Overview

Economic theory and evidence tell us that the more educated a society is, the more productive its economy will be. Countries or regions with highly educated people will attract advanced industries, generate more savings and investment and create entirely new economic sectors.

That promise is not yet fulfilled in Canada. Despite having one of the world’s highest rates of postsecondary education and a steady rise in postsecondary attainment over the past quarter century, economic performance, including productivity, is lagging. Too many graduates have advanced degrees that don’t deliver an advanced economic return. Not enough employers can build teams with the right skill sets. Too often, students don’t know how their programs line up with the labour market. And our international students continue to struggle to gain productive work in a fast-changing economy.

The challenges are all the more pressing in a worsening trade environment in which many Canadian businesses are looking to quickly pivot to more global, and more competitive, opportunities. Trade wars mean talent wars.

Of course, this is not entirely new. Canada’s postsecondary sector, and employers and governments, have been working for years — decades, really — to build a more productive, knowledge-driven and skills-based economy.

But for all the innovations in workforce-readiness, there‘s still a substantial gap between education inputs and economic outcomes, which Canada’s struggling economy and productivity cannot afford.

In this report, we identify why Canada is not reaping the benefits of its globally respected postsecondary education systems and we make recommendations about how to address our current postsecondary education/productivity disconnect. Getting that relationship right is key to sharpening Canada’s competitive edge. At the end, we present examples of what more productive economies have done to leverage the knowledge capital and research capacity of their postsecondary systems. And we highlight innovative experiments in postsecondary delivery, giving food for thought.

RBC launched The Growth Project initiative this year to discover a new generation of ideas for the Canadian economy. Throughout this project, we’ve been exploring key drivers of economic growth including productivity. To build on our report on why the economy is stuck in neutral, we’ve partnered with the Business + Higher Education Roundtable (BHER) to address the role of postsecondary education in Canada’s productivity crisis.

Productivity is an important measure of an economy’s efficiency at generating additional income from each hour worked. Some economies generate more additional income per hour worked than others, leading to better economic performance and growth.

Where we are

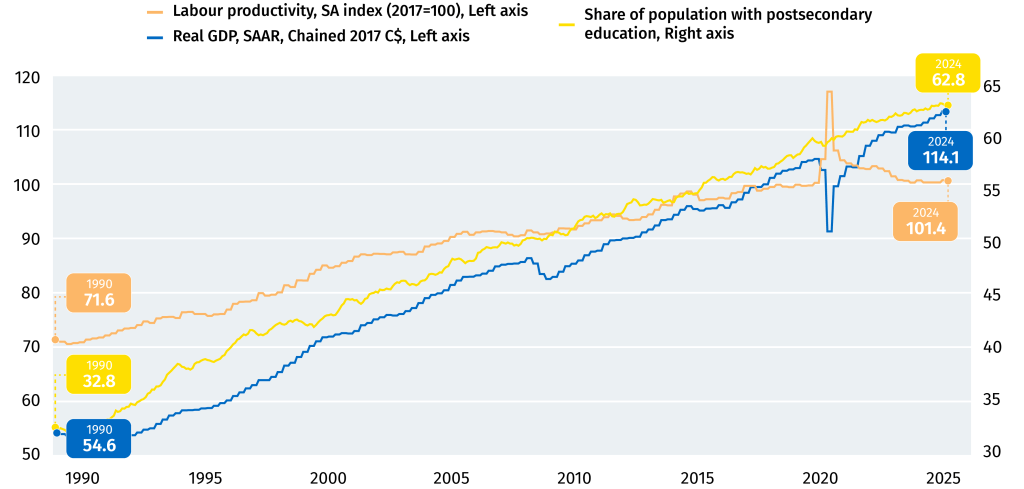

Canada’s labour productivity growth falters even as more Canadians obtain postsecondary education

Source: Statistics Canada, RBC Economics

Canada’s population is highly educated but our productivity doesn’t match — We are the most highly educated population in the G7 and above average across OECD countries. In 2024, some 63% of Canadians aged 25 to 64 had a postsecondary credential compared to an OECD average of 41%.1 Yet these two charts show that our productivity record has not kept up and is not only lagging our peers but has worsened over the past decade even as the rate of higher education, including for new Canadians, has improved.

