More than 500 business, government, policy, and community leaders, along with policy thinkers and academics, came together for the annual U.S.-Canada Summit, hosted by RBC and the Eurasia Group in Toronto on June 11, to discuss where the world’s most prosperous relationship is at—and where it might go.

Here’s some of what emerged:

1. Spring thaw, or false spring? Whispers of warming

Tone matters—and this year’s summit carried none of last year’s hostility. Both countries’ ambassadors spoke of hope, although with different expectations, and both sides spoke of tariffs as a new normal, again with different expectations. The fundamentals are too large to ignore: $1.3 trillion in annual two-way trade, 120-million border crossings per year, and a relationship woven through shared IP, talent, capital, and innovation. Trump’s former trade czar Robert Lighthizer acknowledged Canada is not the main problem—America’s real frustration is with China, Germany, and Japan. But Canada isn’t exempt, and he was blunt: tariffs aren’t going anywhere for a generation.

That’s not to suggest there’s rapprochement. Business leaders agreed the damage to Canada-U.S. relations is not irreparable—but there is damage, and it will take time to heal. Trust comes back slowly. Uncertainty recedes slowly, too. But the economic logic of closer Canada-U.S. ties remains strong. One Canadian portfolio manager said that no matter how they run their risk models, they end up with a 50-60% allocation to the U.S. The two governments now have the summer, and likely part of the fall, to find a way forward on trade. They’ll also have to recognize how much their economies are changing at the same time. This isn’t your parents’ trade zone anymore.

2. The visible hand: Industrial policy is back in both countries

As hopes for free trade fade, a new age of state capital is evolving. Both Washington and Ottawa are now explicitly using government spending, tariffs, procurement, and regulation as tools of economic strategy—and the era of assuming that politics would leave globalization alone is over. Daleep Singh of asset manager PGIM put it plainly: we are in a world of fiscal dominance, with industrial policy in the midst of renaissance. Every cross-border linkage—trade, capital, energy, technology—is now at risk of being weaponized for geopolitical leverage. The result is more government debt, higher trend inflation, more political risk and a stronger case for physical assets connected to economic security.

Will this also mean a return to mercantilism? If governments try to gain economic favour by diminishing and constraining others—competitive strength over comparative advantage—Canada will need to play its many cards more assertively: low-carbon natural gas, critical minerals, food and fertilizer, nuclear fuel, and a stable rule-of-law environment that capital increasingly prizes. It presents material opportunities for business, too, as governments create incentives to reshore economic sectors and underwrite the scaling of companies, from AI to life sciences. Annesley Wallace of pension manager HOOPP captured the investor mood: Canada now has the attention of global investors in a way it didn’t a few years ago. But capital wants to see execution and policy certainty, not just ambition.

3. The data deficit: Canada’s struggle to compute (at scale)

Data centres are the new factories—the physical infrastructure of the AI economy. And Canada is largely absent from the map. Hamid Moghadam of Prologis, one of the world’s leading logistics companies with $5 billion invested in Canada, was direct: companies building data centres go where it is easiest. Canada is not on that list. Prologis currently has no AI data centre capacity in Canada, with the Netherlands and the United States dominating. The culprit is a “quirky provision” in Canadian tax law that imposes a 15% burden on U.S. tax-exempt capital invested in Canadian properties—a friction that doesn’t apply in reverse. That could be the greatest cross-border risk as enterprise users (unlike the hyperscalers) turn more to inference models that can use low-latency infrastructure. Bell Canada is seizing on that with a new data centre in Regina that is, initially at least, expected to rely on U.S. users.

