It was Finance Day at #COP28, and there was talk of money everywhere.

You might expect that in Dubai, with its splashy display of wealth and ambition at every turn. But at the big UN climate conference that’s underway here, there were plenty of questions about where that money is coming from and where it needs to go.

Bottom line: we need to mobilize $100 trillion over the next 25 years, and even by Dubai that standards requires a stretch of imagination.

Let’s start with the big bucks. The host of this year’s climate mela, the United Arab Emirates, is among many nations looking to invest in this new age of emissions-free development. The Dubai COP (for Conference of the Parties that have signed the UN climate framework) has already raised $57 billion from member states, according to the organizers. In addition, the UAE has pledged $270 billion by 2030. The oil-rich host is also developing a proposal for a $50 billion climate investment fund, which it along with BlackRock and TPG would finance.

Much of that money is needed in lower-income countries, where industry is not able to finance a transition to non-polluting energy systems, and large investors are showing what can be done through things like solar farm and hydrogen production.

The smaller bucks are more challenging. That’s the stuff of carbon markets that allow polluters to pay people and companies around the world for climate-smart actions like tree-planting or no-till farming to absorb some of the greenhouse gases they emit. Such markets are growing slowly but steadily, promising to eventually transfer billions of dollars and inspire waves of better emissions management.

But over the past year, a spate of scandals — misreporting of tree-planting, for instance — has slowed their development.

I sat with some of the world’s largest investors on Finance Day, listening to their concerns about these growing pains for carbon markets. They’re worried climate “purists” will prevent this relatively new market from maturing. They need only look out the door to an official COP poster that reads, “let’s fix climate finance.”

The debate continues whether that can happen fast enough, especially when the finance world is still talking billions when trillions may be needed.

Also on Finance Day, Canada was on the global stage talking Indigenous equity. Chana Martineau (right, below), the CEO of Alberta Indigenous Opportunities Corporation, took the stage with Alberta Premier Danielle Smith (left) to explain how the province’s $3 billion loan guarantee facility has helped Indigenous communities gain a share and say in economic development. In just four years, the AIOC has helped produce thousands of jobs, $27 million a year in new income for communities and a clear path for $1.5 billion in benefits over the next 30 years.

Think what Canada could do with a national Indigenous loan guarantee, like the one promoted in the Fall Economic Statement. A great moment for reconcili-action.

Beyond Fossil Fuels

It’s Energy Day at #COP28 in Dubai, and given the location for the big UN Climate Conference, you might think it means oil and gas. Think again.

Fossil fuels are, of course, a focus of COP, but there’s also emphasis on renewables and nuclear. This region is fast becoming a centre for solar and wind power. It’s also one of the many growth regions for nuclear, which it wants to help champion. COP28 has already won agreement by 50 countries to triple nuclear production by 2050; one of them, China, is building 22 nuclear plants (although it has 5,000 coal-fired electricity plans). And in Europe, Germany is close to 50% renewable.

For many here, the focus of Energy Day was fixed was less on energy supply and more on energy security — at the national and household level. Countries on every continent continue to exhibit scar tissue from Russia’s Ukraine invasion, which caused prices to spike. They seem to generally too adhere to the new American doctrine that energy security is national security.

African leaders, in particular, spent the day voicing concerns about their own vulnerability to energy shortages and shocks. Many of those countries are still reliant on biomass to heat and cook, and could use better access to natural gas before they transition fully to renewables.

Into the gap come newer energy technologies like hydrogen and fusion, as well as abatement technologies like carbon capture and nuclear fusion. John Kerry, the US special envoy on climate, said he’s finally convinced fusion is no longer “30 years away.” And if that’s the case, it has the potential to transform the way the world powers itself.

Europe continues to push hydrogen, but the economics may not work.

Kerry was frank in his assessment that energy demand will continue to rise with economic and population growth: “Demand needs to be addressed.”

He urged the UN conference to set two priorities. One is to ensure all production is abated; that is, producers capture emissions that leave a plant, refinery or well. Second is to focus on methane reduction, where the sector is making enormous gains. More than 50 companies at this COP have signed the Global Methane Pledge.

With one week to go at COP28, the Dubai leadership at COP wants to maintain that focus, believing the sector can engineer itself to a cleaner future. In the coming days, it will try to make the case that in the long run, climate security will require energy security.

Glass & Steel Shrouded By Climate Anxiety

It was Buildings Day at COP28, and where better to discuss the climate impact of office towers and urban sprawl than Dubai.

Like many cities in emerging markets, Dubai’s shimmering skyline used to epitomize the human quest for progress and prosperity. Now, all that glass and steel is shrouded by climate anxiety.

Construction contributes to 40% of global emissions, sending 38 billion of tonnes of carbon dioxide into the atmosphere every year, largely from the intense heat required to make steel and concrete. At recent growth rates, emissions could double in the next 25 years, as hundreds of millions of people move to cities. And the climate oil pact would be severe. Think of all the heat needed to make all the steel and glass.

I was part of one COP28 panel that included cement companies and engineers explaining what’s possible and not. We agreed the building sector needs to find new ways to bundle climate friendly buildings, for investors and tenants, and disaggregate elements of them for investors who may want to own part of a building, like a solar-paneled rooftop, and others to stick to the main course.

Governments can do more with procurement, too, instructing developers to ensure new schools, hospitals and public office spaces are as close to Net Zero ready as possible.

The consulting firm McKisney & Co. estimates 11% of all building’s emissions could be cut with better management practices, and that don’t add to the construction costs of a building. Those savings could grow to 22% by 2030, and 40% if some costs were absorbed.

A city like Dubai could probably pay for that, using current oil and gas revenues. But it may need support to invest more.

Further down the road, new approaches like offsite construction, electrified site equipment and recycled scrap steel could help. And there are new technologies like heat pumps that can dramatically change local energy systems.

Dubai — and fast-growing cities like it — could be a good test case. The conference centre where the United Nations is gathering is more like a campus of low-rise and open buildings, each repurposed this week for climate. Such unobtrusive buildings could be a template for a new kind or urbanism — if rapidly developing countries are willing to forego skyscrapers.

Diane Hoskins, a leading architect who is co-CEO of Gensler, told our COP gathering that architects and engineers need to be more flexible, as do local governments. And they need to ensure buildings not only fight climate change, but are resilient to its harsh impacts, including heat.

The best efforts may emanate from successful business models, as the profit motive becomes an ever-more powerful driver of climate action.

A good example can be found in Hong Kong, where MPD Energy has helped the construction industry get off fossil fuels by deploying portable batteries to power equipment. Just three years ago, 100% of construction in Hong Kong relied on fossil fuels. Today, it’s 40%, thanks to batteries that can produce up to 500 kW of power and have already helped the industry cut its emissions by 40%.

The Abate Debate

Get used to the word “unabated.” It’s a clunky term that’s fast-taking centre stage at the United Nations climate conference in Dubai. The world’s major economic powers and oil producers, including host country United Arab Emirates, want COP28 to call for the winding down of “unabated” fossil fuel production, meaning anything that doesn’t capture greenhouse gas emissions at source.

Opponents of the term fear it will give oil and gas producers carte blanche to produce as much as they want, as long as they’re using carbon capture technologies. They fear such an enthusiasm for abatement overlooks the emissions caused by the combustion of fossil fuels when people drive their cars or heat their homes. And they worry there’s not enough proof that abatement technologies work at the scale that will be needed.

The abate debate will likely define COP28, which is living up to its nickname as the “Oil and Gas COP.” Not surprisingly, given its location, the conference has attracted large delegations from oil producing countries, as well as executive teams from many of the world’s biggest oil and gas companies.

They’re promoting a view that the world relies heavily on fossil fuels and won’t reduce that dependency any time soon, no matter how fast the growth of renewable energy. One astonishing fact that a UAE oil executive shared today: at the time of the world’s first climate summit, in 1992, roughly 82% of the world’s energy came from oil, gas and coal; today, during COP28, that share is 80%. Surprisingly, more than a quarter of the world’s energy still comes from coal.

Such slow progress has many climate activists pushing for more radical solutions, to force wholesale change to renewable energy. But they’re swimming against some strong currents of both supply and demand. The United States, which is now the world’s largest oil producer, is on course to pump a record amount this year and may look to increase that again next year — an election year, no less – to keep gas prices low. That’s fueling speculation that Saudi Arabia will ramp up its own production, to drive prices even lower and drive US producers out of business.

