Canada’s economy has proven resilient through early 2026—bending, not collapsing despite significant headwinds.

A second consecutive gross domestic product decline in Q1 sparked recession concerns, but the underlying data tells a more encouraging story: Per-capita growth shows Canada is in an early-stage recovery rather than a contraction.

To be clear, the economy is not strong yet. Unemployment is still too high. Population declines will continue to limit the underlying growth rate that can be generated. Sectors directly targeted by U.S. tariffs continue to underperform, and high fuel costs are cutting into household purchasing power.

But, headline growth numbers mask an important shift: Slowing population growth is depressing aggregate GDP while measures that reflect how households experience the economy show signs of improvement.

On a per-person basis, the economy is still growing. The unemployment rate also edged lower (6.6% in May from 6.8% at end of 2025)—a seemingly contradictory outcome that makes sense only when accounting for the contraction in the available workforce.

We remain cautiously optimistic that enough support remains in place to sustain gradual improvement in those per-person and per-worker economic indicators this year with further tailwinds building into 2027.

Oil price shock hasn’t derailed consumer spending

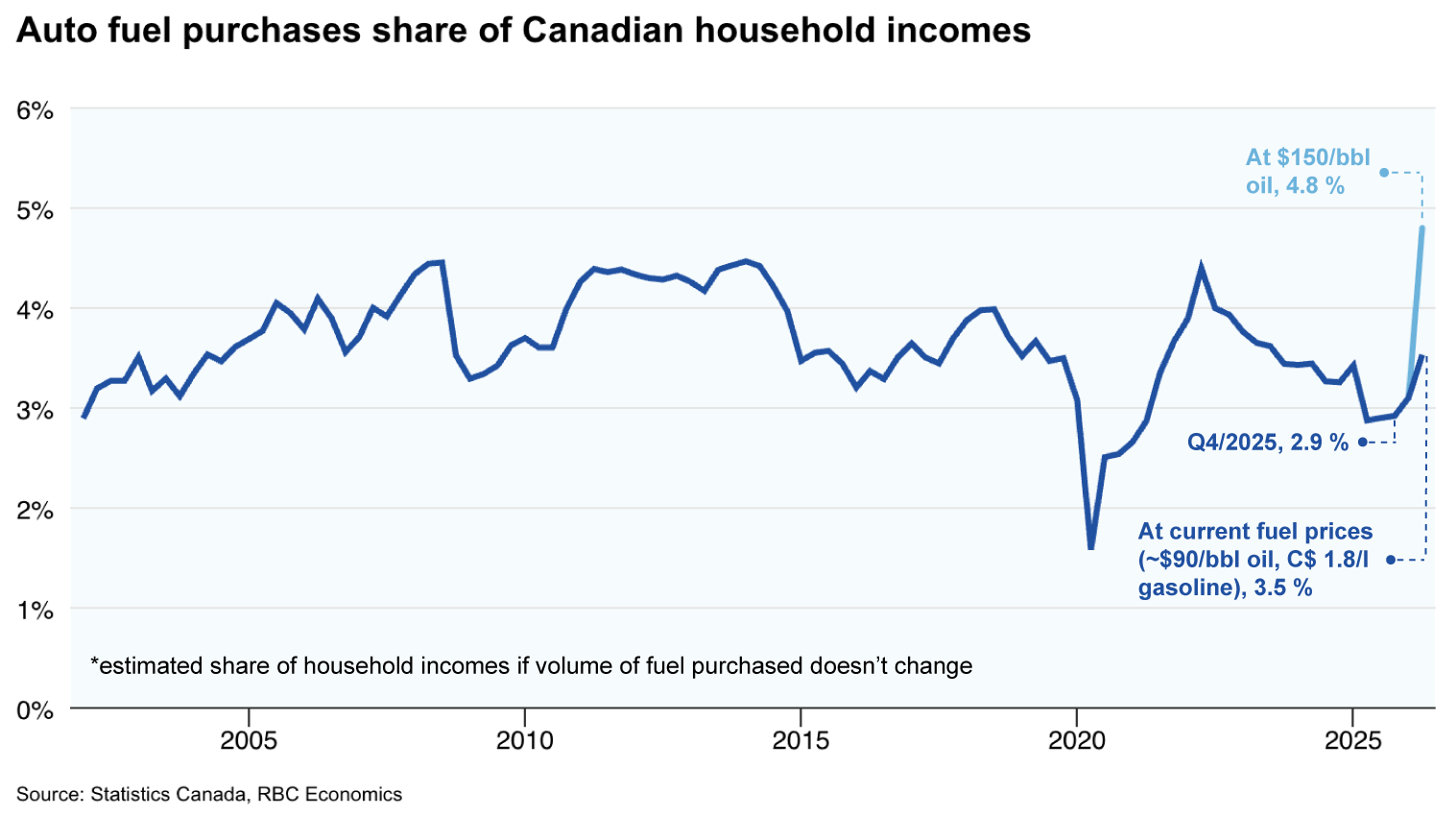

Higher energy costs are a real headwind, particularly for lower-income households where transportation costs absorb a much larger share of disposable incomes.

Yet currently, purchases at the gas pumps account for about 3.5% of household incomes overall —up from 2.9% in Q4, but not historically high.

The longer the energy price shock lasts, and the higher oil prices go, the larger the threat to consumer spending. But, for now, households have broadly continued to spend.

Canada is also a net oil exporter, and rising oil prices significantly increase revenues flowing into pockets of the economy, and boost the purchasing power of Canadian exports.

Canada’s terms of trade—the ratio of export prices compared to import prices—rose sharply in Q1 as oil prices increased. As a result, real gross domestic income—the amount of goods and services that can be purchased from domestic production—jumped 2.7% annualized in Q1 despite the small decline in real GDP.

The caveat is this revenue gain is not evenly distributed. It is concentrated in oil producing regions while high gasoline price hit all households.

Labour markets are improving per worker

We know improving is not the same as strong—Canada’s unemployment rate is elevated, particularly for younger workers.

But the direction of labour market data has been positive once accounting for the unprecedented slowing in population growth.

