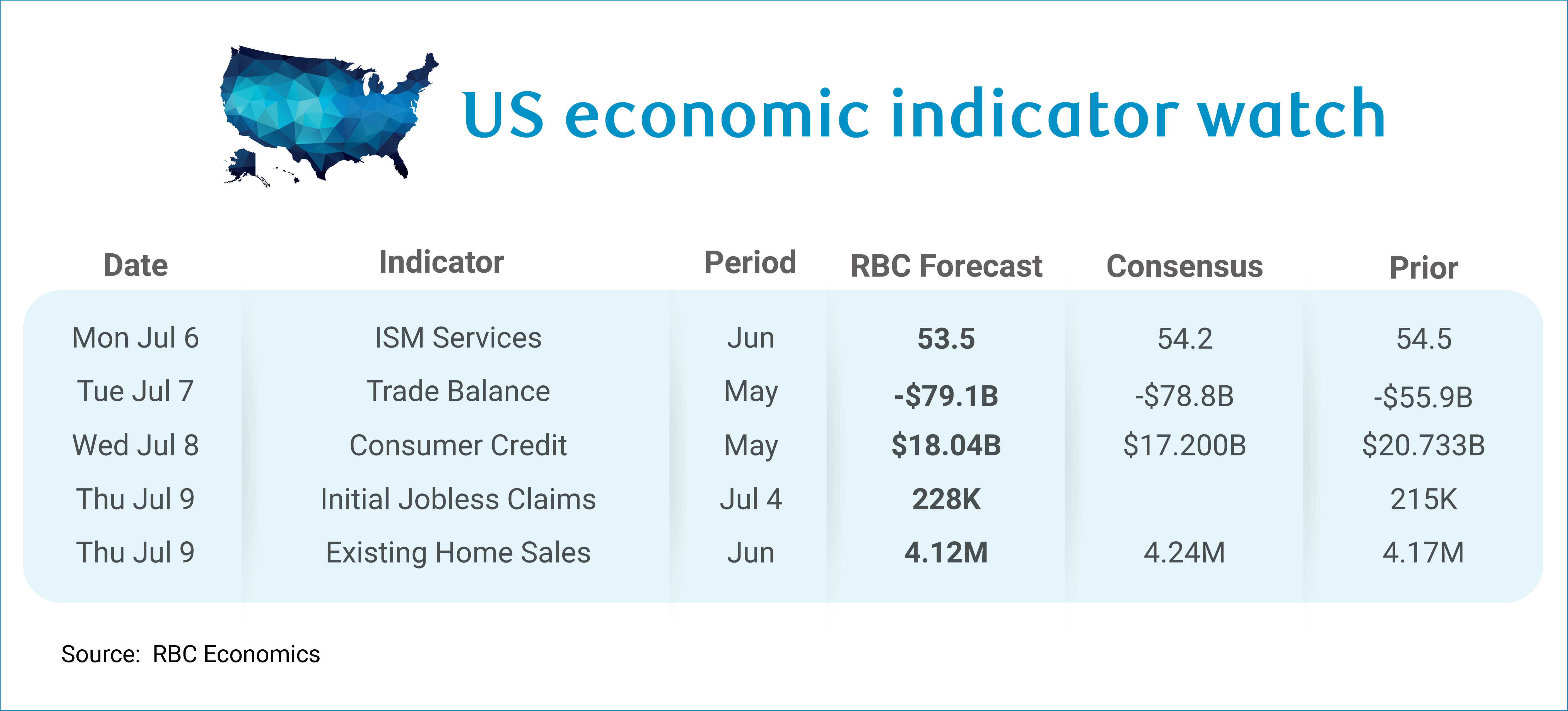

Next week we turn our attention back to trade data following the recent decision by the administaration not to renew USMCA. And we expect that the trade data for May will show a significantly wider (-$79.1 billion) trade deficit, which would mark the deepest deficit since Q1 2025.

