-

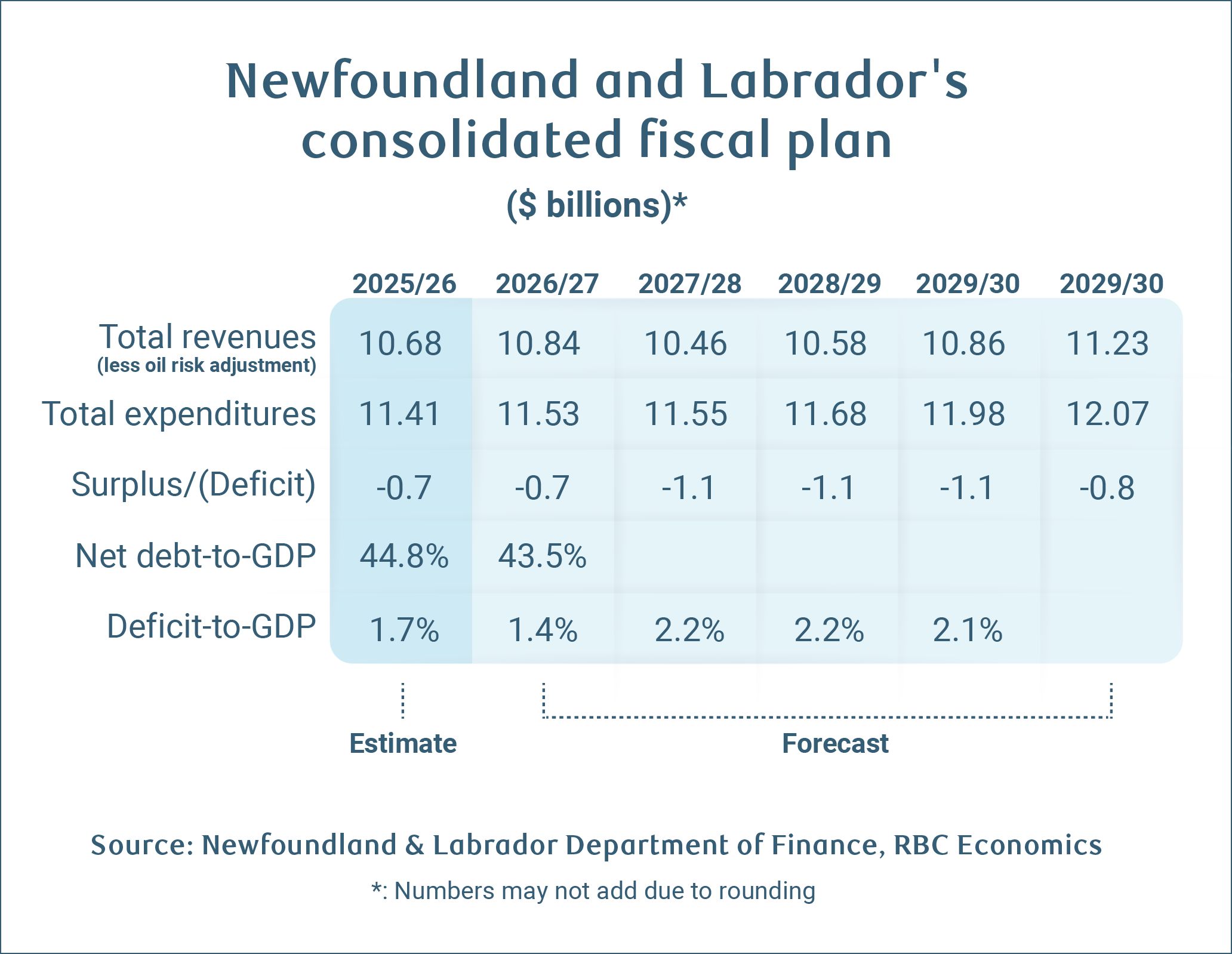

Newfoundland and Labrador projects a $688 million shortfall (1.4% of GDP) in 2026-27, with no plans for balance over the fiscal planning period.

-

The 2025-26 bottom line deteriorates sharply to $729 million—nearly double Budget 2025’s projection and 2.5 times larger than the prior year—driven almost entirely by higher-than-expected Social Sector spending.