We have noted before that Canada is facing an unusual structural challenge: The labour force is shrinking due to immigration pullbacks, and a net population decline.

In this context, modest employment declines, that could normally generate recession concerns, are today still consistent with improving per-worker conditions. Importantly, the unemployment rate has drifted lower this year despite averaging small monthly job losses.

Still, even with early signs of improvement, labour markets are weak. Looking ahead, Canada will eventually face the opposite problem—labour supply shortages driven by retiring workers, and not enough young people entering the market.

U.S. trade policy has stabilized

At the same time, the worst fears about escalating tariffs have still not materialized.

Product-specific tariffs on steel, vehicles, and wood products continue to bite. Manufacturing production remains 3.5% below 2024 with sharp declines in steel and wood products.

But, the vast majority of Canadian exports remain exempt from U.S. tariffs under CUSMA compliance rules, and that exemption is maintained in newly proposed Section 301 tariffs set to replace current Section 122 tariffs in July.

Upcoming CUSMA extension negotiations will be watched closely, but shouldn’t actually change tariff rates here and now. The extension under consideration is the expiry date of the deal a decade from now in 2036, so current trade rules remain in effect if the deal is not extended.

But more reason for encouragement is the direction of U.S. tariffs have moved lower rather than higher. The list of exempted products from broader U.S. tariffs globally has grown to cover almost half of U.S. imports.

Overall (including CUSMA and other exemptions), the share of U.S. imports subject to tariffs has declined from a peak of 45% in June 2025 to just over one-third of imports in April 2026. Plus, average tariff revenues collected by the U.S. administration have continued to edge lower.

Policy backdrop remains supportive

We don’t expect the Bank of Canada to hike interest rates in response to the oil price shock. The BoC is closely watching whether higher oil prices feed into either broader inflation pressures (outside of the mechanical jump in gasoline prices) or longer-run inflation expectations.

But, the odds of this happening have, if anything, eased in recent months. Core inflation measures have moved lower. Much of the disproportionately large surges in jet fuel and fertilizer prices following the closure of the Strait of Hormuz have also unwound.

Meanwhile, both federal and provincial governments are ramping up deficit spending. While most growth benefits will likely appear in 2027 or beyond, the dollar amounts are substantial and will likely support growth this year.

We look for the BoC to pivot to gradual rate hikes in 2027, but that view is contingent on seeing significant improvement in the economic backdrop.

