Also in this edition: Tariff lawsuits ramp up, Canada-India relations are re-energized, and two economic giants strike the “mother of all trade deals.”

Getting our house in order

On the same day the International Monetary Fund released a report showing that the removal of internal trade barriers in Canada could result in a 7% boost in real GDP, an important discussion took place at the Canadian Club of Toronto.

Two of Canada’s top CEOs—Tracy Robinson of CN Rail and Max Koeune of McCain Foods—joined Sean Strickland of Canada’s Building Trades Unions for a discussion with the Business Council of Canada’s Goldy Hyder, on the big changes that Canada needs to make to infrastructure development, business regulation and immigration.

Here are some bottlenecks we need to fix—quickly:

-

Canada is among the worst in the OECD in days lost to labour disruptions. That means our connective tissue to the world—ports, rail, sea lanes—are MIA when the rest of the world is expecting us to be on time.

-

The TMX oil pipeline expansion took longer to permit than to build. Just one of many agonizing stories about our glacial speed of permitting and other approvals.

-

Despite massive shortages in the skilled trades, our provinces are bringing in paltry numbers through immigration. Who else is going to build all those big projects?

-

It’s easier regulation-wise to export food to the U.S. than between provinces. When will we get to the one economy idea?

What needs to be done?

Robinson said we need to review our approach to labour negotiations to ensure the economy doesn’t get shut down as often as it does, especially in a world when other countries are happy to see that happen.

Strickland pushed for better labour force planning, to ensure we’re recruiting the right people and right numbers for the right needs in our economy. We’ve talked about that for years. It’s solvable.

Koeune called for immigration reforms that would give permanent residency applicants a clearer view of how long it will take, and where their application is at. He called the system a “black box,” which I’ve heard from plenty of other employers in recent months.

We can’t take on the world if we don’t take on our own challenges first.

Elbows up, fine. Heads up, better.

–John Stackhouse

Look what’s trending…

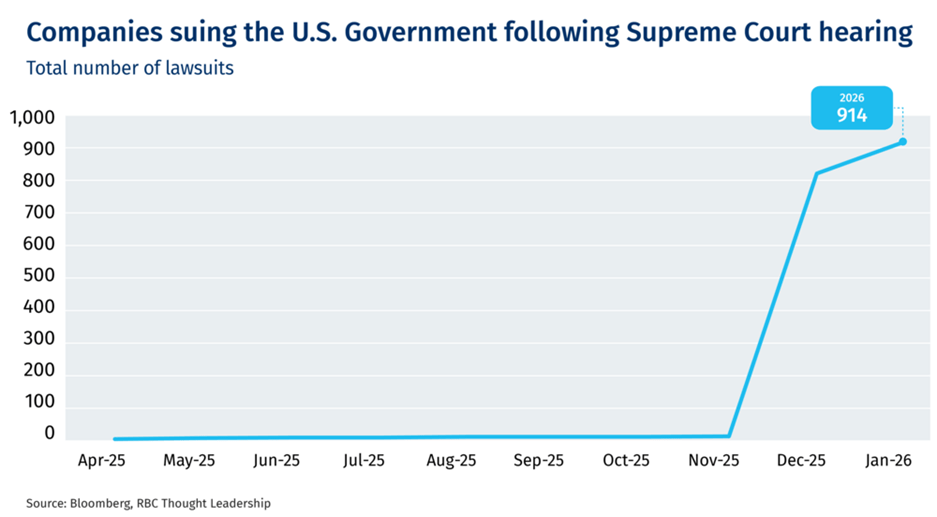

Since the Supreme Court’s November 5th hearing on the legality of U.S. tariffs, more than 1,000 companies, including Costco, Revlon and Ray-Ban, have sued the Donald Trump administration. The reason? If the highest court in the land strikes down the tariffs (verdict date unknown), the suitors hope to recoup some of the money they allege has been lost due to tariffs.

