We’ve been consistent: One shouldn’t bet against the US economy. Primarily, that means the consumer—who accounts for nearly two-thirds of US GDP.

The consumer has held up well since the start of the year even as energy costs surged, buffered by a long list of shock absorbers: Tax refunds, plentiful savings, and manageable debt loads.

Now, as energy costs decline, it’s tempting to think consumer spending can accelerate. But that might be too optimistic a take. Despite headline resilience, the energy shock, coupled with persistent non-energy prices, have weakened the US consumer and their capacity to absorb further price pressures.

That’s not enough to break our cautiously optimistic U.S. narrative. The K-shape and ultra-resilient high income consumer is still in play, so too is a tight labor market that will keep Americans employed.

But, businesses may increasingly find their ability to pass prices through to end consumers is eroding for the first time after the pandemic, and that’s a shift worth monitoring.

Non-energy inflationary pressures remain in the system

At around US$75/barrel for West Texas Intermediate oil, energy will continue to put upward pressure on year-over-year headline inflation in until February 2027—meaning we expect another nine months of “ugly” headline inflation data.

It will be easy to “look through” the pressure over that horizon as backward looking, telling us more about an energy shock from the past (hopefully) than what’s in the future. It will, however, be much harder to look through the rest of the inflation picture, particularly as consumer prices have run above the Federal Reserve’s 2% target for well over five years—a trend new Federal Reserve Chair Kevin Warsh has expressed particular concern over.

Our concerns about inflation haven’t been confined to energy, but the broad-based nature of U.S. inflationary pressures that have persisted over a multi-year horizon. Goods inflation has risen off the back of tariffs, there are no signs of deflationary pressure coming from a tight housing market, and there is a floor under how far services ex-housing inflation can decline as the labor market stays tight. Just look at super core (core services ex-shelter) running at 3.5% year-over-year.

While the “peak” in headline inflation is likely behind us, we aren’t convinced that’s the case for non-energy inflation. In particular, there are signs that businesses aren’t done passing their higher input costs through to consumers. Producer prices are, for example, re-accelerating to a sizeable of 6.5% YoY, core producer prices are at 4.9% and core finished consumer goods (i.e. ex-food and energy) +3.5% YoY.

Moving forward, supply chain disruptions are likely to push food prices higher, and that’s a basket that no consumer can substitute away from.

Eroded buffers for consumers…

There’s no doubt that falling energy prices remove a significant consumer headwind. Problematically, however, the past four months of surging energy prices combined with ongoing non-energy inflation have meaningfully contributed to the erosion of financial buffers of the past six years, notably for low-and mid-income Americans. This group is now ill poised to absorb new shocks; particularly, additional price shocks should they appear (e.g. another surge in energy prices or new tariffs).

To be sure, signs of stress are building for most consumers:

-

Real wages have turned negative and eroded purchasing power. Wages are the primary source of income for most low and mid-income earners (in contrast to the top 10% of earners, who derive more income from dividend, rent, and interest payments).

-

The personal savings rate has slumped to concerning levels (2.6% in April), down a full percentage point from February.

-

Revolving credit in Q2 is running 3.8% above a year-ago—an unusual development during a period when tax returns typically would have supported paying down debt. But that’s part of the problem. Those tax refunds are acting as a buffer to higher gas prices for many households, and that will soon be depleted (unlike 2023 when stimulus was still a more substantial tailwind). The combination of debt and high interest rates means personal interest payments are weighing on consumption, sucking up 2.5% of disposable income from consumers every month.

And yet, it’s still too early to bet against the US economy

Our outlook might seem bearish on the surface. A bruised consumer, ongoing inflation in the system, and eroding business pricing power are not typically the foundations of a positive take.

Yet, the economy continues to be meaningfully fragmented with structural trends that produce guardrails around environments that would otherwise create wobbles.

Three core guardrails against the bruised consumer include:

-

Businesses have the capacity to absorb prices even if it isn’t wanted. Corporate profit margins remain elevated as a share of gross value added (GVA)—sitting at 18%—unseen since 1965. At the same time, the compensation share (i.e., the cost of labor) has fallen to nearly 55% of GVA—lowest in the history of the data. The silver lining of this dynamic is we do think there is room to boost wages without a more significant risk of layoffs.

-

The job market is still tight, largely due to structural factors but now, increasingly, some cyclical support. We continue to expect that even in the presence of some demand destruction, a shrinking labor force means labor hoarding is more likely than cost cutting with some variation per sector. As we continue to express, the new measure of US consumer health is not whether a worker has a job, but whether they work enough hours, and earn enough to cover the cost of living.

-

The K-shaped economy is still in effect and likely widening. We are believers that the top 10% of American consumers have held up aggregate spending, supported by significant financial assets that continue to boom with ongoing stock market strength. However, there is a critical distinction to be made about topline growth forecasts and shifting dynamics under the surface. The former will look stable; the latter will become more volatile.