Provincial overview

Economies diverging on growth

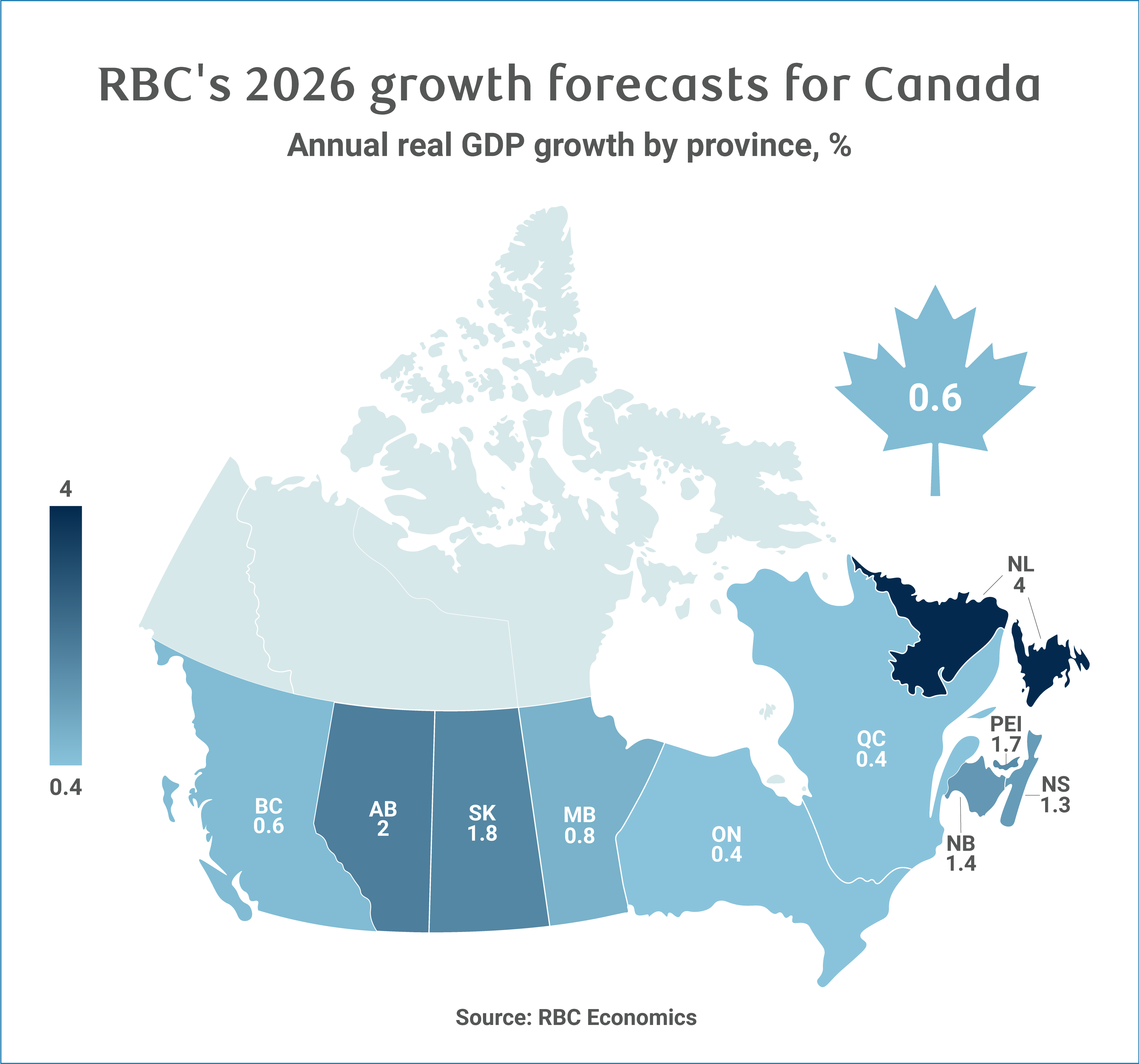

Tariffs, demographic shifts and commodity cycles are keeping Canada’s provinces on different tracks. Energy and mining hubs are set to outperform again, while more tariff-exposed provinces—like Ontario, Quebec, and British Columbia—remain behind.