And that productivity growth lags many OECD countries

Average annual labour productivity growth, 2014-2023, %

Source: OECD, RBC Economics

Our graduates get jobs, but their incomes — College and university graduates experience lower levels of unemployment and earn more over time than Canadians with a high school diploma or less.2 But, regardless of education level, Canadians earn an average of 8% less than their American peers,3 a gap that is wider in many professions.4 This is one reason for a perennial migration — a brain drain — of people with advanced degrees to the United States and a loss to Canada, economically and otherwise. The differing costs and standards of living in the U.S. aside, Canada still only falls in the middle of the pack when we look at individual returns on investment from higher education compared to peer countries.5

The Challenges

At its best, higher education contributes to productivity by developing a skilled workforce, driving innovation through research and fostering industry collaboration. Postsecondary institutions equip graduates with critical skills, support businesses with cutting-edge research and fuel economic growth by creating new technologies, startups and talent. Research has shown a positive relationship between a region’s economic health and the presence of higher education institutions, with an additional 0.4% in future GDP for every 10% increase in the number of universities per capita11. This effect is driven by boosts to human capital and innovation, not just direct institutional and student spending.

Higher learning institutions also contribute to the social and intellectual vitality of a community, region, and society that are hard to quantify. Nevertheless, Canada’s record underscores that the presence of a higher education system with a high rate of participation and research activity does not always translate into high returns when we look at economic measures.

So, what’s missing? Pinpointing which factors contribute to the overall economic value of a postsecondary education is limited by a lack of data and research12 13. But we can look to other countries with higher productivity and strong postsecondary systems for clues about what works and is showing promise — some of those are highlighted later in this report. We can also identify clear gaps here at home, whether that’s in human capital development or in research.

Disconnects persist between the knowledge and skills outcomes of Canada’s higher education systems and labour market needs.

The OECD has noted that “higher educational attainment does not always directly correspond with higher skills14.” Employer surveys consistently indicate that companies still have a hard time finding new hires with the skills they need, especially interpersonal and communication skills15. We also know that there is a growing gap in graduates’ technical skills related to artificial intelligence, cybersecurity and working with big data, all areas rapidly growing in importance.

Postsecondary business models are inadequate to meet the outcomes expected of Canada’s higher education systems in the current global economy.

Postsecondary institutions have a balance sheet problem. Their finances are rapidly changing due to stagnating provincial government funding, restrictions or even freezes on student tuition increases, and a federal immigration policy shift that has led to steep drops in international students and the significant revenue their higher tuition contributed to the bottom line. The postsecondary revenue crunch is likely to worsen without a reformed business model — one that is capable of responding to the demands of a changing economy.

Trouble is, postsecondary leaders are constrained by insufficient control over their revenue sources, regulations that circumscribe how they run their budgets, and little to no ability to cut or reallocate some of their biggest fixed costs. Staff wages and benefits amount to more than 50% of total expenditures at both colleges and universities16 and a high presence of permanent faculty and teaching staff protected through collective agreements, tenure or both limit institutions’ ability to nimbly adjust or close programs as enrolments and demands change. The hiring of contract faculty to teach students has been one attempt to gain some flexibility but the practice is not a panacea and has led to a teaching underclass with insufficient access to resources or basic job stability.

Amid this shaky and constrained financial picture, academic programs that connect best with high productivity industries are the most expensive to run. Science, technology, engineering and mathematics programs – STEM — have been expanding over the last 30-plus years as labour market and student demands have shifted, from 18.3% of enrolments in 1992-1993 to nearly 26% in 2022-202317. But labs, computers and other equipment mean they cost at least twice as much as training for a humanities or business student. If traditional revenue sources are no longer reliable, colleges and universities need to be freed – and encouraged – to develop fresh revenue streams, funding models and educational redesigns that make sense for them and the broader societal and economic needs they serve. The case of Arizona State University (illustrated later in this report) is an example of an institution that has taken an entrepreneurial approach, reimagining its programs and research activities as well as its business model to gain back institutional control from reduced state funding while making student access a priority, including for marginalized students.

Canada lacks comparable data to assess outcomes of our postsecondary systems and support linkages with labour market information.

It’s hard to fix what isn’t well-measured and Canada falls down on data to assess outcomes of its postsecondary systems20. While completion and employment rates data are sometimes tracked, outcomes data are not uniform across provinces or even institutions; nor is it timely or robust enough to confirm alignment between graduates’ skills and the labour market. The provincial/territorial control of higher education systems may seem to make national standardization of this data a non-starter. But given the renewed exploration of how to better harmonize provincial/territorial economies and trade, there is a perfect opportunity to bring postsecondary institutions into the discussion.

