Bottom Line:

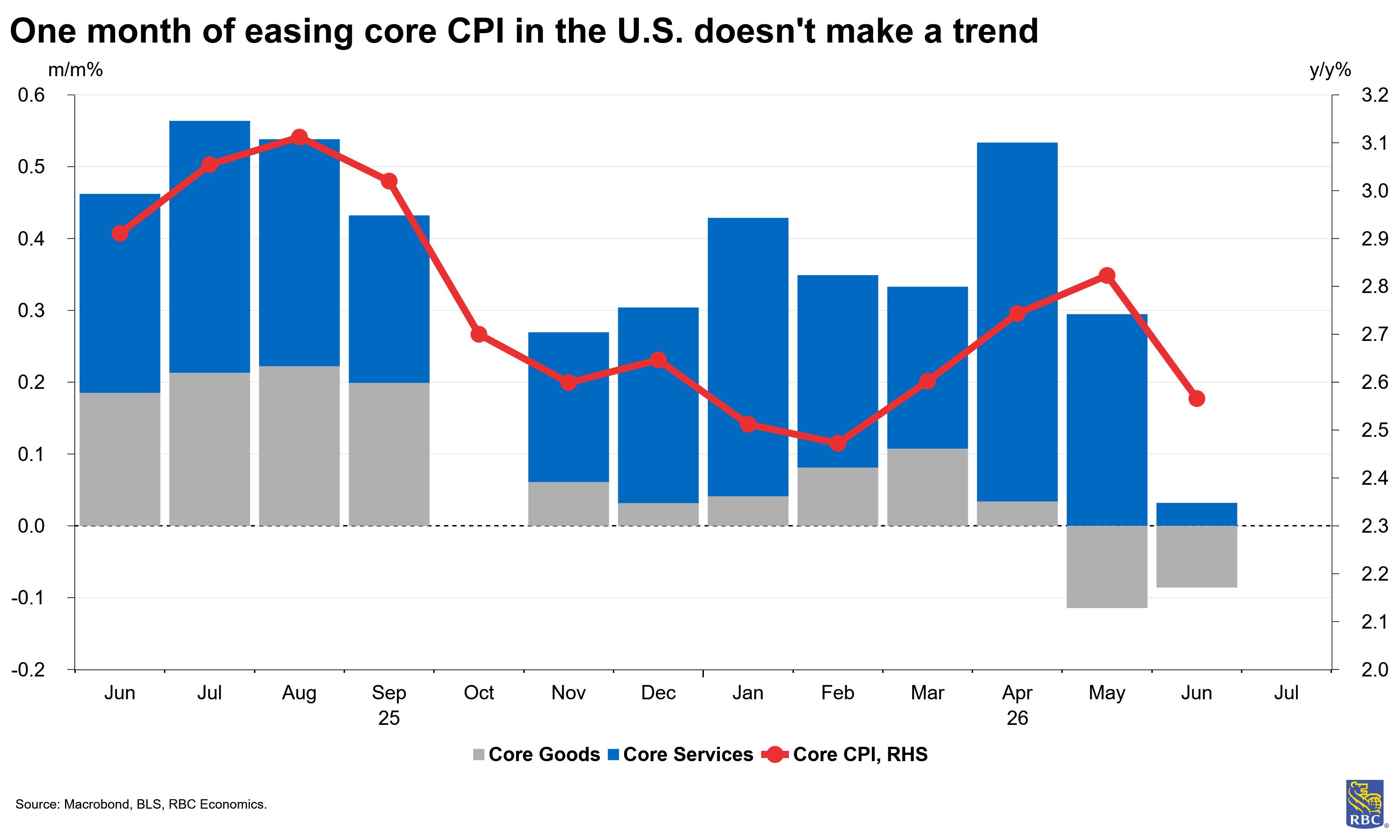

The June CPI report gave the Fed a welcome surprise, as both headline and core reported below expectations. Headline inflation declined -0.4% m/m, helped in large part by the drop in gas prices. More notable was the core inflation reading – at 0.0% m/m it was a welcome reprieve. And while it rounded to flat, this was technically the first negative month-over-month print since May 2020. Tariff pressures appear to have peaked in H1 (as we anticipated), and we did not end up seeing any pressures from FIFA as expected. Still, recent geopolitical events present upside risks to both headline and core inflation and importantly, there remains a notable gap between the y/y pace of PPI and CPI, meaning there is pressure in the pipeline.

Indeed, one month doesn’t make a trend but the underlying details should allow the Fed to remain on hold for the foreseeable future. The June print was especially consequential for the market – it widely viewed the June CPI report as the determining factor for whether a hike would materialize at the July meeting.

The combination of a slowdown in payroll growth along with the surprise core inflation reading means the Fed will see two additional months of data before their meeting in September.

There are three core themes that stood out in today’s report:

1) Core inflation outright declined (technically)

-

Core goods inflation declined -0.1% m/m. Blanket tariff pressures (IEEPA/Section 122) appear to have peaked, and we are now primarily seeing disinflation in the trade-exposed core goods space (except for recreation commodities). But product-specific tariffs (Section 232) are still weighing on motor vehicle parts and equipment pricing.

-

Core services inflation was entirely flat (+0.0%). Housing pressures appear to be abating. Month-over-month price growth for shelter was the weakest since January 2021. While OER remained firm at +0.2%, rent of primary residence rose only 0.15% m/m. And lodging away from home outright declined even amid major sporting events for the World Cup.

-

Amidst concerns of AI-fueled inflation, we have yet to see a meaningful uptick in CPI for information and technology commodities. In fact, IT commodities declined -0.5% m/m (though spikes in PPI for electronic components and accessories for intermediate demand remain a concern).

-

This morning’s prints on their own do suggest a cooler PCE print in June, though June PPI data will be crucial in determining the trajectory of PCE.

2) The breadth of inflation is decelerating

-

In the month of June, the breadth of inflationary pressures (adjusted for weighting) decelerating meaningfully. On a one-month basis, only about one-quarter of CPI basket items reported price growth at or above 3%, which is even below the pre-pandemic average share of 35%.

-

The year-over-year pace of headline inflation is now in-line with average hourly earnings (up 3.5% y/y in June). The upshot is this means we do not expect to see a spike in demand-driven inflation in the near-term, as US consumers play catch-up after gas price spiked at the same time that tax refunds are wound down.

3) No June gloom for the Fed – this print buys them time

-

It is too soon to declare victory on inflation even as we saw a retracement in June. But the outright decline in super core inflation is a welcome development. June’s print buys the Fed time – but this is not yet a trend.

-

Much of prior price pressures stem from external shocks (geopolitical, trade-related, and a structural AI buildout) and the situation remains extremely fluid with oil prices rising above post-MOU levels.

-

Spending continues to be underpinned by high-income households and retired Baby Boomers, who are benefiting from non-labor income growth, even as lower-and-middle-income cohorts remain squeezed. We are reasonably optimistic on the consumer outlook, though momentum may wane in the back half of the year if gas prices spike again, without a buffer from tax refunds.

About the authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s U.S. economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. She is responsible for generating RBC’s US economic forecasts across GDP, employment, and inflation, and providing macro commentary through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.