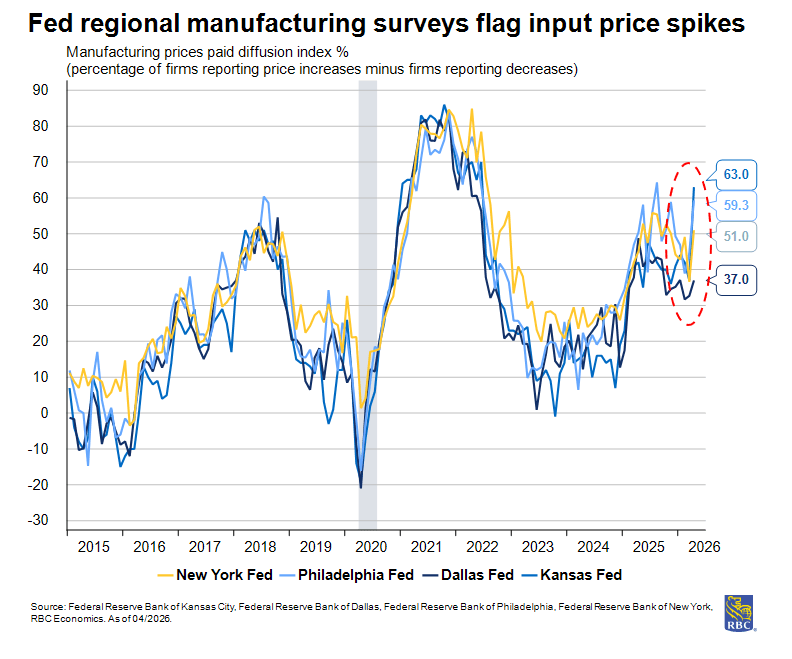

Next week will be quiet on the data front but we will get some useful signals coming from University of Michigan consumer sentiment, S&P PMIs, as well as some regional Fed Surveys (Kansas City Fed Manufacturing and Services, New York Fed Services, and Philadelphia Fed Business Outlook). We expect all of these will continue to show rising concerns about inflation.

Specifically, we are watching final inflation expectations for May – with elevated gas prices, consumers are increasingly concerned about inflation. One-year expectations have been heating up since 2025 but spiked materially since the oil price shock – from 3.4% in February to 4.5% in the preliminary May release. The preliminary data captured two weeks of interviews (April 21st to May 4th); the final release adds two additional weeks of elevated prices. Gas prices have not trended higher since May 4th, but in a volatile environment, survey timing matters. While consumer sentiment has become less useful from a forecasting perspective, persistently elevated inflation expectations are a concern for the Fed, especially as it relates to wage pressures. If higher gas prices become more entrenched (among other things like food and clothing), consumers are likely to demand wage adjustments. The April FOMC meeting minutes on Wednesday may offer a better sense of how the committee is viewing the risks around inflation and wages following the strong employment report.

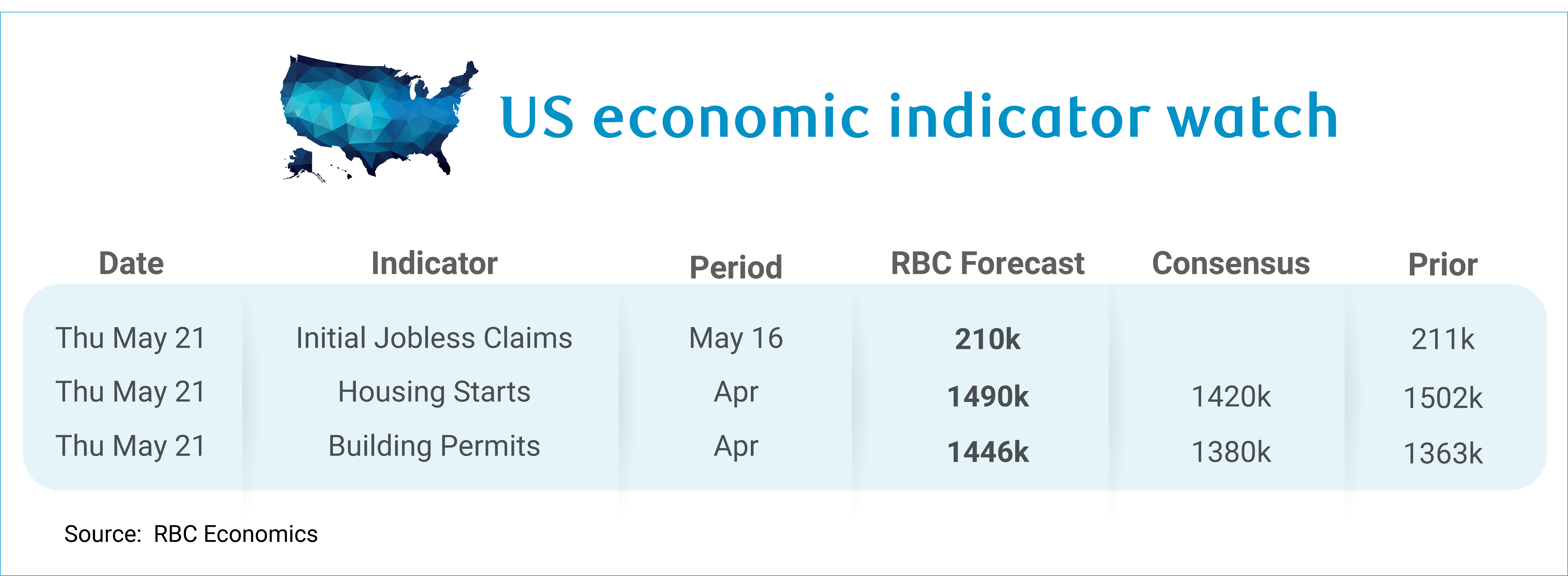

Regardless of the Fed’s near-term decisions, sticky long-end rates will continue to hold the US housing market hostage. We expect building permits ticked up in April (to 1446K) – mortgage purchase applications remained above year-ago levels (+6% y/y), which is supportive. But even with an uptick, permits will be constrained by affordability on the demand side and cost pressures on the supply side. Housing starts are expected to fall slightly (to 1490K). Permit issuance typically leads starts by one month and permits fell between February and March.

Aside from the housing market data, we expect to see jobless claims hold steady for the week ending May 16th. Both initial and continuing claims have moved lower on a four-week moving average basis since the fall. We continue to expect that the unemployment rate will move sideways through the remainder of the year, despite recent headlines announcing layoffs.

About the Authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. Carrie is responsible for projecting key US indicators including GDP, employment, consumer spending and inflation for the US. She also contributes to commentary surrounding the US economic backdrop which she delivers to clients through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.