The June 17 FOMC meeting was far more exciting than a “no policy change” headline would imply. As was widely expected, interest rates were held steady at 3.50-3.75%. However, notably, we got significant insight into Chair Warsh’s strategies for leading the Fed as well as his views on the dual mandate. His plans include new advisors, new task forces, new data, and a new regime that sounded hyper focused inflation. In fact, labor felt like an afterthought – he did not discuss the topic in the press conference until the very end. And that’s a big shift from what we heard from Powell. In contrast, Warsh acknowledged at the start of the presser “inflation has been running well ahead of the Fed’s long-stated inflation goal of 2%. That’s been going on for more than five years.”

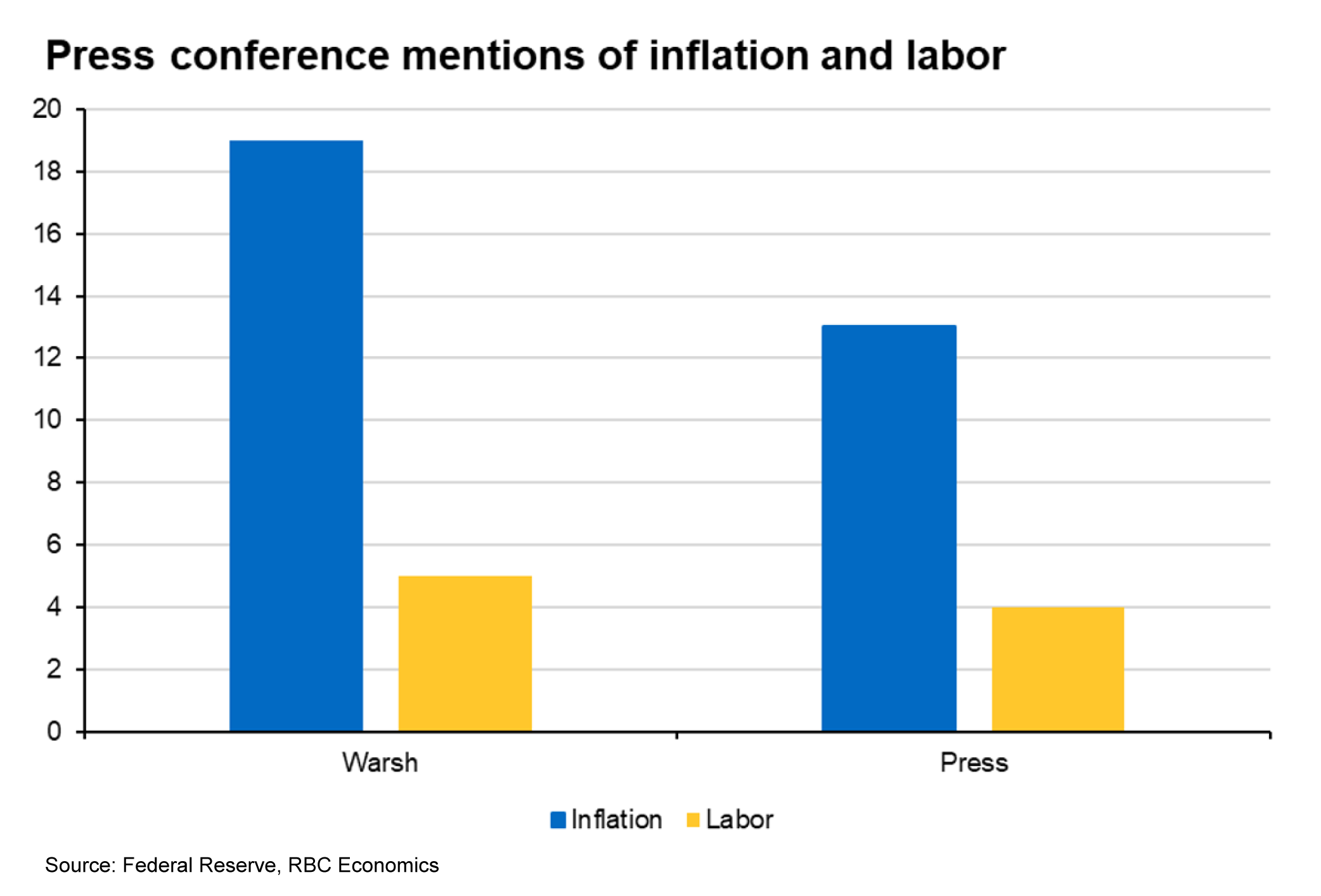

Inflation first, labor an afterthought

Most conspicuous was the jarring pivot: Warsh’s focus is clearly centered on inflation. By our count, inflation was mentioned by Warsh himself 19 times compared to only 4 mentions of labor during the press conference (to be sure, the press was equally biased). After Warsh’s opening remarks, the state of the US labor market was not mentioned until over halfway through the question period. Warsh, himself, did not speak to the state of the labor market until the very last question, at which point he simply stated, “the jobs data has been moving in a good direction,” before closing with a comment on productivity. Warsh’s current focus is very clearly directed to inflation over labor.