The potential of another oil war drew an unlikely visitor, Vladimir Putin, to the UAE this week. The Russian leader didn’t attend COP but he did meet with Emirati leaders, before heading to Saudi Arabia, to talk about oil production. The UAE is the world’s eighth largest oil producer and is looking to increase supply by 40% this decade.

Can all that production be abated? It’s a question COP28 likely can’t answer. But it will try to challenge the world with it.

It’s here at last—but not there yet. The federal government unveiled its much hyped (and to some, much feared) oil and gas emissions cap “framework” at the midpoint of COP28, laying down its most ambitious climate policy to date.

No other oil and gas exporting nation has placed a cap on emissions. Now Canada—the world’s fourth largest oil producer—is aiming to cut emissions by 35-38% by 2030.

To get there, the government wants to limit the sector’s emissions and establish a cap-and-trade system that would charge producers for going over the limit and put the money into clean tech funds or, if necessary, carbon offsets.

The big oil producers think they’re already on a course to hit those targets, using abatement technologies like carbon capture, but won’t get there until the mid-2030s. And then there’s jurisdiction. Alberta has been quick to say Ottawa doesn’t have the right to tell provinces how to manage their natural resources.

Ottawa put the cap framework out for 60 days of consultation. Here are some of the questions we’re wondering:

What will oil and gas demand look like in the 2030s? The feds have gone with a forecast from the Canadian Energy Regulator that shows oil production higher in 2030, at 5.1 million barrels a day, with most of the increase coming from the oilsands and Trans Mountain pipeline expansion project. Gas production will remain steady, while LNG exports will be much higher. If nothing were done, the sector’s emissions would go from 174 megatons in 2019 to 199 MT in 2030. But with abatement technologies, emissions are forecast to come down to 134 MT, which would fit within the cap.

Where’s the money? The sector won’t come close to cutting emissions at that scale without massive subsidies from Ottawa and the provinces. Exhibit A will be the Pathways Alliance, a group of oilsands companies looking to build a massive carbon capture and sequestration project for their emissions. They’re still negotiating the terms with government and expect to have a memorandum of understanding within weeks. But they will need to see clear financial commitments before breaking ground. That includes a lot more clarity from Ottawa on its proposed investment tax credits, which currently are set to expire in 2030.

Can Ottawa set up a credible tech platform? Companies are likely to push for the right to channel their own money into their own clean tech projects, subject to emissions commitments. Others will push for an independent fund, or something like Emissions Reduction Alberta, to collect money from emitters and then disburse it to credible projects. The amounts will run into the billions, which could help position Alberta as a global leader in the energy transition. Or create a trail of boondoggles.

Can the cap include a cleaner approach to offsets? The cap framework offers up a lot of flexibility for offsets, including international ones, to help those emitters who can’t get their emissions down in time. Trouble is, the global offsets business has faced growing criticism this year, largely over the integrity of climate-positive activities like forestation and land protection. The credibility of the cap will be determined in part by the credibility of the offsets that companies buy.

What do other provinces think? All eyes are on Alberta and whether the federal cap can work harmoniously with the provincial system. But the challenges of “interoperability” don’t stop there. The cap also applies to British Columbia’s LNG ambitions, Newfoundland’s offshore oil dreams and Saskatchewan’s conventional oil business, each operating under a different emissions regime. Each province may want its emissions payments to remain at home, but an open market may be needed for more options.

How much flexibility will there be? It’s extremely ambitious to think the sector can cut its emissions by 2030. So the framework includes some important “shock absorbers” that allow for production swings— oil and gas markets are volatile, if nothing else — and also possible delays in technology. The framework offers up something called “multi-year compliance periods” that sound a bit like a homework extension of three years should carbon reduction projects not come together by 2030.

Will anyone go to jail? Penalties for non-compliance are, so far, vague, ranging from a warning letter to possible imprisonment under the environmental protection laws that will house the cap. The lack of clarity on enforcement measures will continue to cause anxiety among executives who have to make the whole thing work. A good cap will need a good cop.

After a winter of consultations, the feds will have to spend another year, in all likelihood, crafting the cap into law. And by then — if not before — Canada will be in the heat of election battle. Which means all this may be a prelude for an epic national debate about the future role of oil and gas in our economy.

If there were any doubts how far climate has fallen down Santa’s wish list for the Trudeau government, read Chrystia Freeland’s Fall Economic Statement. She delivered the government’s annual economic strategy without once mentioning “climate change” or “environment.” (“All I Want for Christmas is Two” could be her holiday jingle, as she dreams of 2% inflation.) Such a narrow consumer focus may be bad news for her green caucus. But Freeland’s renewed focus on execution may be welcome. In her government’s strategy for the “clean economy”—Ottawa speak for climate—she made a few things clear.

First, the new Canada Growth Fund will allocate roughly half its $15 billion funding for “carbon contracts for difference”—essentially carbon price guarantees if government policy changes. That’s a lot of money but may not be enough to underwrite a clean economy. Second, the government will soon introduce legislation for investment tax credits for carbon capture and clean technology projects, which were promised a year ago but never finalized. They will be critical to decarbonization projects, and there is some concern they’re still not competitive with U.S. incentives. Ottawa is also pushing ahead with its hydrogen agenda, promising tax breaks for ammonia, and giving more incentives for waste biomass (wood chips and crop residue) that can be used in sustainable aviation fuel. To attract more capital, Freeland gave the green light for a “taxonomy” to help banks and pension funds label investments as “green” or “transition,” and she will push pension funds to invest more in Canada’s “clean economy.”

How a taxonomy treats natural gas will be contentious, as will another Freeland proposal: a national Indigenous loan guarantee. Will Ottawa limit what Indigenous communities can buy, depending on its climate impact? A group of 130 Indigenous nations were quick to say, not a chance. After centuries of colonization, they’ll pick their own projects, including natural gas, thank you very much. Such debates will dominate the winter term, as the Trudeau Liberals try to show they can manage the current economy and help build a new one.

The weather in Ottawa turned gnarly this week, as did the politics around Net Zero. Is this the winter of our climate discontent? I spent Thursday at the Canadian Climate Institute’s third annual conference, and it was hard not to feel a change in weather. The sunny ways of the past decade are now clouded by economic reality, as governments (and consumers) look increasingly for economically minded ways to decarbonize our world. The days of free money are gone, which is undermining venture capital and all those innovators trying to create and scale new energy technologies. Governments (like consumers) are running low on fiscal gas, which will limit the billions they had hoped would stimulate climate action. The mood for regulation also seems to be dwindling, judging by the Trudeau government’s muted presentation of an oil and gas emissions cap (now called a “framework”) at the event. And then there’s all that global volatility—two hots wars and a cold one—that’s got energy markets (and market confidence) everywhere on edge.

Looking to 2024, the outlook for climate action may seem dark. But if there’s hope, it’s in private sector. This year’s CCI conference had a greater business focus, with steelmakers, oil producers and builders sharing their plans to decarbonize—not just for the planet but for their own competitiveness. That was also a clarion call from the Biden Administration, which sent its top energy diplomat to Ottawa this week to talk up business-led climate action. Geoffrey Pyatt laid out how the Inflation Reduction Act is transforming America’s energy systems (and its competitiveness), creating significant opportunities for business and trade for its allies. On that count, Pyatt wanted to know about Canada’s “political geography,” and how we can fit into a continental energy strategy that will include oil, nuclear, hydrogen and natural gas. In other words, climate security is now energy security, and both are about national security. The climate crowd didn’t embrace every word, but they did get the message. It’s a new season.

I visited Winnipeg last week and there’s a new energy in the air. The election of Wab Kinew as Manitoba premier—one of the first Indigenous persons to lead any province—has put a new spotlight on the province, its role in reconciliation and leadership in the race to Net Zero.

I met with Premier Kinew to discuss his climate policies, insights from the RBC Climate Action Institute, and whether Manitoba could be a new model for Canada’s transition. He kept returning to a single word: hydrogen. His NDP government wants to make Manitoba a green hydrogen hub, even though the province is running short of surplus industrial power. Kinew is also keen to advance electric vehicle adoption, especially for the buses, trucks and farm machines that account for a third of Manitoba’s emissions. He has a hometown advantage in New Flyer Industries, a global player in electric and hydrogen buses, but needs a growing economy to finance the transition.

More electricity generation and transmission will be an added challenge for Kinew’s promise of reconciliation. His province’s population is 20% Indigenous, the highest in Canada, and new projects will face growing tests of “free, prior and informed consent.” The same challenge will face the NDP’s promise of critical minerals production. (The province claims to hold 29 of 31 key minerals, including lithium.) Kinew said he is hoping to see “enthusiastic consent” exhibited through business partnerships.

