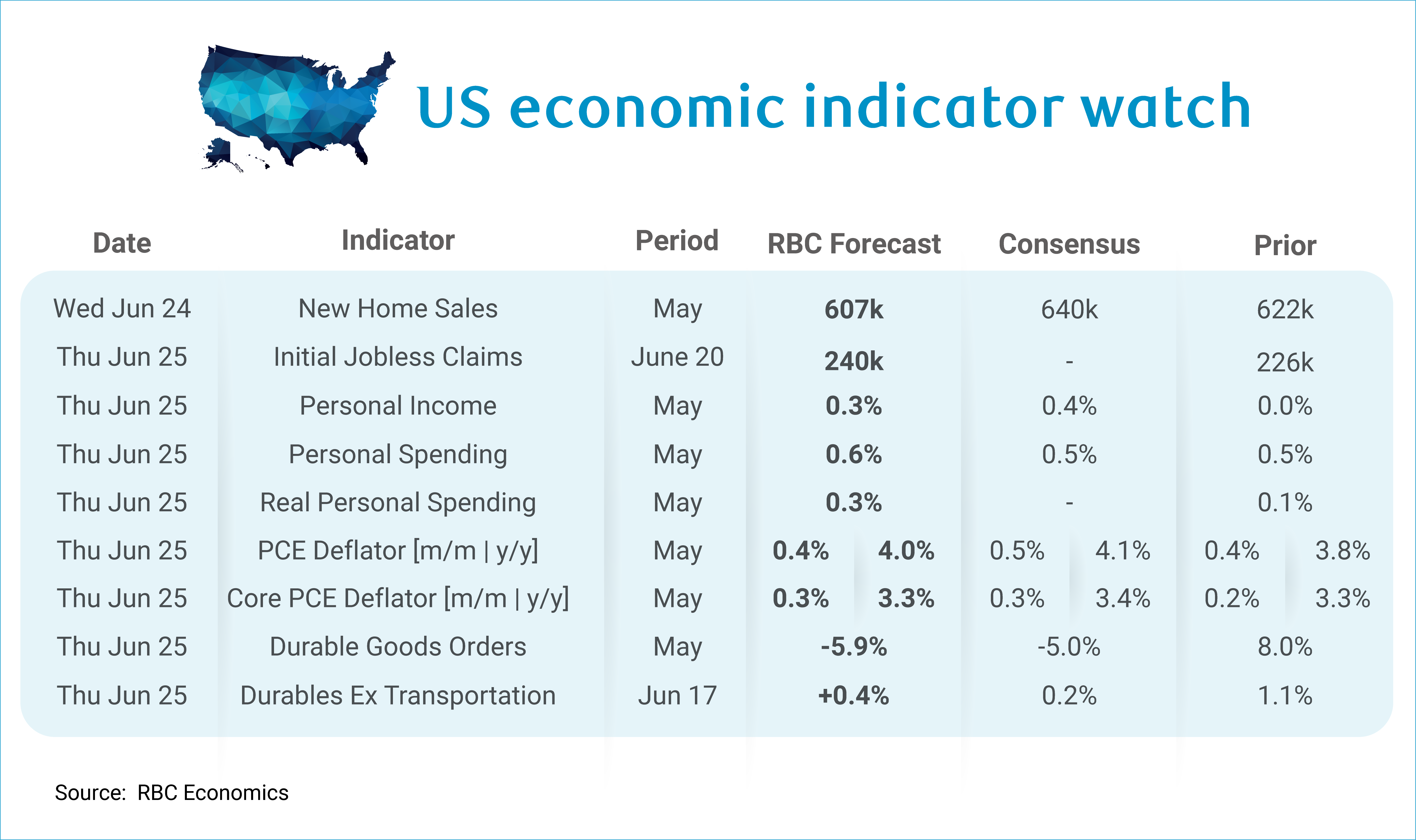

We will be watching the PCE deflators next week following Warsh’s comments at his first meeting as the new Fed Chair. The notable shift in tone suggests the Fed will be focused on bringing inflation down, and PCE has been the Fed’s preferred measure of inflation.