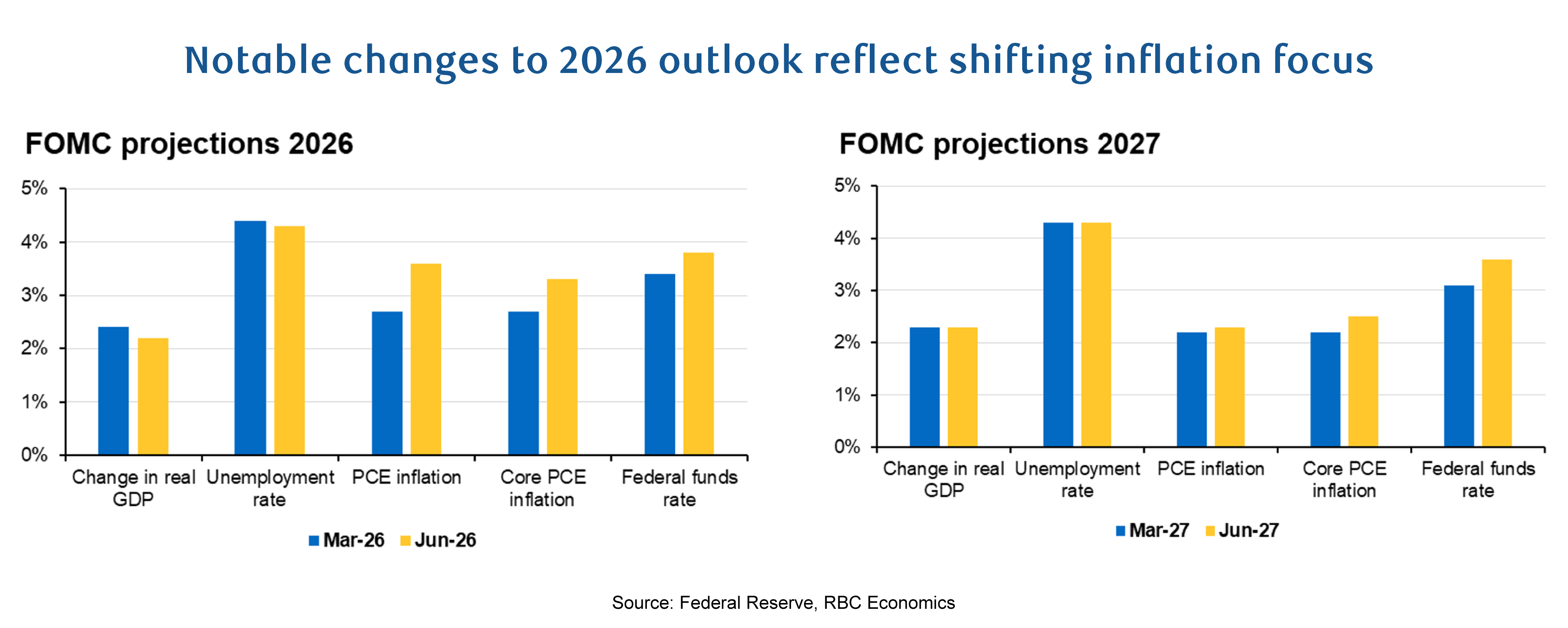

The Summary of Economic Projections signaled inflation risks are unambiguous

As expected, the Summary of Economic Projections (SEP) echoed what was stated unambiguously by Chair Warsh: inflation is the side of the Fed’s mandate warranting more immediate triage. Both headline and core PCE were revised materially higher since the March SEP, with median annual core PCE for 2026 marked up to 3.3% from 2.7% for 2026 and to 2.5% from 2.0% in 2027. Conversely, median projections for growth and unemployment moved minimally, with growth revised down slightly for 2026 (2.2%) and the unemployment rate revised to 4.3% to reflect current data.

What is most interesting in the SEP is the decidedly hawkish lean. The Fed Funds Rate projections have been adjusted to reflect a hiking bias in 2026, rather than the previously projected 25-basis point of easing implied in the March SEP. The SEP dot plot was also telling. At the March meeting, the majority of participants expected at least one cut in 2026. But just three months later, half of participating committee members have assessed that the appropriate course of monetary policy in 2026 involves at least one hike. The other half mostly assessed the current policy rate to be appropriate (with the exception of a singular Dove).

The perceived risks to inflation are skewed to the upside, if the June SEP is any indication. The range of core PCE assessments for 2026 have risen from 2.6% at the low end to 3.5% at the high end for 2026 (from 2.2% to 3.0% previously). And the range of expectations for core PCE in 2027 have widened by 50 basis points (from 2.0-2.5% to now 2.0-3.0%). Risks to unemployment are largely unchanged in the near-term, but there were wider bands around the projections for changes in real GDP in both 2026 and 2027, with growth prospects skewed slightly higher in 2027.

But as uncertainty persists, and the Fed’s path forward will become more ambiguous

