The federal government’s 2026 Spring Economic Update was more of the same strategy, staying true to the course set out in Budget 2025 of big (growth-focused) spending, with few surprises but a couple of complementary additions.

Recently announced affordability measures were incorporated into the books, offset by a stronger baseline, leaving deficits mostly unchanged.

If anything, the new Canada Strong “sovereign wealth” Fund reinforces the view that major projects are a centerpiece of the government’s strategy to lift private business investment. It’s evident the government is willing to put more on the line to make this happen, although with an opportunity to participate in the upside.

Therefore, the spring update leaves us mostly with the same perspectives from Budget 2025.

The government is betting big on a public balance sheet that it can crowd in private capital to make the economy stronger. If they succeed, federal finances would look better than expected now.

Steering fiscal spending toward growth measures takes time. It’s a big ship to turn, and affordability pressures remain critically important to Canadians. Finally, execution is paramount. A lot has been done behind the scenes since the fall budget, but its biggest initiatives have yet to come to fruition.

-

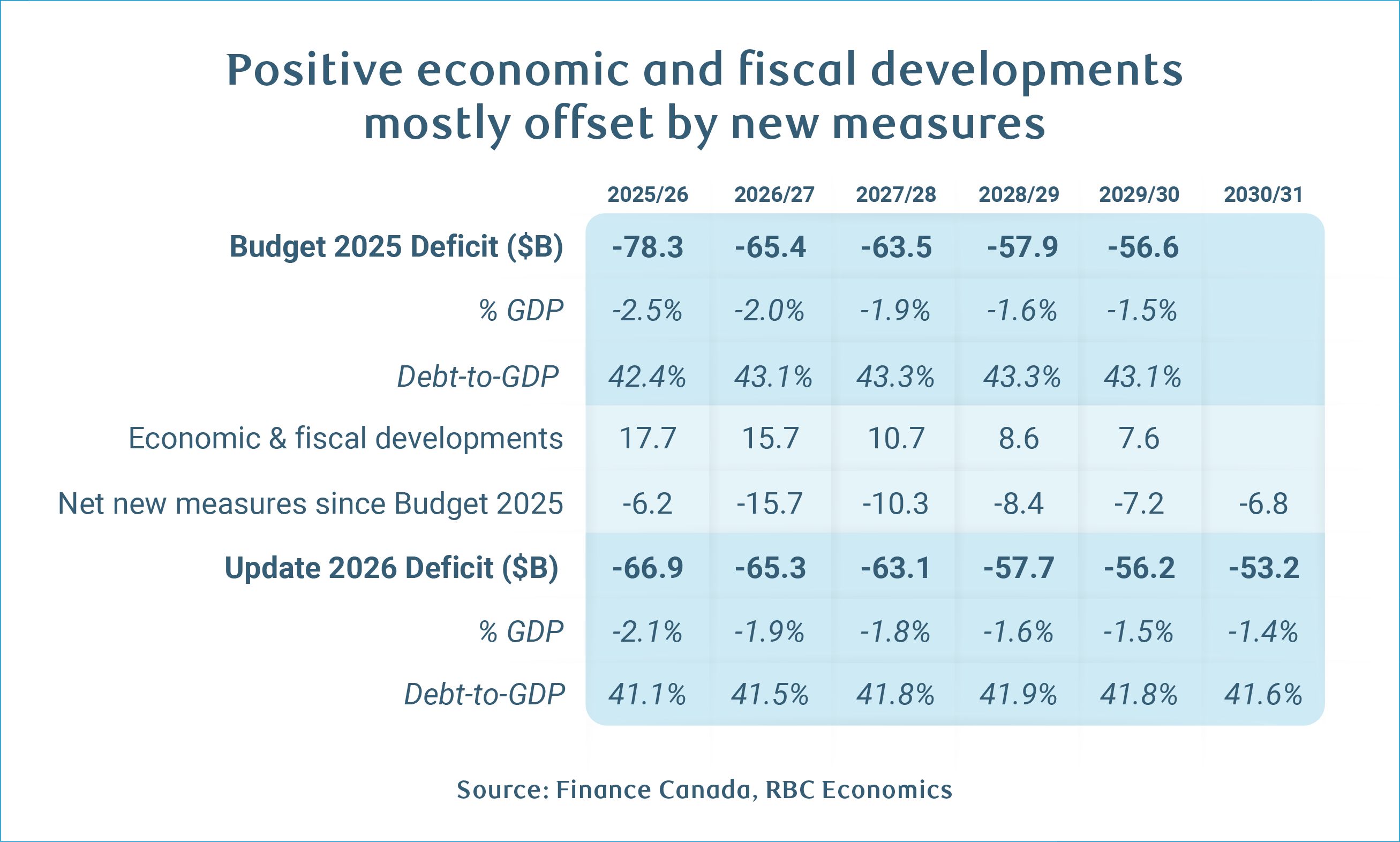

The deficit track remained essentially unchanged, except for small improvements in 2025-26. The government offset higher revenues and lower spending to date with additional new measures.