The slower pace of AI adoption in Canada—fewer than one in five companies, and fewer public sector users have deployed the technology—is starting to show up in economic and business performance. Canada is trying to catch up with a new national AI strategy that aims to invest in AI awareness and skills, as well as business adoption. Jenny Johnson of investment management firm Franklin Templeton put it starkly: the pace of AI is moving so quickly that companies that get it right will leave others in their sector behind permanently. She told her own executives: if you aren’t building agents yourself, you’re already behind. Trouble is, citizens in both countries are increasingly anxious and skeptical about AI. That’s leading to more grassroots pressure, including in this year’s mid-term election campaigns in the U.S., to regulate AI.

4. Trust and algos: A diverging tech sovereignty race

Both Canada and the United States are navigating a crisis of public trust in technology—but they are responding in ways that could put them on a collision course over regulation, data, and digital trade. In the U.S., the AI boom is turbocharged by private capital, hyper-scalers, and a permissive regulatory culture. The concern is less about governance and more about falling behind China in the AI arms race, although local resistance to data centres, especially over their use of electricity and water, could change the conversation. Canada, by contrast, is pursuing a more rights-based, sovereignty-first approach.

In both countries, and across their borders, the AI revolution is moving so quickly that governments seem destined to react. Ian Bremmer, Eurasia Group’s founder and president, warned of a deepening crisis in which no political leader could overcome a structural gap between technological transformation and outdated governance systems. Technology companies, he said, increasingly act as functional sovereigns in their own domains—and the absence of governance around AI is one of the most urgent risks on the horizon. Canada’s AI Minister Evan Solomon acknowledged the paradox: Canada’s best and biggest AI partner remains the United States, and access to frontier models, compute, and capital still flows primarily north-south. But as Canada builds its own AI sovereignty framework—and as the Safe Social Media Act, new privacy rules, and the AI for All strategy take shape—conflicts over data flows, platform regulation, and digital trade are increasingly likely.

5. Fortifying the continent: National defence as economic offence

Defence is again central to the relationship, and central to emerging divisions. One big one: what technologies will dominate the battlefields and defensive lines of tomorrow? Case in point: Three days before the summit, an Iranian drone shot down a U.S. Apache helicopter, and then an American sea drone rescued the two downed airmen. The U.S. is investing heavily in AI systems, robotics and autonomous war machines, as well as bio- and cyber-weaponry. Canada is trying to catch up on advanced military technology, and at the same time restore and restock bigger hardware like fighter jets and submarines. The Canadian strategy is driven by economic policy as much as defence strategy, to build trade ties with European and Asian allies.

The wars in Ukraine and the Middle East have rewritten defence doctrine. Scalable production and resilient supply chains have proven as decisive as firepower. MDA Space CEO Mike Greenley put it this way: defence and space remain areas of full collaboration and full integration, even amid trade tensions. “The stronger we are, the better partner we are.”

That may require an intricate matrix of supply chains and partnerships in which Canada could continue to play a role in the F-35 fighter jet program while also building the GlobalEye partnership between Sweden’s Saab with Bombardier to make surveillance aircraft for Arctic defence. Energy and critical minerals will be a critical component of this new chapter. Vivek Lall of defence firm General Atomics identified a technology triad linking AI, nuclear energy, and autonomy as the defining framework for the next generation of defence capability—and argued Canada-U.S. collaboration has significant potential across all three.

6. The Contested North: The Arctic as a continental lynchpin

The Arctic is no longer a remote policy afterthought. It has become a global economic, geopolitical, and strategic battleground—and one where Canada and the United States have no choice but to work together, and quickly. Olafur Grimsson, former President of Iceland, framed the challenge: the past decade has seen a flood of new arrivals into the Arctic, as China, Russia, and a constellation of Asian economies sought access. The old notion of sovereignty, where lines on a map settled the question, no longer applies in an environment that is rapidly becoming both economically accessible and strategically contested.

Thomas Dans, Chairman of the U.S. Arctic Research Commission, was direct about Washington’s view: both countries have “a lot of room both to catch up, but also to surpass and to really lead.”