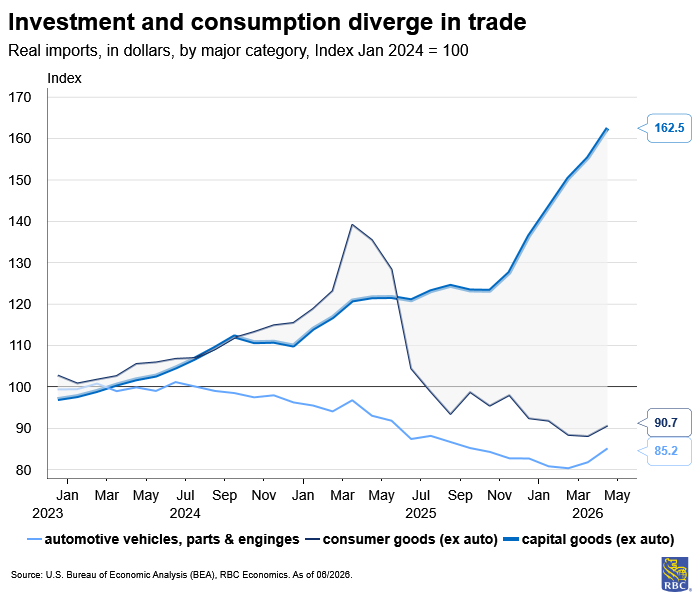

The Advanced goods report flagged a $105.8 billion goods deficit – a 14 month high – driven by a surge in consumer products, industrial supplies, and auto imports while exports fell. The trade deficit is still well-below pre-pandemic levels, moving in the wrong direction for an administration that has focused its agenda on closing the gap. But the composition of what’s driving the trade deficit matters and with AI demand surging, the deficit shows few signs of narrowing.

On the policy side, the landscape remains in flux. After SCOTUS overturned IEEPA in late February, the administration pivoted to blanket 10% tariffs on all global imports under Section 122, effective February 24th — but those are set to expire after 150 days (on July 24th). Congress can vote to extend tariffs under Section 122, but that is unlikely. As we wrote before, the administration has other options available to pursue their trade agenda, and there are numerous country-specific (under Section 301) and product-specific investigations (under Section 232) underway. But to date, tariffs haven’t delivered the deficit reduction for which they were intended. Part of what’s working against deficit reduction is the AI infrastructure buildout which continues to drive demand for capital goods. Just under 30% of goods imports are now computers and electronics products – double the share pre-2024. The April import surge was overwhelmingly a computers and electronic products story, and we expect that this will continue to be the case in May.

The manufacturing sector trade balance hit its lowest level ever after tariffs were imposed and remains deeply negative. While PPI for intermediate electronic components & accessories have soared as of late, upticks in capital goods imports is not exclusively a price story. Real capital goods imports rose +3.2% in April, suggesting that even stripping out price effects yields a material rise in real import volumes. A massive dip in the trade deficit in Q4 coincided with a significant uptick in real non-residential equipment investment. At the end of Q4, a sizeable dip in the trade deficit foreshadowed a massive uptick in real non-residential equipment investment in Q1. If computer and electronic product imports continue at the current pace through Q2, this would support another strong quarter for business investment. Indeed, tariffs are not curbing the appetite to support the buildout of AI infrastructure.

Here’s what else we’re watching next week:

-

We get ISM Services data on Monday and we expect the index will register 53.5 in June, reflecting an expansion in activity but at a slower pace from May. Only one of four regional Fed Surveys (Texas) pointed to a ramp up in the pace of services activity while others either expanded at a slower pace (Kansas City) or contracted? (Philly and Richmond Fed).

-

We expect to see Consumer Credit utilization increased by $18.04 billion in May from a likely uptick in revolving credit as consumers facing higher gas prices leaned on savings and credit to maintain consumption.

-

We forecast initial jobless claims (228k)are likely to show layoffs remained subded for the week ending July 4th.

-

Existing home sales data will likely show a slight decline in June as homebuyers sit on the sidelines after a jump in mortgage rates in May.

About the authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. She is responsible for generating RBC’s US economic forecasts across GDP, employment, and inflation, and providing macro commentary through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.