-

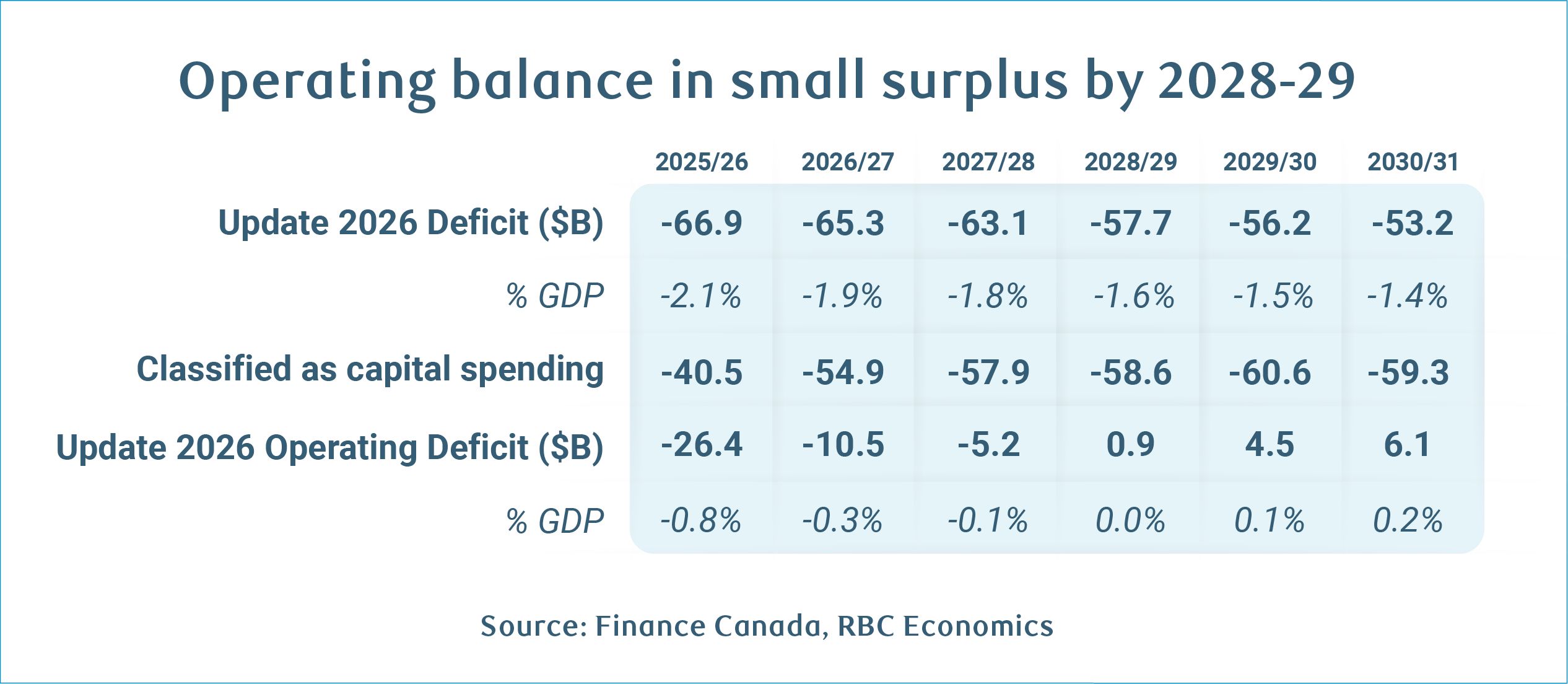

As a result, the budget remains within fiscal anchors of a declining deficit-to-GDP ratio and balancing the operating budget by 2027-28.

-

The trajectory of the debt-to-GDP ratio is also essentially unchanged, only turning downwards in the early 2030s. But, GDP revisions and improved growth projections have shifted down the debt burden from Budget 2025.

-

There are limited new details on the new Canada Strong Fund, but it’s clear it will initially be oriented toward major projects or those with federal support, providing equity upside to taxpayers alongside the risk.

-

Wages subsidies and grants to train an additional 80,000-100,000 Red Seal Trades over five years to support major projects, housing, and other infrastructure investments was the other major add on, consistent with the government’s strategy.

Deficits are stable outside of 2025-26

The deficit for 2025-26—the fiscal year just ended—is projected to come in at $67 billion (2.1% of GDP) versus $78 billion (2.5% of GDP) in Budget 2025.

