Pathways to 2030

Emissions from heavy industry such as steel, cement, chemicals and fertilizers have fallen 15% since 2005, but must drop another 31% by 2030.

Carbon abatement technologies vital to ensure chemicals sector emissions dropped 40% from 2005 levels.

The Year In Climate Policy

Alberta’s new ITC for CCUS projects gave a boost to the decarbonization of cement, chemicals and other heavy industries.

Ontario started developing a regulatory framework for CCUS after shunning the technology for years.

U.S.-based Dow Chemical Co. approved an $8.9 billion investment to build its Path2Zero facility in Fort Saskatchewan, Alberta.

Germany’s Heidelberg Materials and Ottawa signed a memorandum of understanding to develop the world’s first full-scale CCUS facility at the company’s Edmonton cement plant.

H2 Green Steel, a Swedish company, began talks with Ottawa to develop a $9-billion green steel facility in Quebec.

Canada's Chemical Sector Near Top Of Pack In Emissions Intensity

GHG emissions (Mt) per billion dollars of revenue

Source: CEFIC, StasCan, National Inventory Reports of Countries Specified, RBC CAI

Three Things To Watch In 2024

Dow Chemical will start work on its Path2Zero Net-Zero petrochemicals complex in Alberta.

Public consultations on the development of Ontario’s CCUS regulatory framework for large commercial projects begins.

UN treaty to end plastic pollution expected to be signed.

CASE STUDY

Emission As An Ingredient

Carbon Upcycling Inc.

Calgary, Alberta

THE SPARK

An immigrant who made Alberta his home, Apoorv Sinha has helmed Carbon Upcycling for a decade, focusing the company on the U of carbon, capture, utilization and storage (CCUS. It’s a relatively untapped, but ultimately lucrative market that could transform carbon emissions from a liability into an asset.

“I’m a chemical engineer by training, and I found the complexity and multi-faceted nature of the problem intriguing,” Sinha said.

THE CHALLENGE

Concrete is the second most used resource in the world and its primary ingredient, cement accounts for 8% of global emissions. The cement sector’s immense carbon footprint is a challenge, especially as it gears up to meet rising global infrastructure demands. The sector has struggled to rein in emissions as the cement making process requires immense energy and releases carbon emissions through an innate chemical reaction, hence its hard-to-abate reputation.

There are other complications. Making concrete requires fly ash or slag—byproducts of burning coal for power and steelmaking, respectively. As coal fired power reduces and steel manufacturing becomes less reliant on coal, cement companies are left scrambling to find the raw materials they need. At the same time, the industry is trying to lower its emissions footprint.

THE SOLUTION

Carbon Upcycling targets both problems by reimagining waste—blending carbon emissions from cement manufacturing with waste materials like mine tailings to create new materials that replace cement, enhance the performance of concrete and store carbon emissions in perpetuity.

The technology is a full-stack carbon capture and carbon avoidance solution that helps companies 60 reduce waste and CO2 emissions by up to 60% at full scale, while ensuring they have the materials they need. Carbon Upcycling is currently working with leading cement manufacturers like CRH and Cemex to deploy their technology in commercial projects.

The company’s carbon utilization technology is also being deployed in a wide range of consumer products. Carbon Upcycling’s consumer brand, Oco, sequesters CO2 into solid material that can replace carbon-intensive incumbents in products including inks, yoga mats, 3D printing filament among others. Oco also recently announced a pilot with Adidas, which will see 400,000 pairs of shoes using its carbon-captured ink.

WHAT’S NEEDED

Carbon Upcycling was founded a decade ago but raised its first venture capital round in 2022—an anomalously long timeline for a startup. Critical early-stage funding, while the company was still developing the core chemistry behind its technology, came from provincial and federal agencies like Emissions Reduction Alberta, Alberta Innovates, National Research Council Canada and Natural Resources Canada.

The team, which has grown to 30-strong, is now focused on commercializing its technology and implementing it in partnership with large cement companies. Sinha cites this federal and provincial government early-stage support and engineering capability as key strengths for Canadian clean technology.