Taken together, the US economy is not currently facing recession risk and our aggregate expectation for US growth is still comfortable in the 2% range for this year, supported by significant AI infrastructure investment, government spending and wealthy households.

But, after six years of consumer resilience, the group is at greater risk from additional shocks and the pricing power baton is passing. How businesses choose to carry it will define the next chapter of the economic cycle.

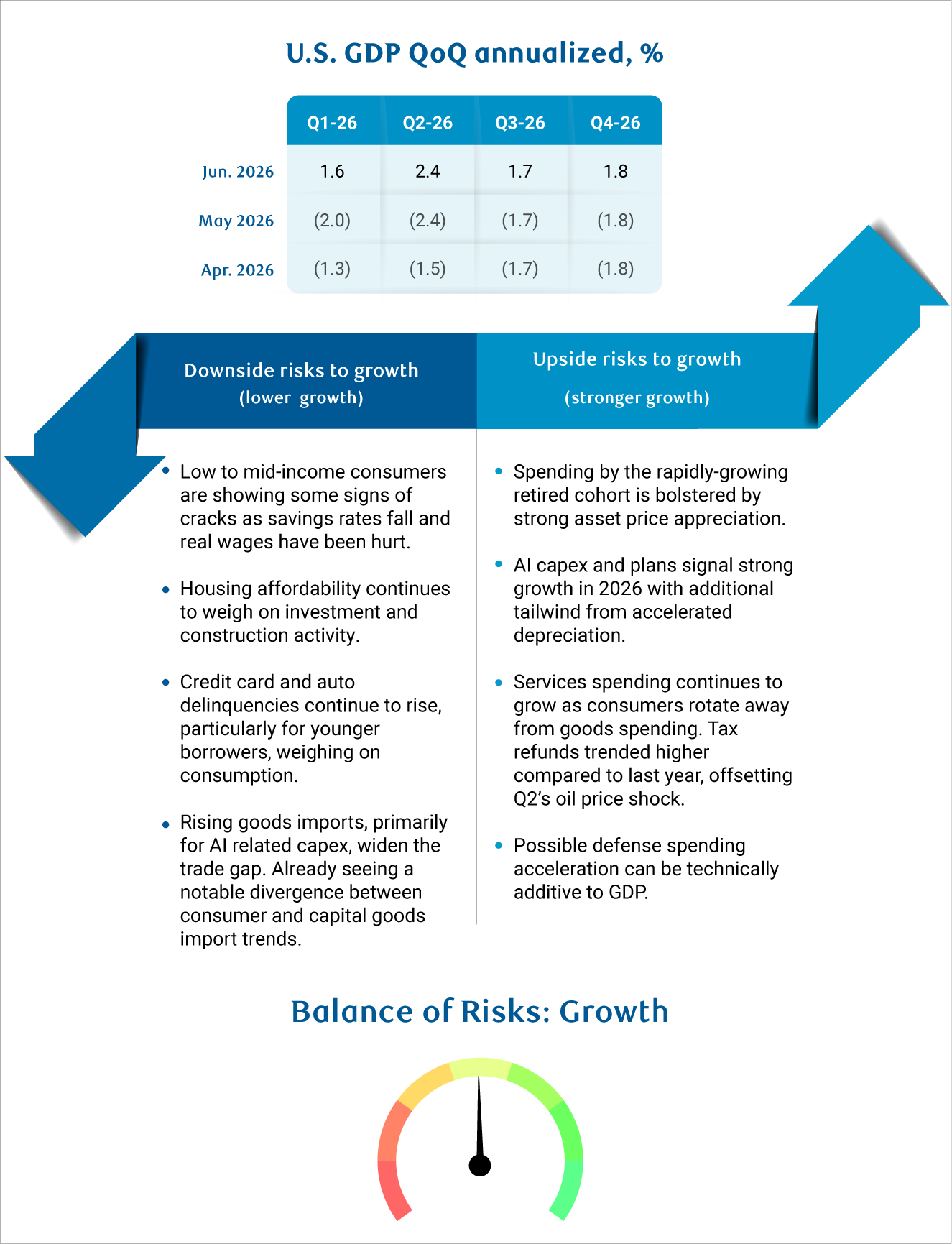

Growth outlook

House view: US economic resilience continues with underlying growth moving along a roughly 2% trend, though diverging trends persist beneath it. AI continues to drive the entirety of the business investment story: Spending on information processing equipment and data center infrastructure has surged, while CAPEX outside of the AI buildout remains exceptionally weak. On the consumer side, stronger tax returns and resilient high-income spending absorbed the energy shock, but there are signs consumer buffers among low to middle-income earners are developing cracks worth monitoring. As energy prices settle, we view risks to the economy as roughly balanced with upside surprises still possible from productivity and the AI build, and downside surprises still possible should another inflationary shock rear its head.