Recent fiscal monitor results for February 2026 (11/12 months) showed a deficit of only $26 billion (0.8% of GDP), which means a lot of net spending is slated to come in March and year end.

The lower 2025-26 deficit is attributed to almost $18 billion in improved developments to date—split almost evenly between improved revenues and lower spending—slightly offset by new announced measures.

Improved developments carry across the forecast horizon, except they have been fully offset by new measures from 2026-27 onwards. As a result, the deficit track is essentially unchanged, hovering over $50 billion (1.4%) of GDP by the end of the projection period.

Fiscal anchors continue to be met with narrow buffers

The deficit-to-GDP ratio, however, continues to trend downwards, meeting one of the government’s two fiscal anchors set in Budget 2025, and reaffirmed in this update.

The government also meets its second fiscal anchor of balancing the operating budget by 2028-29. With minimal changes to capital allocations, the operating balance continues to improve. However, the buffer against this anchor has been reduced further, standing at only $900 million in 2028-20 and $6.1 billion by 2030-31 at the end of the forecast horizon.

There is a single mention of Budget 2025’s ultimate fiscal objective—attracting $500 billion private capital over five years—although it’s not framed so strongly, and there are no details on measuring progress.

Debt burden still rises but from a lower level

The mostly stable deficit versus Budget 2025 means the trajectory of the net debt-to-GDP ratio is also generally unchanged.

Thus, it is expected to continue to trend upwards for the next three years, only turning notably downwards in the early 2030s. However, GDP revisions, slightly improved growth projections, and a slightly reduced near-term financial requirement (see box below) have shifted the debt burden downward versus Budget 2025.

Financial Requirement

The lower deficit in fiscal year 25/26 combined with reduced non-budgetary transactions to provide a significantly smaller financial requirement of $105 billion versus $138 billion in Budget 2025. For FY26/27, financial requirements were reduced by $16 billion to $133 billion due to non-budgetary transactions. These declines mostly reflect reduced requirements in accounts payable, receivable, accruals and allowances. Financial requirements were kept within $5 billion of Budget 2025 numbers for subsequent fiscal years despite the inclusion of funding for the Canada Strong Fund.

For Government of Canada bond issuance in FY26/27, there were no changes to Budget 2025’s DMS that showed aggregate bond issuance of $298 billion. This means the current pace of bond issuance should be maintained over the fiscal year. The total is off the record high of $317 billion on a net basis (excluding Bank of Canada purchases) that was set in the just completed FY25/26. The main development in the DMS was a $18 billion decline in the planned treasury bill stock over the course of FY26/27 to $268 billion as of 31 March 2027.