Newfoundland and Labrador stands alone as Canada’s only accelerating growth province in 2026, topping our ranking with a 4% expansion. Growth will be powered by elevated oil prices and newly available production capacity at mines and offshore oil vessels—all four that are back online.

Alberta (2%) will see similar benefits with higher energy prices and robust international demand for oil supported by the recently expanded Trans Mountain pipeline. Saskatchewan (1.8%) is bolstered by additional momentum from tariff relief from China on canola.

Manitoba is set to be the slowest growing of the Prairies, expanding just 0.8%—though it will also stay ahead of the national average despite facing steep U.S. tariff pressures.

The story is more challenging in central Canada. Ontario and Quebec are projected to expand by just 0.4%—at the bottom of our growth ranking. U.S. tariffs had the greatest impact on manufacturing and investment in both provinces, while accelerating population declines compound the challenge—especially in Ontario where the population is on track to shrink in 2026.

B.C. rounds out the slower-growing provinces at 0.6%, squeezed by demographic outflows and ongoing tariff headwinds on lumber and aluminum exports.

Atlantic Canada shows more resilience. Prince Edward Island (1.7%), New Brunswick (1.4%), and Nova Scotia (1.3%) all outpace the national average, supported by government spending, and an agri-food recovery. Still, moderating construction and softer housing markets will slow growth.

Per capita GDP will see gains

While most economies are decelerating in 2026, the underlying picture isn’t quite as soft as headline numbers suggest. Slowing population growth will lift per-capita GDP in most provinces, narrowing the performance spread between the fastest and slowest growing regions.

Modest real GDP gains paired with population contractions will dramatically cut the relative weakness in Ontario and B.C. when measured per capita. Per person growth in these provinces is projected to improve and move closer to the national average, which could make economic conditions feel less strained than headline numbers suggest.

Quebec, however, will struggle in its position among the slowest-growing provinces even on a per capita basis as neither population nor growth dynamics provide meaningful support.

British Columbia – Demographic headwinds constrain growth

British Columbia’s economy showed greater resilience than expected in 2025 with stronger-than-anticipated real estate and non-residential construction, along with a material increase in pipeline transportation pushing real GDP growth to 2%.

However, momentum is expected to moderate in 2026 to an estimated 0.6% as demographic headwinds, slumping real estate construction, and trade-related challenges weigh on the economy.

Like Ontario, population growth has been slowing more sharply in B.C. than other provinces, seeing population declines over the past two quarters. Net outflows of non-permanent residents and interprovincial migrants have been key contributors with the former expected to continue as immigration levels recalibrate through 2027.

Slower population growth combined with personal income tax hikes introduced in Budget 2026-27 are expected to weigh on household spending. Retail sales growth has already eased to 1.6% year-over-year in Q1 2026, a marked slowdown from more than 6% last year.

The export outlook is mixed. Nominal exports were essentially flat in 2025 as stronger shipments to China offset weaker lumber and aluminum product exports to the U.S. Tariffs are expected to remain a headwind, while softer homebuilding is unlikely to provide sufficient domestic demand to offset weaker U.S. lumber exports. B.C. softwood lumber production fell to its lowest level in at least 11 years in 2025. A ramp up in natural gas exports from LNG Canada’s Kitimat facility could provide some export support, buoyed by elevated prices and global demand.

Sluggish housing activity has contributed to challenges for construction. Residential construction investment has been trending lower since December 2025 as weaker demand and slumping prices take a toll. Higher public-sector investment is providing some offset, alongside development of major energy projects including Woodfibre LNG and Cedar LNG among others. However, broader business investment is likely to remain subdued amid ongoing trade uncertainty, and from the impact of a potentially far-reaching land title court decision last year.

Alberta– Energy sector strength underpins outlook

Alberta’s economy posted solid performance last year, advancing 2.7% supported by strong oil and agricultural production, and construction.

Higher global energy prices, resilient oil production, and robust demand for takeaway oil capacity should keep the economy on a solid footing this year, though headwinds from slowing demographic growth are weighing on residential construction. We project the economy to moderate to 2% growth this year, but that still keeps it at the front of the pack.

