CUSMA has served as a critical backstop for Canada-U.S. trade amid the U.S. administration’s aggressive tariff stance. Product-specific measures (steel, aluminum, autos, lumber, etc.) have hurt Canada’s economy, but about 90% of U.S. imports from Canada have remained duty free largely thanks to CUSMA.

The pre-scheduled joint review of the agreement has drawn substantial attention, because of its significance. However, an important distinction is that while no agreement was reached on July 1 to extend CUSMA, the deal doesn’t expire until 2036, and tariff rates don’t change as a result.

Indeed, the renewal process built into CUSMA anticipated that extending the agreement could be politically challenging. Therefore, it requires all three parties to begin negotiating a decade before its 2036 expiry—a process that formally begins now.

Non-renewal isn’t a termination

Near-term trade risks for Canada haven’t gone away. Article 34.6 of CUSMA still allows any country to leave the agreement with six months’ written notice.

But, we continue to view the outright termination of CUSMA as unlikely if economic reasoning holds. Decades of free trade in North America have left industrial supply chains heavily integrated across borders, and exporters and importers in Canada, U.S. and Mexico with strong incentives to preserve the deal.

Indeed, in the proposed U.S. Section 301 measures set to replace expiring Section 122 tariffs later in July, CUSMA exemptions were preserved again.

U.S. tariffs that would replace CUSMA exemptions have gotten smaller

Losing CUSMA protections would still be a significant shock for the Canadian economy. But, in the (unexpected) event that the agreement were to end, the U.S. tariff rate that would replace duty free Canadian access has been getting smaller.

The U.S. Supreme Court decision in February against IEEPA tariffs didn’t significantly impact Canada, where most trade with the U.S. was already exempt under CUSMA. Should CUSMA lapse, however, U.S. imports from Canada will face 10% tariffs from current Section 122 (and proposed Section 301) tariffs compared to 35% previously under IEEPA measures.

Share of exports exempt from U.S. tariffs without CUSMA has increased

Outside of CUSMA exemptions, Section 122 tariffs in place include a separate list of exempted products that applies to all U.S. trade partners—measures largely replicated in proposed Section 301 tariffs.

By our count, this list covers about half of Canadian exports to the U.S. in the last 12 months, protecting them from U.S. tariffs regardless of CUSMA status. Also carved out are exports already subject to Section 232 tariffs, which will continue to be tariffed under that regime rather than Section 122/301.

That leaves about one-third of CUSMA-exempted exports vulnerable to a 10% tariff hike if the deal were to be terminated—not the (almost) 90% of Canadian exports currently crossing the border duty free.

Impact of (unexpected) CUSMA tear-up still significant for targeted sectors

Overall, without CUSMA protections, the average effective U.S. tariff rate on Canadian exports could rise to 6.6%—doubling from 3.2% in April, but it still ranks relatively low compared to major U.S. trade partners.

This offers little consolation to the subset of Canadian exporters that would be hit with higher tariffs. Currently, CUSMA exempted auto parts (HTS 87) would see the largest tariff increase (in dollar terms) if the agreement ended, followed by machinery and parts (HTS 84), plastics and articles (HTS 39), aluminum and articles (HTS 76) as well as wood products (HTS 44).

Some of these sectors already have a large proportion of production subject to Section 232 tariffs, but could still face more vulnerability as CUSMA protects a chunk of exports not targeted with Section 232 measures.

Still, the economic impact of a CUSMA termination today would not be as broad as it would have been under previous U.S. tariff rules.

Rules of Origin could come into focus during joint review

Our base case forecast assumes the more likely scenario: The joint review proceeds while CUSMA and related exemptions continue to function as is.

During the review, U.S. Congress’ role is not clearly defined. Significant changes to USMCA/CUSMA would likely require congressional approval. Alternatively, CUSMA countries can pursue side agreements to the deal to address bilateral trade irritants without legislative action.

What could come into focus are Rules of Origin (ROO) requirements, which generally establish a minimum North American production value threshold for goods to qualify for CUSMA treatment. These content rules serve as effective guardrails against transshipment—preventing goods from non-member countries to be routed through CUSMA partners to avoid tariffs.