Manitoba’s other great climate opportunity? Agriculture. I visited the University of Manitoba’s Glenlea Research Station, south of Winnipeg, to see Canada’s oldest soil sequestration test site, aimed at capturing greenhouse gases. The station is also developing technologies to capture gases from the province’s four million cows, hogs and pigs.

Manitoba is home to only 1.4 million people. It will need all the climate tech it can develop to harness their—and the province’s—energy.

Last fall RBC partnered with BCG’s Centre for Canada’s Future and Arrell Food Institute at the University of Guelph. We set out to explore what we believe is Canada’s moonshot: to produce 26% more food by 2050 (enough to maintain our contribution to the global population as it grows) with fewer emissions. The result was The Next Green Revolution: How Canada can produce more food and fewer emissions.

Throughout the past year, here’s what we learned:

Canada is uniquely placed to lead: Our assets are unparalleled, but we need to do more to maximize them. Other nations are allocating substantial funding to promote climate-smart agriculture. Canada can proportionally match those investments while establishing new market mechanisms to help finance agriculture’s sustainable transition.

Nothing will happen without accurate measurement technology: Tools to monitor emissions accurately (especially carbon sequestration in soil) are essential to building markets and helping producers take advantage of them.

Cross-sector collaboration is key: A successful transition to Net Zero demands a new approach. It requires public-private actors across the fragmented agriculture supply chain to work together, as one sector, toward a single vision.

Private sector R&D is insufficient: Canada has invented some of the most important agricultural technologies globally. But private sector funding for innovation is at an all-time low. To remain leaders in this space, we’ll need private actors to invest.

Skills gaps are limiting growth: The sector requires more workers to drive the Net Zero transition. From on-farm managers to data analysts, qualified workers and advisors are desperately needed on Canadian farms, but post-secondary funding is insufficient.

Early adopters should be rewarded: A significant number of producers across Canada have engaged in climate-smart agricultural practices for years—if not decades. These pioneers could be left out as programs develop to financially incentivize farm operators making their first transitions to better soil health methods. To continue growing current carbon stock levels, early adopters must receive a financial benefit for their continued contributions.

The world needs Canada more than ever: With global supply chains under stress from the Ukraine-Russia War and extreme climate events, many countries are facing food shortages or unstable supply lines. As a politically stable country, and a reliable supplier of safe, high-quality food, Canada has an opportunity to become the world’s sustainable breadbasket.

Key takeaways

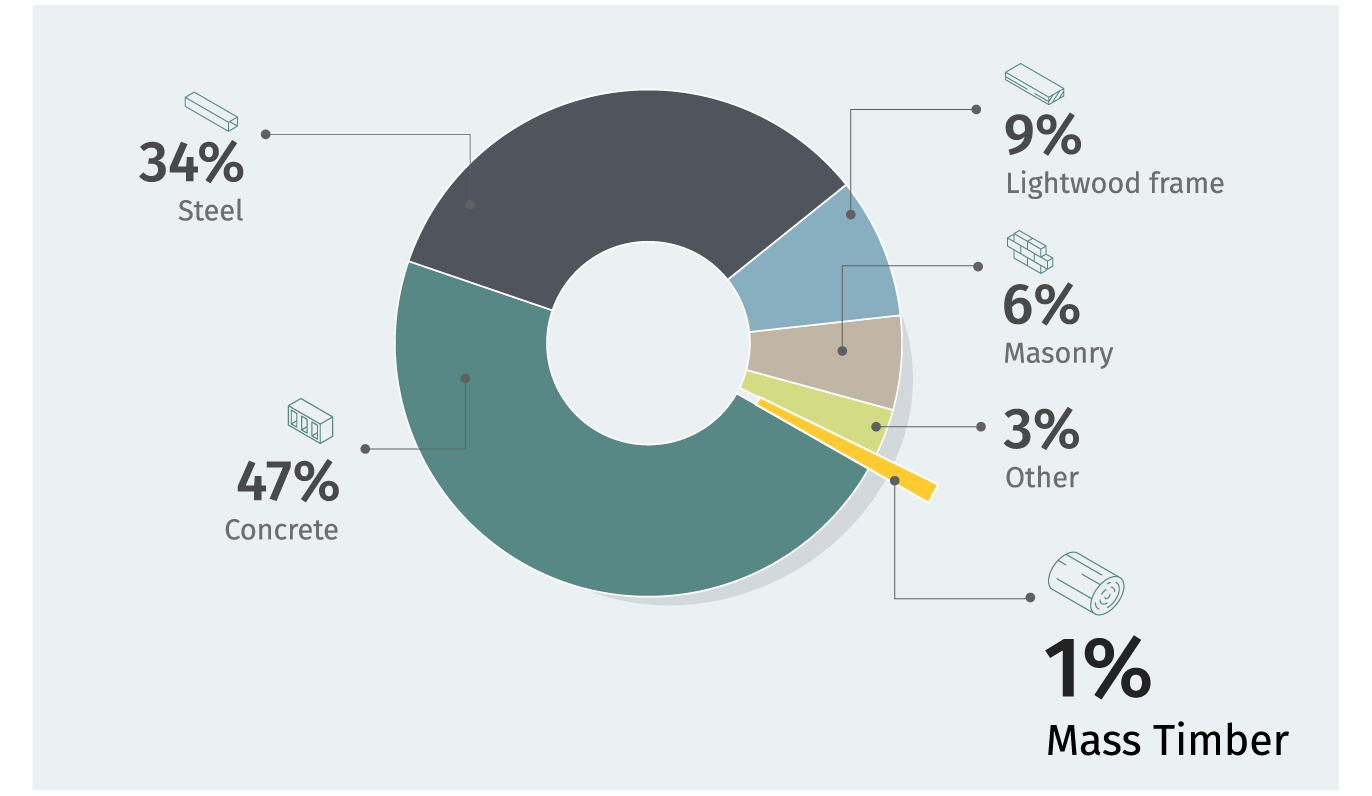

The building sector is the 3rd most carbon intensive industry in Canada, accounting for 13% of all emissions in 2022, or 92 million tonnes (MT) of CO2e. Canada aims to cut that amount to 53MT by 2030.

Widespread adoption of wood, specifically mass timber, as a substitute or complement to concrete and steel could cut embodied emissions in buildings by as much as 25%.

Mass timber deployment in new apartments, condos, and office towers could cut emissions by at least 9MT, or nearly 10% of the sector’s emissions, by 2030.

Aside from emissions savings, greater use of mass timber in building construction could conservatively grow the mass timber market by $1 billion by 2030. A share of this growth is anticipated to flow to Indigenous communities as they are in the employment catchment areas for logging sites, sawmills and mass timber manufacturing facilities.

Addressing the cost of construction and occupancy insurance, and mismatch between supply and demand is essential before Canada can achieve emissions savings, economic, and job growth opportunities.

Canada has all the puzzle pieces required to become a global leader in mass timber. The country’s climate commitments are an opportune time for all players in the building sector to come together to act on this collective ambition.

British Columbia And Quebec Spearheading Canada’s Timber Drive

Completed mass timber projects, 2022

Source: Natural Resources Canada’s Mass Timber database, RBC Climate Action Institute

661

The number of completed mass timber projects in Canada

87%

B.C., Ontario & Quebec’s share of Canada’s mass timber projects

12

The number of storeys permitted for mass timber projects in Canada

A 10-storey building rising near Toronto’s Harbourfront may not stand out among the crush of the city’s skyscrapers, but as an environmental statement it stands tall. George Brown College’s Limberlost Place is a mass-timber-and-glass structure with ambitions of being a net-zero carbon emissions building.

It’s an idea whose time has come.

While towering steel-and-concrete structures once symbolized economic growth, they are now emblematic of the climate challenge that needs to be scaled. The extensive use of carbon-intensive cement, steel and aluminum in buildings has made it the third most emissions generating sector in Canada, accounting for 92 MT of CO2e1, or 13% of all emissions in 2022. Rising populations, continued urbanization and a rush to develop multi-storey concrete buildings to address a housing supply crisis could make it harder to rein in emissions.

Canada can tap into its rich forestry resources to create a global market for large beams, panels and posts made of treated wood, that can potentially replace concrete and steel or dramatically cut their use—and their associated emissions. The rise of Limberlost Place, and the smattering of similar structures dotting Canada, suggests we may be on the cusp of the next wave of sustainable buildings: made with low-carbon mass timber and assembled like an Ikea wardrobe to help bring down emissions.

What is mass timber?