Countries such as the U.S. and Australia do a better job with postsecondary data tracking, enabling well-informed public policy discussions and change. In the U.S., tracking has been federally mandated for institutions that participate in federal student aid programs, and data is available through its Integrated Postsecondary Education Data Systems. Australia has developed its Quality Indicators for Learning and Teaching, a suite of annual government-endorsed surveys that follow higher education students from enrolment to employment.

There is a mismatch of graduates with advanced degrees.

Nearly 15% of Canada’s working-age population hold a graduate degree today — just below the share that held a bachelor’s degree in 1997, at 16%21.But those degrees aren’t always leading to jobs that require them. (In fact, there are more job vacancies for positions requiring only a high school diploma than there are openings for positions requiring a bachelor’s degree or higher22.)

As a result, there’s a rising number of highly educated Canadians working in jobs that do not make effective use of their degree. The OECD has ranked Canada as having the second-highest overqualification rate of 37 countries23, with an overqualification rate of 10.6% for Canadian-born workers and 11.8% for Canadian-educated immigrants in 202324.

Degree-holders undoubtedly enjoy a wage bump compared to those without a postsecondary degree. But that wage premium is shrinking when comparing the benefit of a master’s degree to a bachelor’s. Between 1997 and 2019, that premium averaged 23%. Since the pandemic, that’s fallen to 18% as more graduate degree holders compete for the comparatively smaller pool of jobs that require their credentials.25 What people pursue in their advanced degrees matters too: business PhD holders were the highest earners in a 2021 analysis of doctoral graduates, although they represented only 4% of all PhDs, while humanities and science PhDs (9% humanities and 22% sciences) were among the lowest. Math and computer science doctorate holders meanwhile showed the highest earnings growth in the five years after PhD completion26.

As well, fewer Canadian PhDs are working for private industry, compared to the U.S., which may be partly tied to an economy that is still heavily resource-based and where we have lower levels of industry R&D investment that would demand their skills27. Nevertheless, graduate students have relatively low levels of participation in work-integrated learning experiences (discussed later in this report) and lack opportunities to demonstrate and apply their skills and expertise to Canadian firms that could benefit from them. Canada certainly needs people with advanced degrees, but more thought should be given to which programs are of greatest need and how to make the most out of the skills and knowledge they produce.

Canada has seen expansion of postsecondary campuses and programs over the last 25 years but it’s unclear whether we have the right number or distribution.

Participation in higher education has expanded over the last 35 years and along with it has come expansion of programs and campuses. We need a high-quality postsecondary sector to educate and inspire the next generation of talent and skilled workers while generating transformative discovery. But it’s worth asking whether the size and spread of Canada’s roughly 100 public universities and 200-plus colleges with associated campuses and 25,000-plus programs are aligned as well as they could be with the country’s most pressing needs and the challenge of creating a more productive economy.

This question becomes more urgent given the pullback on international students who until 2024 functioned as a significant counterweight against more recent shrinkage in domestic enrolment and revenue, which has been acute in some regions. Population demographics forecast modest growth among Canada’s over the next decade before declining to something slightly above current numbers28.

Memories are also relatively fresh of the 2021 financial crisis at Laurentian University in Sudbury, Ont., when the institution declared insolvency due to what was later deemed primarily to be poorly planned capital projects combined with administrative bloat29.

Let’s think seriously about how to better align higher education resources with a broader student demographic and the evolving needs of the economy.

We are not setting up international graduates of Canadian postsecondary education for integration into high productivity labour sectors.

International students are part of the solution to Canada’s future economic needs and its productivity crisis. But over the last several years we’ve seen how the country’s efforts to recruit these students ballooned out of control, leading to students being underserved and/or ending up in programs without pathways to high value industries. As one example, international students are more likely to be enrolled in business or management programs versus STEM30,and many have struggled to find jobs after graduation when their visas allow them to stay.

As Canada works to reduce and recalibrate this student pool, we should focus on recruiting and educating high quality international students with targeted workforce development in mind. The federal government recently made this a requirement, with new rules about fields of study that international students need to be enrolled in to qualify for post-graduate work permits.

That’s a start, but the execution left something to be desired and threw many postsecondary institutions into crisis-mode trying to fill financial and programmatic gaps overnight. When the dust settles, fields of study should be chosen with consideration of regional labour demands too. International students will also need more help to translate their skills to the workplace, via focused career counselling and work-integrated learning opportunities, which some struggle to access due to immigration work restrictions.