The energy sector remains a primary growth driver. Middle East conflicts have kept oil prices elevated, supporting robust production. Oil output continues to rise aided by the TMX pipeline expansion, which helped boost energy exports to non-U.S. markets by $4 billion or 65% year-over-year in 2025. Strong international demand, driven in part by global supply constraints, is expected to support TMX operating near full capacity. Planned optimizations of the TMX could unlock an additional 90,000 barrels a day by next year. Dredging work by the Vancouver Fraser Port Authority also seeks to increase tanker capacity at the Trans Mountain marine terminal in Burnaby.

Labour market conditions are finding better balance amid softening demographic growth. Alberta’s unemployment rate declined from its 8.2% peak last summer to 6.6% in May—supported by solid job growth. Population growth remains highest nationally at about 1.2% year-over-year as of Q4 2025, down from more than 4% in 2024, driven in part by still strong net inflows of interprovincial migrants. This should keep consumer spending on a solid track. Nominal retail sales growth in Alberta has outpaced all other provinces, rising 5.5% in Q1 2026 year-over-year above last year’s 3% gain.

Residential construction investment has moderated as demographic growth slows. Housing starts have declined to roughly 47,000 annualized units in Q1 2026 from a peak of about 65,000 in Q2 2025. Non-residential investment is partially offsetting this weakness, supported by increased spending in commercial, and government projects. Capital intentions at the start of the year pointed to a 5.9% nominal increase in investment, though higher sustained oil prices could spur additional energy-sector investment.

Saskatchewan – Chinese tariff relief and mining output bolster growth

Saskatchewan’s economy advanced 2.2% in 2025, ranking among the country’s top performers, driven by record agricultural production and robust mining.

We expect the pace to moderate slightly to 1.8% in 2026, though the province should remain among the country’s fastest-growing economies, underpinned by rising mining output and Chinese tariff relief.

China’s revisions to agricultural tariffs on Canadian exports in March provide relief for exporters with the reduction in canola seed tariffs from 75.8% to 15% already prompting a notable rebound in shipments and canola prices. More broadly, Saskatchewan’s resource sector continues to benefit from favorable market conditions. Elevated oil prices will lend near-term support to its energy sector. Mining output remains robust with potash production up 8% year-to-date, and the McIlvenna Bay copper mine now in production amid near-record copper prices.

Agricultural production was a major driver of momentum last year, supported by record crop yields. While planting conditions have been less favourable in 2026, with weather-related challenges initially slowing seeding progress, the latest crop report suggests seeding has advanced to 93%, though still trailing the five and ten-year average of 97%. Farm cash receipts are up 1.9% in Q1 2026 from the same period last year, a modest gain given last year’s strong production. But, we expect improved Chinese market access, strong domestic demand for canola crushing, and increased demand for biofuel amid higher oil prices to provide further support going forward.

Construction is cooling as slower demographic growth eases pressure on residential investment. Home resales are down about 7% year-to-date contributing to softer housing starts, which tracked around 4,800 annualized units in Q1 2026, down from last year’s near 6,200-unit pace. Higher commercial and government spending is providing a partial offset with major projects like BHP’s $14 billion Jansen Potash mine continuing to support employment and growth. Capital spending intentions earlier this year suggested nominal investment would tick slightly lower down about 1% from near-record levels last year, but that would still rank at around the third highest private capital investment since at least 2006.

Manitoba – Manufacturing faces growing trade headwinds

Manitoba’s economy expanded by a modest 1.3% in 2025 as strong agricultural production and construction helped offset pressure on manufacturing.

The province continues to face significant headwinds from U.S. trade measures. Tariffs on heavy trucks, buses and patented pharmaceuticals, along with the expanded scope of existing tariffs on metal derivatives are expected to weigh on manufacturing, contributing to a moderation in overall growth to 0.8% in 2026.

Manitoba experienced notable nominal export losses last year as marginal gains to countries like Japan and Mexico couldn’t offset weaker U.S. demand. Some relief may come from an improved trade outlook with China, where tariff relief on canola seeds and peas provide near-term support to agriculture and food manufacturing. While early weather-related challenges slowed seeding progress, current reports suggest seeding is at 93%, near the five-year average of 95%.