Trade posts

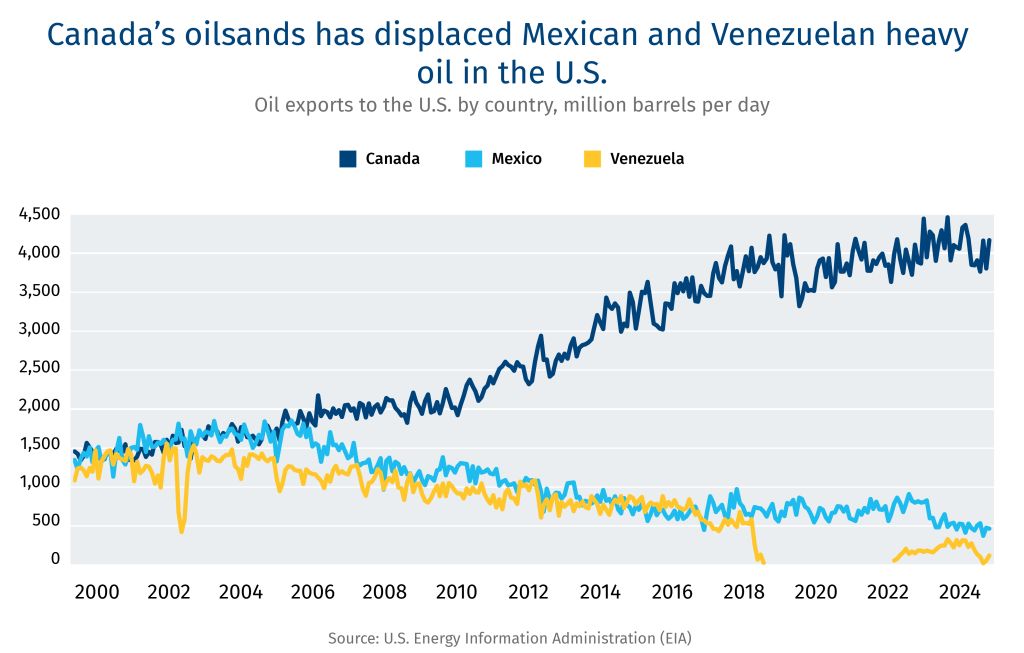

Record Canadian oil output finds new markets

-

Despite weak global prices, Canada’s oil industry is pumping record volumes and boosting exports to Asian markets, particularly China where sales more than quadrupled last year, as well as India and South Korea.

-

Though most Canada’s oil exports still go to the U.S., the sector’s resilience, record output driven by expanded pipeline capacity, and growth in Asian markets, is boosting oil majors’ shares and strengthening the country’s economic diversification drive. Expect more calls for additional pipeline capacity, to sustain this trend.

Canada-India pursue apolitical, reliable energy trade

-

As diplomatic relations continue to improve, officials pledged that Canada would supply more crude oil, liquefied natural gas, and liquefied petroleum gas to India, and that more refined petroleum products will be sent the other way.

-

Energy minister Tim Hodgson noted that India represents the fastest-growing source of energy demand while assuring his counterparts “we will never use our energy for coercion.” The relaunch of a “ministerial energy dialogue” between Canada and India promises to facilitate greater reciprocal investment and collaboration in other areas including hydrogen, uranium, biofuels, batter storage, critical minerals, electricity, and AI.

-

India’s High Commissioner to Canada said Prime Minister Carney will likely visit India in March, and that under his government no longer views Canada as the “younger brother” of the U.S.

India and EU agree “mother of all trade deals”

-

As Washington targets both with steep tariffs, two of the world’s biggest markets have agreed a trade deal that, once in effect, will eliminate tariffs on more than 90% of goods, marking a new era in economic relations.

-

The two sides made no secret of the fact this breakthrough was catalyzed by U.S. trade policy, to soften the blow of tariffs and increase their economic autonomy. This will result in boosts to India’s export of manufactured goods and give the EU preferential access to a massive, growing market.

-

The EU is already one of India’s largest trading partners, and while India is only the EU’s ninth-trading partner, the EU predicts its exports there to double by 2032. Negotiations over an Investment Protection Agreement are ongoing.

–Thomas Ashcroft