Students need a more complete skills toolbox.

We need data scientists who are storytellers, electricians who can communicate technical complexity to their clients, and culture creators who can make magic by leveraging cutting-edge digital technologies. Hard skills and knowledge learned in STEM programs are valuable, but so are the skills where humanities excel: persuasive and effective writing and speaking, critical thinking and creative approaches to problem-solving.

We also know that students may not end up working in the domain where they received their education, whether that was in STEM or business/humanities31. Not enough postsecondary programs encourage cross-pollination across disciplines. But programs such as McGill University’s Bachelor of Arts and Science (B.A. & Sc.) degree, which allows students to study disciplines in both faculties, BCIT’s Bachelor of Creative Industries program that combines training in the arts, technology, and business, or Langara College’s Environmental Studies program, blending biology, chemistry, English and geography, are promising examples32. Many programs leave room for electives, too, where students can acquire that breadth of skills independently.

But this is tinkering along the edges of what’s possible and needed. As enrolments continue to slide in humanities programs, postsecondary institutions must reimagine the core competencies the humanities provide to all students and how to extend that across subjects, disciplines and faculties in a world of growing STEM demand. Critical thinking and the ability to analyze complex problems are top skills for the most needed jobs in the face of advancing artificial intelligence and automation33 as is the ability to identify how to effectively use these technologies. Can we start to break down entrenched silos that prevent the STEAM concept from being embedded more directly into most students’ programs and curricula?

Canadian companies are not making the most of postsecondary research output and are weak adopters of postsecondary research innovations.

In 2022, Canada ranked 10th globally in terms of scientific publications34 and we are a global leader in specific fields, such as artificial intelligence. But Canadian companies aren’t picking up the ball when it comes to making the most of made-in-Canada discoveries. The U.S., with a much better track record, benefits from a more robust ecosystem to support research translation into market applications, including venture capital funding, supportive public policies and an intellectual property framework that incentivizes researchers and postsecondary institutions to pursue commercialization.

All told, Canadian business investment in research and development was just 1.7% of GDP in 2022, putting us below the OECD average and well below highly productive countries like Israel (6.0%), South Korea (5.2%) and the U.S. (3.6%)34. Even in AI research, where Canada is a global leader, we lag peer countries in its commercial use.

How we can do better

The discussion about aligning postsecondary education and training with labour market needs isn’t a new one. Colleges and universities recognize this, and there are growing pockets of innovation. But employers and economic data signal a different story: that Canada is still missing the mark in generating the skills and knowledge needed to meet its evolving productivity challenge in an increasingly competitive world. Here are a few things we can do differently:

Eliminate barriers to institutional innovation.

Postsecondary institutions in Canada require new business models that free them to be more entrepreneurial and in control of their financial destinies while remaining responsible and accountable to the people and communities they serve.

Too often institutions that attempt to innovate are frustrated by a host of mostly provincial but also federal regulations on everything from tuition to procurement to partnerships and mandatory programs without corresponding government financial support. Reasonable deregulation would help clear the way for institutions to become more creative, collaborative and in step with a changing world. Internally, colleges and universities need mechanisms to incentivize change where barriers and resistance exist within institutions to creating or altering programs at scale or incorporating industry into program design.

Enhance the awareness and articulation of skills developed in PSE programs.

Prospective students and new graduates need to know the skills they will emerge with, allowing them to fairly evaluate whether a program is for them and to communicate these skills to employers. Some programs are already clear about this, notably at colleges, but the practice should become widespread and should be tied into a larger drive towards national comparable postsecondary outcomes data that can be linked to labour market information.

The challenge can be more acute for advanced degree holders, most of whom won’t spend their careers in academia. They, and employers, also need to understand what skills they’re developing through their research and how these can be translated to a non-academic workplace.

Get work-integrated learning to where it’s needed most.

Work-integrated learning, or WIL, is the practice of integrating work and real-world experiences into a student’s higher education program. Internships, practicums, co-op programs, entrepreneurial mentorship and field work are common examples. These experiences help students connect and apply their learning to workplace realities, acquire new and relevant skills and assist businesses to recruit and develop students for their specific labour needs.