-

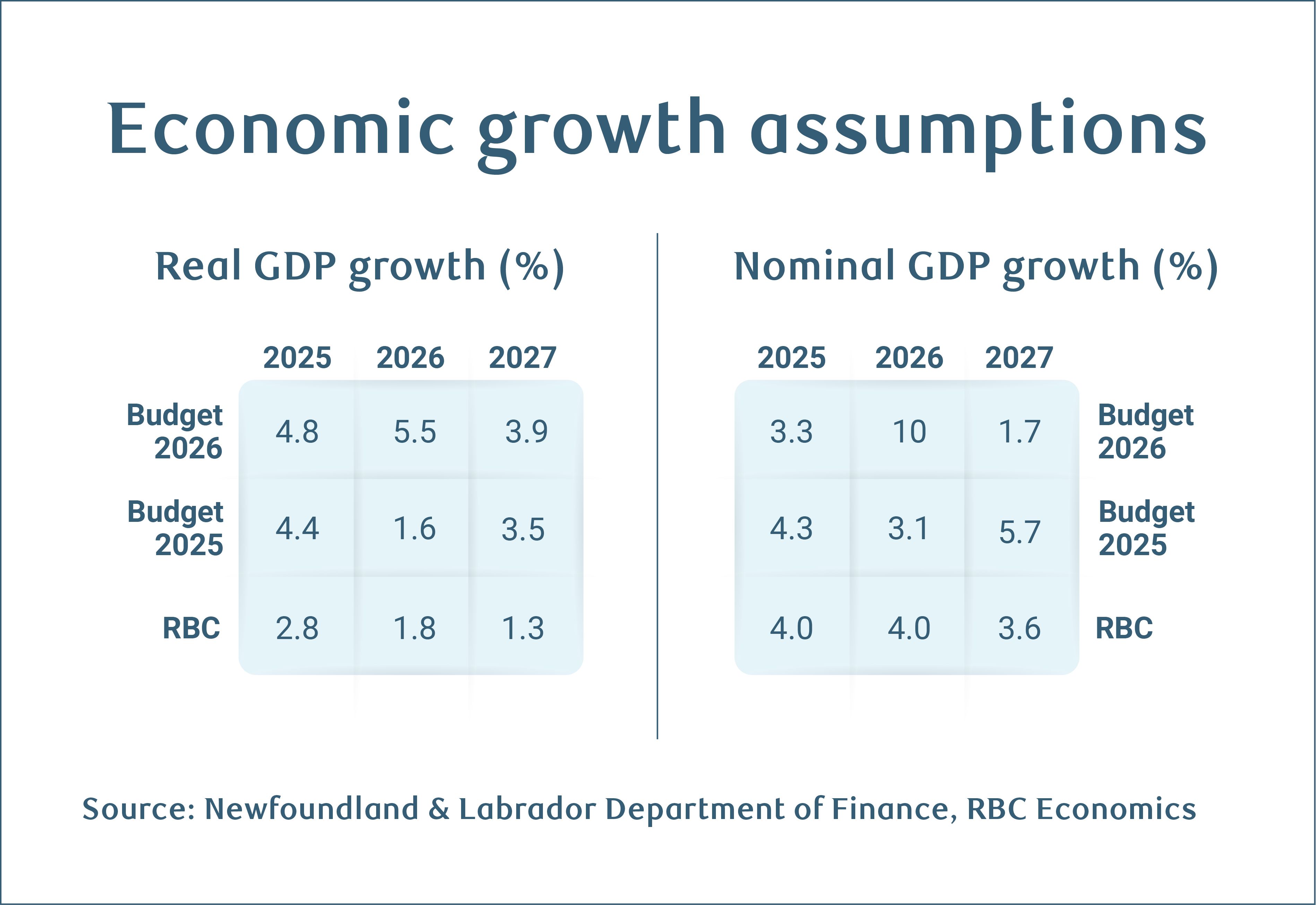

The province projects nominal GDP growth of 10% in 2026, driven by stronger oil and mining export value.

-

The improved economic backdrop will marginally narrow the net debt-to-GDP ratio to 43.5% in 2026-27, but this still leaves Newfoundland and Labrador with the highest debt burden of the provinces.