Mass timber products are solid, structural load-bearing building components such as columns, beams, and panels . They have similar fire and seismic performance as concrete and steel but are significantly lighter in weight. Mass timber can be a substitute for steel and concrete in low and mid-rise buildings. For taller buildings mass timber is typically used in conjunction with concrete and steel, where concrete is used for a building’s stairwell and elevator core and steel is used for columns.

Rise of mass timber

The emergence of mass timber in Canada as a complement and alternative to concrete and steel first emerged in 2007, with the completion of several commercial and institutional buildings in British Columbia, Ontario and Quebec2. These include the College of the Rockies Kootenay Centre South in Cranbrook, B.C., the Winnipeg Humane Society in Manitoba, and the OslerBrook Golf Clubhouse in Collingwood, Ontario. Prior to this point in time, national and provincial building codes did not permit the use of mass timber. Canada now boasts 661 completed mass timber projects. The United States, in comparison, has about 356 completed projects.

Governments or colleges/universities commissioned most of the early commercial and institutional buildings. And while they still dominate the building type mix, there’s a notable shift to multi-storey residential buildings, driven by private developers and builders. Today, a third of all planned and under construction mass timber projects are residential multi-storey projects.

Insight

Wood first:

B.C.’s Mass Timber Playbook

Several enabling policies has made British Columbia a leader in the use and production of mass timber within Canada and internationally.

The long-time champion of its forestry sector and its products, B.C. introduced The Wood First Act in 2009, with the mandate to use wood in provincially funded buildings. The “wood first” procurement approach for public projects continued with successive governments and culminated with the establishment of the Office of Mass Timber Implementation in 2020. A Mass Timber Demonstration Program was announced in 2020 to support early adopters of mass timber, such as Adera Development, to accelerate wider adoption of this low-carbon building material. The province remains quick footed in addressing regulatory barriers, specifically building code requirements. British Columbia was the first province to permit six-storey wood frame residential buildings. When the National Building Code of Canada (NBC) was revised, in 2020, to permit 12-storey mass timber buildings, the province followed suit, even though the NBC was not finalized.

The province leveraged its abundant forestry resources to mirror the playbook used by many European countries to promote mass timber. Countries with sizeable forestry sectors, such as Austria, Germany, Sweden and Finland were some of the first European countries to remove building code restrictions on wood—the most significant obstacle to mass timber use and adoption. Recognizing that government support is often needed to commercialize and scale widespread adoption of new products, these governments also provided project development, and research and development grants for builders and developers to build with mass timber.

The 9 MT emissions imperative

12-25%

Drop in buildings emissions if developers swap concrete & steel with mass timber

6%

Concrete, steel and aluminum’s contribution to Canada’s emissions

9%

Decline in building sector emissions due to widespread use of mass timber

Concrete and steel’s emissions profile is 6 and 5 times greater than wood, respectively3. Within the context of buildings and embodied emissions, concrete, steel, and aluminum account for 6% of Canada’s total emissions or 41 MT of greenhouse gas emissions, in 20224.

In multi-storey buildings, the floor system is the largest total surface area within a building and accounts for 50% of a building’s embodied emissions,5 which reside in the materials that are considered especially challenging to decarbonize. Given the emissions profile of a building’s floor system, much of current decarbonization efforts have focused on this structural building element.

Multi-storey buildings constructed with a mass timber floor system can reduce their average emissions by 27% for the floor system and 12% to 25% for the entire building structure6, according to builders with extensive experience working with mass timber.

Embodied emissions profile of a mid-rise tower

The sector could cut 5.5 MT in emissions by 20307 if one-third of all new apartments and condos and all new office towers, in major urban centres, were constructed using mass timber. Emissions could decline by another 3 MT if all future apartments and condos were constructed using a mass timber floor system and domestic manufacturing capacity was not a constraining factor8. These emission savings demonstrate that small efforts, such as changing one element of a building’s structure, can lead to significant emissions savings, even though the size of the gains may pale in comparison to other purely technology-based solutions, such as heat pumps or electric vehicles⁹.

Construction with mass timber could also lower on-site vehicular traffic and reduce the use of fossil-fuel powered heavy equipment. Unlike concrete, mass timber is a prefabricated wood product that can be delivered in a few shipments and then stored on a construction site.

Mass timber practitioners, Veronica Madonna of Athabasca University and founder of architect firm Studio VMA, and Lee Scott of Element5, a mass timber manufacturer with plants in Quebec and Ontario, have found that this storage benefit can reduce on-site vehicular delivery traffic by 80 to 90%, compared to the construction site for a traditional concrete and steel building.

Insight

The story of embodied emissions in steel and concrete

Mass timber, steel, and concrete all have their origins as natural materials extracted from or below the earth’s surface.

The energy and industrial processes required to transform iron ore into steel and limestone and clay into cement, and eventually concrete, are the reasons for their high embodied emissions profile, compared to mass timber. The industrial processes for steel and concrete require using extraordinarily high heat, between 1,400 to 1,600 degrees Celsius, to transform raw materials in blast furnaces or kilns. Energy required to power blast furnaces for steel-making accounts for 87% of emissions generated in the steel making process, according to the International Energy Agency. For cement production, the reverse is true, with 65% of emissions attributable to industrial processes, specifically, the release of greenhouse gases from the heating of limestone and clay in kiln ovens. Mass timber’s significantly lower emissions profile can be attributed to a manufacturing process that largely leaves the original raw materials intact.

Another advantage is that mass timber weighs about 30% less than concrete. The downstream benefit of lower on-site delivery traffic and higher weight differential is lower transportation related emissions. The prefabricated nature of mass timber combined with its relative lightness compared to steel and concrete, means that less heavy machinery such as cranes are needed on a construction site. And when they are used, they have a shorter running time. Both practices reduce the fossil fuel used to operate construction machinery, lowering emission levels.

Canada’s opportunity to capture a slice of the global mass timber market

3x

Growth in Canadian jobs associated with mass timber by 2030

3x

Growth in Canadian GDP from mass timber by 2030

$4.9B

Global mass timber market by 2030

Mass timber accounted for 1% of all building construction materials in North America last year. The global mass timber market reached $1.6 billion in 2022 and is forecast to rise to $1.9 billion this year10. Analysts estimate the market could reach $4.9 billion by 2030 if global demand continues to grow at an annual rate of 14.5%.

Canada’s share of the global mass timber market is $379 million in 2023. And it’s growing, with an additional $649 million expected to be added to the country’s economic output from the production of mass timber, under a scenario where there’s no new manufacturing capacity by 2030. Increased production capacity and efforts by Canada to capture 25% of the global mass timber market could see economic output surpass $1.2 billion by 2030.

If the construction material mix moves away from carbon-intensive concrete and steel and mass timber industry takes off, it could account for a larger share of the estimated $2.6 trillion global building materials market by 2030.

While there are no official employment data for the mass timber sector, we estimate that the sector employs, directly and indirectly, about 4,000 Canadians in 202311. The sector’s job growth is anticipated to triple by 2030, to a high of 12,150 jobs across manufacturing, technology, forestry, design and engineering, if future demand materializes.

Some of these jobs are anticipated to flow to Indigenous peoples as the employment catchment areas of logging sites, sawmills and mass timber manufacturing facilities often encompass their communities.

Canada’s Forestry Resources Could Boost Its Low-Carbon Economy

Two scenarios for Canada’s promising mass timber economy

RBC Climate Action Institute derived analysis using data in Polaris Market Research’s Cross Laminated Timber Market report, Natural Resources Canada Mass Timber data base, and Statistics Canada sectoral GDP data.

Barriers to Canada’s mass timber and climate ambitions

The steady increase in the number of mass timber projects underway in Canada is a testament to the building sector’s green ambitions. Industry interviews suggest a strong desire to increase the use of mass timber, but fundamental challenges are preventing market participants from raising their ambitions at a pace necessary to reach Canada’s climate goals.

Mass Timber’s Big Opportunity To Grab Greater Market Share

Breakdown of building construction materials use in North America

Source: RBC Climate Action Institute, Mantle Developments, 2022

Insurance underwriting has emerged as the most difficult challenge for both building construction and occupancy insurance. Presently, each building requires a bespoke policy, which significantly adds to a project’s final cost,12 and is ultimately passed down to the end buyer. Construction insurance premiums for a mass timber building can be up to 10 times the costs of a similar building constructed with steel and concrete. This layer of cost erodes the competitiveness of buildings featuring mass timber and hampers its widespread use in residential, commercial, and institutional buildings13.

A second structural issue is a mismatch between the location of mass timber production and demand for the material.