The company has won awards at federal and provincial innovation competitions, and earned millions in capital from U.K.-based Climate Investment, U.S.-based Clean Energy Ventures, and Canada’s BDC Climate Tech Fund. Still, there are challenges. Often the Canadian government’s early-stage support for a startup fades as the company ramp up, leaving the firm vulnerable just as it’s poised for a growth spurt. In addition, private Canadian investors did not appear to be as eager to buy into Sinha’s desire to make a global splash. “American investors, or even European investors, see a much bigger picture, a much bigger addressable market. And they’re willing to bet on a global scale.”

Sinha’s biggest concern is that Canada, which has punched above its weight globally in clean technologies like CCUS, could lose momentum. Canada has no CCUS projects commissioned to go online between now and 2027. “We have had a few successes in the past in Quest, Alberta Carbon Trunk Line, and Boundary Dam. But we have nothing we can point to and say that is going online. We’re going to lose because others will catch up on CCUS.”

WHAT’S NEXT

Carbon Upcycling is poised to tackle the sector’s carbon challenge as it prepares to execute a commercial project very close to home—Ash Grove North’s Mississauga cement plant, in Ontario, the largest in Canada. The company is developing a similar project in the U.K., at Cemex’s Rugby cement plant near Birmingham, England. Emerging markets also present a massive opportunity to store carbon in products.

“There isn’t much of a global hub of hardware companies in clean technology that have been able to become highly successful,” Sinha has found. “I think Calgary is moving quite quickly and is one of the top five locations to do this kind of work.”

Deep Dive

Green Chemicals

- Chemicals and fertilizer emissions have fallen 28%. Ontario facilities’ switch to cleaner and cost-effective natural gas liquids have sent emissions tumbling over three decades.

- New tech is needed for further cuts. Carbon capture and clean hydrogen technologies deployment, along with novel manufacturing processes, would drive emissions reduction.

- Canada can emerge as a low-carbon chemicals magnet. Cheap and abundant natural gas, competitive carbon policies, and clean technology infrastructure could attract green dollars.

- Alberta can capitalize on its strengths. The province’s natural gas resources, incentives, and infrastructure could transform it into a global petrochemical hub.

- Lean on the circular economy to cut emissions. Plastic recycling could cut volumes of new plastics manufactured and avoid additional emissions.

From food to fabrics, chemicals are a constant feature of modern life. As building blocks of fertilizers and plastics, mascara tubes, batteries and Barbie dolls, they serve a vital function in our everyday lives and across the economy. Chemicals and their derivatives like plastics, pharmaceuticals, and fertilizers have enabled our high living standards and economic prosperity. Chemicals is the fourth largest manufacturing sector in the country, generating over $68 billion in economic activity1. The chemical and fertilizer sector also accounts for 3% of Canada’s GHG emissions.

Chemical manufacturers need to re-think how their products are made with growing demand for their goods and the imperative to decarbonize.

They also have a surprising environmental story to tell. The sector’s emissions are down 28% over the past three decades as Ontario-based facilities switched feedstock from oil to the cleaner and cost-effective natural gas liquids from the Marcellus shale formation in Pennsylvania2.

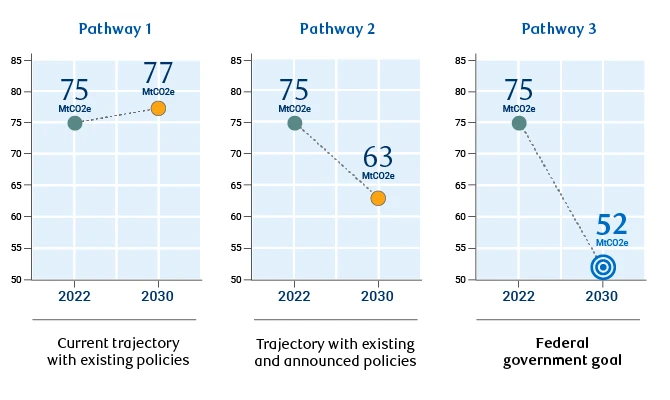

Emissions from the chemicals sector could drop much further to 15 million tonnes by 2030, realizing a 40% reduction from 2005 levels, according to Canada’s Emissions Reduction Plan (ERP) modelling.3 That requires a reduction of 750,000 tonnes per year—three times the average annual reductions since 2005.