He said North America needs to look over the North Pole and also toward the North Star. First challenge is Russia. Even though there may be room for cooperation over fisheries and shared resources with the Kremlin, Grimsson warned the West risks losing sight of what Moscow is doing in its own Arctic, particularly as Russia deepens energy, pipeline, and mining links with China, India, and other Asian powers. The same sort of resource development is possible on the North American side. Then there’s the skyward trajectory. Continental defence may rest in the ionosphere, but it doesn’t stay up there. The two countries need to develop land and sea-based systems in the Arctic to connect with their growing space-based defence operations.

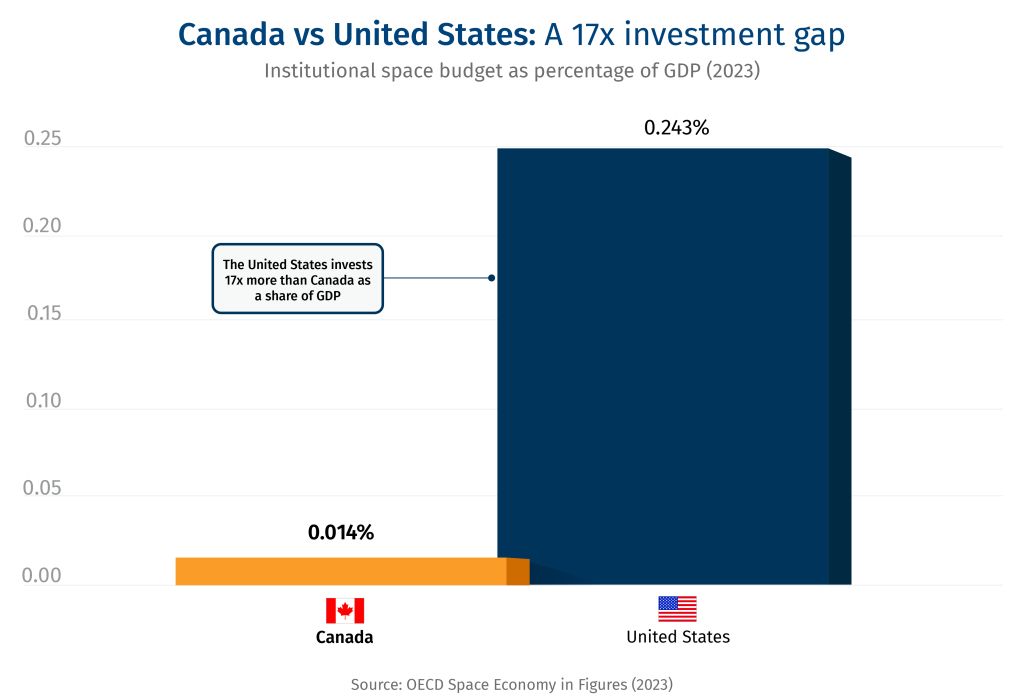

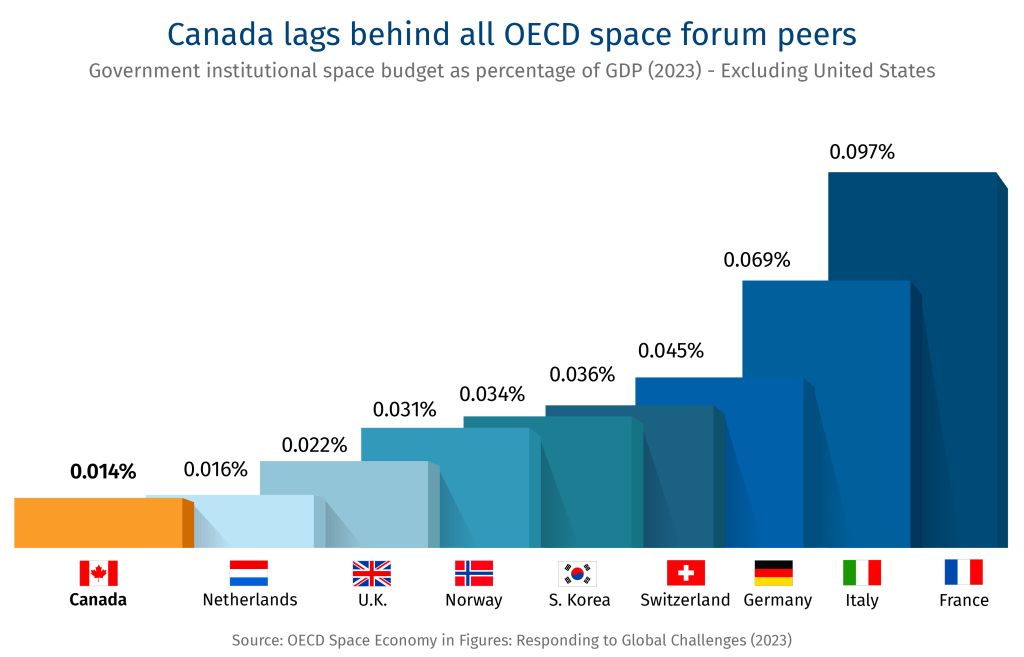

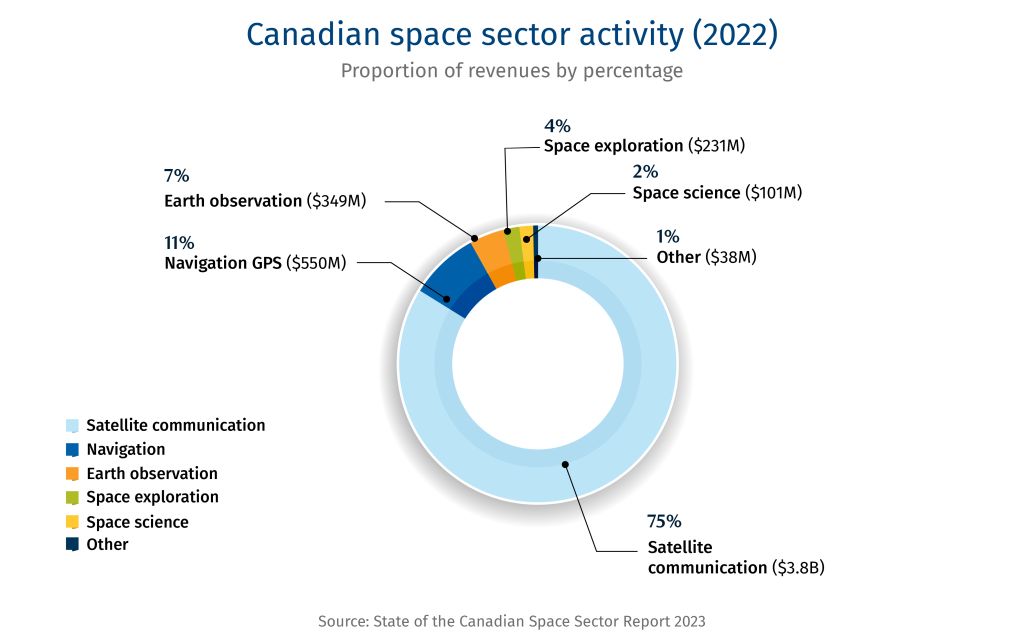

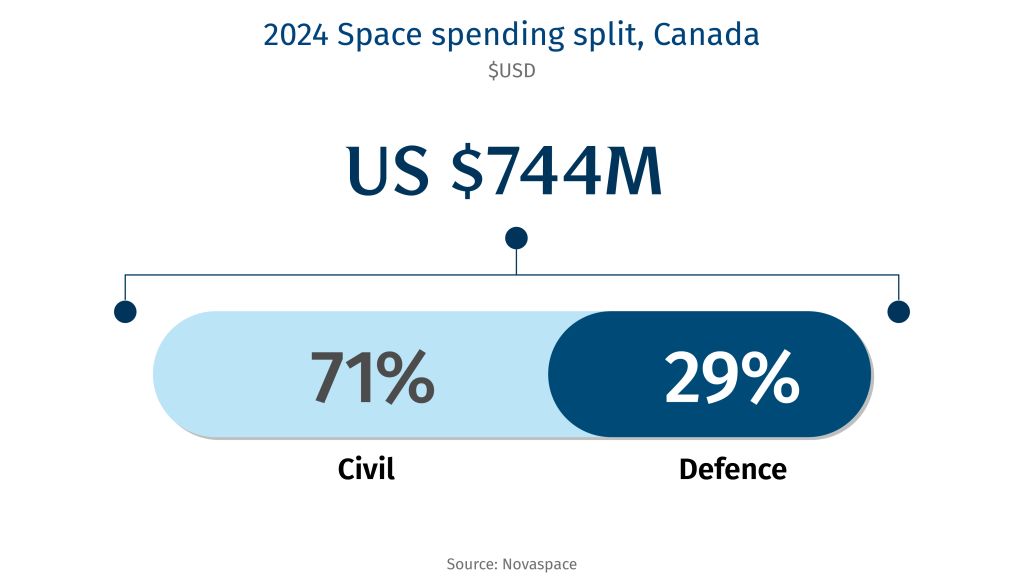

7. New frontiers: The longest undefended border moves to space

Canada has always punched above its weight in space—but largely as a junior partner to NASA. That posture is shifting. Canada is now trying to carve out a distinct space identity, rooted in its own strengths and connected to a broader set of international partners, while remaining deeply integrated with the U.S. It may pose the greatest challenge to