Unfortunately for the Fed, we do not expect that the reprieve that we saw in core CPI will be reflected in core PCE. In fact, we are forecasting a +0.3% m/m increase in core PCE in the month of May, which would leave the year-over-year pace of price growth at 3.3%. Headline PCE is expected to rise +0.4% m/m, with year-over-year price growth for all items at 4.0%. The components of PPI that matter most for PCE, namely health care and financial services, accelerated in May.

As oil prices settle lower for the first time in months, core inflation remains the most pressing concern for the Fed. The FOMC removed its easing bias from the June meeting statement and the Summary of Economic Projections (SEP) now reflect a reality that the Fed will be unlikely to cut interest rates in 2026. In fact, the Fed Funds Rate projections in the SEP have been adjusted to reflect a hiking bias.

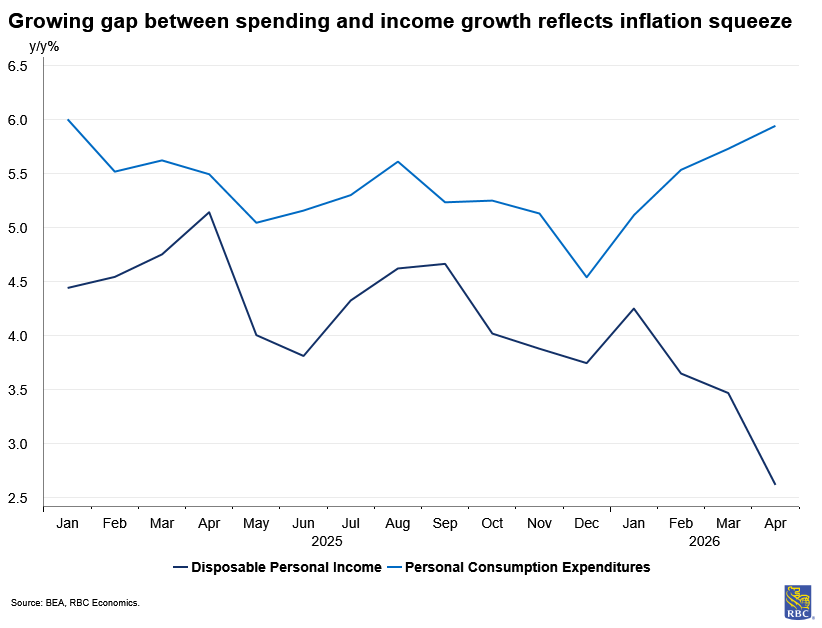

It has become clear that the US consumer has been able to weather the storm of higher prices, but at the expense of saving – and May personal spending data should confirm this. Our forecast calls for a +0.6% m/m increase in personal spending. However, we are forecasting a +0.4% m/m increase in personal income in May, which suggests that nominal spending is continuing to outpace personal income growth. This confirms that the household spending buffer is not coming from higher incomes but instead from higher tax receipts and reduced savings allocations. The personal savings rate has fallen by a full percentage point (from 3.6% in February to 2.6% in April) and we will be watching to see if it falls further in May.

Still, after netting out the impact of inflation, real personal spending likely continued to rise (+0.3% m/m). The May retail sales data confirms that real spending on goods moved meaningfully higher, quelling concerns of demand destruction amid higher gasoline prices.

Outside of personal spending data, here’s what else we’re watching:

-

We expect to see that new home sales will report lower in May at 607k. While mortgage applications rose in May, high mortgage rates and lack of affordability have weighed on housing markets this year.

-

Initial jobless claims are expected to come in slightly higher at 240k for the week ending June 20th. The week corresponds with the end of the school year and can temporarily push jobless claims higher. Importantly, we do not view this as a sign of layoffs picking up.

-

We expect to see a sizeable retracement in durable goods orders (-5.9% m/m) in the month of May, but this is a Boeing order story after aircraft orders were lower in May relative to a flurry of activity in April. Excluding transportation, we expect to see durable goods orders rose +0.4% m/m.

About the authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. She is responsible for generating RBC’s US economic forecasts across GDP, employment, and inflation, and providing macro commentary through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.