But progress has stalled over the past decade as gains from feedstock switching and energy efficiency began to slow. Combustion emissions—produced when natural gas is burned to sustain the high-temperature processes that make simple chemicals—is the only heavy industry segment that has seen emissions tick up since 2005, rising by 13%.4 Process emissions, a byproduct of the manufacturing process, have stayed near constant over the same time and are struggling to be contained as demand for chemicals continues to rise.

Further emissions reductions are now colliding with the industry’s focus on meeting rising domestic and global demand. The challenge is daunting, but there is also opportunity. Canada could emerge as a centre for clean chemical manufacturing, thanks to cheap and abundant natural gas, clean electricity, competitive incentives, and carbon management infrastructure.

Chemical Emissions Are Falling

Left: Chemical Manufacturing Emissions in ktCO2e; Right: Stationary combustion emissions, ktCO2e

Source: National Inventory Report, Canadian Climate Institute, RBC Climate Action Institute

Now Comes The Hard Part

Canada’s chemicals industry is relatively clean compared to other countries in fuel use. About 30% of the industry’s final energy comes from electricity and 63% from natural gas,5 positioning it favourably against countries like Germany and China that rely heavily on crude oil6 and coal7 for feedstock and fuel.

Approximately 75% of emissions from Canada’s chemicals and fertilizer sector comes from the manufacturing of petrochemicals (that help make food packaging), industrial gases like CO2 and hydrogen (the building blocks of fertilizers), and the manufacture of those fertilizers (used for boosting crop yields).8 And it’s all high intensity—temperatures must reach 800 to 900oC9 to make ethylene, a basic chemical used to make plastics, which only fossil fuels can power.

Reducing these emissions will need Canadian manufacturers to deploy carbo, capture, utilization and storage (CCUS) at large scale and replace current hydrogen manufacturing with low-carbon methods like electrolysis, or by retrofitting CCUS to existing facilities in areas where geological conditions and renewable energy supply enable these technologies to scale. Drawing the investment necessary to build such projects is a key challenge.

The next phase of decarbonization will be harder still as it requires new manufacturing processes and technologies like novel catalysts to allow chemical reactions to happen at lower temperatures, biomass for fuel, and chemical recycling being implemented. The costs of these technologies could erode chemicals’ razor-thin margins in global commodities markets. Also, the long timelines required for CCUS and large-scale hydrogen projects to be constructed will push deep emissions cuts into the 2030s.

Canada’s Chemical Manufacturing Powered By Relatively Cleaner Sources

Source: Statistics Canada to StatsCan

Offsetting these challenges, Canada’s advantages include cheap and abundant natural gas, competitive carbon policies, and clean technology infrastructure like CO2 pipelines, which could help attract new investments as chemical buyers push their suppliers to cut emissions. But such investments may require further government support. In just two years since 2021, the U.S. has seen around 68 new hydrogen and CCUS projects dedicated to chemical manufacturing announced with 10 more in Canada over the same time.10

Petrochemicals And Fertilizers Emit The Most Within The Chemicals Sector

Sum of Total Emissions (tonnes CO2e), 2021

Source: RBC Climate Action Institute, Canada GHG Reporting Program

Canada And The U.S. In Race For Clean Chemical Dollars

Announced project count

Source: Bloomberg NEF, RBC Climate Action Institute

Alberta Advances, Ontario Lags

In just a few years, Alberta has seized on the potential in petrochemicals to produce more by helping companies cut emissions, and has already attracted investors. The Alberta Petrochemicals Incentive Program, alongside ITC for CCUS introduced by the federal government helped catalyze the development of Dow Chemical’s $9 billion Net Zero ethylene cracker11 and derivatives complex and Air Products’ $1.6 billion Net Zero hydrogen complex12.