Residential investment remains a key source of resilience, increasing 35% year-to-date, though cracks could be emerging. Housing starts have moderated from last year, but remain above the five-year average. Strength may become harder to sustain, however, as weaker home resales, down 11% year-to-date and slowing population growth temper housing demand.

The province’s $3.7 billion capital investment plan for fiscal 2026–27, similar to last year, should provide support to non-residential construction and employment. However, trade-related uncertainty is weighing on business investment, which has been softening. Capital intentions at the start of the year pointed to a 2.5% decrease in investment, marking the first decline in five years.

The labour market remains a bright spot with the unemployment rate at 5.5% in May—the lowest among all provinces. Moderating population growth has allowed labour force growth to better align with job creation. Improved labour conditions combined with the removal of provincial sales tax on grocery store food announced in Budget 2026 should provide some underlying support to household spending, preventing a sharper pullback.

Ontario – Slowdown deepens as trade tensions persist

Segments of Ontario’s economy remain fragile. Trade tensions with the U.S. continue to weigh on manufacturing and investment with particularly acute pressures in the southcentral and southwestern regions.

Real estate remains a drag on growth, while consumer spending—though resilient so far—faces headwinds from slowing population growth, and eroding purchasing power from higher gas prices. We expect Ontario’s real GDP growth to moderate to 0.4% in 2026 from 1.3% in 2025, marking the slowest year for growth on record outside of a severe recession1.

It’s still a tricky time for business investment. Another auto manufacturer recently shelved plans for a $15 billion complex, underscoring broader hesitation among private investors. Government investment—which provided substantial support in late 2024—didn’t sustain momentum into the first quarter of the year either.

Toronto is the exception, where FIFA World Cup preparations have been bolstering non-residential construction investment, making it one of few Ontario CMAs to report growth in this category. Once construction activity subsides, the tournament should also provide a meaningful boost to hospitality and tourism.

Manufacturing remains a sore spot. Winter retooling resulted in the shutdown of several auto plants, suppressing output and job creation. Tentative signs of stabilization have emerged, however as the industry recently stopped bleeding jobs—likely tied to auto plant reopenings as well as government support, and some U.S. tariff rule adjustments. Revised tariff measures now exempt products with less than 15% metal content among additional tariff cuts.

Exports provide some support, driven primarily by surging gold demand. Shipments to new trading partners—like the United Kingdom and European Union—have risen dramatically, but largely reflect gold storage location shifts and price movements, rather than a fundamental redirection of provincial output. Nonetheless, prices are projected to remain elevated through 2026, which should keep a floor under nominal exports this year.

Consumer spending has supported growth to date, with Q1 retail sales tracking near the national average. But warning signs are emerging. Delinquency rates on mortgage and non-mortgage loans have reached the highest levels in the country, pointing to intensifying household financial stress. Contracting population growth adds additional risk to the province’s consumer spending outlook.

Quebec – Scraping by

The new year started on a positive note for Quebec with manufacturing activity bouncing from a five-year low, and consumers showing persistent resilience.

It’s a relief after a rough ride for the economy this past year. Heavy trade turbulence and pullbacks in private sector capital investment caused it to contract twice—in Q2 and Q4—pushing annual growth to a nation-low 0.8% in 2025.

Still, the outlook remains muted. Thick trade war fog will keep businesses guarded, and declining population is poised to sap some of the momentum in consumer-focused sectors. We project the economy to grow by just 0.4% in 2026.

Many provincial manufacturers are struggling in the current trade environment. The sector shrank 4% in 2025.

But increases in food products, primary metals and aerospace industries have helped stabilize the situation early in 2026.

Whether this will translate to a broader sectoral recovery this year remains to be seen, though. We expect manufacturers of wood products, furniture and metal fabricated products among others will continue facing adversity until tariffs are significantly reduced or eliminated.

While some indicators of confidence have improved, the private sector is still holding back investment. Non-residential construction spending fell 15% from a year ago in Q1.

The public sector is the main driver of capital investment. There are large transportation infrastructure, hospital, and electricity production and transmission projects on the go.

Meanwhile, consumers aren’t letting up. Retail sales in Q1 rose 3.5% from a year ago, and sales at restaurants and other food services were up 2.6%.

But, the foundation is starting to show some cracks. Our tracking of RBC cardholder spending in the province into April points to a more modest 1.9% increase, suggesting real household expenditures may be edging lower.