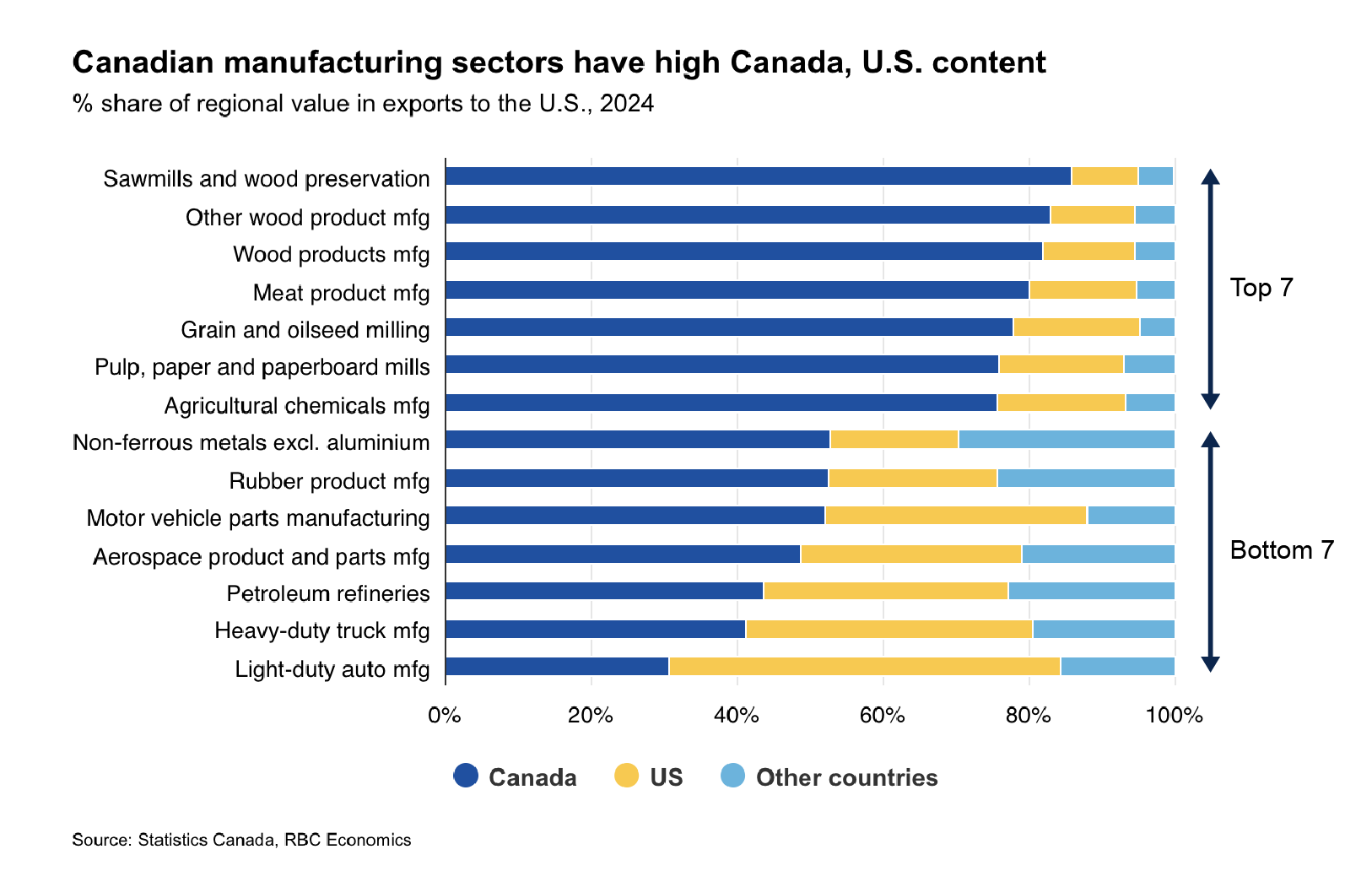

Most Canada-U.S. trade qualify (or exceed) ROO requirements

The reality is also that the bulk of Canadian trade flows with the U.S. already qualify for (or exceed) these requirements. Still, a push for increased North American or U.S. content during the joint review—the latter already embedded in Section 232 tariffs—could prove disruptive for businesses.

Using the latest value added in exports data, more than 90% of U.S. imports from Canada in 2024 had North American content: 73% Canadian-origin and 19% U.S.-origin. For manufacturing products, that share is slightly lower at 86%, though with higher U.S. content (58% Canadian-origin and 28% U.S.-origin).

Proposals to align with U.S. trade rules could also emerge

CUSMA already includes restrictions on any country signing a free trade agreement with a “non-market” economy—including China.

Still, the U.S. could take it one step further to require commitments from Canada and Mexico to police offshore trade and investment by including mechanisms such as coordinated trade restrictions and export control alignment similar to provisions in other U.S. trade agreements negotiated in the past year.

Strategic arrangements with the U.S. could constrain opportunities to expand and diversify Canada’s trade beyond North America, which broadly improved last year but remains limited. Excluding energy and gold, 72% of Canada’s goods exports in the last 12 months went to the U.S.—down from 76% a year ago.

Tariff exemptions and trade uncertainty likely to persist

Even in the best-case scenario of an immediate CUSMA renewal, trade uncertainties are unlikely to go away.

The U.S. administration has demonstrated both willingness and capacity to impose tariffs on top of free trade agreements as seen with Section 232 tariffs that overwrote CUSMA in product-specific cases last year.

Ultimately, we assume that neither the specifics of CUSMA nor the effectiveness of related exemptions will meaningfully change this year as a result of the joint review. Businesses seeking immediate resolutions will be disappointed, but the review remains relevant.

It will be the first such process for any U.S. free trade agreement, and will bear procedural importance in terms of scope, process, and legislative requirements that will establish precedents for similar reviews in the future, even if it yields little tangible change.

About the authors:

Claire Fan is a Senior Economist at RBC. She focuses on macroeconomic analysis and is responsible for projecting key indicators including GDP, employment and inflation for Canada and the US.

Nathan Janzen is an Assistant Chief Economist, leading the macroeconomic analysis group. His focus is on analysis and forecasting macroeconomic developments in Canada and the United States.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.