As such, WIL is part of the solution to Canada’s productivity and skills challenges – two-thirds of employers participating in WIL programs through BHER reported an increase in their productivity.36But while the country has made important strides in providing these opportunities, WIL is not yet the norm – just under half of all postsecondary graduates in 2020 had experienced a WIL opportunity.37 There are also variations in uptake, with PhD students (18%) and those in the humanities (16%) less likely to have a WIL experience38.

Most businesses in Canada are small and medium-sized enterprises (SMEs) and face more barriers than larger organizations to participating in conventional forms of WIL in terms of resources, time and risk. For them, shorter-term, more flexible and less resource-intensive forms of WIL aligned more closely with SME realities and needs make more sense. These should be considered as part of a robust suite of WIL experiences. They include consulting engagements, multiple short-term placements of up to 10 days, online projects and placements, and engagement in industry challenges through hackathons, competitions and course-based projects submitted by employers39.

Develop upskilling and reskilling opportunities.

Businesses have a responsibility to help workers stay current with the skills needed to keep doing their jobs as they evolve with technological and other changes. Postsecondary institutions are well-positioned to be providers for that learning and can take advantage of these opportunities as revenue streams in a reformed business model. Too often Canada’s companies struggle to partner with postsecondary institutions and end up developing their own in-house training solutions40.

To do that well, higher education must stay on top of and respond to upskilling opportunities in their communities, partner with employers (and vice versa) to understand and respond to specific skills gaps and create programs that fit the working and personal lives of learners. Continuing education departments are particularly well-positioned to do this. An opportunity also exists for governments to financially support and promote these programs, such as through tax and other incentives, as they look for policy responses to labour force disruption. Microcredentials – rapid, often virtual courses — are one form of upskilling that have proven effective in complementing workers’ existing skills41.

especially the programs and courses that are developed by postsecondary institutions (for example, Ontario provides access to these via its provincially funded eCampus portal).

Similar opportunities exist for postsecondary institutions in reskilling programs where workers exiting one industry acquire an entirely different set of more in-demand skills. Partnering with local companies’ outplacement programs is one example. Given that it’s a more substantial undertaking than upskilling, the reskilling shift can be trickier, especially if we want it to happen quickly. Competency-based education (CBE) courses may offer a way forward. CBE is singularly focused on mastery of a discrete set of competencies, often required for a particular job, such as nursing. CBE courses tend to be flexible, virtual, personalized, self-directed and recognize prior learning. The approach has been used in limited ways in Canada, is more widespread in the U.S. and may offer inspiration for reforming the structure and delivery of traditional programs42.

Intensify the drive towards institutional differentiation.

Canada has done an excellent job of providing access to public postsecondary education across a big country and into remote communities. But we neither need nor can we afford to have every institution offering the same menu. Not every institution needs its own artificial intelligence research hub or history department.

Differentiation is critical, where public colleges and universities are encouraged to lean into the teaching, learning and/or research they are best at, and discouraged from unnecessary program duplication. The government of Ontario has followed this policy, though without a strategic vision for the sector or what separate roles should be played by colleges and universities43.

Differentiation might mean institutions that are focused on and excellent at teaching mostly undergraduates, such as members of eastern Canada’s Maple League of Universities, or that are highly research-intensive, such as the University of Toronto, or whose teaching and research are strongly aligned with key local industries, such as the country’s polytechnic institutes.

Differentiation can also happen through the business model an institution uses to sustain itself and remain relevant. It can be promoted through strategic mandate agreements negotiated between institutions and government funders, as Ontario does. Government research funding models can also encourage differentiation and build capacity by favouring institutional specialization, such as through the federal government’s Canada First Research Excellence Fund.

The growing financial sustainability crisis faced by colleges and universities makes differentiation a strategic imperative for each institution.

Make it easier for Canadian businesses to adopt and invest in research.

Our world-class postsecondary researchers are part of an innovation pipeline that includes Canadian businesses who can adopt researchers’ discoveries, commercialize, refine and run with them, boosting their own competitive edge. But that pipeline is slowed by Canada’s fragmented regulatory and approval processes, at every level of government, which delay and complicate business investment decisions. Streamlining those processes by implementing, for example, a harmonized federal-provincial environmental assessment process for projects of national strategic importance would speed up approvals and drive private sector investment into new major projects.

Our outdated tax system is also in need of a comprehensive review with an eye to encouraging greater private sector investment in Canadian research and development. This review could include an assessment of the impact of recently announced changes to the, could further spur private sector R&D investment.