Some softening could be emanating from a deteriorating job market where numbers have disappointed. Employment fell by 87,000 in the first four months of 2026, and the jobless rate increased by almost a full percentage point to 6.2%.

A shrinking population is also likely becoming a drag. The sharp reduction in immigration is tempering growth in consumer demand. We expect this to continue as immigration policy recalibrates through 2027.

New Brunswick – Growth to moderate amid construction and utilities normalizing

New Brunswick’s growth is expected to slow to 1.4% in 2026 from 2% in 2025—keeping it in the middle of our provincial growth ranking. Construction, manufacturing, real estate, and healthcare will drive growth, though some sectors will offer more modest contributions than last year.

The construction sector delivered strong gains through Q1 this year, lead by residential investment—up 19% year-to-date. This put the industry on a good footing, but we don’t expect the momentum to be sustained. Home price growth is expected to moderate further this year, alongside slowing population growth, which will weigh on housing demand, and put a damper on new residential construction.

Since residential construction accounts for roughly three quarters of all construction investment in the province, the sector will face headwinds. That said, housing starts are not expected to weaken enough to subtract from overall growth. Government capital spending—to increase 21% over last year—will provide some offset as well.

Manufacturing is expected to turn positive after detracting from growth in 2025. Food manufacturing, dominated by potatoes and seafood, accounts for roughly 20% the sector, and stands to benefit from restored tariff-free trade with China.

Healthcare employment is off to a solid start, supported by 2026’s budget allocation of an additional $710 million (5% increase) over last year, which includes funding toward capacity expansion that should bolster growth.

Energy sector activity, however, faces headwinds. Saint John, Canada’s largest oil refinery and a major U.S. supplier, has been negatively impacted by Middle East supply disruptions. The refinery traditionally relies on crude from the Persian Gulf, but geopolitical conflict has choked off those supplies. Sourcing alternatives—including Newfoundland and Labrador’s offshore reserves—remain constrained and costly, creating operational challenges for the energy sector.

The utilities sector is also expected to make a smaller contribution to growth after providing an outsized boost in 2025. Much of last year’s strength reflected volatility in electricity generation, including a rebound in early 2025 after maintenance-related disruptions in Point Lepreau in 2024. Slower population growth and normalizing production this year, however, point to more modest gains for the year ahead.

Nova Scotia – Government spending keeping the economy afloat

Nova Scotia’s economy is expected to moderate in 2026 after another solid year. Real GDP growth is forecast to slow to 1.3% in 2026 from 2.3% in 2025 as real estate headwinds, and softening construction investment outweigh continued strength in public sector spending. Still, this will keep Nova Scotia in the middle of our provincial growth ranking, and ahead of the national average this year.

Government spending is slated to do a lot of heavy lifting for the economy again. The government released another outsized capital plan, nearly 50% larger than last year’s, keeping an otherwise weakening construction industry afloat.

Federal defense spending adds some upside as well. Nova Scotia’s concentration of naval activity, shipbuilding capacity, and defense-related services positions it to benefit meaningfully from Canada’s increased focus on military procurement and defense capabilities.

Still, construction is unlikely to contribute to real GDP growth as much this year. Residential investment—which partly drove the industry’s strength last year—has been on a downtrend since mid-2025. A soft outlook for housing starts suggests weakness will persist, meaning the construction sector won’t provide the same support to growth in 2026.

Real estate will be another drag on growth in 2026. Home prices are on track to fall—a sharp reversal from 4.5% growth in 2025. This shift may lead to real estate subtracting from growth, compounding the slowdown from softer construction.

However, we’re seeing early signs of relief in the fishing industry as Chinese tariff pressures ease. Provincial exports of farm, fishing, and intermediate food products were still down from a year ago in Q1, but this likely reflects export softness before China suspended Canadian seafood tariffs on March 1. More encouragingly, employment in the industry appears to be rebounding alongside food manufacturing sales. We expect the sector to be on better footing in 2026.

Prince Edward Island – Construction pullback offset by agricultural recovery, consumer strength

Prince Edward Island’s growth is expected to slow to 1.7% in 2026 from 2.8% in 2025—still near the top of our provincial rankings, but reflecting waning tailwinds from a softening construction sector. We see rebound in the agri-food sector, and robust consumer spending preventing a sharper slowdown.