Patrick Chouinard, the founder of Element5, noted that B.C.’s early mover status resulted in a manufacturing base that is concentrated in western Canada, but current and emerging demand largely coming from eastern Canada and central and northeastern United States. Patrick Crabbe, Director of Mass Timber at Bird Construction, an early adopter and proponent of mass timber, estimates that 62% of capacity and 22% of demand is concentrated in western Canada, but 78% of demand and 38% of capacity is concentrated in eastern Canada14.

Insight

Sky-high premiums for mass timber buildings

Lack of data to assess the fire risk of mass timber buildings is primarily why building construction and occupancy insurances for mass timber buildings is 6 to 10 times higher than conventional steel and concrete buildings.

Exacerbating this situation is the small and niche market for mass timber. The lack of actuarial data has meant that insurance companies typically insure mass timber buildings to the closest approximate building structure archetype—a wooden frame house constructed with 2×4 lumber. Recognizing that wider adoption of mass timber is necessary to decarbonize the sector, construction services firm Ellis Don has made attempts to bridge the knowledge and information gap that exists in the insurance industry, by bringing industry players together to discuss the insurance challenge and explore potential solutions. These actions have yet to yield the desired outcome, either in Canada or internationally, and continue to present a significant obstacle to scaling the use of mass timber.

For manufacturers, one of the biggest impediments to scaling their operations is the cost of acquiring specialized mass timber machinery and technology, which is produced by only a handful of European based manufacturers. High cost of manufacturing equipment is also preventing new players from entering the mass timber business. The capital required to set up a manufacturing facility, with 50,000 m2 capacity, is estimated to cost $200 million, with the bulk of the costs attributable to machinery.

Canada’s sawmills are dominated by players who produce “dimension lumber”, which are the 2×4/6/8 lumber found at big box home improvement stores and used to build the structural frame of single detached homes. Mass timber products are manufactured using dimension lumber but the moisture content and milling requirements of the lumber are materially different. These differences have created a shortage of appropriate mass timber “feedstock”, leading to a mass timber supply storage.

Craig Applegath, a partner and architect at DIALOG, and early adopter of mass timber, estimates that there’s a two-year waitlist for mass timber in Canada15. Some mass timber manufacturers have addressed this third structural issue through backwards integration, by purchasing sawmills to control the type of wood that is sourced and how it is processed into feedstock.

Bird Construction’s Crabbe applauds the leadership role that various governments have taken to spur interest in and use of mass timber. He notes that the success of their efforts has unintentionally led to the supply and demand imbalance. If not resolved, this market imbalance could slow the pace of mass timber adoption and the building sector’s decarbonization goals.

Recommendations

Canada may be late to the mass timber market, but it has caught up with its European competitors in less than a decade, both in the use and manufacturing of mass timber. It didn’t happen by chance either. Tailored federal and provincial policies and programs that were attuned to evolving market and regulatory forces, combined with visionary entrepreneurs along the building value chain drove Canada’s early successes.

But we are just getting started. Canada has an opportunity to play a leading role in the global mass timber movement if it adopts the following recommendations:

Standardize insurance underwriting to lower costs. Standardizing insurance fire risks for mass timber buildings, during building construction and occupancy, will lower insurance premiums and overall costs for builders and building owners.

Continue funding capital expenditure grants. Federal and provincial grants have played a pivotal role in lowering machinery costs and enabling additional manufacturing capacity, either from existing manufacturers or new entrants. Continuing these programs would ensure supply can keep pace with double digit growth in domestic and international demand.

Conclusion

In the course of conducting research for this report we repeatedly heard from builders, architects, engineers, and manufacturers that Canada can and should be a global leader in mass timber research, manufacturing, and use, while spearheading efforts to decarbonize the building sector. While there are fundamental challenges that must be addressed before these ambitions can be realized, there’s industry consensus that these challenges are not insurmountable. Now is the time for all players in the building sector to work together to act on these challenges and solutions. And for Canada to showcase to the world that we are a nation of innovators in building construction and climate action.

Some architecture historians would argue that mass timber is not a new building material to Canada. Mass (or heavy) timber had been used in Canada since the late 1800s. The oldest surviving heavy timber building in Canada, which was built in 1895 and is still in use today, is located at 312 Adelaide Street West in Toronto.

Hsu, S.L. (2010, June). Life cycle assessment of materials and construction in commercial structures: variability and limitations. Massachusetts Institute of Technology.

RBC Climate Action Institute estimate based on analysis of data from the United Nations Environment Programme: 2022 Global Status Report for Buildings and Construction (section 3.3 Emissions in the Buildings Sector) and the Canadian Climate Institute’s Early Emissions Estimates for 2022.

Interview with Mark Gaglione and Vince Davenport, co-leaders of Ellis Don’s Building and Material Sciences Department. Craig Applegath of Dialog estimates that for some building forms, a building’s floor system can account for 70% of total building materials used.

The floor system emissions reduction savings is based on the assumption that the mass timber building is constructed with a concrete and steel foundation. The 12% and 25% total savings is for a mass timber structure versus an equivalent structure constructed using a composite steel and beam method.

Residential units constructed between 2025 and 2030.

The current mass timber manufacturing capacity in Canada is estimated at 1.1 million cubic meters, based on data from Natural Resources Canada. In comparison, Architectural Record reports that European capacity is 1.6 million cubic meters.

The emissions from using a mass timber floor system would be negative, were biogenic carbon taken into consideration. Ellis Don’s Building Materials and Science Department has estimated biogenic carbon savings of negative 170Kg/CO2e/m2.

RBC Climate Action Institute derived analysis using data in Polaris Market Research’s Cross Laminated Timber Market report, Natural Resources Canada Mass Timber data base, and Statistics Canada sectoral GDP data.

RBC Climate Action Institute derived analysis using data in B.C’s Mass Timber Action Plan, Polaris Market Research’s Cross Laminated Timber Market report, Natural Resources Canada Mass Timber data base, and Statistics Canada sectoral GDP data.

Builders of projects that cost more than $50 million to construct typically need to bring in several insurance carriers to provide coverage for their projects. This practice cannot be avoided because insurance carriers have a lower maximum insurable limit for mass timber than other conventional building materials such concrete, steel, and traditional wood.

Builders with extensive experience in building with mass timber have been able to achieve cost parity with conventional steel and concrete buildings by optimizing design, construction, and scheduling practices.

Data presented by Patrick Crabbe at the Brookfield Sustainability Institute’s Toronto Mass Timber Conference, September 2023. Data obtained from Forest Economic Advisor Mass Timber North America report, July 2022.

Estimate made in October 2022 in a Medium article titled: 10 Reasons to Build with Mass Timber.

Last fall RBC partnered with BCG’s Centre for Canada’s Future and Arrell Food Institute at the University of Guelph. We set out to explore what we believe is Canada’s moonshot: to produce 26% more food by 2050 (enough to maintain our contribution to the global population as it grows) with fewer emissions. The result was The Next Green Revolution: How Canada can produce more food and fewer emissions.

Throughout the past year, here’s what we learned:

Canada is uniquely placed to lead: Our assets are unparalleled, but we need to do more to maximize them. Other nations are allocating substantial funding to promote climate-smart agriculture. Canada can proportionally match those investments while establishing new market mechanisms to help finance agriculture’s sustainable transition.

Nothing will happen without accurate measurement technology: Tools to monitor emissions accurately (especially carbon sequestration in soil) are essential to building markets and helping producers take advantage of them.

Cross-sector collaboration is key: A successful transition to Net Zero demands a new approach. It requires public-private actors across the fragmented agriculture supply chain to work together, as one sector, toward a single vision.

Private sector R&D is insufficient: Canada has invented some of the most important agricultural technologies globally. But private sector funding for innovation is at an all-time low. To remain leaders in this space, we’ll need private actors to invest.

Skills gaps are limiting growth: The sector requires more workers to drive the Net Zero transition. From on-farm managers to data analysts, qualified workers and advisors are desperately needed on Canadian farms, but post-secondary funding is insufficient.

Early adopters should be rewarded: A significant number of producers across Canada have engaged in climate-smart agricultural practices for years—if not decades. These pioneers could be left out as programs develop to financially incentivize farm operators making their first transitions to better soil health methods. To continue growing current carbon stock levels, early adopters must receive a financial benefit for their continued contributions.

The world needs Canada more than ever: With global supply chains under stress from the Ukraine-Russia War and extreme climate events, many countries are facing food shortages or unstable supply lines. As a politically stable country, and a reliable supplier of safe, high-quality food, Canada has an opportunity to become the world’s sustainable breadbasket.