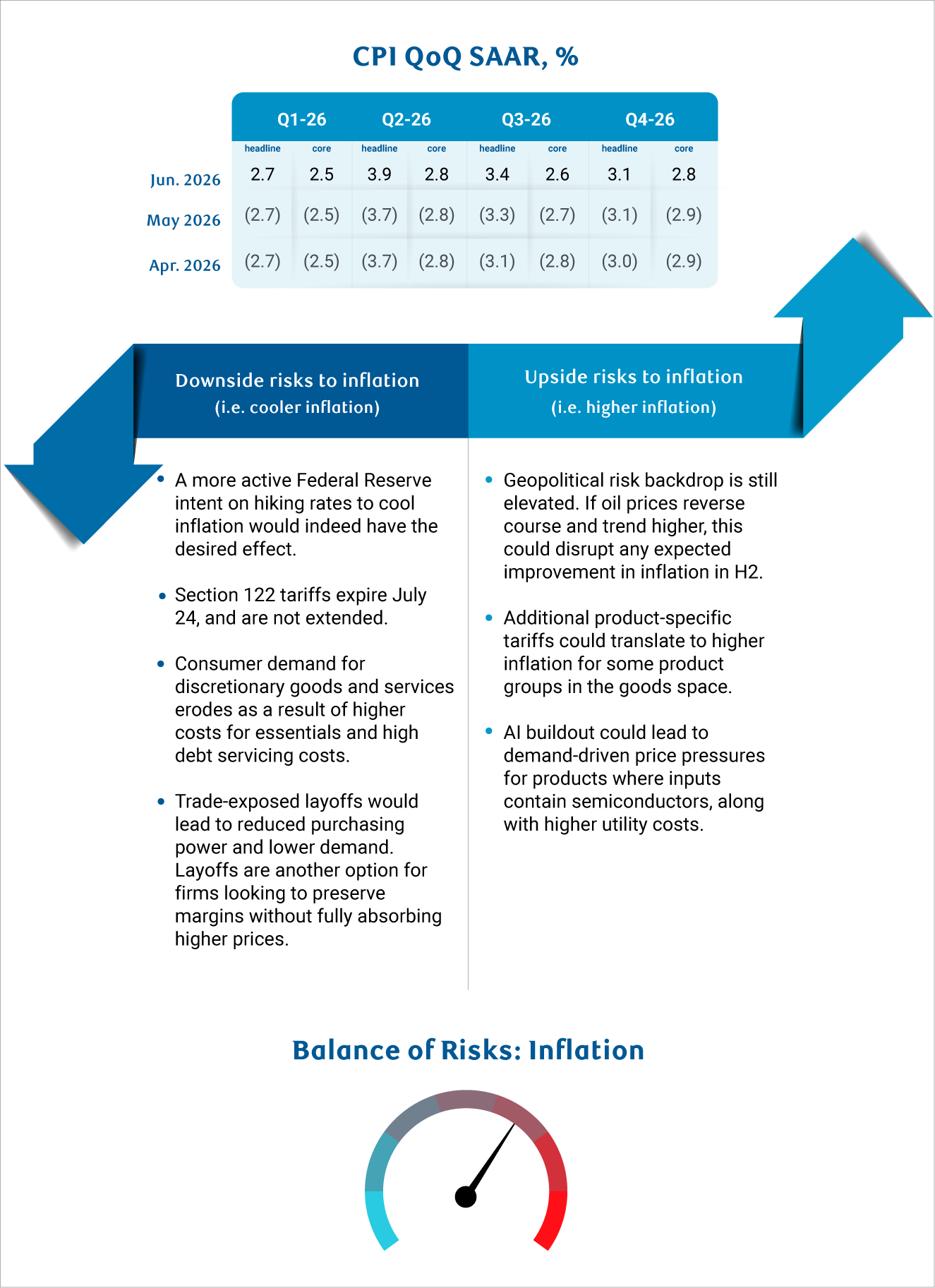

Inflation outlook

House view: Even as energy prices settle, inflationary pressures remain broad and persistent. Housing inflation is still running hot, strong wage growth continues to put a floor under core services, and tariff passthrough to core goods is still likely coming through the pipeline—as evidenced by the gap between Producer Price Index and Consumer Price Index. We expect core inflation to settle just below 3% by year-end. The new wrinkle in our outlook is incoming Federal Reserve Chair Kevin Warsh, who has decidedly positioned the central bank as keen to return inflation back to the 2% target. Should the Fed begin hiking again, the heat under inflation may be more contained.

