The Canadian consumer has proven remarkably resilient over the past year. Despite trade wars, immigration cuts, and persistent economic uncertainty, household spending remained a steady engine of growth.

RBC cardholder data suggests that resilience extended into Q1 2026, even as a significant new shock hit the economy—this time at gas pumps.

Oil prices surged past US$100 per barrel in late February—unseen since 2022—and have held firm. Gas prices have climbed more than 30% from a year ago, meaningfully cutting into household purchasing power.

Yet, that erosion to purchasing power hasn’t translated to lower spending overall.

Our measure of core retail sales (which excludes spending at gas stations) grew 8.2% in Q1 from the previous quarter—on par with last year—and continued to climb 1% into April month-over-month seasonally adjusted.

Spending on discretionary services led gains, indicating households are absorbing higher energy costs by increasing overall spending—rather than reallocating in existing budgets.

A gradually improving labour market should support spending momentum ahead—though gains are unlikely to land evenly across income groups and regions.

Savings provide buffer—but not for everyone

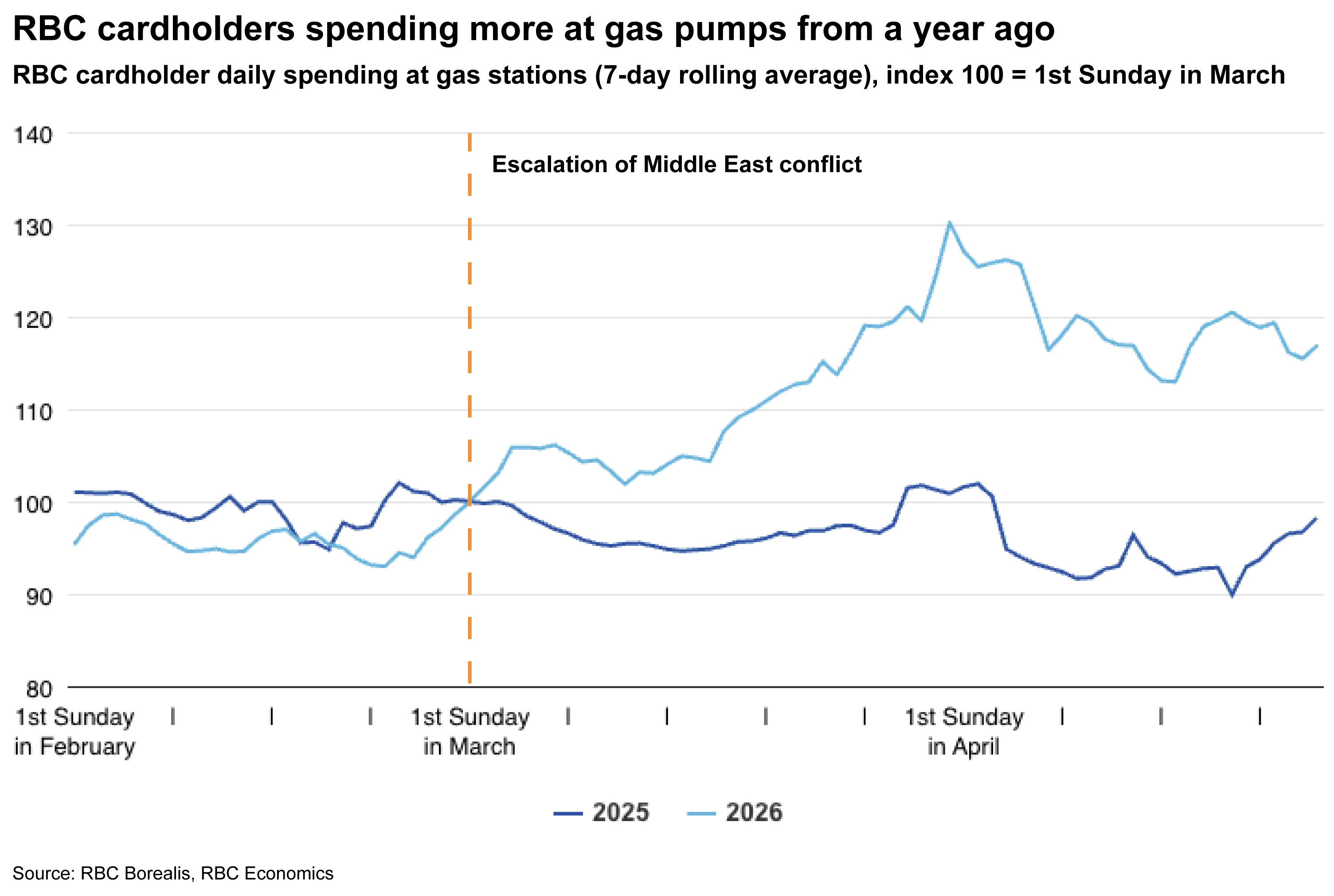

RBC cardholder spending at gas stations jumped 8.4% in March from February seasonally adjusted as the Middle East conflict escalated. This was the largest monthly jump since mid-2022—the last time oil crossed the US$100 per barrel threshold. April didn’t let up with gas spending climbing another 8.8% from March.