Canada’s investment in climate-smart agriculture lags global peers

Source: BCG analysis, RBC analysis, USDA, and OECD

Brazil and Indonesia were not included due to climate-related funding directed to financing programs

The world’s top food producers are on the move. Making sustainable agriculture a strategic priority, Canada’s peers are laying the foundations for formidable climate-smart food supply chains backed by sizeable funding and bold policy measures.

Amid these dramatic investment and policy shifts, a pivotal moment is emerging for Canadian agriculture. The sector risks falling behind if Canadian governments don’t match their competitors in supporting producers with the funding and policy tools to grow more food with fewer emissions.

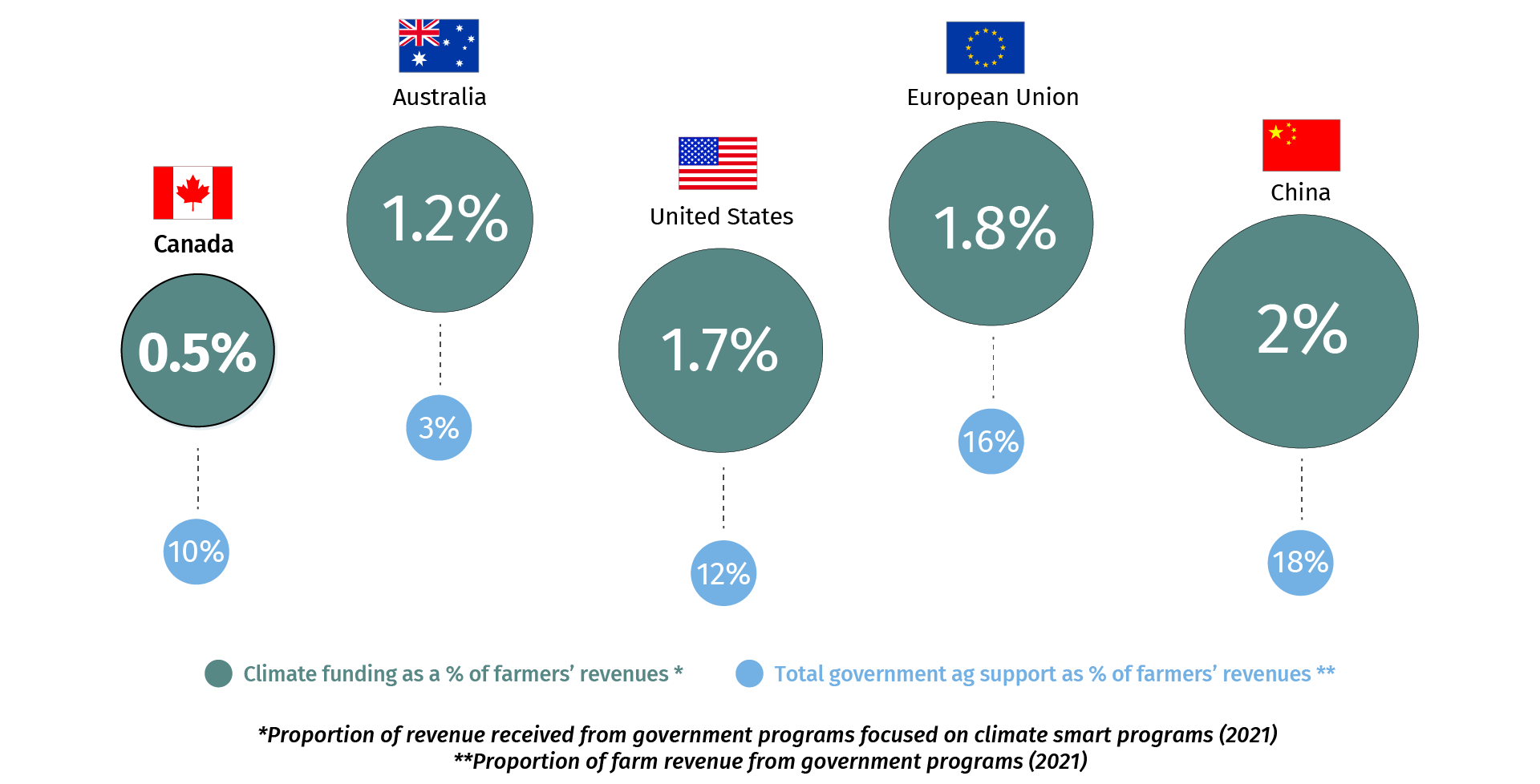

Canada is already falling behind. The agriculture sectors in the U.S., EU, Australia and China get roughly three times the climate funding that Canada provides to its industry. Yet the expectations placed on our farmers are growing: to produce more (in increasingly adverse weather conditions), to cut emissions and to help boost global food security.

We began to explore the opportunities around climate-smart agriculture last year, in the midst of twin global crises over food shortages and climate shocks. Since then, our research teams have spoken with more than 500 farmers and food producers, to gain a better understanding of what practical policies could make a difference now.

The right policy measures will help strengthen our economy, soften geopolitical threats and accelerate emissions reductions.

Ottawa and the provinces will need to transform their approach to agriculture policy to protect a sector that accounts for 7% of national GDP—with huge potential for further growth.

This report lays out nine polices across five areas—soil, methane, fertilizers, talent & technology, and consumers—that can slingshot Canada’s agriculture sector to the forefront of the next green revolution and compete globally.

The nine-point plan could serve as a powerful response to IRA’s ambition, and lays the ground for a prosperous, expanded, and sustainable food powerhouse.

Currently, Canada’s ag policy and funding falls well short of the US$19.5 billion in incentives and tax credits embedded in the Inflation Reduction Act to support ag-tech, conservation and other measures. Even before Washington rolled out its signature climate program, U.S. climate funding as a percentage of total farmers’ revenues stood at 1.7%—more than three times the level in Canada. The proposed US$1.5 trillion Farm Bill could further extend America’s advantage.

China, meanwhile, is revitalizing farmland through an annual US$7 billion investment, while the European Union is dedicating US$224 billion to “climate-relevant initiatives” through 2027.

The farmers we spoke to suggest agriculture is already ahead of other economic sectors in fighting climate change, and in deploying technologies, innovations and methods that have reined in emissions. But soaring global and national emissions mean there are new expectations—from domestic and global markets—on Canada’s major sectors to raise the bar.

Our proposed policies will reduce agriculture sectors’ emissions, which currently account for more than 10% of the nation’s total greenhouse gas emissions.

A climate-era agriculture business model involves farmers to provide demonstrable proof of emissions reduction to meet challenging government and investors targets and growing consumer expectations.

The good news: Canada is already a vital contributor to global food security and has a head start in climate-smart farming.

Canada is already a top food exporter, with a food system ranking among the highest in sustainability, according to the Food Sustainability Index. Over 65% of Canada’s farmers have adopted at least one practice to improve their farm’s resiliency to adverse soil, water or biodiversity challenges.I

Now is the time for Canadian governments to build on our farmers’ successes. The nine-point plan could serve as a powerful response to IRA’s ambition, and lays the ground for a prosperous, expanded, and sustainable food powerhouse.

Soil As An Asset Class

A corn farmer near the township of Elmira, Ontario, recently shared his excitement with us about the prospect of boosting his bottom line by integrating carbon credits into his farming practices.

He’s not alone. Thousands of Canadian farmers are also eyeing the carbon credit market, which promises fresh sources of revenue and recognizes their efforts to remove carbon from the atmosphere.

However, stories and experiences of unsuccessful pilots that didn’t ultimately pay out, unclear guidelines on access, and limited data and knowledge is dampening enthusiasm. In addition, producers that implemented practices to sequester carbon at a higher rate years ago feel left behind and rue their timing.

Canadian governments could pursue three policy measures to create thriving carbon markets.

1. Build Standards To Support Carbon Markets

Opportunity

A $4B carbon market by 2050

Challenge

No clear standards

Serving as a powerful carbon sink, active farmland in Canada can sequester between 35MT to 38MT of carbon by 2050, around 40% to 45% of the oilsands’ current annual emissions.

Currently in a nascent stage, Canadian voluntary carbon markets could emerge as a $4 billion behemoth by 2050, our research shows. An active market could mean tens of thousands of dollars in fresh revenues streams for some operators—and over a $1 million for larger operations.

But the building blocks of a viable carbon inset or offset carbon market in Canada will rest on a solid system for measuring and reporting soil carbon and emissions.

