Earlier this week, U.S. Trade Representative Jamieson Greer clarified what had been building for months: the U.S. will seek to keep the core of CUSMA intact but negotiate new and bifurcated terms with Canada and Mexico.

Under the CUSMA status quo, different terms do currently exist for Canada and Mexico with the U.S. But Greer’s comments represent a material shift, one that widens the scope of issues under examination in the Canada-U.S. economic relationship and will fundamentally change how it is governed.

A deal with many strings attached

-

By negotiating bilateral grievances under parallel agreements with Canada and Mexico, Washington is predicating market access for the two countries on outcomes across multiple files, rather than a single, fixed set of rules.

-

For instance, rather than locking in a 16-year extension, Greer indicated that the U.S. is likely to trigger a process of annual reviews that can run for up to a decade–keeping the agreement in force, but under continuous pressure of renegotiation.

-

Practically, that means trade policy becomes more iterative. Outcomes on tariffs, procurement, digital rules, dispute resolution, or enforcement will not be settled once but revisited as negotiations evolve.

-

Politically, Greer is foreshadowing that it’s impossible to neatly resolve this all by the July 1st deadline, where instead he can now announce that the core protocols of CUSMA remain in place while thornier issues continue to be hashed out in expanded side agreements.

-

Additionally, with the current unpredictability in energy markets, Greer may have been looking to assure investors that the integrated North American energy market will continue with some semblance of a process in place.

-

Steve Verheul, Canada’s former chief trade negotiator, noted that the war on Iran has strained America’s supply chains across energy, aluminium, fertilizers—commodities that Canada could help supply, giving Ottawa some leverage.

The central question is about a baseline market access tariff

-

The most important issue is whether the U.S. introduces a broad market access tariff and, if so, what’s the number.

-

Many on the Canadian side argue anything above 5% would be unacceptable. But the U.S. may look to push for as high as 10%, albeit this would likely come with significant carveouts and exemptions.

-

A baseline market access tariff would have broader implications for the Canadian economy than the more concentrated effects the sector-specific Section 232 tariffs have had, as demonstrated in RBC Economics latest report: One year of tariff shocks in Canada.

Beyond trade: a more strategic negotiation

-

Prior to Greer’s comments, the USTR also released its annual National Trade Estimate Report on March 31st, listing what it deems as “significant foreign trade barriers” for partners, including Canada.

-

Most of the irritants listed aren’t surprising, they are becoming increasingly central to negotiations.

-

Because of Trump’s trade war, some of these gripes have evolved and expanded, including provincial liquor stores no longer stocking U.S. alcohol.

-

Others cut into how Canada structures parts of its economy: increased “Buy Canadian” procurement provisions, dairy supply management, digital and streaming regulations, and newfound sovereign data ambitions.

-

Adding to that is the U.S.’s strategic ambition with respect to critical minerals. Canada’s level of participation in those ambitions will be a key issue, as we discussed in February.

The timeline ahead and how it impacts strategy

-

June 1st: Greer must report to Congress on the administration’s intent–whether to extend CUSMA as is or pursue changes.

-

July 1st: Canada, Mexico, and the U.S. will meet formally for the six-year review built into the agreement, at which point the U.S. likely pushes to shift towards a 10-year framework of annual reviews.

-

The U.S. is positioning for a sustained model of negotiation under the rolling review, where it can continue to exert leverage on unresolved issues.

-

One of Ottawa’s objectives, in addition to ultimately maintaining favourable, broad access to the U.S. market, is to push decisions on priority files as close to the mid-term elections as possible, without jeopardizing the entire agreement.

–Thomas Ashcroft, Global Policy Issues Lead

Tariff Toll

It’s been a year since Donald Trump stood in the Rose Garden at the White House and announced his government’s “Liberation Day” tariffs. This week, our colleagues at RBC Economics took a close look at the impact of those tariffs. Here are a couple of the key takeaways (click on the links for plenty more analysis):

Canada: One year of tariff shocks in Canada: What we learned

-

Despite heightened trade tension, Canada was still the largest source of imports for 22 American states last year, unchanged from 2024.

-

Canada’s limited retaliatory measures minimized the trade war’s impact on consumer prices in Canada.

-

Since the U.S. tariffs on Canadian goods are targeted, the impact has been uneven across the country.

The U.S.: One year later: How U.S. tariffs and trade policy have reshaped the landscape

-

Tariffs have not reduced trade imbalances, particularly with China.

-

Tariffs revenue has little impact on reducing the deficit—for one thing, they don’t come close to making up for the Big Beautiful Bill tax cuts.

-

There is no evidence that tariff policy has led to a reshoring of manufacturing jobs.

Making headlines

-

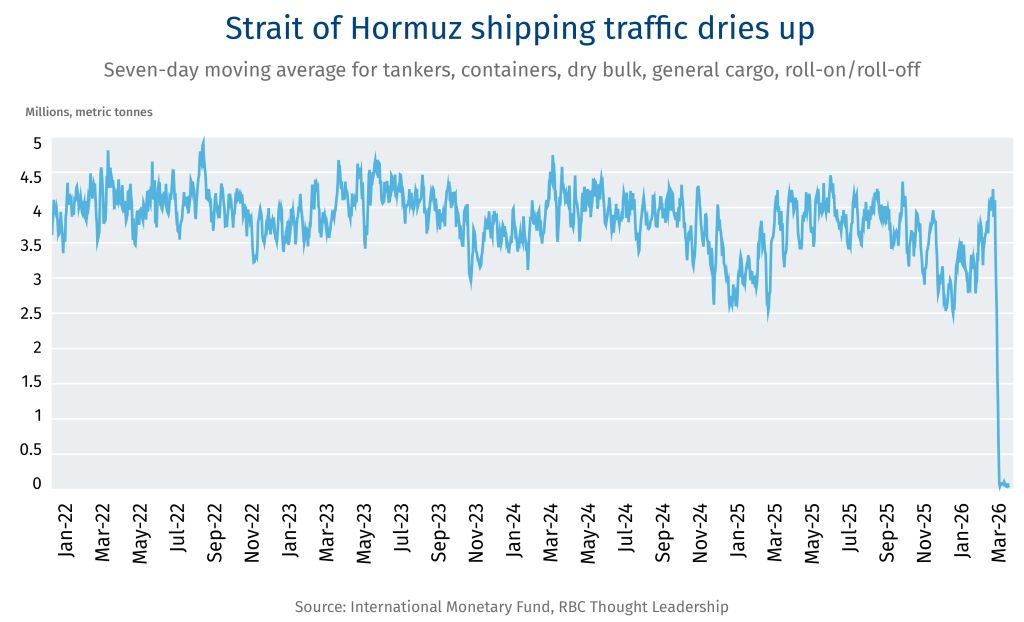

The shutdown of the Strait of Hormuz is forcing Japan to release 20 days’ worth of oil planned for May.

-

Despite heightened tensions between the U.S. and the European Union on several files, a deal on critical minerals, as part of an effort to lessen their reliance on China, is bringing the two together.

-

Global demand for AI chips drove Taiwan’s exports in March (up almost 61% year-on-year) to an all-time high.

-

International Monetary Fund plans to cut its global growth forecast. “Buckle up,” the IMF’s chief Kristalina Georgieva said, noting that the world is ill-equipped to respond to the shocks of the war in Iran.