– Simon Deeley, Canada rates strategist

Revenue growth revised slightly higher but little to do with oil price shock

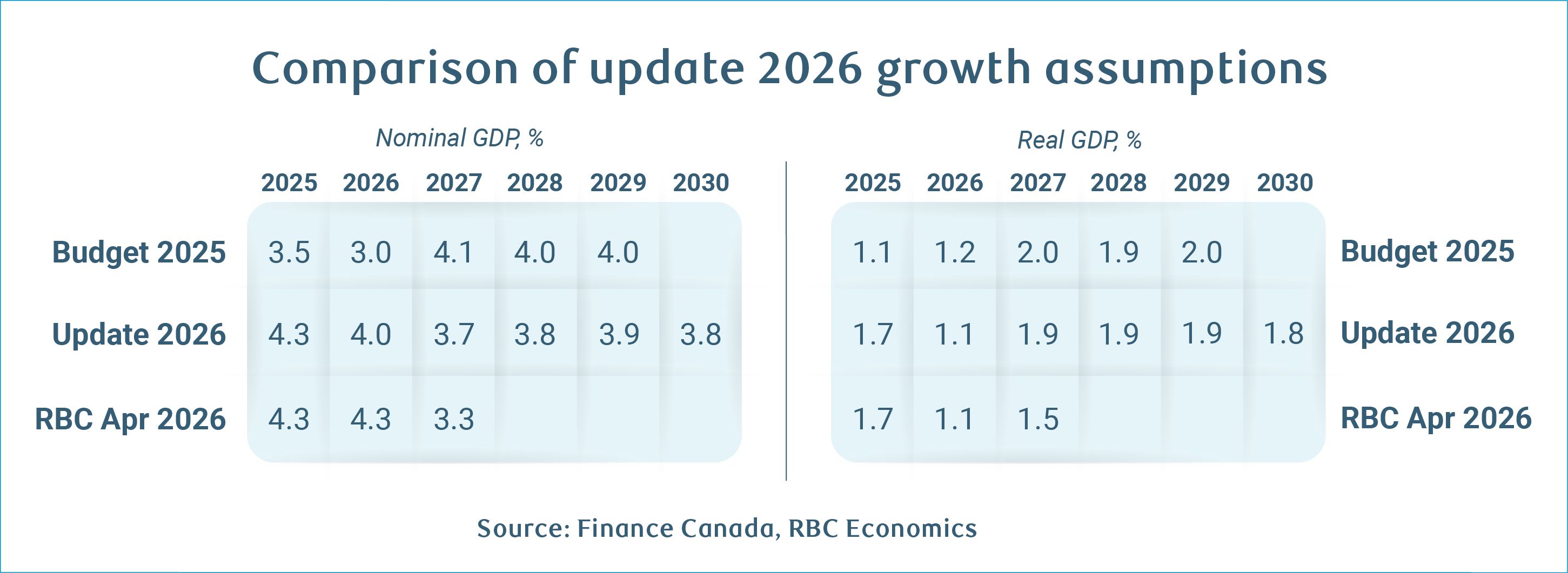

Revenue projections have been revised slightly higher across the forecast versus Budget 2025 based on higher results to date and higher projected nominal GDP in 2026.

Contributing to the nominal GDP revision is impact from the oil price shock from the Middle East conflict. Private sector forecast has West Texas Intermediate oil prices averaging US$73 per barrel in 2026 versus the US$65 expected in Budget 2025. Our most recent forecast incorporates an average of US$80 per barrel.

However, the update’s sensitivity analysis echoes our view that higher oil prices are relatively neutral for the Canadian economy overall.

While higher oil prices raise nominal GDP, the impact on real GDP and fiscal balance are more modest. Even a persistent 10% increase in WTI (about US$6.50 per barrel) would raise nominal GDP ~0.5% per year over two years, while it would be only 0.1% for real GDP and $2 billion for the fiscal balance.

Spending

The update’s presentation of measures reflects the dual challenges of government policy: Pivot spending toward growth-enhancing measures, while addressing top-of-mind affordability challenges for many Canadians.

Growth focused

The most significant new measure is the Canada Strong Fund. Otherwise, the section reiterates much of the policy directions set in Budget 2025, including advancing Major Projects Office, tax measures to encourage business investment (productivity super deduction and SRED incentives), trade diversification, defence investments, the Build Communities Strong Fund (provincial infrastructure), and expenditure review savings among others.

-

Canada Strong Fund

The update has few additional details from the pre-announcement, except that a transition office will move rapidly to finalize the fund. It will have a mandate to invest in strategic Canadian projects and companies seeded with $25 billion in federal equity over three years (no impact on the budgetary balance) and will be run by an independent, professional Crown corporation. Equity investments are its focus with projects referred to the Major Projects Office or those that receive federal support in the initial deal flow.

It’s clear this is not a sovereign wealth fund in the conventional sense of channeling surplus revenue streams, but a vehicle for allowing the taxpayer to participate in the equity upside of projects that federal programs will subsidize (at least initially). With identified major projects facing some key headwinds, the government is clear that existing entities like the Canadian Infrastructure Bank or Canada Growth Fund can help derisk projects, but this has conventionally been in the form of debt.

There is appeal to this approach, but risks as well. Both will depend critically on further details.

Individual and affordability focused

Significant new measures include the skilled trade development program, Team Canada Strong. Its objective is to train and hire 80,000-100,000 new Red Seal Trades by 2030-31. Wages subsidies up to $10,000 for small and medium-sized businesses for program apprentices, $400 weekly apprenticeship grants during technical training, and a $5,000 Red Seal completion bonus are available.

A reduction in the Canada Pension Plan contribution rate to 9.5% from 9.9% effective January 2027 was also announced providing a broad-based increase in take-home pay for workers alongside a small reduction in payroll deductions for employers.

New measures previously announced, including enhancement to the GST credit, Canada Groceries and Essentials Benefit, temporary suspension of the federal fuel excise tax, and part of the funds committed to improve housing supply (municipal development charges) have been incorporated in the update.

Combined federal and provincial balance see small changes

Combining deficits for the federal government and provinces (with nine out of 10 having tabled 2026 budgets rounded up here) shows the 2025-26 combined deficit is expected to total $102 billion (3.1% of GDP) versus $113 billion (3.5% of GDP) in fall projections with the improvement driven entirely at the federal level.

Going forward, the combined balance moves in the opposite direction. The collective balance is expected to erode with higher reported deficits driven by provincial numbers.

That said, our provincial fiscal roundup highlights how higher oil prices could improve Alberta’s 2026-27 fiscal balance enough to offset the total projected provincial increase in that year.

About the Author:

Cynthia Leach is the Assistant Chief Economist at RBC covering the team’s structural economic and policy analysis. She joined in 2020.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.