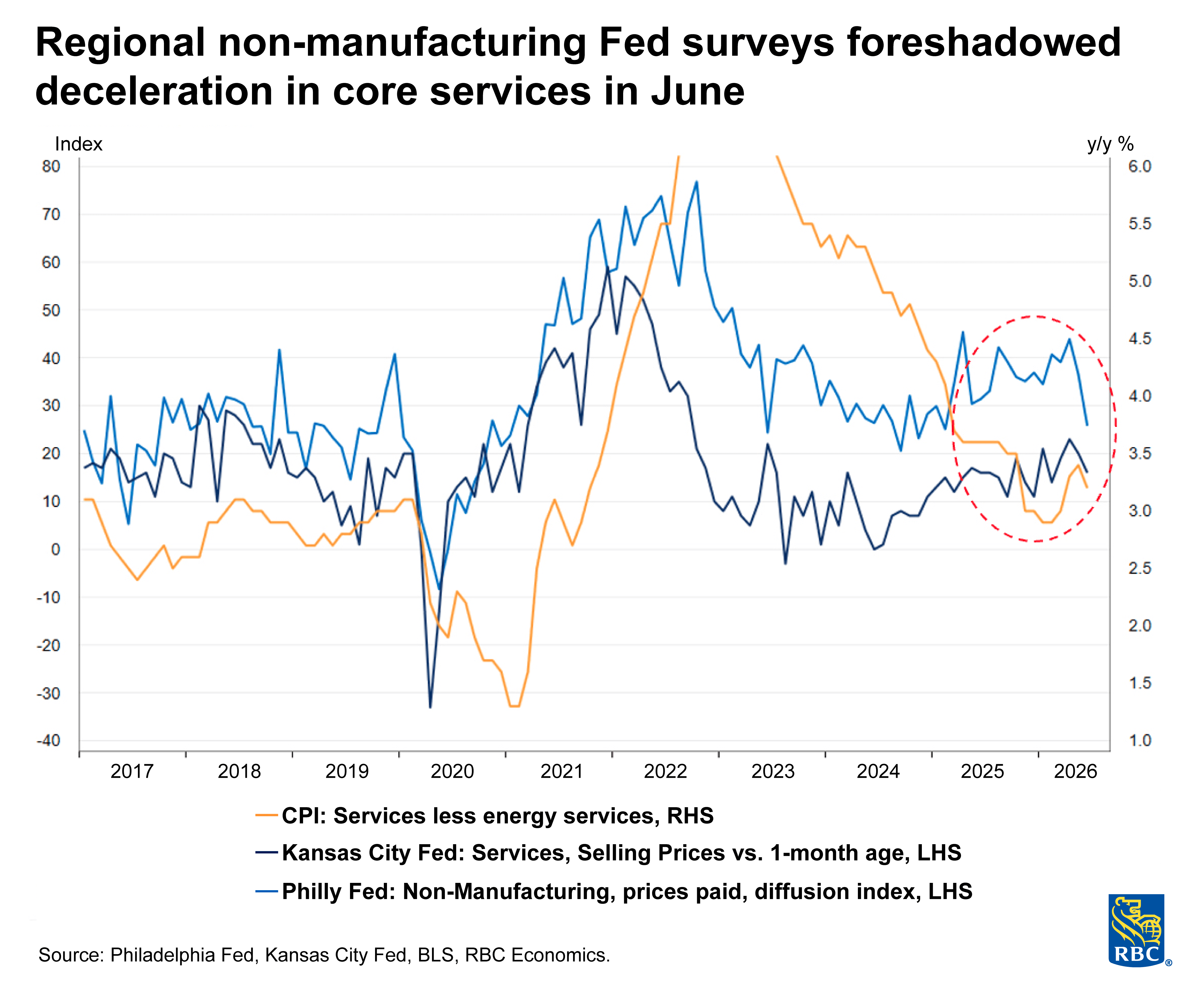

Next week is a quiet one following a deluge of inflation and consumer data. In the absence of major data releases, we will be closely watching the July releases of the regional Federal Reserve Bank surveys for early indications of price pressures and whether demand is holding up.

We recently upgraded our 2026 outlook — but the re-escalation of the conflict with Iran presents a downside risk. We will be looking for signs in these surveys to gauge how businesses are reacting to oil prices moving higher following a brief reprieve. Oil prices have hovered around $80/bbl, up from the $70 trough post-MOU. While this represents a meaningful improvement from the near- $100/bbl peak, oil prices have still risen nearly +30% relative to before the Middle East conflict base case in February.

