Twice annually we consolidate federal and provincial fiscal balances to understand how it may affect the economy. As we await new federal numbers in the April 28 spring update for a complete analysis, here we dive into changing provincial deficit projections from 2026 budgets.

-

Projected provincial balances represent a combined deficit of 1.1% of gross domestic product (GDP) in 2026-27, stable relative to 2025-26, and 0.6% of GDP higher than in fall projections. A higher combined deficit is also expected for 2027-28 versus the fall.

-

Adding back in various excluded contingencies would result in a notably higher collective deficit.

-

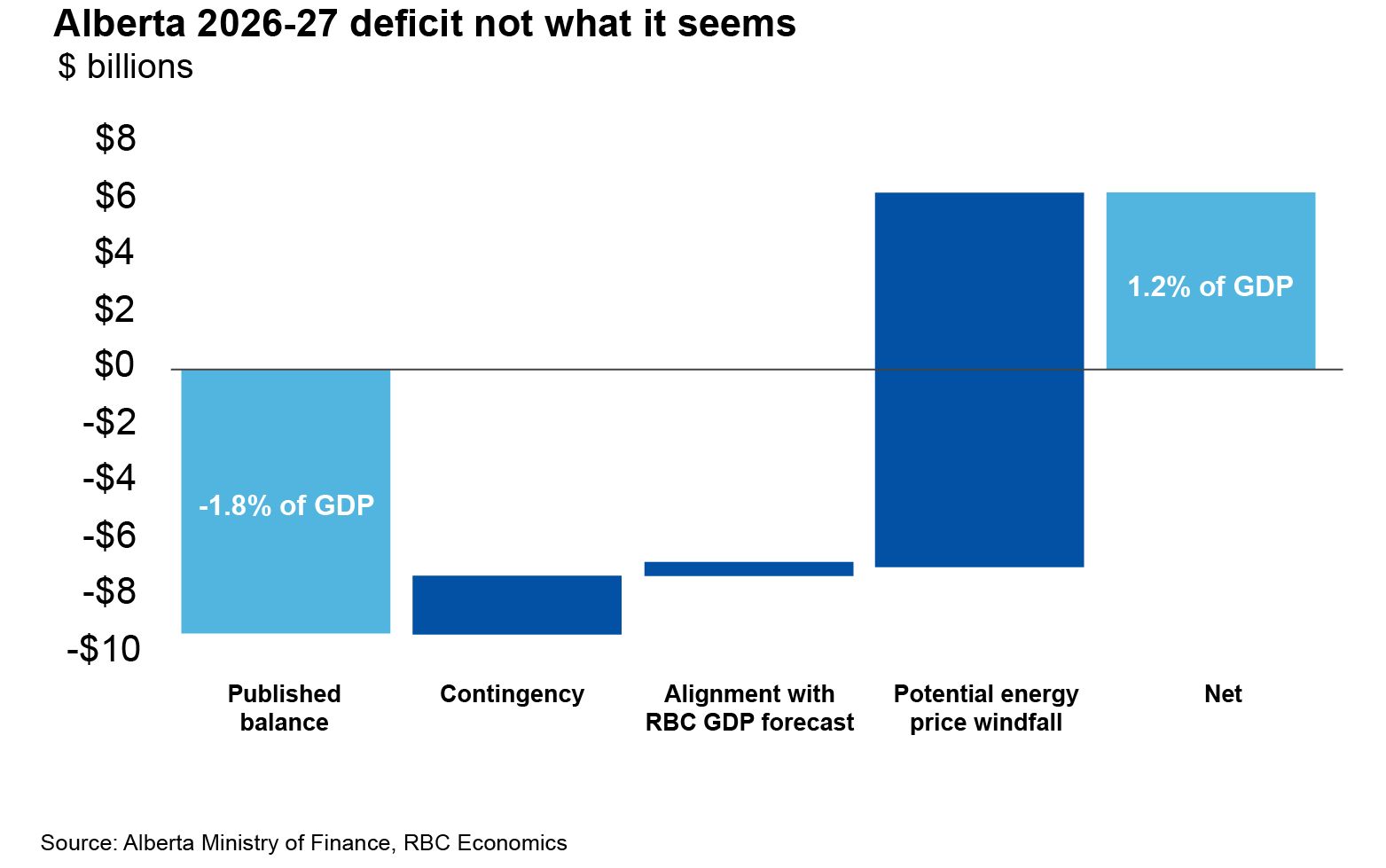

High oil prices from the Middle East conflict could swing Alberta’s reported 1.8% of GDP deficit in 2026-27 to a 1.2% surplus.

-

All provinces reported higher deficits for 2026-27, except for Quebec, with a similar story for 2027-28. Higher budgeted healthcare spending was a core contributor. Meanwhile, New Brunswick, Prince Edward Island, and Nova Scotia numbers reveal a marked fiscal deterioration.

The federal update will reveal whether the lower-than-expected 2025-26 deficit in monthly tracking translates into a lower projection for 2025-26, and how that carries across the forecast.

Collective provincial deficit jumped this budget round

With nine out of 10 provinces reporting, the combined provincial deficit for 2025-26—the fiscal year just ended—is expected to be 1.1% of GDP. It’s the same as fall estimates, and similar to 2025 budgets (rounded up here and here).