Uncertainty, by Warsh’s own admission, remains elevated – due primarily to the conflict in the Middle East. But the skew of risks is shifting and the Fed will be less likely to opine on the economy’s path moving forward. One of the first and most notable changes under Chair Warch was the shorter (and simpler) policy statement – providing only the facts without the forward-guidance. Indeed, the committee felt it was no longer appropriate to provide forward-guidance in the current state of affairs. Reading between the lines, this suggests the range of outcomes for the US economy is uncertain and is being driven by forces outside of the influence of the central bank. When speaking to the dots and forecasts that were submitted by other members of the FOMC, Warsh said “they submitted their forecasts — to be clear, they weren’t this was more likely than not. This was more likely than their other scenarios. So I didn’t hear tons of conviction.” Put simply, Warsh does not want the markets to take the SEP at face value, with the understanding that forecasting must be done with humility. Interestingly, he wants to shift the responsibility of interpreting economic data to the markets:

“I think financial markets perform best when they react to incoming data. I think the financial markets work less efficiently when they ask a question, how will the Federal Reserve react to that incoming information? The more that markets are paying attention to what’s happening in the real economy, deciding what’s good data and what’s less good data, the more financial markets can price what they believe is the most likely and what are the tail risks. But when all the financial markets are doing is reflecting back what we’ve said, we’re taking the most important source of information and we’re being blind to it. I’d like us to create a system where those blinders come off.”

Following the recent string of positive labor market data, and concerning inflation readings, we maintain our view that the Fed will remain on the sidelines for the rest of 2026. Even as oil prices come down, there is notable inflationary pressure in the pipeline: key components of PPI are accelerating and have yet to reach the consumer, new tariffs are being implemented, and wage growth remains robust. And if those forces persist, the Fed’s next move will more likely be a hike than a cut.

About the authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. She is responsible for generating RBC’s US economic forecasts across GDP, employment, and inflation, and providing macro commentary through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.