June marked a notable downside surprise to core CPI, and core PPI pressures moderated meaningfully. One month does not make a trend, but it buys the FOMC time. We remain optimistic that peak tariff passthrough has likely already occurred, with the exception of product-specific Section 232 tariffs. If regional Fed surveys continue to suggest acute price pressures abating into July, this would further protect against a demand-driven inflation spike.

Consumer momentum continues to paint a robust picture if June retail sales are any indication. Regional manufacturing and non-manufacturing indices will offer some insight into business activity heading into the summer months. We continue to expect consumer momentum to moderate in the back half of the year but AI capex remains robust.

Here’s what else we’re watching next week:

-

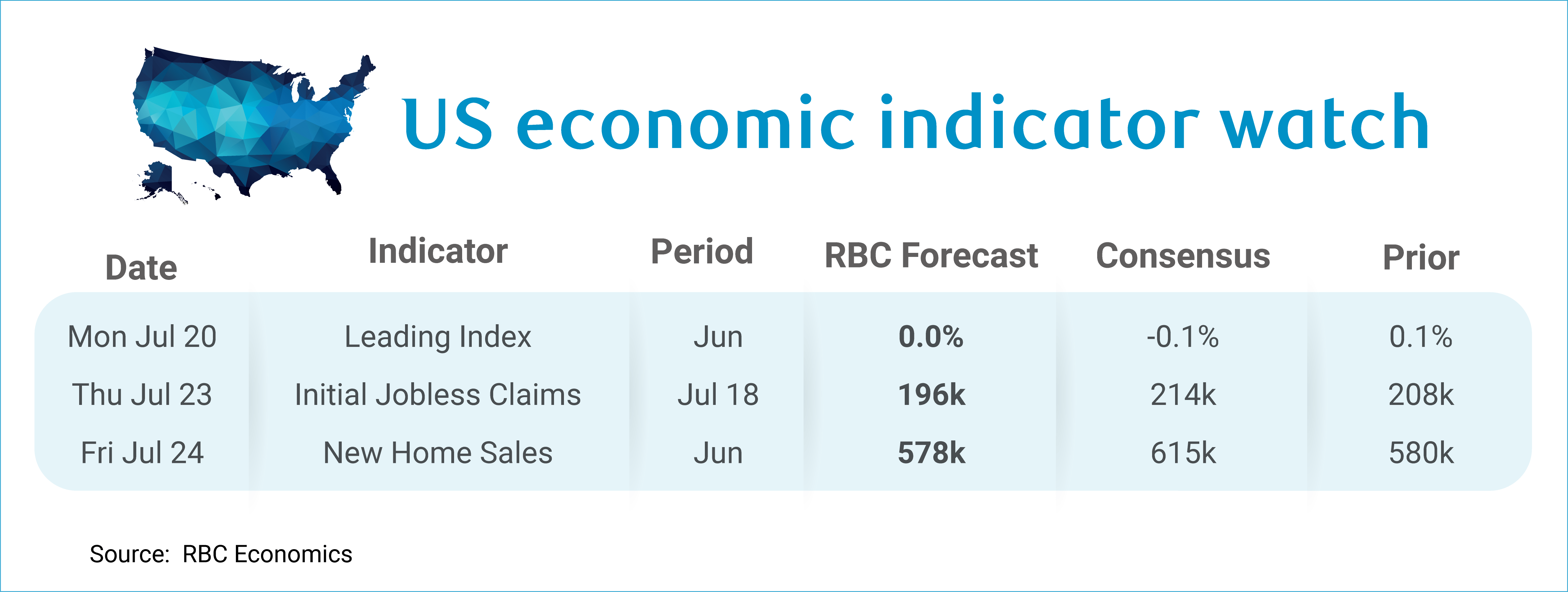

We expect to see the Conference Board’s Leading Economic Index (LEI) report flat (0.0% m/m) in June after a mixed bag of monthly data. Weekly hours worked in manufacturing declined and the OFR Financial Stress Index deteriorated alongside the ISM Manufacturing new orders index. But the S&P500 improved alongside consumer expectations and jobless claims remained low.

-

Initial Jobless Claims will likely tick lower yet again (we expect to 196k) for the week ending July 18th after a sizeable downside to claims the week prior.

-

New home sales are expected to tick down slightly (to 578k) after mortgage applications declined month-over-month.

About the authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. She is responsible for generating RBC’s US economic forecasts across GDP, employment, and inflation, and providing macro commentary through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.