However, the collective fiscal balance eroded in subsequent years, with the deficit 0.6% of GDP higher in 2026-27 and 2027-28 than in fall projections. As a result, the collective provincial deficit (contingencies removed) is expected to be unchanged year-over-year in 2026-27 at 1.1% of GDP before falling to 0.6% in 2027-2028, and 0.3% in 2028-2029—the final forecast year available for all provinces.

These numbers exclude reserves, contingencies and other unallocated deductions (“contingencies”) from the fiscal balance since they can distort comparability.

There were big increases in budgeted contingencies—published deficit numbers inclusive of these amounts increased by almost 1% of GDP in 2026-27 and 2027-28. If realized, provincial deficits as a share of the economy would trend upwards this year versus the stable profile expected now.

About a quarter represent Quebec’s contributions to its Generations Fund, which are consolidated with provincial finances per accounting standards. Other amounts may correspond with suspected pressures known inside government, but it’s been a mixed bag of tapping into them in recent years. They are omitted for analysis, especially since they vary significantly by province and year.

High oil prices could almost cancel 2026-27 upward revision to collective deficit

Budget assumptions were largely set before the Middle East conflict, but high oil prices could improve Alberta’s fiscal balance enough to leave the collective 2026-27 deficit much lower—closer to fall projections at only 0.6% of GDP versus 1.1% noted above (no contingencies).

This is an example of the large distributional effects of oil price shocks on the Canadian economy even as the current shock is likely to be relatively neutral on growth in aggregate, at this time.

Alberta reported a large, projected erosion in its 2026-27 balance in its budget 2026, partly on the assumption that West Texas Intermediate oil would average only US$61 per barrel. Our current forecast1 has it averaging almost US$80 in 2026-27 before returning close to prior expectations in 2027-28. Using Alberta’s published fiscal sensitivities, this could yield an additional $13 billion in-year, playing the starring role in swinging its budgeted 2026-27 deficit to a potential 1.2% surplus. Saskatchewan and Newfoundland could also see (much) smaller improvements.

Harmonizing provincial balances to a common (RBC Economics) nominal GDP forecast results in other small deviations—Alberta deficit lower and British Columbia higher—that net out to small changes overall2.

Healthcare spending main driver of higher deficits

Setting aside the revised Alberta narrative, all reporting provinces revised 2026-27 deficits higher (no contingencies), except for Quebec, with a similar story for 2027-28.

Drivers are nuanced for individual provinces, but in aggregate, higher healthcare spending was the main reason for eroded fiscal balances. It contributed more than 100% of the combined deficit increase for the big four provinces, led by Alberta and Ontario.

Like for some education spending, high levels are probably partly a holdover from exceptionally high in-migration in recent years, although we have highlighted before that provinces are still in the early days of rising baby boomer healthcare costs. As partial offsets, higher revenues helped only a little with lower expenses in other spending categories more important.

Atlantic provinces see marked fiscal deterioration

New Brunswick, Prince Edward Island, and Nova Scotia saw the most significant deficit jumps as a share of the economy relative to fall projections. Higher healthcare spending played a key role in these revisions. Importantly, all three expect to maintain deficits of more than 1% of GDP by the end of the forecast period in 2028-29.

As a result, 2026 budgets bake in very significant increases in the expected net debt-to-GDP ratio relative to 2024-25. These provinces already had higher-than-average debt burdens.

Full picture to come with feds and Newfoundland

In the fall, the combined federal and provincial fiscal balance looked like it would total a deficit of 3.5% of GDP (no contingencies) in 2025-26—the fiscal year just ended—before falling but remaining at elevated levels. Large federal deficits from budget 2025 represented 70%-plus of the total balance across forecast years.

Provincial budgets now look to deliver higher-than-previously-expected deficits in outer years, but there’s a chance of more consequential changes on the federal side.

Based on results to date for 2025-26 (10 out of 12 months), the federal deficit is tracking way below budget, about 1% of GDP versus 2.4% planned. A surprisingly resilient Canadian economy has been boosting revenues, especially corporate taxes, but with outlooks not significantly changed, lower-than-planned spending is also at play.

The spring update is expected to factor in a higher rate of spending for the final months of the year, and a significant year-end add to the provision for contingent liabilities to come closer to budget numbers. Our estimate for the full-year 2025-26 deficit is under 2% of GDP.

The key question is how 2025-26 developments translate into deficit projections for the current year onwards. A portion of higher revenues and slower pace of spending should carry across the forecast, but slower implementation of prior measures and other spending pressures are likely to lead to a large share of funds being reprofiled or reallocated.

About the author:

Cynthia Leach is Assistant Chief Economist at RBC covering the team’s medium-term economic analysis, including primary research areas of federal and provincial fiscal analysis, structural government policy, and demographics.

- Current economic forecast as of April 13, 2026. WTI assumptions taken mostly from the forward curve. ↩︎

- Aligned with RBC Economics’ April 2026 nominal GDP forecast for those provinces that report fiscal sensitivities – Ontario, Quebec, Alberta, British Columbia, and Manitoba (collectively 90% of GDP). ↩︎

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.