Ontario, Canada’s other main chemicals sector, has fewer decarbonization options—for now. The province’s long-standing ban on CCUS, which was rooted in its effort to phase out coal-fired power, was reversed only in early 2023. The province is currently developing a regulatory framework for test and demonstration CCUS projects, which will eventually pave the way for commercial-scale deployment. Ontario’s hydrogen production is also in its nascent stages. Although plans for industrial-scale hydrogen hubs in Sarnia are advancing, the province’s current clean hydrogen production is less than 500 tonnes per year and is not dedicated for industrial decarbonization such as steel, chemicals and cement.13

Another opportunity could be through recycling chemicals as the province’s population—and plastics consumption—continues to grow. Companies are already exploring the possibilities including Calgary-based Nova Chemicals and U.K.-based Plastic Energy, which are studying the feasibility of a 66,000 metric tonnes (MT) advanced chemical recycling facility in Sarnia that could reduce the need to produce virgin plastic.14

More efforts to reduce the manufacturing of virgin plastic will need new policies and investments. British Columbia has led the country in implementing extended producer responsibility programs that place the onus of recycling on manufacturers and extended producer responsibility programs are in development across several provinces.

Canada’s Chemical Emissions Are Centered In Alberta And Ontario

Source: National Inventory Report, RBC Climate Action Institute

The prize is big. Canadians consumed 6.2 million metric tonnes of plastic in 2019, equivalent to 78 years of Lego production, and released 43,000 tonnes into the environment, and produced 402,000 tonnes (about 7% of total consumption) of recycled plastic flakes and chips that could be turned back into plastic products. The key will be to improve cleaning and pre-processing of plastic waste to prepare it for recycling. Only 11% of discarded plastic in Canada was ready for recycling in 2019.15

CLIMATE ACTION HERO

Hydrogen Optimized

Andrew Stuart is the CEO of Hydrogen Optimized and a third-generation hydrogen technologist. The Owen-Sound-based company, Andrew says, is developing electrolyzers, a type of clean technology that could take the world’s most difficult-to-decarbonize industries closer to Net Zero by generating clean hydrogen—expected to be a US$1.4 trillion market by 2050.

Important Notice Regarding Information on this Website and Caution Regarding Forward-Looking Statements

The information on the Climate Action Institute website is intended as general information only and does not constitute an offer or a solicitation to buy or sell any security, product or service in any jurisdiction; nor is it intended to provide investment, financial, legal, accounting, tax or other advice, and such information should not to be relied or acted upon for providing such advice. Nothing herein shall form the basis of or be relied upon in connection with any contract, commitment, or investment decision whatsoever. The reader is solely liable for any use of the information contained herein, and neither Royal Bank of Canada and its subsidiaries (“RBC,” “we,” “us,” or “our”) nor any of RBC’s affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damage arising from the use of any information contained herein by the reader.

From time to time, we make written or oral forward-looking statements within the meaning of certain securities laws, including on this website, in filings with Canadian securities regulators or the U.S. Securities and Exchange Commission and in other communications. Forward-looking statements on our websites include, but are not limited to, statements relating to our economic, environmental (including climate), social and governance-related objectives, vision, commitments, goals and targets as well as potential events and actions. By their very nature, forward-looking statements require us to make assumptions and are subject to inherent risks and uncertainties, which give rise to the possibility that our predictions, expectations or conclusions will not prove to be accurate, that our assumptions may not be correct, and that our objectives, vision, commitments, goals and targets will not be achieved. We caution readers not to place undue reliance on these statements as a number of risk factors – many of which are beyond our control and the effects of which can be difficult to predict – could cause our actual results to differ materially from the expectations expressed in such forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest Climate Report, available at our ESG Reporting site.

Except as required by law, none of RBC or any of its affiliates undertake to update any information on this website.

All expressions of opinion on this website reflect the judgment of the authors as of the date of publication and are subject to change. We do not guarantee the accuracy of the information or expressions of opinion presented herein and they should not be regarded as a complete analysis of the subjects discussed. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by RBC or any of its affiliates.

All references to websites are for your information only. The content of any websites referred to on this website, including via website link, and any other websites they refer to are not incorporated by reference in, and do not form part of, this website. This website is also not intended to make representations as to ESG-related initiatives of any third parties, whether named herein or otherwise, which may involve information and events that are beyond our control.