continental cooperation. Canadian astronaut Jeremy Hansen said the two countries will find the most opportunity by playing to their strengths, rather than for diplomatic reasons. For Canada, those strengths include Earth observation, space-based communications, and robotics, as well as onboard computing.

Countries are increasing spending rapidly, creating a 2.5x economic multiplier for space manufacturing and technology. But leaving the so-called final frontier to commercial firms may underestimate the geopolitical tensions up there. In the race to return to the moon, China is partnering with 11 nations, the U.S. with 60. Canada is in the latter coalition and contributing meaningfully. Hansen compared the challenge to the ethos of a space crew: “People who can point out what’s broken and stop there is not acceptable in our space culture.” Canada’s space ambition requires the same discipline—specific proposals, not just aspirations.

8. The long way around: Diversification without decoupling

Canada is seeking to diversify its economic and security relationships, without undermining its integral relationship with the U.S. Industry Minister Mélanie Joly said Canada has trade agreements with 52 countries. Discussions with the EU are deepening—not just as a response to tariffs, but to create genuinely integrated Canadian-European companies, and align industrial policies. Michael Sabia, Clerk of the Privy Council, was equally clear: Canada’s U.S. strategy and its broader global strategy are mutually reinforcing. “We are not decoupling. We are diversifying.” On China, his framing echoed U.S. language precisely—de-risking, not decoupling—with clear guardrails defining where Canada can and cannot engage.

But diversification is not free, and the infrastructure required to redirect Canadian trade is largely not built yet. West Coast pipeline capacity remains critically constrained, limiting Canada’s ability to sell oil and gas at premium prices in Asian markets. Port infrastructure in Vancouver and other Pacific gateways—rail connections, bridge capacity, terminal throughput—lags badly behind the ambition of a serious Pacific trade strategy. And permitting timelines for new infrastructure projects remain a systemic bottleneck. Those are solvable problems. Sabia’s closing argument was that Canada holds a genuinely strong hand—low-carbon gas, food, fertilizer, critical minerals, AI capabilities, and a trust premium that flows from values and history. “This is not a time for national anxiety. This is a time for confidence.”

John Stackhouse is the Senior Vice-President in the Office of the CEO at Royal Bank of Canada