Agriculture and AgriFood Canada (AAFC) and Environment and Climate Change Canada (ECCC) have done extensive work in this space, but more can be done collaboratively.

Here’s how we can build a vibrant Canadian carbon market:

Based on the private sector’s work, the federal government can publish methodologies on the most credible approaches to creating offsets and insets (see box).

To receive any carbon credit payment, the impact must be measured scientifically. Working with farmers/ranchers and agribusiness and through regional pilots across the country, AAFC and ECCC could introduce publishing standards for a preliminary measurement, reporting, and verification (MRV) framework for different climate-smart practices. This would work in tandem with the soil database detailed in the next section. It will be tricky, though. Finding a consistent and cost effective MRV methodology to measure the impact of climate-smart agricultural practices (including cover cropping and no-tillage) on soil carbon sequestration and emissions remains challenging.

An MRV framework would guide producers on earning credits in an affordable way, and enable buyers to confidently purchase those credits or incorporate them in an inset program.

Governments should explore viable ways to ensure market prices are stable and farmers and investors can secure a consistent and substantial return.

The U.S.’s 8-year, US$300-million investment in MRVs could serve as a template for Canada. The investment will enable improved data collection mechanisms and build algorithmic models to establish current and future emission baselines. It will also determine the protocols needed for soil testing, identify scalable and affordable remote sensing and soil sampling technologies, and establish a nationwide network of research to improve on-farm practices. Canada will need to match this funding proportionally to ensure producers can compete.

Insets

Organizations directly avoid or reduce emissions within their own supply chains. The process helps companies avoid or reduce Scope 3 emissions in their supply chains and better prepares for them for future regulations that may be more stringent.

Offsets

Companies or individuals purchase tradeable credits generated by renewable energy or other emissions-reducing projects. This credit negates or offsets the same amount of carbon emissions created by their operations.

2. Create A Climate-Smart Database To Help Farmers

Opportunity

A data-smart ag sector to manage risks and boost productivity

Challenge

Lack of accessible knowledge

A deep and extensive data pool is critical for measuring status of climate practices and future areas of focus. But a lack of government funding for climate-smart data programs has hampered efforts to manage risks and boost productivity.

The federal government, in cooperation with provinces, can address these challenges and accelerate the adoption of efficient methods by developing the framework for a national soil database:

Building on years of work by the AAFC and provinces, a national soil database can collect data through a common system. This is critical to understanding the current health of various soil classes across Canada, particularly since some soil maps have not been updated since the 1950s. It’s also key to understanding soil’s impact on nitrous oxide emissions (which is especially damaging to crops and human health), carbon sequestration and organic carbon stock patterns.

Established and funded by the AAFC, the database could serve as a portal delivering real-time and downloadable economic intel to producers, experts, and decision makers.

The slew of data, from provinces, soil laboratories, ag-machinery providers and remote-sensing operators, will create real-time regional and national baseline emissions. It will also help in charting regional crop modelling, establishing ways to improve nutrient management, encourage biodiversity and water conservation practices.

Armed with insightful data, farmers could reduce the risk of adopting climate-smart agricultural practices by understanding potential economic impacts of adopting new practices. The database could also serve as an invaluable tool for companies and research firms looking to develop export-ready agricultural technologies.

3. Develop A Fair System That Ensures Market Equity

Opportunity

A system that incentivizes early-adoption of sustainable technology

Challenge

Little recognition for first movers

The first two pieces of our soil policy package are aimed at incentivizing future behaviour. This final segment recognizes past actions.

Canadian farmers have been ahead of the curve, with many implementing climate-smart practices that pre-dates the Paris Accord, sometimes by decades. But these early adopters’ worry their carbon stock may not have been documented consistently over the years. After all, to be rewarded in a carbon market, producers must demonstrate an increase in carbon absorption over time.

Failing to reward these early adopters could bring unintended consequences. It could demotivate farmers or compel them to once again till their land (thereby releasing carbon) to set a lower baseline for carbon in their soil—leading to higher payouts in the future.Early adopters who can demonstrate they have increased carbon stock could be compensated in the following ways:

An expanded capital gains exemption could be created for qualifying farmland. Currently, there is an exemption of $1 million of property value that is not taxed on qualified property during intergenerational transfers. The new policy would entitle producers to the total value of organic carbon in their soil based on latest market prices (in addition to current exemptions). It would be associated with the value of the farmland at the time of transfer and exclude the exemption received. Through back-casting, a modelling process where past changes in soil-bound carbon are estimated, we can chart the evolution of soil organic carbon stock over several years. This method can be used to determine baseline estimates to compensate farm operators.

Producers could receive a pool of tax credits, based on scientifically proven carbon stock on their farms, that can be used toward paying taxes. An allotment of credits can be spread over 10 years with producers choosing the year they want to pay business taxes.

Parts of the Scientific Research and Experimental Development (SR&ED) can be simulated to encourage environmentally beneficial on-farm investments. A new program would issue investment tax credits to farm operators that invest in projects promoting ecosystem services. If an investment matches an activity from a list of appropriate on-farm investments, producers can submit a claim to receive a tax credit.

Methane As A

Growth Opportunity

A dairy farmer just south of Ottawa told us he was eyeing a biodigester, but worried about its substantial price tag and economic viability. The biodigester will help break down organic materials (such as manure) at his farm to produce biogas, mostly methane. But he, and other farmers we spoke to, believe Canadian policies are not attractive, even under the supply management program. This made the biodigester hard to justify, despite its role in cutting costs and managing emissions.

It’s a different story south of the border. Under IRA, American farmers are well positioned to benefit from 30% tax credits from the production of biogas through at least 2025. In addition, the U.S. Department of Agriculture’s Rural Energy for America Programs have provided US$2 billion in loans and grants to increase energy efficiency and renewable energy like biogas.

Canada will need to match the U.S.’s investment in biogas to tap its improved sustainability benefits, waste-to-energy conversion and lower energy costs.

4. Promote Ways To Make Methane Cuts Profitable

Opportunity

Create a robust value chain for biogas

Challenge

Investments are not profitable

While Canada needs to produce more food, it must do so with fewer emissions. Crops and livestock production currently generates more than 10% of Canada’s greenhouse gas emissions, with methane among the most potent sources.

As a signatory to the Global Methane Pledge, the federal government acknowledged that agriculture is responsible for 31% of the country’s total methane emissions. Enteric fermentation, the digestive process of ruminant animals, accounts for 86% of that total with manure responsible for the rest. While manure contributes to methane emissions, it can also emerge as a source for renewable natural gas, or biogas.

The technology and tools to tackle methane are ready, but successfully deploying them will require both financing and a broad system approach. We recommend the following approaches:

The federal government could co-ordinate with provinces to create a nationwide blend mandate to incentivize utilities to purchase renewable natural gas (RNG) from digesters. Provinces such as Quebec and British Columbia mandate natural gas providers have a blend of over 10% minimum renewable content within their supply by 2030, motivating utilities to purchase RNG. It has encouraged farm operators to install biogas-producing digesters that can then be converted into RNG at an upgrader. Through a nationwide mandate, provinces would be expected to establish a minimum blend requirement.

Support more proposals for the construction of digesters through the Strategic Innovation Fund (SIF). Though SIF currently accepts agrifood proposals, this is not a core feature of the program.

Credits can be granted to producers through the Clean Fuel Regulations (CFR) for biofuels used in the transportation market. To ensure the program is effective, ECCC could review the program after a year to ensure all participants are receiving appropriate financial compensation and that obstacles to installing biodigesters are reviewed and fixed in a timely manner.

Installation cost of digesters and pipes could be included in the Cleantech Investment Tax Credit. IRA provides a tax credit of up to 50% of project costs to businesses that install digesters. A similar tax credit will be needed for Canada to compete and develop a market that will use the RNG produced from this technology. Accelerating RNG production investment will lead to a greater supply of ultra-clean fuel for the transportation market.

Create agile regulations and government policies for methane-reducing feed additives to reduce methane emissions. These feed additives currently can’t enter the Canadian market due to stringent regulations. A permanent and independent panel of experts could advise regulators on the abatement potential and productivity benefits of low-emission livestock feed technologies. This panel could be empowered to work with regulators at Health Canada and the Canadian Food Inspection Agency (CFIA) to review regulations, collect data, and provide technical guidance on policies related to the new additives. As many feed additives are considered veterinary drugs, the panel will review and update regulations to ensure innovation and competitiveness are key criteria. The panel could also collaborate with key trading partners to develop standards that recognize producers who use methane reducing feed additives.