If households maintain transportation spending, we estimate the rise in gasoline prices would add about $67 to monthly fuel bills. For the top 40% of households—who have ample savings and financial flexibility—this adjustment is manageable.

Lower income households, however, are much more constrained. With little or no savings cushion, they could face budget trade-offs or need to take on more debt to absorb higher energy costs.

Lower-income households also allocate twice the share of their income to fuel than the average household, meaning a larger proportion of their purchasing power will experience a dramatic rise in prices.

Debt service ratio suggests some room to manoeuvre but not equally

Household debt service ratios—which measure the share of disposable income required to service total debt—remains manageable on aggregate. At current levels, ratios sit below pre-pandemic norms, suggesting households retain capacity to absorb shocks by borrowing if needed.

As discussed above, this aggregate picture obscures real vulnerabilities. Lower-income households carry materially higher debt service burdens, leaving them with far less flexibility to take on additional debt.

Likewise, some provinces have a higher concentration of households with strained debt service ratios—meaning energy price shocks could add to broader credit stress.

Labour market recovery will bolster household prospects

Though income-based vulnerabilities pose real risks for some households, the aggregate savings cushion and an improving labour market should support growth ahead.

Early labour market data this year hasn’t reflected this optimism—but underlying signals are encouraging. We continue to expect the unemployment rate will drift lower across most provinces in 2026 as population growth stalls, the trade backdrop stabilizes, and government spending ramps up.

Prime-age workers are showing particular strength, which is positive for consumer spending given their high earning power. Youth unemployment, however, remains a concern and could constrain spending among younger cohorts—even as the overall labour market stabilizes.

Regional rifts in the savings cushion

The capacity to absorb higher energy prices differs regionally as well. Households in Ontario, British Columbia, Manitoba and Atlantic provinces have accumulated less savings than other provinces, which could limit their ability to weather higher energy prices without cutting discretionary spending.

Ontario and B.C. may be especially squeezed, having experienced the largest loss in real estate values in 2025. Though declining home values don’t directly impact savings balances, households’ conscious of the decline may become more hesitant about discretionary spending.

Adding to this headwind, Ontario and B.C. are now facing population contractions as of Q1 2026, further suppressing overall spending as the consumer base shrinks.

Credit stress is already emerging in these regions. Sixteen of the top 17 CMAs experiencing the largest annual increases in mortgage delinquencies are located in Ontario and B.C.

Non-mortgage loan delinquencies are also rising most sharply in Ontario, where debt service ratios are highest, and labour markets the weakest. This could weigh on discretionary spending as more household income is diverted toward debt servicing and arrears management.

Canada’s oil-producing regions face a more mixed picture. While higher fuel costs pressure households, elevated oil prices will simultaneously boost provincial government revenues.

The net effect on households depends critically on how the government deploys those revenues—either through increased spending, or other support to help households deal with a higher cost of living—like lowering taxes.

Household consumption remains a pillar of growth

Household consumption has contributed positively to headline gross domestic product growth in most quarters since 2023. What makes this resilience notable is that it’s unfolded against a backdrop of significantly slowing population growth.

Per-capita consumption rebounded to positive in 2025 after contracting in the previous two years. We expect moderate growth for overall household consumption in 2026 and 2027 with per-capita spending poised to improve further.

That said, the aggregate picture masks disparities. While households on aggregate have sufficient savings buffers to weather near-term shocks, lower-income cohorts and regions with declining populations and persistent labour market weakness may face more binding constraints.

An improving labour market and accelerating wage growth offer important offsets, but ultimately, the outlook will hinge on how households balance competing budget pressures ahead.

About the Authors:

Rachel Battaglia is an economist at RBC, providing forecasts for the Canadian provincial economies and analyzing key trends in housing and consumer spending.

Abbey Xu is an economist at RBC. She is a member of the macroeconomic analysis group, focusing on macroeconomic forecasting models and providing timely analysis and updates on economic trends.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.