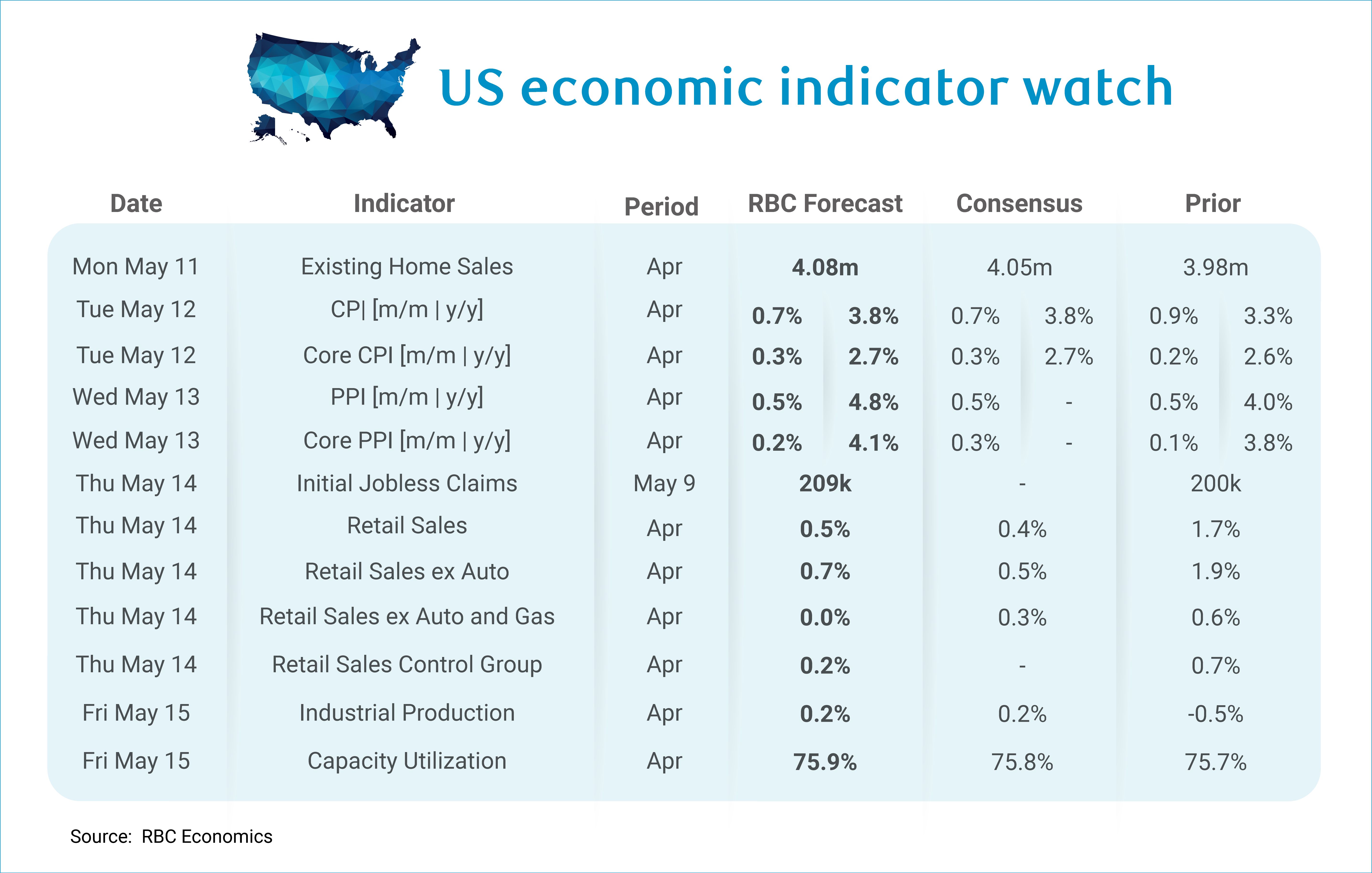

The focus next week will be on inflation. The CPI and PPI data will provide a fresh read on how dual inflation shocks – energy and tariffs – are impacting prices. We expect to see another spike in April headline inflation (+0.7% m/m) due to gasoline prices remaining elevated. But even after stripping out food and energy, we expect core inflation will accelerate to +0.3% m/m, pushing up the y/y pace to 2.7%.