Supply Chains As

Strategic Drivers

A potato producer in Lethbridge, Alberta, acknowledged the efficiencies of the 4R Nutrient Stewardship program—the right fertilizer source, at the right rate and time, and in the right place.

But he believes the government can do more in the fertilizer space to ensure the security of inputs vital for safeguarding the national food supply-chain.

Worrisomely, Canada does not have enough agricultural inputs to support the entire industry if it’s cut off from external suppliers, especially major exporters such as Russia.

Promoting a domestic industry of fertilizers and other agricultural inputs would reduce costs and ensure a steady supply of innovative solutions to farmers across Canada.

A domestic push on sourcing agriculture inputs will also create jobs in rural regions, as the raw resources for many innovative fertilizers, like biostimulants, originate in rural areas and are processed close to their source.

Beyond focusing on revenues, farmers need to ensure the supply of fertilizers and agriculture solutions, is affordable and accessible.

Fertilizers are made of three vital components: nitrogen, phosphorus, and potassium. They ensure plants have the right access to nutrients to grow and increase yields. While Canada is the world’s largest producer of potash (a common form of potassium) and supplies 31% of global demand for this commodity, the country is reliant on other nations for nitrogen and phosphorus.

This has become a major pain point in light of the Russian invasion of Ukraine and Canada’s dependence on Russian nitrogen fertilizer. Before 2022, farms in central and eastern Canada used over 660,000 tonnes of nitrogen fertilizer imported from Russia annually (representing over 85% of total nitrogen fertilizer used in the region). With the government issuing steep tariffs on fertilizers to punish the Russian economy, Canadian producers have been left paying the bill.

Biological products, such as biocontrols, biostimulants and biofertility (see box), can emerge as critical add-ons or substitutes to traditional agricultural solutions. Biostimulants can be blended with traditional fertilizers to promote healthier soils and increase efficiencies and currently represent a US$12 billion global market.[i] Canada is in a unique position to lead in this space given the raw resources required to create these solutions are found in rural regions. Firms making these products are often headquartered in rural communities and can ensure that local demand for organic nitrogen fertilizers is met while creating high-paying jobs.

The following steps can help build a resilient, home-grown agriculture value chain:

CFIA, which is tasked with registering biological products, should streamline approval processes. CFIA should also seek further funding for additional staff, as it currently takes the agency more than 380 days to approve new registrations–-not including potential delays.

The federal government, in conjunction with provinces, should bolster supply chains by improving transportation networks such as roads, railways and ports. Governments should also continue their support and expansion of carbon capture, utilization, and storage projects and research and development initiatives for domestic nitrogen fertilizer production.

Provide funding from the federal government to biological companies to improve domestic and foreign market development. Biological products can help reduce soil erosion, which is costing Canadian and American farmers over $3 billion annually, according to research. Research grants should be awarded for on-field trials for marketing purposes. While many fertilizer programs will continue to use chemical products, farmers can blend biological options to improve soil health.

The seaweed extract opportunity, often used as a biostimulant, can generate 30,000 jobs in rural British Columbia alone, the industry estimates.

Establish biological products as a lucrative made-in-Canada product. Several Canadian companies are currently providing innovative biological solutions, and many markets, including Europe and South America, are adopting them. In 2021, half of Canadian fertilizer retailers had a positive view of biostimulants while over 80% sold a biostimulant product. Common biostimulants include enzymes that promote nitrogen fixing, seaweed extracts, or beneficial bacteria and fungi.

Types of biological solutions

Biocontrol:

Assists plants in biotic stress and prevents further damage from pests, pathogens, and other organisms.

Biostimulant:

Supplies plants with support during abiotic stress to improve overall crop quality by increasing nutrient use efficiency.

Biofertility:

Promotes crop growth through the application of living organisms to soil, seeds, or plant surfaces to colonize internal plant tissue and encourage growth.

Technology & Talent As

Competitive Advantages

On the outskirts of Saskatoon, Saskatchewan, a canola producer told us he won’t bother posting a “Help Wanted” sign this year after recent efforts to find talent had failed. Like other farmers, the Saskatoon producer believes sourcing talent is about more than getting labourers to participate during harvest. Farms need on-site specialists and a network of advisors to identify key requirements. These specialists need to communicate quickly with data collected from machines to boost efficiencies.

Farmers are also concerned about cost of critical technology and new innovations that could eliminate time-consuming tasks remain cost prohibitive. On-farm specialists and technology that can help manage droughts and weather episodes are going to be central to their success.

Yet, investment in the space has been declining over the past few years. To guarantee operators’ access to technology and talent, the federal and provincial governments could increase their support of research and development to decrease the cost of new innovations, advisory networks, and education.

The following policy package could help hone talent and drive innovation:

6. Nurture An Innovation-Driven Ag Sector

Opportunity

Find the next wave of Canada’s ag-tech giants

Challenge

Minimal investment in ag-tech

The launch of a thriving carbon market and growth of big data analytics will sow the seeds for the next crop of tech-savvy Canadian agriculture companies.

However, ag-tech investment in Canada is lagging global peers, stymying innovation. In 2021, over US$6.9 billion in venture capital funding went to American ag-tech companies. By comparison, only US$270 million went to Canadian ag-tech firms. More public and private research and development (R&D) funding is needed to scale Canadian ag-tech companies.

Here’s how Canada can fine-tune its funding mechanisms:

The private sector and Innovation, Science and Economic Development Canada, could invest in the creation of a network, similar to the Clean Resource Innovation Network (CRIN) for oil and gas projects that promote research and development. The public-private partnership would include farm operators, smart farms, research institutions, investors, and companies (small, medium, and large) throughout the agriculture supply chain.

Hold competitions (similar to CRIN) to develop and commercialize sustainable technologies. For instance, a call for proposals focused on reducing harmful nitrous oxide emissions could spur innovation in the genetics of nitrogen-fixing crops, enhanced efficiency fertilizers, or other technologies that allows plants to take nitrogen directly from the atmosphere, reducing the need for energy-intensive fertilizers.

Allow innovative companies to showcase their solutions and finance their innovations. Participating farm operators and smart farms in the network can evaluate innovations directly through on-field trials at minimal cost. Researchers can also initiate studies that companies can use for marketing purposes, gaining access to investors at different levels. Corporations involved in the network can have priority access to investments and can pair their R&D teams with the ag-tech firms participating in the challenges.

Increased private sector R&D in agriculture will ensure that current obstacles to on-farm labour are eliminated in the future. Technologies can automate processes, enable farm operators to focus on management, decrease inputs and grow yields.

7. Revive Canada’s Knowledge-Sharing Network

Opportunity

Build a Canadian ag knowledge portal

Challenge

Insufficient infrastructure

Agriculture extensions—a network of agriculture experts dotted across provinces— and Canadian universities have historically supported farmers with guidance. Agronomists and experts in these networks often offered advice to producers on the most suitable strategies and technologies. But over the years most universities have stepped back, while provincial extension services diminished due to funding cuts. The U.S. witnessed the reverse, with many land-grant universities providing a series of programming initiatives to help producers.

Here’s how Canada can revive these networks:

Farmers can acquire information and knowledge from privately funded experts, but greater provincial involvement is needed as the urgency of climate challenges build. Indeed, on-farm demonstrations are the most effective tools for increasing adoption of new management practices and innovation. Farmers have also identified a lack of access to experts, on-farm demonstrations and knowledge as the main barriers to further adoption.

A new approach to extension service programs should consider a collaborative approach involving public, private, and institutional actors. A new blended approach would encourage provinces to partner with agricultural colleges and post-secondary institutions through increased federal and provincial investment in research facilities on campuses. It would also promote in-house consultancies in provincial agricultural departments (as in Nova Scotia) that can drive further recruitment.

The private sector has a powerful role to play, too, with in-house agronomists offering farmers real-time recommendations to boost productivity.

8. Boost Investment In Post-Secondary Education

Opportunity

Grow and deepen the ag sector’s talent pool

Challenge

Difficulty in attracting diverse set of skills

Canada’s agricultural sector will soon enter one of its biggest labour and leadership shifts. Current immigration policies that fast-track skilled farmers and on-farm labourers should continue to expand to meet this challenge.

Here’s how we can ensure future generations of producers and a network of advisors and consultants are on hand to provide expertise:

Agricultural colleges and universities should continue creating programs that welcome students from different educational backgrounds and micro-credential programs. Creating programs that blend the expertise of different faculties will help increase students’ exposure to agriculture.

A carbon management program could invite students from different faculties to understand how greenhouse gas emissions are tracked, ways to create corporate objectives to decrease emissions, and effective methods to monitor progress.