Newfoundland and Labrador is the latest province to scratch out its plans for balance and show deficits over the entire course of the fiscal plan—a shift that’s particularly troubling given the upward revisions to the economic growth outlook, which typically strengthen a government’s fiscal position.

The province’s deficit for 2025-26 is expected to reach $729 million—nearly double Budget 2025’s projection and two and a half times the prior year’s deficit. The deterioration stems largely from higher-than-anticipated spending in education and health—key campaign commitments from the new government.

But the fiscal decline didn’t emerge suddenly. The province’s December update had already signalled a $948 million deficit for 2025-26, driven partly by a downward revision to oil prices to US$66 per barrel, from the $73 assumption in Budget 2025.

Moving forward, deficits are set to deepen medium-term. Spending is expected to remain on a higher track as expenditures grow modestly—rather than fall outright in the current and subsequent two fiscal years, as previously planned.

Revenues are targeted to grow this fiscal year (2026-27) before dropping 3.5% in 2027-28 to accommodate new measures including:

-

Increasing the basic personal amount exempt from income tax to $15,000.

-

Increasing the Newfoundland and Labrador Seniors’ Benefit by 20% effective July 1st.

-

Reduction in the Small Business Tax rate to 1.5% from 2% effective January 2027, then to 1% effective January 2028.

Additionally, potential revenue from a deal to develop the Upper Churchill and Gull Island have been removed from the budget, contributing to lower revenues over the course of the fiscal plan. A Memorandum of Understanding regarding the development of these hydroelectric projects has been referred to an Independent Review Committee, which is expected to deliver its final report on April 30.

Should the committee’s findings support proceeding with the development, we’d likely see a substantial increase in projected revenues in the next fiscal update.

Improved growth outlook rests on stronger oil and mining sectors

The 2026 budget projects nominal GDP to expand by a whopping 10%—substantially above consensus forecasts, which cluster around 5%.

Upgrades to the economic backdrop reflect a stronger outlook for the oil and mining sectors. Higher oil prices—Brent crude is assumed to be US$81.10 per barrel or 13% higher in 2026 compared to Budget 2025’s assumption—and rising oil production from the West White Rose field is commencing in the second half of the year, alongside the first full year of production from the Valentine and Hammerdown gold mines will supercharge the province’s resource output. Together, these developments are expected to boost royalties and mining taxes.

The 10% nominal GDP projection may not be farfetched considering Newfoundland and Labrador posted 20% nominal growth in 2021, the last time oil prices soared.

Though materially higher than our own assumptions, the province’s outlook reflects more recent information on the Middle East conflict, which emerged only days before publication of our most recent provincial forecast.

Material downside risks remain, however. Trade policy uncertainty and commodity price fluctuations could dampen growth and revenues, widening deficits if projections miss.

Spending cuts shelved as government abandons deficit reduction plan

Last year, we noted that the government’s plan to achieve budget balance by 2026-27 hinged on their plan to cut spending by 3.1% and holding that line through the end of the decade—a tall order given Newfoundland and Labrador has recorded only two year-over-year spending declines in the last twenty years. We cautioned that if the government failed to execute these cuts, deficits would deteriorate significantly—which is precisely what’s playing out.

Budget 2026 abandons plans to reduce expenditures and now projects a 1.1% ($120 million) increase in 2026-27 as well as modest expenditure growth over the remainder of the fiscal plan. This will keep spending above the $11 billion mark for the entire forecast period.

Higher spending will stem entirely from the General Government Sector in 2026-27—which is slated to grow 11% to $2.8 billion. Cuts to the Resource (-2%) and Social (-2%) sectors—including a 4% ($188 million) drop in Healthcare and community services spending—won’t be enough to offset the increase.

Debt burden remains the heaviest in Canada despite GDP upgrade

By our calculation, Newfoundland and Labrador’s net debt burden is projected to narrow marginally to 43.5% of GDP in 2026-27.

The sizable upgrade to the province’s GDP forecast has tempered what would’ve otherwise been a more dramatic deterioration in the province’s net debt position. Newfoundland and Labrador will continue to hold the highest net debt-to-GDP ratio of any province, making it the least fiscally flexible to buffer the economy from new shocks or respond to economic headwinds should they arise.

About the Author:

Rachel Battaglia is an economist at RBC, providing forecasts for the Canadian provincial economies and analyzing key trends in housing and consumer spending.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.