Part of the acceleration will likely come from housing inflation. Challenges associated with missing data during the October government shutdown led to methodology changes that could translate to a hotter-than-usual housing print in the April. Since housing accounts for roughly 40% of the core CPI basket, there is more upside than downside risk to this month’s print.

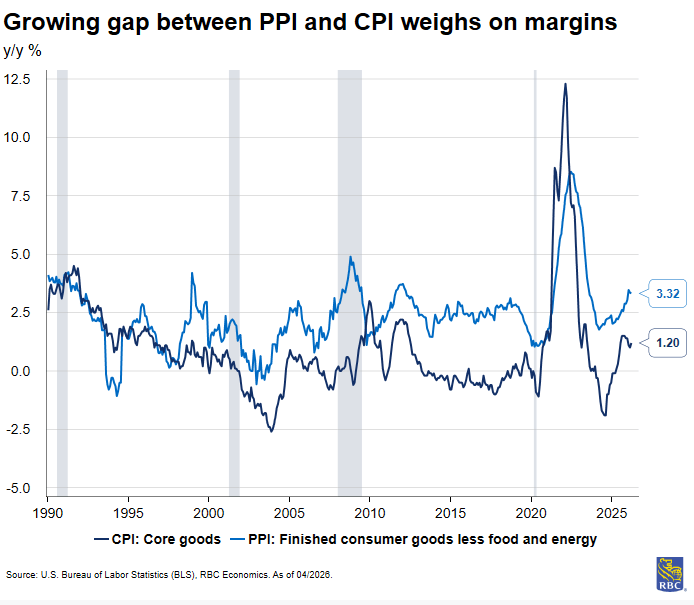

Headline PPI is expected to rise +0.5% m/m primarily due to higher energy prices. Our core PPI forecast expects a more modest rise of +0.2% m/m. We anticipate that these higher prices will be passed along to consumers in the coming months. The growing gap between PPI finished core consumer goods and CPI core goods illustrates the concern – the gap between y/y pace of growth widened to 2.1ppts in March 2026 from 1.0ppts in September 2025. The growing gap suggests that wholesaler acquisition costs are rising faster than retail firms’ ability to raise prices for consumers – and that is a concern for corporate profits.

Our retail sales forecast calls for a strong headline print (+0.5% m/m), driven by higher gas prices, though weaker autos will partly offset some growth. Since retail sales are nominal, we are watching real retail sales closely for a better gauge of consumer health. Real retail sales growth has trended lower on a year-over-year basis since 2025, but we do not expect it will turn negative in the face of higher gas prices. For now, households appear to be saving less at the expense of higher gasoline prices – the personal savings rate is down 1.5ppts from year-ago levels. Still, tax refunds should continue to support spending, though these are disproportionately benefiting high-income households. This dynamic also means we expect to see consumer sentiment continue to grind lower, as middle- and lower-income households bear the brunt of inflation’s impact on their household budgets.

Outside of tier-one data, here’s what else we’re watching next week:

-

We expect to see slightly stronger existing home sales in the month of April at 4.08m. Pending home sales data suggests activity picked up in April relative to March. Pending home sales in March improved but remains below year-ago levels as housing sector activity remains continuously dormant with long-end rates stagnant for the foreseeable future.

-

Initial jobless claims likely ticked up – we are forecasting +209k for the week ending May 9th. Jobless claims have held steady this spring despite geopolitical uncertainty. We expect that this will continue to be the status quo this year as firms avoid layoffs in a tight labor market.

-

We expect industrial production rose in April (+0.2%) as April’s ISM manufacturing production index remained in expansion territory. April’s ISM manufacturing report noted increased production in four of the six largest manufacturing industries: transportation equipment, machinery, computer and electronic products, and chemical products.

About the Authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. Carrie is responsible for projecting key US indicators including GDP, employment, consumer spending and inflation for the US. She also contributes to commentary surrounding the US economic backdrop which she delivers to clients through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.