Conclusion

Postsecondary education is one of this country’s greatest strengths. But we’re not using it to its full potential and we’re not keeping pace with the rest of the world as a result. Our productivity crisis is clear and urgent with direct impacts on the standard of living all Canadians can expect, including the graduates of tomorrow, especially in a global economy that is more divided and disruptive. Governments, institutions and employers must each play a role in bridging the gap:

-

Take action on regulatory and tax reform to encourage greater private R&D investment and adoption of made-in-Canada research discoveries.

-

As federal departments work through a reformed strategy for international students, focus on ways to match their abilities and interests with programs aligned to Canada’s most pressing economic needs, regionally and nationally. Eliminate immigration restrictions that prevent international students from participating in work-integrated learning.

-

Address business barriers and raise awareness about the value of participating in work-integrated learning experiences, especially among SMEs, by investing in partnership and capacity building.

-

Use tax incentives and federal funding to encourage industry partnership with postsecondary institutions in support of cost-effective, high-quality upskilling and reskilling programs for employees.

-

Engage in pan-Canadian work and leverage relevant federal programs and departments to develop comparable, accessible, comprehensive and easy-to-understand data for timely identification and analysis of postsecondary education outcomes, including by institution and program.

-

Implement a clear vision and strategy for the province’s postsecondary systems that differentiates between the purpose of college vs. university programs and incentivizes differentiation within them.

-

Embark on a process of limited postsecondary deregulation that gives institutions more control over their finances, revenue streams and promotes innovation in programs and industry partnerships.

-

In parallel, promote accountability through mandatory institutional reporting of comparable and detailed data on postsecondary outcomes by institution and program, including graduates’ skills, which can be linked to labour market information.

-

Continuously and rigorously review changing labour needs and update labour market information to better support alignment with postsecondary programs.

-

Be explicit about the skills students will develop through the programs and courses offered to them and provide ways to communicate those to employers. Draw on the expertise of continuing education departments which are already well-positioned to help.

-

Encourage, support and incentivize departments and faculty to explore new models of teaching and learning, especially where these integrate skills students will need in the workplace.

-

Break down faculty, disciplinary and subject siloes that interfere with cross-curricular and interdisciplinary learning needed to promote STEAM skills and expose students to problems in high labour demand sectors.

-

Look for novel ways to spread student awareness of work-integrated learning opportunities, why they’re valuable and help them overcome barriers to access.

-

Engage with postsecondary institutions — or intermediaries like the Business + Higher Education Roundtable that can help navigate to and through them — to communicate skills needs and identify potential opportunities for collaboration.

-

Explore becoming a work-integrated learning participant to bridge the skills gap and potentially develop the next crop of employees.

-

Look to postsecondary institutions for short-duration programming to help upskill and/or reskill your employees before turning to untested third-party providers.

-

Engage in local outreach to high schools to raise awareness about their industry, why it’s an exciting place to work and the education pathways to a fulfilling career in that sector.

-

Continue to contribute to labour market information systems by sharing data with governments and collaborate to find new ways to enhance the accuracy and relevance of labour market analyses and policy development.

-

South Korea – This east Asian powerhouse has the highest rate of postsecondary education attainment in the OECD, at nearly 70% of its population and is an OECD leader in productivity growth. The country has leveraged its educational advantage towards its economic development, with a strong top-down system of close research collaboration between government, industry and the academic community. Although it is currently facing slippage in its record, its fundamentals remain strong and it stands as an example of what’s possible through robust policy, investment and collaboration.

-

Israel – With a 6.5% growth rate in 2022, Israel’s high-tech sector accounts for more than 15% of GDP and universities are tightly woven into its activities. Israel was ranked first globally for AI talent concentration and fifth for AI talent penetration by Stanford University’s 2024 AI Index Report. This has been attributed to “an exceptional ecosystem of startups, academia, and strategic support from both local and multinational players.”

-

Slovenia – Showing strong productivity gains over the last decade, this small eastern European nation has also seen significant gains in postsecondary education attainment since 2012, from 35.3% of the population to 47.3% in 2022. The country directs about 1% of GDP towards higher education, has seen rapid growth in STEM program graduates and manages higher education within the same government ministry as science and innovation.

Digital Technologies Program, York University

-

The challenge: Address skills gaps in the digital economy and foster a diverse, innovative workforce.