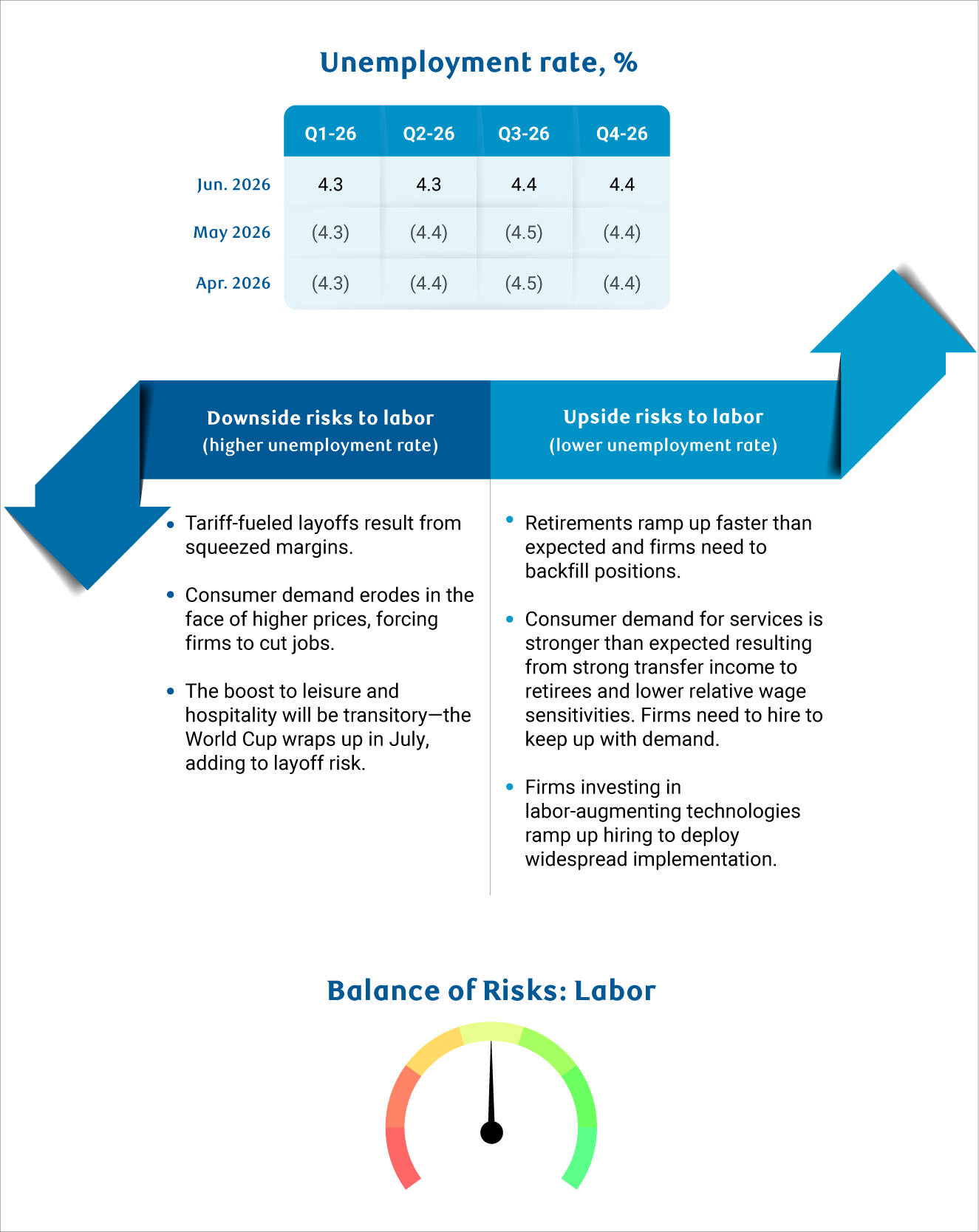

Labor market outlook

House view: We continue to expect that both structural and cyclical factors will keep the US labor market very tight. Monthly hiring has outpaced expectations—even in the context of exceptionally low breakeven employment. The composition of hiring has also broadened After a year of near-total dependence on health care, cyclical goods and services sectors are adding back some jobs shed in 2025. Still, employment in white-collar sectors remains in decline, contributing to a significant skills-matching problem facing new graduates. The unemployment rate also remains elevated for younger workers entering a market where firms are hiring selectively to backfill retirees rather than creating new roles. Real wage growth is still in negative territory, and the risk of demand destruction has not fully dissipated.

Download the report

About the authors:

Frances Donald is the Chief Economist at RBC and oversees a team of leading professionals, who deliver economic analyses and insights to inform RBC clients around the globe. Frances is a key expert on economic issues and is highly sought after by clients, government leaders, policy makers, and media in the US and Canada.

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. Carrie is responsible for projecting key US indicators including GDP, employment, consumer spending and inflation for the US. She also contributes to commentary surrounding the US economic backdrop which she delivers to clients through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.