Construction activity has softened significantly since the second half of 2025 and is expected to continue declining in 2026. Housing starts are projected to weaken as population growth moderates and home price gains ease.

Unlike other Atlantic provinces, P.E.I.’s government will provide minimal offset as capital expenditures remain flat in 2026. This, alongside slow homebuilding, leaves the construction sector at risk of shrinking after accounting for half of the province’s real GDP growth in 2025.

Public spending will also provide less support for growth. The latest budget plans for modest 2% expenditure growth in 2026-27—essentially flat after accounting for inflation. This marks a sharp deceleration from the robust 13.2% expenditure increase in the previous year (the largest of any province) that funded public service expansions—particularly in healthcare that drove outsized growth in the sector in 2025.

Agri-food could be a good news story. The sector is poised for a rebound about severe drought in 2025 brought P.E.I. potato production down to a 25-year low. With weather conditions normalizing and trade relations with China improving, the industry should see a recovery this year.

Consumer spending is anticipated to be a significant source of growth as well. Retail sales have been the strongest in the country, buoyed by above-average population growth and strong wage gains linked to a tight labour market.

Newfoundland & Labrador – Commodity boom leaves households behind

We’re upgrading our 2026 real GDP forecast for Newfoundland and Labrador to 4% from 1.8%, driven by elevated commodity prices and robust production across oil and mining sectors. But, headline growth shouldn’t be mistaken for broad-based strength. The commodity boom is narrowly concentrated, leaving households largely on the sidelines.

Oil production momentum has accelerated sharply as idled offshore vessels were brought back into full operation. Year-to-date production is up 29% compared to the prior year with monthly output reaching post 2020 peaks. This expanded capacity is coinciding with elevated global oil prices, amplifying the growth contribution of the newly available supply.

The mining sector is delivering similar strength. Record gold prices have hit just as the recently completed Valentine Gold mine is ramping up and expected to reach full capacity in Q2 this year. The confluence of production expansion and high prices is setting the natural resources complex up for a record year.

That said, employment gains remain largely divorced from the commodity story. The natural resource sector is capital-intensive, meaning the direct impact on jobs from extraction doesn’t commensurate with the increase in output.

With growth coming almost entirely from natural resources, our outlook for the household sector remains relatively unchanged. That is, we expect it to be neutral to growth rather than a driver. Residential investment showed promise in April, but slowing population growth and sluggish employment gains should pull housing starts lower as the year progresses. With major resource projects now complete, non-residential construction offers little support to growth.

Detailed forecast tables:

About the authors:

Frances Donald is the Chief Economist at RBC and oversees a team of leading professionals, who deliver economic analyses and insights to inform RBC clients around the globe. Frances is a key expert on economic issues and is highly sought after by clients, government leaders, policy makers, and media in the U.S. and Canada.

Robert Hogue is an Assistant Chief Economist, responsible for providing analysis and forecasts on the Canadian housing market and provincial economies.

Nathan Janzen is an Assistant Chief Economist, leading the macroeconomic analysis group. His focus is on analysis and forecasting macroeconomic developments in Canada and the United States.

Rachel Battaglia is an Economist at RBC, providing forecasts for the Canadian provincial economies and analyzing key trends in housing and consumer spending.

Salim Zanzana is an economist at RBC. He focuses on emerging macroeconomic issues, ranging from trends in the labour market to shifts in the longer-term structural growth of Canada and other global economies.

- Canada’s economy experienced two slightly negative quarters of real GDP growth in Q4 2025 and Q1 2026. Ontario’s Q1 GDP data has not yet been released. As such, the full extent of the provincial weakness remains uncertain. ↩︎

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.

Get the latest forecasts and analysis from RBC Economics.

Subscribe Now

- Oil price shock hasn’t derailed consumer spending

- Labour markets are improving per worker

- U.S. trade policy has stabilized

- Policy backdrop remains supportive

- Economies diverging on growth

- Per capita GDP will see gains

- British Columbia

- Alberta

- Saskatchewan

- Manitoba

- Ontario

- Quebec

- New Brunswick

- Nova Scotia

- Prince Edward Island

- Newfoundland & Labrador