-

The innovation: Canada’s first fully work-integrated learning degree, where students spend 80% of their time in the workplace, including paid work opportunities, and 20% on coursework. The competency-based curriculum allows students to apply real-world skills while moving through advanced tech-related topics. Employers highlight gains in productivity resulting from longer-term placements and deeper student engagement with projects.

Electrical Technician Program, Nova Scotia Community College

-

The challenge: Meet the demand for new skills as Nova Scotia’s government works to grow its onshore wind generation.

-

The innovation: With an investment from RBC Foundation as part of a larger $2-million commitment, NSCC is updating its Electrical Technician Program to include large-scale wind energy training, in alignment with labour market demand and provincial clean growth initiatives. The funds will support new course development and hands-on training materials.

Global Innovation Clusters, Innovation, Science and Economic Development Canada

-

The challenge: Solve complex problems and improve Canada’s productivity in key emerging industries.

-

The innovation: Better known as the “superclusters,” this program brings together businesses, academic institutions and nonprofits under five industry categories to drive growth and innovation, backed by shared government and industry funding. The program generated more than $1.6 billion in project spending by the federal government and industry partners between 2018 and 2023 and created nearly 24,000 full-time jobs.

Mitacs Research and Internship Partnerships

-

The challenge: Connect postsecondary research expertise and innovation to problems faced by businesses and bridge the skills translation gap for undergraduate and graduate students.

-

The innovation: Through several programs, this not-for-profit organization brings students and post-doctoral researchers together with private sector partners through internships and collaborative research projects focused on real-world challenges faced by the business. Mitacs also provides dedicated professional skills development for graduate students and postdocs. The program has resulted in an 11% increase in productivity for its more than 12,000 partners and $1.2 billion in R&D spending between 2018 and 2023, according to a Statistics Canada/Mitacs analysis.

For more, go to rbc.com/thegrowthproject.

Download the Report

Contributors:

RBC Thought Leadership

John Stackhouse, Senior Vice-President, Office of the CEO, RBC

Caprice Biasoni, Graphic Design Specialist

Shiplu Talukder, Digital Publishing Specialist

Business + Higher Education Roundtable

Val Walker, CEO

Matthew McKean, Chief R&D Officer

Andrew Bieler, Director of Partnerships & Experiential Learning

Carmela Busi, R&D Associate

External Contributor

Moira MacDonald, Writer & Copy Editor

1. OECD. Adult Education Level. Retrieved from: https://www.oecd.org/en/data/indicators/adult-education-level.html?oecdcontrol-4e20b448f7-var6=TRY

3. RBC Economics (2024). Canada’s Growth Challenge: Why the economy is stuck in neutral.

4. Statistics Canada and RBC Economics Research.

5. OECD and RBC Economics Research.

10. Ibid.

12. OECD (2019), Benchmarking Higher Education System Performance, Higher Education, OECD Publishing,

13. Paris.

15. OECD (2019), Benchmarking Higher Education System Performance, Higher Education, OECD Publishing,

16. Paris.

21. Usher, Alex, “The Shifting Cost-base of Ontario’s Higher Education System,” February 2020.

23. Statistics Canada. Retrieved from Labour Force Survey.

24. Statistics Canada (2023). Unemployment and job vacancies by education, 2016 to 2022.

26. Ibid.

27. Statistics Canada. Retrieved from Labour Force Survey microdata.

29. Ibid.

31. Office of the Auditor General of Ontario (2022). Special Report on Laurentian University.

34. RBC (2018). Humans Wanted: How Canadian youth can thrive in the age of disruption.

35. Nature Index. (2023). 2022 Research Leaders.

36. OECD. Gross domestic spending on R&D.

38. Statistics Canada. Table 37-10-0249-01 Work-integrated learning participation during postsecondary

39. Ibid.

42. Pichette, J. & Courts, R. (2024) Postsecondary-offered Microcredentials in Ontario: What Does

43. The Evidence Tell Us? Higher Education Quality Council of Ontario

46. Statista (2025). Share of people with tertiary education in OECD countries in 2022, by country.

47. Lee, Soo & Jung, Hyejoo. (2021). Higher Education in the National Research System in South Korea.

48. World Bank. Retrieved from https://data.worldbank.org/country

49. OECD Economic Surveys 2023: Israel.

51. European Commission (2024). Country Reports: Slovenia.

52. Ibid.

53. Government of Canada (2022). Innovation Superclusters Initiative: Economic analysis final report.