The Bottom Line:

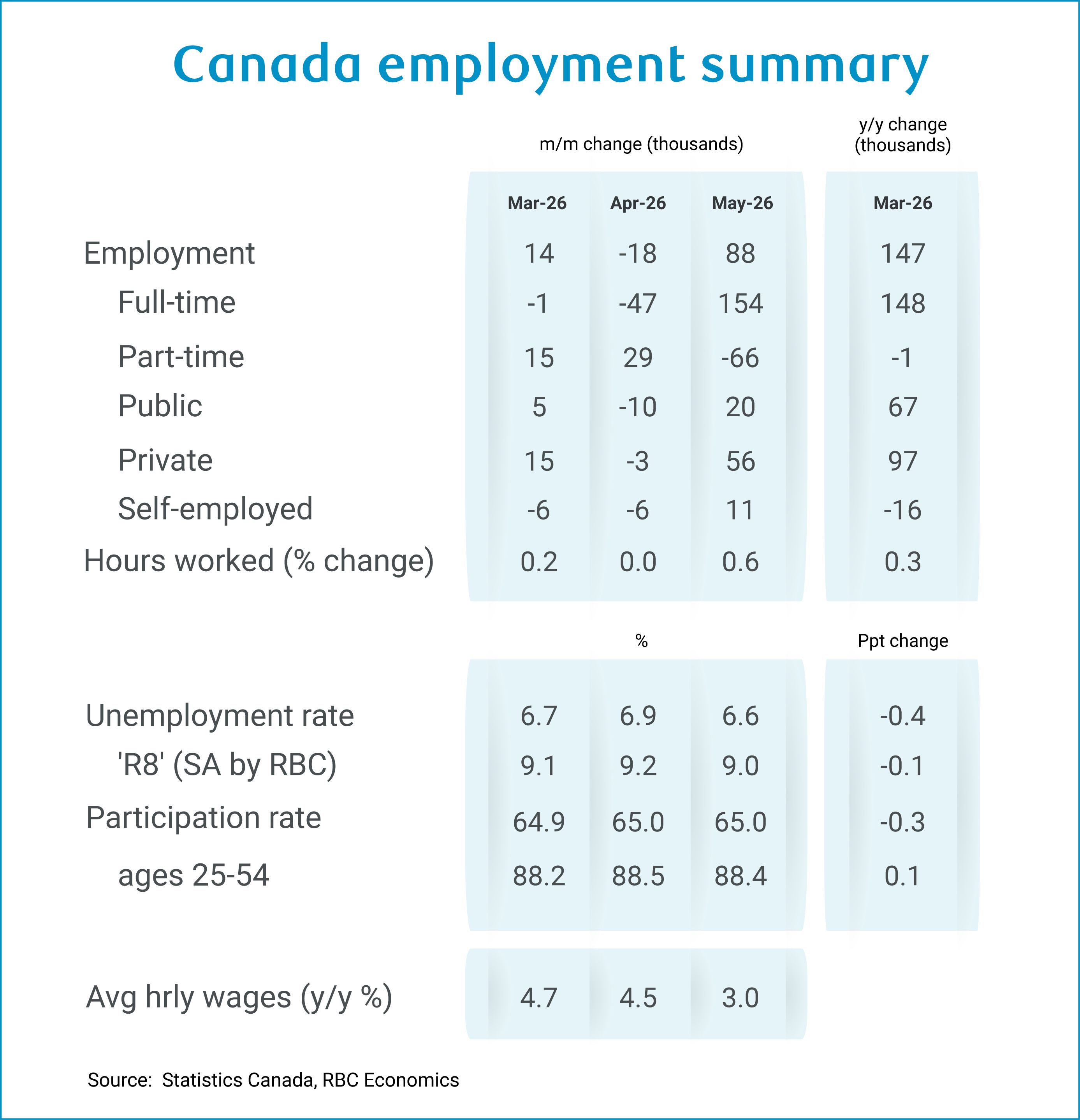

The larger-than-expected increase in employment (88k) and drop in the unemployment rate (to 6.6% from 6.9%) in May is a welcome upside labour market surprise after a surprisingly soft GDP report for Q1 last week raised concerns that the economic growth backdrop could be faltering.

The jump in employment in Canada in May was still just the second increase in the last five months, and still left the employment count down slightly year-to-date in 2026.

But we have argued before that a sharp slowing in population growth is distorting the comparison of employment growth relative to historical comparisons – ~26k workers retired per month over the last year, and caps on temporary resident arrivals are reducing the supply of workers available from abroad.

The sharp drop in the unemployment rate remains consistent with per-worker labour market conditions broadly continuing to improve since the unemployment rate peaked at a 7.1% rate in August/September of 2025.

Looking ahead, the economic growth backdrop still faces headwinds. Trade uncertainty remains ahead of negotiations to extend CUSMA this summer, and higher energy prices are cutting into household purchasing power. But we remain cautiously optimistic that per-person economic growth and labour market conditions will continue to gradually improve this year, with the unemployment rate edging broadly lower.

The details:

-

Employment jumped 88k in May following an 18k decline in April, with broadly positive underlying details.

-

Full time employment jumped by 154k with offset from a 66k drop in part-time positions.

-

On an industry basis, retail and wholesale employment fell by 35k (a fourth straight monthly decline) but the heavily trade sensitive manufacturing sector posted a 15k increase and construction employment bounced back 27k after falling 16k in April.

-

Public administration employment fell by 8k despite census hiring that usually shows up in May of census years. From separately-reported data, that hiring typically adds ~15k paid positions in May of census years.

-

The unemployment rate fell to 6.6% from the 6.9% rate in April—still slightly above the recent low 6.5% rate in January but below the 7.1% peak levels in 2025 and down 0.4 ppts from a year ago. The labour force participation rate was unchanged at 65.0%.

-

Critically layoffs continued to decline—this has been a persistent feature of the Canadian labour force in recent months, even when unemployment rates have increased it has been largely due to longer job searches for new labour market entrants rather than layoffs.

-

And there were some early signs of relief for hard-hit youth labour markets—the unemployment rate for 15-24 year olds is still high but fell to 13.4% in May from 14.3% in April in what is the first month of the typical student summer jobs market.

-

Hours worked jumped 0.6% in May—consistent with a pickup in GDP growth after the surprisingly weak Q1 GDP report.

-

Regionally, employment gains in May were broad-based across provinces. Ontario led with a 42,000 increase, marking the second consecutive monthly advance and bringing year-to-date cumulative gains to 15,000. The province’s unemployment rate declined 0.5 percentage points to 7.0%-the lowest since September 2024. Toronto’s jobless rate also fell to its lowest level (6.8%) since November 2023.

-

More broadly, employment gains were posted in British Columbia (25,000), Alberta (14,000), and Quebec (13,000), driving their unemployment rates lower. Alberta’s employment gains reached 104,000 year-over-year, the largest increase across all provinces.

-

Wage growth was one of the few soft spots in the May labour market data—but the slowing in average hourly earnings growth to a 3.0% rate (from 4.5%+ readings in each of the two prior months) is more consistent with a still elevated unemployment rate. The unemployment rate has begun to edge lower but is still elevated, and that should keep downward pressure on wage growth in the near-term.

About the author:

Nathan Janzen is an Assistant Chief Economist, leading the macroeconomic analysis group. His focus is on analysis and forecasting macroeconomic developments in Canada and the United States.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.