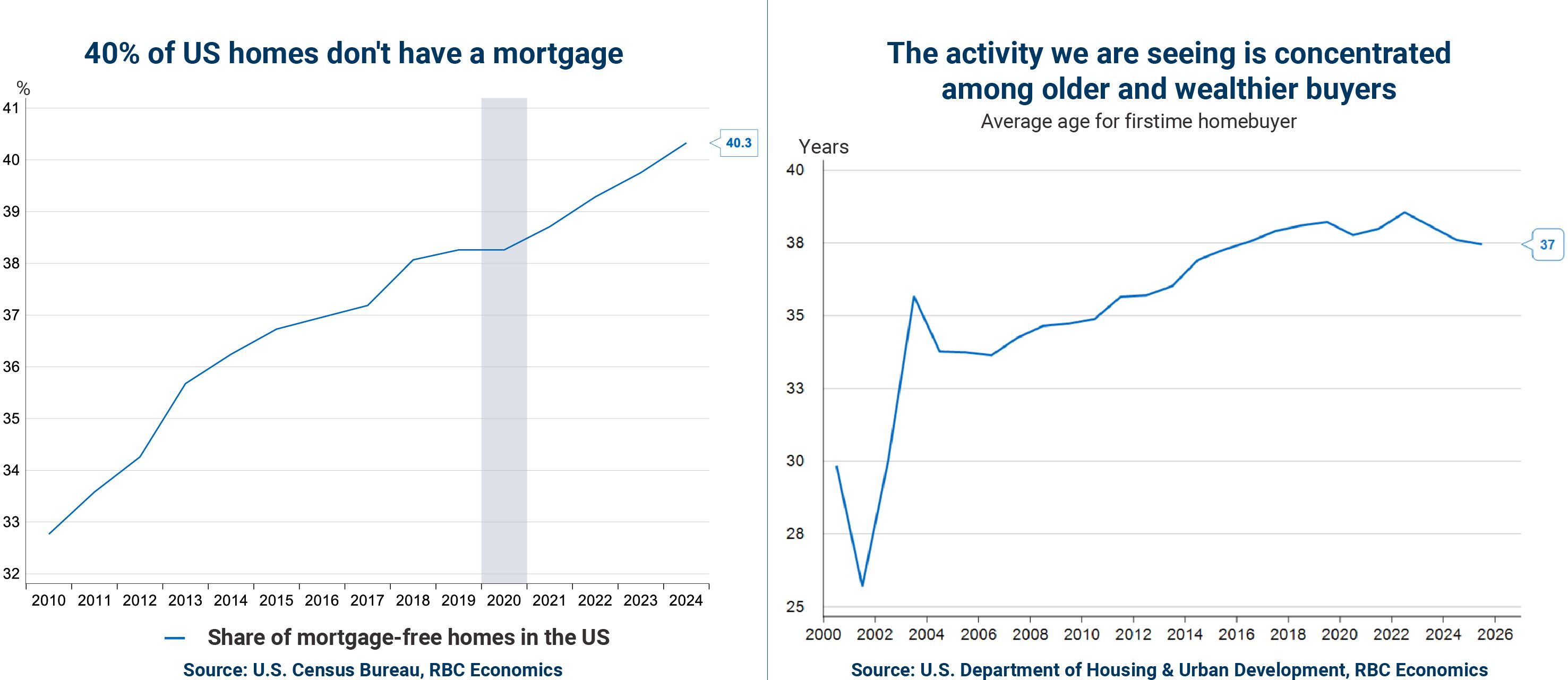

Headwinds aside, nearly 40% of homes owned are mortgage-free, and residential investment’s contribution to GDP growth has already bottomed out.

The housing market is isolated enough to avoid large risks to growth, but unable to find a path towards recovery without a meaningful change in mortgage rates or prices. Until then, we expect the market is likely to remain in this stalemate throughout 2026.

Here are 15 charts that explain what’s happening with the US housing market.

About the Authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. Carrie is responsible for projecting key US indicators including GDP, employment, consumer spending and inflation for the US. She also contributes to commentary surrounding the US economic backdrop which she delivers to clients through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.