Bottom Line:

June payrolls came in below expectations at 57K after last month’s 129K revision. For the Fed, the report threads the needle: job creation is slowing enough to ease concerns about demand-driven inflation without signaling outright deterioration

A retracement in the unemployment rate (which fell to 4.2%) was a product of declining labor force participation, and therefore, lower recorded unemployment.

While we continued to see signs of broadening payroll growth, the slowing pace of job creation helps ease concerns about the trajectory of (demand-driven) inflation.

We know that average hourly earnings garnered more weight in a backdrop where inflation is the most pressing concern. In June, average hourly earnings rose by +0.3% m/m, nudging the year over year pace at 3.5% which is still strong but still below the pace of May inflation.

Here are the four themes that stood out in this morning’s report:

1) Sectoral broadening continued in the June report

-

Despite a muted payrolls print, we are still seeing signs of broadening out in June. Only one-third of job creation was accounted for by health care and social assistance – in 2025 this sector accounted for the vast majority of hiring.

-

Surprisingly, leisure and hospitality (-61K) more than reversed May job gains (+40K). Within the sector, the decline was broad-based in accommodation, food services, and performing arts ad spectator sports.

-

Professional and business services continued to add jobs (+36K) and professional, scientific, and technical services accounted for two-thirds of gains.

-

Trade-exposed sectors are no longer shedding jobs. So far in 2026, roughly 200K of the near 400K jobs lost in trade-exposed sectors in 2025 have been added back. In June, jobs continued to be added back in both manufacturing (+3K) and transportation and warehousing (+2K) but with a more subdued pace than in prior months.

2) The AI buildout is supporting goods-sector hiring

-

One story that is likely not going away any time soon is the fact that the AI buildout is supporting the construction sector. Non-residential construction added 17K in June and 71K jobs since January while the residential sector – which remains in a chokehold amid extremely limited housing demand and has shed -21K jobs since January.

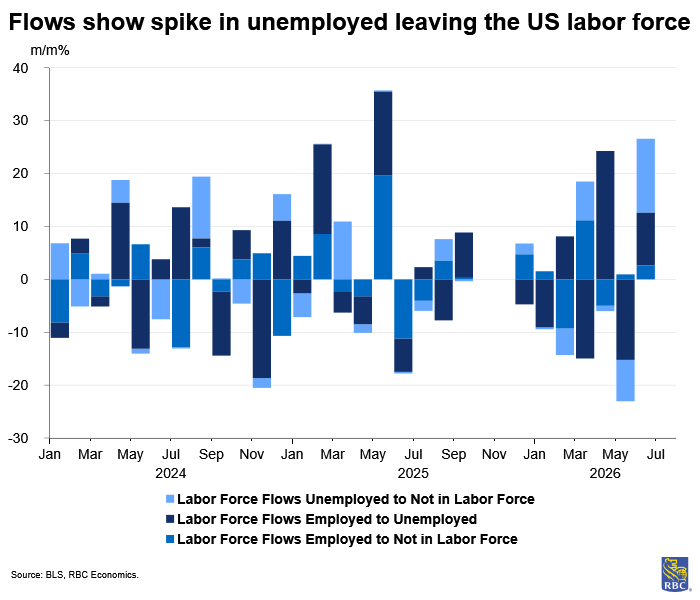

3) We saw a massive labor market exodus in June – this may well be a retirement story

-

June is typically a month where we see an influx of new college graduates searching for work. But this past month, the household survey flagged that the size of the labor force contracted by 720k, marking a massive exodus.

-

The unemployment rate fell to 4.2% as both the number of unemployed workers and the size of the labor force pulled back. This may well be a story of retirements but could also be a story of prior job seekers dropping out of the labor force.

-

The U6 unemployment rate also fell to 7.9%, with part-time workers and unemployed workers declining.

-

To-date, 27% of unemployed job seekers are considered long-term unemployed – in line with last month but still elevated.

-

Both voluntary quits and layoffs fell among unemployed workers. It is important to note that quits only counts unemployed job seekers – so retirements are not included in that number.

4) Despite a cooling labor market – the Fed is still expected to be zoned in on inflation

-

Job creation continues to look strong despite the cooling pace of new hires.

-

The good news is that the labor market does not appear to be overheating in June.

-

Even more consequential was the average hourly earnings print, which rose 0.3%, as expected. This is still considered firm wage growth, but prior to the gas price correction (as of May), real wages were hit by price pressures. Continued wage growth helps consumers recover from this hit, but the winddown of tax refunds will be a headwind at the same time.

-

The June jobs data is still expected to allow the Fed to remain squarely focused on inflation – but will certainly help alleviate concerns of imminent demand- driven inflationary pressures.

About the authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s U.S. economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. She is responsible for generating RBC’s US economic forecasts across GDP, employment, and inflation, and providing macro commentary through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.